URBAN AIR MOBILITY Confidentiality, Forward Looking Statements and Non-Reliance

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

My Personal Callsign List This List Was Not Designed for Publication However Due to Several Requests I Have Decided to Make It Downloadable

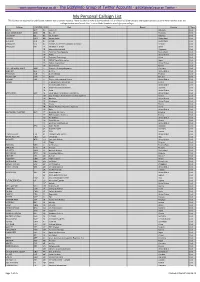

- www.egxwinfogroup.co.uk - The EGXWinfo Group of Twitter Accounts - @EGXWinfoGroup on Twitter - My Personal Callsign List This list was not designed for publication however due to several requests I have decided to make it downloadable. It is a mixture of listed callsigns and logged callsigns so some have numbers after the callsign as they were heard. Use CTL+F in Adobe Reader to search for your callsign Callsign ICAO/PRI IATA Unit Type Based Country Type ABG AAB W9 Abelag Aviation Belgium Civil ARMYAIR AAC Army Air Corps United Kingdom Civil AgustaWestland Lynx AH.9A/AW159 Wildcat ARMYAIR 200# AAC 2Regt | AAC AH.1 AAC Middle Wallop United Kingdom Military ARMYAIR 300# AAC 3Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 400# AAC 4Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 500# AAC 5Regt AAC/RAF Britten-Norman Islander/Defender JHCFS Aldergrove United Kingdom Military ARMYAIR 600# AAC 657Sqn | JSFAW | AAC Various RAF Odiham United Kingdom Military Ambassador AAD Mann Air Ltd United Kingdom Civil AIGLE AZUR AAF ZI Aigle Azur France Civil ATLANTIC AAG KI Air Atlantique United Kingdom Civil ATLANTIC AAG Atlantic Flight Training United Kingdom Civil ALOHA AAH KH Aloha Air Cargo United States Civil BOREALIS AAI Air Aurora United States Civil ALFA SUDAN AAJ Alfa Airlines Sudan Civil ALASKA ISLAND AAK Alaska Island Air United States Civil AMERICAN AAL AA American Airlines United States Civil AM CORP AAM Aviation Management Corporation United States Civil -

Aviation Human Factors Industry News January 11, 2007 NTSB

Aviation Human Factors Industry News January 11, 2007 Vol. III, Issue 02 NTSB Updates Status Of Recent Investigations # 1: US National Transportation Safety Board said it will investigate a Friday morning runway incursion incident at Denver International Airport in which a Frontier Airlines A319 was forced to execute a missed approach in order to avoid a Key Lime Air Swearingen Metroliner that "inadvertently" entered the runway. The aircraft missed each other by 50 ft., NTSB said. The Airport Movement Area Safety System alerted the tower at the same time that the Frontier pilots spotted the Metroliner. # 2: Holidays Saw 12 Fatal GA Accidents. National Transportation Safety Board Chairman Mark V. Rosenker said last week that, during the recent 12-day holiday period between December 22, 2006 and January 2, 2007, he dispatched regional air safety investigators to 12 fatal general aviation accidents. These accidents resulted in a total of 31 fatalities. Pilots in Mo. crash went on a joy ride WASHINGTON — Federal crash investigators Tuesday blamed a pair of joking pilots who flouted safety rules for a 2004 crash in Missouri that highlighted shortcomings in training and safety oversight at regional airlines. Capt. Jesse Rhodes, 31, and co-pilot Peter Cesarz, 23, died when Pinnacle Airlines Flight 3701 crashed 2½ miles short of an airport in Jefferson City, Mo., on Oct. 14, 2004, after losing power in both engines. The pilots of the Bombardier CRJ-200, who were moving the jet from Little Rock to Minneapolis with no passengers aboard, repeatedly violated company safety rules, the National Transportation Safety Board (NTSB) said. -

URBAN AIR MOBILITY Additional Information and Where to Find It

URBAN AIR MOBILITY Additional Information and Where to Find It Experience Investment Corp. (the “Company”) intends to file with the U.S. Securities and Exchange Commission (“SEC”) a Registration Statement on Form S-4 (the “Form S-4”), which will include a preliminary proxy statement/prospectus in connection with the proposed business combination (the “Merger”) and will mail a definitive proxy statement/prospectus and other relevant documents to its stockholders. EIC’s stockholders and other interested persons are advised to read, when available, the preliminary proxy statement/prospectus, and amendments thereto, and the definitive proxy statement/prospectus in connection with EIC’s solicitation of proxies for its stockholders’ meeting to be held to approve the Merger because the proxy statement/prospectus will contain important information about EIC, Blade Urban Air Mobility, Inc. (“Blade”) and the Merger. The definitive proxy statement/prospectus will be mailed to stockholders of EIC as of a record date to be established for voting on the Merger. Stockholders will also be able to obtain copies of the Registration Statement on Form S-4 and the proxy statement/prospectus, without charge, once available, at the SEC’s website at www.sec.gov or by directing a request to Experience Investment Corp., 100 St. Paul St., Suite 800. Denver, CO 80206 or [email protected]. Participants in the Solicitation EIC, Blade and certain of their respective directors and officers may be deemed participants in the solicitation of proxies of EIC’s stockholders with respect to the approval of the Merger. EIC and Blade urge investors, stockholders and other interested persons to read, when available, the Form S-4, including the preliminary proxy statement/prospectus and amendments thereto and the definitive proxy statement/prospectus and documents incorporated by reference therein, as well as other documents filed with the SEC in connection with the Merger, as these materials will contain important information about Blade, EIC and the Merger. -

Developments in Norwegian Offshore Helicopter Safety Final

Developments in Norwegian Offshore Helicopter Safety Knut Lande Former Project Pilot and Chief Technical Pilot in Helikopter Service AS www.landavia.no Experience Aircraft Technician, RNoAF Mechanical Engineer, KTI/Sweden Fighter Pilot, RNoAF Aeronautical Engineer, CIT/RNoAF Test Pilot, USAF/RNoAF (Fighters, Transports, Helicopters) Chief Ops Department, Rygge Air Base Project Pilot New Helicopters/Chief Technical Pilot, Helikopter Service AS (1981-2000) Inspector of Accidents/Air Safety Investigator, AIBN (2000-2009) General Manager/Flight Safety Advisor, LandAvia Ltd (2009- ) Lecturer, Flight Mechanics, University of Agder/Grimstad (UiA) (2014- ) Sola Conference Safety Award/Solakonferansens Sikkerhetspris 2009 Introduction On Friday 23rd of August 2013 an AS332L2 crashed during a non-precision instrument approach to Sumburgh Airport, Shetland. The crash initiated panic within UK Oil and Gas industry, demanding grounding of the Super Puma fleet of helicopters. Four people died when the CHC Super Puma crashed on approach to Sumburgh Airport on 23 August 2013. 1 All Super Puma helicopter passenger flights to UK oil installations were suspended after a crash off Shetland claimed the lives of four people. The Helicopter Safety Steering Group (HSSG) had advised grounding all variants of the helicopter. The HSSG, which is made up of oil industry representatives, advised that all models of the Super Puma series including: AS332 L, L1, L2 and EC225 should be grounded for "all Super Puma commercial passenger flights to and from offshore oil and gas installations within the UK." The Norwegian civil aviation authority had earlier rejected appeals from its unions to ground all its Super Pumas – which operate in the North Sea in very similar weather conditions to the UK fleet – insisting that Friday's crash was an isolated incident. -

Landing Gear Collapse, Aircraft Accident Report, New York Airways, Inc

Landing gear collapse, Aircraft Accident Report, New York Airways, Inc. Sikorsky S-61L, N619PA, Pan Am Building Heliport, New York, New York, May 16, 1977 Micro-summary: The landing gear of this helicopter collapsed while the engine was running. Event Date: 1977-05-16 at 1735 EDT Investigative Body: National Transportation Safety Board (NTSB), USA Investigative Body's Web Site: http://www.ntsb.gov/ Cautions: 1. Accident reports can be and sometimes are revised. Be sure to consult the investigative agency for the latest version before basing anything significant on content (e.g., thesis, research, etc). 2. Readers are advised that each report is a glimpse of events at specific points in time. While broad themes permeate the causal events leading up to crashes, and we can learn from those, the specific regulatory and technological environments can and do change. Your company's flight operations manual is the final authority as to the safe operation of your aircraft! 3. Reports may or may not represent reality. Many many non-scientific factors go into an investigation, including the magnitude of the event, the experience of the investigator, the political climate, relationship with the regulatory authority, technological and recovery capabilities, etc. It is recommended that the reader review all reports analytically. Even a "bad" report can be a very useful launching point for learning. 4. Contact us before reproducing or redistributing a report from this anthology. Individual countries have very differing views on copyright! We can advise you on the steps to follow. Aircraft Accident Reports on DVD, Copyright © 2006 by Flight Simulation Systems, LLC All rights reserved. -

How Frasca Supports Offshore Helicopter Pilot Training at Bristow Group

How Frasca Supports Offshore Helicopter Pilot Training At Bristow Group Customer Feature Bristow Group Needed a New Training Solution In the mid-2000s, Bristow Group’s training needs analysis identified a requirement for a suite of new full flight simulators (FFS) to support the introduction of a new generation of twin-engine IFR helicopters used to support offshore oil and gas exploration and production: Airbus EC225, Sikorsky S- 76C++ and Sikorsky S-92 Frasca Designed and Manufactured 3 Custom Full Flight Simulators Frasca was contracted to design, manufacturer and install three state-of-art full flight simulators in Bristow’s North Sea helicopter training center in Aberdeen, Scotland. Bristow Group - Leading Provider Of Industrial Aviation Services The company began building its oil and gas credentials before the first discovery in the North Sea, tracing its beginnings back to an adventurous businessman named Alan Bristow. The company’s long history started in 1955 with Bristow Helicopters Ltd. in the UK. In 1996, Offshore Logistics of the United States pur- chased a stake in Bristow Helicopters Ltd., and the company was rebranded as Bristow Group Inc. in 2006. Today Bristow employs approximately 5,000 people and operates 345 aircraft - 296 helicopters and 49 fixed-wing aircraft – plus 119 aircraft flown by joint-ven- tures partners, with major operations in the North Sea, Nigeria, the U.S. Gulf of Mexico, and in most of the other major offshore oil and gas producing regions of the world, including Australia, Brazil, Canada, Russia and Trinidad. Mission Profile In the central and northern North Sea, the U.K.’s offshore oil and gas fields are primarily served from Aberdeen airport — the world’s busiest helicopter hub —, which handles about 500,000 passengers each year. -

Special Helicopter Stamp and Cover Issue

THE A OS JOU N Special Helicopter Stamp And Cover Issue VOLUME XXV ll - NO. 9 JUNE, 1956 Errors, Varieties, & Airmails For 30 years we have been specializing in all UNUSUAL Items, ERRORS, VARIETIES, e:tc., regardless if :they are or are not listed. Now we .have on hand a very large selection of Airmails, U. P. U., U. N .. F. D. R., Ro:tary, Inverted Centers, Sports, Topicals, Miniature f~1ee:ts, De Luxe Sheets, Proofs, etc., etc. We have oddities and un usual items from many different countries as •.• A!byi;sinia, A1bania, Belgium, Brazil, Canary Islands, Colombia, Con go, Croatia, Czechoslovakia, Danzig, Ecuador, Epirus, Far East, France & Colonies, Greece, Georgia, Honduras. Iceland, Ifni, Iran, Italy & Colonies, Jugoslavia, Latvia, Liberia, Lithuania, Luxembourg, Monaco, N"icaragua, Panama, Paraguay, Poland, Romania Russia, ~aar, Salvador, Scadta, Spain & Colonies Tangier, Tanna Touva, Uruguay, Venezuela, etc., etc., etc. We will gladly make Special Selections for you on Approval and, of course, you have the right to return anything. Please check where you are especially interested. ( Central America ( Booklets ( South America ( Covers ( Asia. ( DeLuxe Sheets ( Africa ( ( Europe ( F. D.R. ( Belgium ( Inverted Centers ( France & Cols. ( Miniature Sheets ( Uberia ( Proofs ( Lithuania ( Rotary ( Poland ( Sport ( Russia ( Topicals ( Spain ( U. N. ( Airmails ( U. P. U. Americana Please t:heck if you are especially interested in: ) Items up to $5 ( ) Up to $15 ( ) Up to $25 ( ) Up to ?? Please check if value of our first selection should be: $50 00, $100.00, $200.00, $500.00, $1000. Additional Information References (if unknown to us) City (Postal No. please) Address Name S., Serebrakian 15 PARK ROW BA 7-3830 NEW YORK 38, N. -

Police Aviation News July 2007

Police Aviation News July 2007 ©Police Aviation Research Number 135 July 2007 IPAR Police Aviation News July 2007 2 PAN – POLICE AVIATION NEWS is published monthly by INTERNATIONAL POLICE AVIATION RESEARCH 7 Windmill Close, Honey Lane, Waltham Abbey, Essex EN9 3BQ UK Main: +44 1992 714162 Cell: +44 7778 296650 Skype: Bryn.Elliott Bryn Elliott E-mail: [email protected] Bob Crowe www.bobcroweaircraft.com Digital Downlink www.bms-inc.com L3 Wescam www.wescam.com Innovative Downlink Solutions www.mrcsecurity.com Power in a box www.powervamp.com Interactive data-stream www.imagebase.co.uk Showing the way www.skyforceobserver.com Airborne Law Enforcement Association www.alea.org European Law Enforcement Association www.pacenet.info Sindacato Personale Aeronavigante Della Polizia www.uppolizia.it AUSTRALIA QUEENSLAND: As the state continues to look with fear at the high costs associated with the purchase of a crime patrol helicopter to supplement the fixed wing fleet mainly as- signed to transportation duties others have a more positive view. The Mayor of the Gold Coast area Ron Clarke is backing a $3 million trial of a police heli- copter in his own region. Other politicians want the helicopter trial to focus on neighbour- hood crime and hooning [a local term for anti-social use of motor vehicles - travelling at speed, showing off etc]. Cr Clarke has previously advocated remote-control helicopters for use in surf rescues. Although this local support is growing in the face of local problems the State Police Minister Judy Spence said a helicopter was not on the State Government's agenda and not appar- ently on the shopping list of the local police. -

My Personal Callsign List This List Was Not Designed for Publication However Due to Several Requests I Have Decided to Make It Downloadable

- www.egxwinfogroup.co.uk - The EGXWinfo Group of Twitter Accounts - @EGXWinfoGroup on Twitter - My Personal Callsign List This list was not designed for publication however due to several requests I have decided to make it downloadable. It is a mixture of listed callsigns and logged callsigns so some have numbers after the callsign as they were heard. Use CTL+F in Adobe Reader to search for your callsign Callsign ICAO/PRI IATA Unit Type Based Country Type GINTA GNT 0A Amber Air Lithuania Civil BLUE MESSENGER BMS 0B Blue Air Romania Civil CATOVAIR IBL 0C IBL Aviation Mauritius Civil DARWIN DWT 0D Darwin Airline Switzerland Civil JETCLUB JCS 0J Jetclub Switzerland Civil VASCO AIR VFC 0V Vietnam Air Services Company (VASCO) Vietnam Civil AMADEUS AGT 1A Amadeus IT Group Spain Civil 1B Abacus International Singapore Civil 1C Electronic Data Systems Switzerland Civil 1D Radixx United States Civil 1E Travelsky Technology China Civil 1F INFINI Travel Information Japan Civil 1G Galileo International United States Civil 1H Siren-Travel Russia Civil CIVIL AIR AMBULANCE AMB 1I Deutsche Rettungsflugwacht Germany Civil EXECJET EJA 1I NetJets United States Civil FRACTION NJE 1I NetJets Europe Portugal Civil NAVIGATOR NVR 1I Novair Sweden Civil PHAZER PZR 1I Sky Trek International Airlines United States Civil Sunturk 1I Pegasus Hava Tasimaciligi Turkey Civil 1I Sierra Nevada Airlines United States Civil 1K Southern Cross Distribution Australia Civil 1K Sutra United States Civil OPEN SKIES OSY 1L Open Skies Consultative Commission United States Civil -

Helicopter Industry I Experience I

HELICOPTER INDUSTRY I EXPERIENCE I BLADE BLADE le charme new-yorkais slicing through traffic vu d’hélicoptère I have always thought a dichotomy lives at the heart of travel. On one hand, you are poised, and have committed, to wrap yourself in J’ai toujours pensé que voyager par la voie des airs présentait une dichotomie. aluminum skin and travel in a metal and composite tube at warp speed D’un côté, vous vous êtes préparé à vous glisser dans une peau d'aluminium, à voyager across oceans and over mountains and yet, getting to the airport, dans un tube de métal et de composites à une vitesse phénoménale par dessus les your launch site, can often take about the same amount of time as fording océans et les montagnes et, d’un autre côté, pour atteindre l’aéroport, votre point de that very same distance on your journey. départ, il vous faut parfois plus de temps que celui nécessaire à la totalité de votre voyage. Text by David Zara - ©blade HI I 12 HI I 13 HELICOPTER INDUSTRY I EXPERIENCE I SIncE thE 1960S… DEpuIS lES AnnéES 1960… AA nd then, along came Blade. The folks at Blade decided EEt puis, est arrivé Blade. Les créateurs de Blade ont the future ought to be now instead and brought travel décidé que l’avenir, c’était maintenant. Ils ont redonné au forward to its glamorous past. The journey begins with a voyage son charme d’antan. Celui-ci commence donc par Landing is at the General Aviation ramp and the Sheltair Nous atterrissons sur le tarmac du FBO de Sheltair, où warm welcome in their beautiful lounges at both the west un accueil chaleureux dans de magnifiques salons, soit à FBO. -

Wire Strike Devices Installed on Civil and Military Helicopters

DOT/FAA/AR-08/25 Safety Study of Wire Strike Air Traffic Organization Operations Planning Devices Installed on Civil and Office of Aviation Research and Development Military Helicopters Washington, DC 20591 September 2008 Final Report This document is available to the U.S. public through the National Technical Information Service (NTIS), Springfield, Virginia 22161. U.S. Department of Transportation Federal Aviation Administration NOTICE This document is disseminated under the sponsorship of the U.S. Department of Transportation in the interest of information exchange. The United States Government assumes no liability for the contents or use thereof. The United States Government does not endorse products or manufacturers. Trade or manufacturer’s names appear herein solely because they are considered essential to the objective of this report. This document does not constitute FAA certification policy. Consult your local FAA aircraft certification office as to its use. This report is available at the Federal Aviation Administration William J. Hughes Technical Center’s Full-Text Technical Reports page: actlibrary.tc.faa.gov in Adobe Acrobat portable document format (PDF). Technical Report Documentation Page 1. Report No. 2. Government Accession No. 3. Recipient's Catalog No. DOT/FAA/AR-08/25 4. Title and Subtitle 5. Report Date SAFETY STUDY OF WIRE STRIKE DEVICES INSTALLED ON CIVIL AND September 2008 MILITARY HELICOPTERS 6. Performing Organization Code 7. Author(s) 8. Performing Organization Report No. Vengalattore T Nagaraj and Inderjit Chopra 9. Performing Organization Name and Address 10. Work Unit No. (TRAIS) Alfred Gessow Rotorcraft Center Dept. of Aerospace Engineering University of Maryland College Park, MD 20742 11. -

FAA HISTORICAL CHRONOLOGY, 1926-1996 You May Use This

FAA HISTORICAL CHRONOLOGY, 1926-1996 You may use this chronology in three ways: Browse by scrolling through this document. Search this document for words, phrases, or numbers (for example, Lindbergh Field or 747). To do this, select Edit, then Find, or use the Control + F command. To quickly reach the beginning of any year, search for that year preceded by an asterisk (for example, *1957). Use the index *1926 May 20, 1926: President Calvin Coolidge signed the Air Commerce Act of 1926 into law. The act instructed the Secretary of Commerce to foster air commerce; designate and establish airways; establish, operate, and maintain aids to air navigation (but not airports); arrange for research and development to improve such aids; license pilots; issue airworthiness certificates for aircraft and major aircraft components; and investigate accidents. (See Introduction.) May 23, 1926: Western Air Express (WAE) became one of the first U.S. airlines to offer regular passenger service, flying from Los Angeles to Salt Lake City via Las Vegas. WAE had begun flying on Apr 17 as the fourth carrier to begin operations under a new air mail contract system that became the major source of income for the era's small but growing airline industry (see Jun 3, 1926). Over twelve years earlier, the St. Petersburg-Tampa Airboat Line had offered the world's first regularly scheduled airline service using heavier-than-air craft. This enterprise lasted for only the first three months of 1914. On Mar 1, 1925, T. Claude Ryan's Los Angeles-San Diego Air Line had begun the first scheduled passenger service operated wholly over the U.S.