John Hancock Emerging Markets Fund

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Cj Enm(035760

August 9, 2018 Result Comment CJ ENM (035760 KS) Decent performance 2Q consolidated operating profit in line at W79.2bn BUY (re-initiate) 3Q consolidated operating profit estimated at W86bn; earnings to stay solid Price (Aug. 8) W236,200 Target Price W270,000 Re-initiate coverage on CJ ENM with a BUY rating and a target price of % variance 14.3% W270,000 HeeJin Park ☎ (82-2) 3772-1562 2Q consolidated operating profit in line at W79.2bn [email protected] CJ ENM posted its first results after the merger on July 1. Consolidated operating profit came in at W79.2bn in 2Q, meeting our forecast of W79.3bn. SeJong Hong ☎ (82-2) 3772-1584 The E&M division delivered solid earnings with sales up 9.2% YoY and operating [email protected] profit up 25% YoY. Broadcasting exceeded expectations with operating profit increasing 22% YoY to W29.2bn. Ad sales growth of 10.2 YoY also turned out better than expected. Music and cinema showed mixed results. The music division KOSPI 2,301.45p posted sales of W66.5bn (+41.1% YoY) and operating profit of W4.2bn (+114% KOSDAQ 783.81p YoY) on strengthening IP (intellectual property) business. By contrast, the Market Cap. W5,179.0bn/ US4,543.0mn cinema/performance division remained in the red with an operating loss of Par Value W5,000 W3.9bn due to stagnant growth of moviegoers and weak line-up. The commerce division (CJ O shopping) registered standalone operating profit of W40.3bn and Outstanding Shares 21.9mn consolidated W33.9bn. -

Proliferation of Hallyu Wave and Korean Popular Culture Across the World: a Systematic Literature Review from 2000-2019

Journal of Content, Community & Communication Amity School of Communication Vol. 11 Year 6, June - 2020 [ISSN: 2395-7514 (Print)] Amity University, Madhya Pradesh [ISSN: 2456-9011 (Online)] PROLIFERATION OF HALLYU WAVE AND KOREAN POPULAR CULTURE ACROSS THE WORLD: A SYSTEMATIC LITERATURE REVIEW FROM 2000-2019 Garima Ganghariya Research Scholar, Department of Mass Communication and Media Studies, Central University of Punjab, Bathinda, India Dr Rubal Kanozia Assistant Professor, Department of Mass Communication and Media Studies, Central University of Punjab, Bathinda, Punjab, India ABSTRACT The exponential growth in the popularity of Korean pop cultural products across the globe known as Hallyu wave has grabbed the attention of people worldwide. At times when the geographic boundaries have become blurred due to the virtual connectivity and advancement in internet technology, South Korean popular culture is developing at an unprecedented rate across the globe. The popularity is such that it has entered the mainstream even competing with the Hollywood films, dramas and music. The field of Hallyu though has attracted many from the academia, as it is still a newer research area, not many significant attempts have been made to review the literature in a systematic manner. The major objective of this paper is to acquire a better understanding, and a detailed review of the research regarding Hallyu wave, its allied areas, current status and trends. Systematic Literature Review (SLR) is the method used for this paper. This research has utilized the methods presented by Junior & Filho (2010), Jabbour (2013) and Seuring (2013). The researchers have deployed a systematic literature review approach to collect, analyze and synthesize data regarding the Hallyu wave, addressing a variety of topics using Google Scholar between 2000 and 2019 and selected 100 primary research articles. -

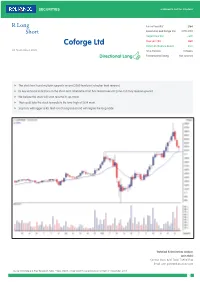

Coforge Ltd Potential Absolute Return 29% 03 November 2020 Time Horizon 9 Weeks Directional Long Fundamental Rating Not Covered

R Long Future Price (Rs)* 2164 Short Recommended Range (Rs) 2170-2150 Target Price (Rs) 2800 Stop Loss (Rs) 1880 Coforge Ltd Potential Absolute Return 29% 03 November 2020 Time Horizon 9 Weeks Directional Long Fundamental Rating Not covered f The stock has found multiple supports around 2080 level post a higher level reversal. f Its key technical indicators on the short-term timeframe chart has tested oversold zone and may reverse upward. f We believe the stock will soon resume its up-move. f That could take the stock towards its life-time-high of 2814 mark. f Stop loss will trigger at Rs 1880 (on closing basis) and will negate the long trade Technical & Derivatives Analyst: Jatin Gohil Contact: (022) 4215 7024/ 7498411546 Email: [email protected] Source: Bloomberg & RSec Research; Note: * Near Month- Single Stock Future price as on 12:15pm 3rd November, 2020 1 Recommendation Summary R Long Short Sr. Reco. Date Time Call Closure Recommendation Company Name Reco. Target Stop Call Status Current Return No Horizon date Price* Loss Price (%) Open Position 1 09-Sep-20 9 Weeks Short Bajaj Finance 3,413 2,550 3,770 Open 3456 -1.3% 2 20-Oct-20 10 Weeks Long Dabur 528 630 484 Open 516 -2.1% 3 21-Oct-20 6 Weeks Long M&M Financial 129 152 119 Open 126 -2.3% 4 30-Oct-20 6 Weeks Short JSW Steel 311 265 345 Open 314 0.9% 5 02-Nov-20 10 Weeks Long MFSL 615 800 545 Open 614 -0.1% Closed Positions 1 09-Oct-20 6 Weeks 28-Oct-20 Long Larsen & Toubro 900 1,065 842 Profit Booked 978 8.7% 2 15-Oct-20 6 Weeks 27-Oct-20 Long Kotak Bank 1,349 1,550 1,235 -

Birth and Evolution of Korean Reality Show Formats

Georgia State University ScholarWorks @ Georgia State University Film, Media & Theatre Dissertations School of Film, Media & Theatre Spring 5-6-2019 Dynamics of a Periphery TV Industry: Birth and Evolution of Korean Reality Show Formats Soo keung Jung [email protected] Follow this and additional works at: https://scholarworks.gsu.edu/fmt_dissertations Recommended Citation Jung, Soo keung, "Dynamics of a Periphery TV Industry: Birth and Evolution of Korean Reality Show Formats." Dissertation, Georgia State University, 2019. https://scholarworks.gsu.edu/fmt_dissertations/7 This Dissertation is brought to you for free and open access by the School of Film, Media & Theatre at ScholarWorks @ Georgia State University. It has been accepted for inclusion in Film, Media & Theatre Dissertations by an authorized administrator of ScholarWorks @ Georgia State University. For more information, please contact [email protected]. DYNAMICS OF A PERIPHERY TV INDUSTRY: BIRTH AND EVOLUTION OF KOREAN REALITY SHOW FORMATS by SOOKEUNG JUNG Under the Direction of Ethan Tussey and Sharon Shahaf, PhD ABSTRACT Television format, a tradable program package, has allowed Korean television the new opportunity to be recognized globally. The booming transnational production of Korean reality formats have transformed the production culture, aesthetics and structure of the local television. This study, using a historical and practical approach to the evolution of the Korean reality formats, examines the dynamic relations between producer, industry and text in the -

Annual Report and Financial Statements

Annual Report and Financial Statements for the year ended 31 December 2019 Dimensional Funds ICVC Authorised by the Financial Conduct Authority No marketing notification has been submitted in Germany for the following Funds of Dimensional Funds ICVC: Global Short-Dated Bond Fund International Core Equity Fund International Value Fund United Kingdom Core Equity Fund United Kingdom Small Companies Fund United Kingdom Value Fund Accordingly, these Funds must not be publicly marketed in Germany. Table of Contents Dimensional Funds ICVC General Information* 2 Investment Objectives and Policies* 3 Authorised Corporate Director’s Investment Report* 5 Incorporation and Share Capital* 9 The Funds* 9 Fund Cross-Holdings* 9 Fund and Shareholder Liability* 9 Regulatory Disclosure* 9 Potential Implications of Brexit* 9 Responsibilities of the Authorised Corporate Director 10 Responsibilities of the Depositary 10 Report of the Depositary to the Shareholders 10 Directors' Statement 10 Independent Auditors’ Report to the Shareholders of Dimensional Funds ICVC 11 The Annual Report and Financial Statements for each of the below sub-funds (the “Funds”); Emerging Markets Core Equity Fund Global Short-Dated Bond Fund International Core Equity Fund International Value Fund United Kingdom Core Equity Fund United Kingdom Small Companies Fund United Kingdom Value Fund are set out in the following order: Fund Information* 13 Portfolio Statement* 30 Statement of Total Return 139 Statement of Change in Net Assets Attributable to Shareholders 139 Balance Sheet 140 Notes to the Financial Statements 141 Distribution Tables 160 Remuneration Disclosures (unaudited)* 169 Supplemental Information (unaudited)* 170 * These collectively comprise the Authorised Corporate Director’s (“ACD”) Report. Dimensional Fund Advisors Ltd. -

Pan Entertainment (068050 KQ) Poised to Benefit from China’S Growing Content Demand

Pan Entertainment (068050 KQ) Poised to benefit from China’s growing content demand Snapshot: Producer of Winter Sonata, the origin of the Korean Wave Founded in 1998, Pan Entertainment was mainly engaged in the business of managing Company Report recording artists and making soundtracks before producing its first drama series “Winter December 5, 2014 Sonata” in 2002. The drama became a huge hit in Japan, setting in motion the “Korean Wave” across the country. Since then, the company has established itself as a drama producer, but has struggled to maintain stable profits due to the small size and buyer- Not Rated driven culture of the domestic market. Catalyst: China’s video content demand is surging, but options are limited Target Price (12M, W) - In China, there are over 4,000 television channels, all of which rely on advertising as their Share Price (12/03/14, W) 6,380 biggest source of income. Because advertising revenue is largely determined by primetime ratings, many broadcasters crave killer content, most preferably in the form Expected Return - of dramas and entertainment shows. But, while China’s video content demand has been rapidly increasing in terms of both quantity and quality, the country’s production capabilities have lagged far behind. Demand has been growing not only among major OP (14F, Wbn) 1 broadcasters and studios, but also among internet portals like Alibaba, and online video Consensus OP (14F, Wbn) 0 streaming sites such as Youku Tudou and Sohu. To make up for the lack of content, EPS Growth (14F, %) - Chinese companies are increasingly turning to Korean pr oducers, as Korean content is 1) Market EPS Growth (14F, %) 1.1 hugely popular in China, 2) of higher quality, and 3) cheaper to produce. -

TRULY GLOBAL Worldscreen.Com *LIST 1218 ALT2 LIS 1006 LISTINGS 11/21/18 11:19 AM Page 2

*LIST_1218_ALT2_LIS_1006_LISTINGS 11/21/18 11:19 AM Page 1 WWW.WORLDSCREENINGS.COM DECEMBER 2018 ASIA TV FORUM EDITION TVLISTINGS THE LEADING SOURCE FOR PROGRAM INFORMATION TRULY GLOBAL WorldScreen.com *LIST_1218_ALT2_LIS_1006_LISTINGS 11/21/18 11:19 AM Page 2 2 TV LISTINGS ASIA TV FORUM EXHIBITOR DIRECTORY COMPLETE LISTINGS FOR THE COMPANIES IN BOLD CAN BE FOUND IN THIS EDITION OF TV LISTINGS. 108 Media L28 Five Star Production C28 NHC Media J10 9 Story Distribution International J30 Fixed Stars Multimedia D10 NHK Enterprises B10-18 A+E Networks G20 Flame Distribution L05 Nippon Animation B10-14 ABC Commercial L05 Fortune Star Media G26 Nippon TV B10-19 About Premium Content F10 FOX Networks Group D18 NPO Sales H36 ABS-CBN Corporation J18 FranceTV Distribution F10 NTV Broadcasting Company H27 ADK/NAS/D-Rights B10-15 Fred Media L05 Oak 3 Films E08/H08 AK Entertainment H10 Fremantle E20 Ocon Studios H32 Albatross World Sales L30 Fuji Creative Corporation B10-9 Off The Fence J23 Alfred Haber Distribution F30 GAD F10 Omens Studios E08/H08 all3media international K08 Gala Television Corporation D10 One Animation E08/H08 Alpha Group L10/N10 Gaumont H33 One Life Studios J04 Ampersand F10 Global Agency E27 One Take Media J28 Anima Istanbul N08 Globo K24 Only Distrib F10 Animasia Studio M28 Gloob Participants Lounge Parade Media Group H08-01 Animonsta Studios M28 GMA Worldwide J01 Paramount Pictures Suite 5201 Animoon J25 GO-N International F10 PGS Entertainment F10 Aniplex B27 GoldBee H34 Phoenix Satellite Television G24 Antares International -

KOREA Morning Focus

March 15, 2018 KOREA Morning Focus Company News & Analysis Major Indices Close Chg Chg (%) SM Entertainment (041510/Buy/TP: W50,000) KOSPI 2,486.08 -8.41 -0.34 Positive on KeyEast/FNC Add Culture acquisition KOSPI 200 321.99 -0.99 -0.31 KOSDAQ 886.92 0.67 0.08 Sector News & Analysis Turnover ('000 shares, Wbn) Volume Value Internet/Game (Overweight) KOSPI 357,035 6,259 Japan visit note: Expanding lifestyle presence KOSPI 200 74,841 4,749 KOSDAQ 920,060 5,181 Market Cap (Wbn) Value KOSPI 1,652,629 KOSDAQ 285,293 KOSPI Turnover (Wbn) Buy Sell Net Foreign 1,580 1,709 -130 Institutional 1,232 1,375 -142 Retail 3,437 3,154 283 KOSDAQ Turnover (Wbn) Buy Sell Net Foreign 366 440 -74 Institutional 184 235 -51 Retail 4,617 4,481 136 Program Buy / Sell (Wbn) Buy Sell Net KOSPI 1,309 1,502 -192 KOSDAQ 187 197 -10 Advances & Declines Advances Declines Unchanged KOSPI 324 502 61 KOSDAQ 525 638 92 KOSPI Top 5 Most Active Stocks by Value (Wbn) Price (W) Chg (W) Value Samsung Electronics 2,588,000 5,000 645 Celltrion 306,500 -4,500 582 Hynix 90,700 700 512 Pharmicell 8,710 2,010 230 KODEX LEVERAGE 17,215 -40 212 KOSDAQ Top 5 Most Active Stocks by Value (Wbn) Price (W) Chg (W) Value SillaJen 119,900 2,600 250 NATURECELL 54,600 2,000 171 CIS 2,495 265 138 Diostech 38,550 250 108 Celltrion Healthcare 104,900 0 92 Note: As of March 14, 2018 Mirae Asset Daewoo Research SM Entertainment (041510 KQ) Positive on KeyEast/FNC Add Culture acquisition Entertainment Acquisition of rivals to strengthen content production business; Maintain positive view Company Update We reaffirm our Buy call and target price of W50,000 on SM Entertainment. -

Holdings-Report.Pdf

The Fund is a closed-end exchange traded management Investment company. This material is presented only to provide information and is not intended for trading purposes. Closed-end funds, unlike open-end funds are not continuously offered. After the initial public offering, shares are sold on the open market through a stock exchange. Changes to investment policies, current management fees, and other matters of interest to investors may be found in each closed-end fund's most recent report to shareholders. Holdings are subject to change daily. PORTFOLIO HOLDINGS FOR THE KOREA FUND as of July 31, 2021 *Note: Cash (including for these purposes cash equivalents) is not included. Security Description Shares/Par Value Base Market Value (USD) Percent of Base Market Value SAMSUNG ELECTRONICS CO 793,950 54,183,938.27 20.99 SK HYNIX INC COMMON 197,500 19,316,452.95 7.48 NAVER CORP COMMON STOCK 37,800 14,245,859.60 5.52 LG CHEM LTD COMMON STOCK 15,450 11,309,628.34 4.38 HANA FINANCIAL GROUP INC 225,900 8,533,236.25 3.31 SK INNOVATION CO LTD 38,200 8,402,173.44 3.26 KIA CORP COMMON STOCK 107,000 7,776,744.19 3.01 HYUNDAI MOBIS CO LTD 26,450 6,128,167.79 2.37 HYUNDAI MOTOR CO 66,700 6,030,688.98 2.34 NCSOFT CORP COMMON STOCK 8,100 5,802,564.66 2.25 SAMSUNG BIOLOGICS CO LTD 7,230 5,594,175.18 2.17 KB FINANCIAL GROUP INC 123,000 5,485,677.03 2.13 KAKAO CORP COMMON STOCK 42,700 5,456,987.61 2.11 HUGEL INC COMMON STOCK 24,900 5,169,415.34 2.00 SAMSUNG 29,900 4,990,915.02 1.93 SK TELECOM CO LTD COMMON 17,500 4,579,439.25 1.77 KOREA INVESTMENT 53,100 4,427,115.84 -

Coforge Ltd (NIITEC)

Coforge Ltd (NIITEC) CMP: | 2456 Target: | 2690 ( 10%) Target Period: 12 months HOLD October 23, 2020 Robust operating performance… Coforge Ltd (Coforge) registered healthy revenue growth, up 8.1% QoQ in constant currency terms, above our estimate of 7.0% QoQ growth. The revenue growth was broad based across verticals mainly led by insurance (up 13.5% QoQ) and BFS (up 10.2% QoQ). Digital revenues (including IP) also increased 18.7% QoQ. Further, Coforge has guided for revenue growth Particulars of 6% YoY organic growth in FY21E and 17.8% EBITDA margin in FY21E Particular Amount before Esop cost. Market Capi (| Crore) 15,116.7 Healthy deal pipeline, digital to drive growth Total Debt (| Crore) 4.8 Update Result Cash & Invests (| Crore) 917.1 Coforge is witnessing healthy traction in cloud, data and artificial intelligence EV (| Crore) 14,204.4 (AI). This has led to healthy growth in digital revenues. The company is driving this growth via partnerships with large players in cloud like Microsoft 52 week H/L 2813 / 739 Azure, Google cloud and AWS and partnering with product start-ups that Equity capital 62.5 can help it to drive new age technology growth. Hence, we expect the Face value 10.0 company to benefit from improved traction in digital technology, going forward. Further, we expect Coforge to witness healthy traction in the BFS Key Highlights and insurance vertical led by large deal wins and wallet share gain in travel segment. In addition, the company expects strong revenue growth in Dollar revenue to improve in coming quarters based on large deal won and healthcare vertical (as seen in this quarter). -

FIRST TRUST EXCHANGE-TRADED ALPHADEX FUND II Form NPORT

SECURITIES AND EXCHANGE COMMISSION FORM NPORT-P Filing Date: 2021-05-21 | Period of Report: 2021-03-31 SEC Accession No. 0001145549-21-027287 (HTML Version on secdatabase.com) FILER FIRST TRUST EXCHANGE-TRADED ALPHADEX FUND II Mailing Address Business Address 120 EAST LIBERTY DRIVE, 120 EAST LIBERTY DRIVE, CIK:1510337| IRS No.: 000000000 | State of Incorp.:MA SUITE 400 SUITE 400 Type: NPORT-P | Act: 40 | File No.: 811-22519 | Film No.: 21945692 WHEATON IL 60187 WHEATON IL 60187 630-765-8000 Copyright © 2021 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document First Trust Asia Pacific ex-Japan AlphaDEX® Fund (FPA) Portfolio of Investments March 31, 2021 (Unaudited) Shares Description Value Shares Description Value COMMON STOCKS (a) – 97.0% Hong Kong (Continued) Australia – 19.4% 21,818 New World Development Co. 3,640 Afterpay Ltd. (b) $ 280,623 Ltd. $ 112,821 26,726 AGL Energy Ltd. 195,892 87,182 PCCW Ltd. 49,119 23,714 ALS Ltd. 174,356 9,818 Power Assets Holdings Ltd. 57,968 3,925 Ansell Ltd. 116,984 12,331 Sun Hung Kai Properties Ltd. 186,850 2,429 Aristocrat Leisure Ltd. 63,374 15,772 Techtronic Industries Co., Ltd. 269,829 34,260 Aurizon Holdings Ltd. 101,486 854,442 2,045 BHP Group Ltd. 70,364 New Zealand – 0.7% 5,733 BlueScope Steel Ltd. 84,260 1,445 Xero Ltd. (b) 138,873 31,931 Boral Ltd. (b) 133,150 Singapore – 7.6% 2,757 Domino’s Pizza Enterprises Ltd. 201,555 105,200 CapitaLand Ltd. -

Abstract: the Purpose of This Paper Is to Investigate

THE ECONOMIC COST OF NUCLEAR THREATS: A NORTH KOREA CASE STUDY. Abstract: The purpose of this paper is to investigate how public announcements of a nation’s nuclear programme development influence neighbouring countries’ stock markets. The countries examined in this case study are North and South Korea. To test this relationship I conducted an event study using MacKinlay’s market model. Six announcement days were studied comprising out of three nuclear tests and three missile and satellite related tests. The findings of this research are in contrast to prior research. Empirical researches on the economic effects of terrorism suggest that acts of terrorism create large impacts on economic activity. The results of our event study show that the announcements caused both negative and positive reactions on the market. Author: Ryan McKee Student number: 6181066 Supervisor: Shivesh Changoer Date: 8th of Jan, 2014 ETCS: 12 INTRODUCTION Stock prices represent investor’s expectations about the future. News announcements effect these expectations on a day to day basis. Terrorist attacks, military invasions, nuclear threats or any other ambivalent events can alter investor’s expectations and so allow the prices of stocks and bonds to deviate from their fundamental value. Once such events have taken place investors often defer from the market in search of safer, more secure financial investments which can lead to panic and chaos on the markets (Chen and Siems, 2004). Such chaos can also be caused by threats from other neighbouring countries. A perfect example of this is the relationship between North and South Korea. Ever since the division of North and South Korea on September 8, 1945 the two bordering nations have had a strenuous relationship, ultimately leading to the Korean war of 1950-1953.