Financial Instruments and Risk Warnings

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

A Guide for Investors

A GUIDE FOR INVESTORS CONTENTS INTRODUCTION 5 MAIN RISKS 7 Business risk or intrinsic risk 7 Economic risk 7 1 Inflation risk 7 Country risk 7 Currency risk 7 Liquidity risk 7 Psychological risk 7 Credit risk 7 Counterparty risk 8 Additional risks associated with emerging markets 8 Other main risks 8 BRIEF DESCRIPTION OF CERTAIN TYPES OF INVESTMENT AND SPECIFIC ASSOCIATED RISKS 9 Time deposits 9 2 Bonds 9 A. Characteristics of classic bonds 9 B. Convertible bonds 9 C. CoCo type bonds 9 D. Risks 9 Equities 10 A. Characteristics 10 B. Risks 10 Derivatives 10 A. Options 11 B. Warrants 11 C. Futures 11 D. Risks 11 Structured products 11 A. Characteristics 11 B. Risks 11 C. Reverse convertibles 11 Investment funds 12 A. General risks 12 B. Categories 12 1. Money market funds 12 2. Bond funds 12 3. Equity funds 12 4. Diversified/profiled funds 12 5. Special types of funds 12 A. Sector funds 12 B. Trackers 12 C. Absolute return funds 13 Page 3 of 21 CONTENTS D. Alternative funds 13 1. Hedge funds 13 2. Alternative funds of funds 13 E. Offshore funds 13 F. Venture capital or private equity funds 14 Private Equity 14 A. Caracteristics 14 B. Risks 14 1. Risk of capital loss 14 2. Liquidity risk 14 3. Risk related to the valuation of securities 14 4. Risk related to investments in unlisted companies 14 5. Credit risk 14 6. Risk related to “mezzanine” financing instruments 14 7. Interest rate and currency risks 14 8. Risk related to investment by commitment 15 3 GLOSSARY 16 Any investment involves the taking of risk. -

Evaluation of Risk Elements in Real Estate Investment in Nigeria: the Case of Uyo Metropolis, Akwa Ibom State

IOSR Journal of Business and Management (IOSR-JBM) e-ISSN: 2278-487X, p-ISSN: 2319-7668. Volume 18, Issue 10. Ver. II (October. 2016), PP 70-75 www.iosrjournals.org Evaluation of Risk Elements In Real Estate investment In Nigeria: The Case Of Uyo Metropolis, Akwa Ibom State Dr. Francis P. Udoudoh, Department of Estate Management, University of Uyo, Nigeria Dr. Usen P. Udoh, Department of Architecture, University of Uyo, Nigeria* Abstract: Risk is a common feature of all forms of investment including real estate which involves the creation of new income yielding assets from land and its resources based on capital analysis of expected costs and benefits within a given time. While some real estate investments have a high-risk profile, others have low-risk profile depending on the type, location and lease term. This study was designed to evaluate the different elements of risk in relation to different stages of real estate development in Uyo Metropolis, Akwa Ibom State. A total of 200 project sites were randomly selected and visited for data collection. Accordingly, 200 sets of questionnaire containing items bordering on types of risk/ project development were administered to the private estate developers while simple percentages was employed to analyse data. Findings indicated that the nature of risk encountered by investors varied according to the stages of project development, especially during preparation of development plans and building construction. Majority of respondents identified lack of access to project finance, delay in issuance of C-of-O and default in rent payment as the major risk elements in their investment. -

3. VALUATION of BONDS and STOCK Investors Corporation

3. VALUATION OF BONDS AND STOCK Objectives: After reading this chapter, you should be able to: 1. Understand the role of stocks and bonds in the financial markets. 2. Calculate value of a bond and a share of stock using proper formulas. 3.1 Acquisition of Capital Corporations, big and small, need capital to do their business. The investors provide the capital to a corporation. A company may need a new factory to manufacture its products, or an airline a few more planes to expand into new territory. The firm acquires the money needed to build the factory or to buy the new planes from investors. The investors, of course, want a return on their investment. Therefore, we may visualize the relationship between the corporation and the investors as follows: Capital Investors Corporation Return on investment Fig. 3.1: The relationship between the investors and a corporation. Capital comes in two forms: debt capital and equity capital. To raise debt capital the companies sell bonds to the public, and to raise equity capital the corporation sells the stock of the company. Both stock and bonds are financial instruments and they have a certain intrinsic value. Instead of selling directly to the public, a corporation usually sells its stock and bonds through an intermediary. An investment bank acts as an agent between the corporation and the public. Also known as underwriters, they raise the capital for a firm and charge a fee for their services. The underwriters may sell $100 million worth of bonds to the public, but deliver only $95 million to the issuing corporation. -

Summary Prospectus

Summary Prospectus KFA Dynamic Fixed Income ETF Principal Listing Exchange for the Fund: NYSE Arca, Inc. Ticker Symbol: KDFI August 1, 2021 Before you invest, you may want to review the Fund’s Prospectus, which contains more information about the Fund and its risks. You can find the Fund’s Prospectus, Statement of Additional Information, recent reports to shareholders, and other information about the Fund online at www.kfafunds.com. You can also get this information at no cost by calling 1-855-857-2638, by sending an e-mail request to [email protected] or by asking any financial intermediary that offers shares of the Fund. The Fund’s Prospectus and Statement of Additional Information, each dated August 1, 2021, as each may be amended or supplemented from time to time, and recent reports to shareholders, are incorporated by reference into this Summary Prospectus and may be obtained, free of charge, at the website, phone number or email address noted above. As permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds’ shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from the Funds (if you hold your Fund shares directly with the Funds) or from your financial intermediary, such as a broker-dealer or bank (if you hold your Fund shares through a financial intermediary). Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report. -

Risk Disclosure Regarding Complex Or Leveraged Exchange-Traded Products

RISK DISCLOSURE REGARDING COMPLEX OR LEVERAGED EXCHANGE-TRADED PRODUCTS Interactive Brokers ("IBKR") is furnishing this disclosure to clients to provide additional information regarding the characteristics and risks associated with Complex or Leveraged exchange-traded products ("ETPs"). Complex or Leveraged Exchange-Traded Products ("ETPs") are funds or notes that trade on an exchange but have very different characteristics from shares of stock or ordinary exchange-traded funds (ETFs) such as an S&P 500 Index ETF. Complex or Leveraged ETPs may include, but are not limited to: (1) leveraged ETFs and ETPs; (2) inverse ETFs and ETPs; (3) volatility-linked ETFs and ETPs; (4) Exchange-Traded Notes ("ETNs"); (5) cryptocurrency ETFs and ETPs; and (6) any other ETP that uses derivatives, that contains imbedded leverage, or that is based on an exotic or volatile underlying commodity or index or financial product. In addition to providing this disclosure, IBKR strongly encourages clients to carefully review the prospectus, Key Information Document or other available disclosures relating to the specific ETF, ETN or other ETP before investing, to understand its unique features, risks, fees, tax treatment and other characteristics. LEVERAGED FUNDS As the name implies, leveraged mutual funds and ETFs seek to provide leveraged returns at multiples of the underlying benchmark or index they track. Leveraged funds generally seek to provide a multiple (i.e., 200%, 300%) of the daily return of an index or other benchmark for a single day excluding fees and other expenses. In addition to using leverage, these funds often use derivative products such as swaps, options, and futures contracts to accomplish their objectives. -

Exchange Traded Notes, Each Linked to a Different Equity Index BMO Capital Markets

Registration Statement No. 333-237342 Filed Pursuant to Rule 424(b)(3) Prospectus Addendum, dated April 20, 2020 to Product Supplements and Prospectus Supplements of Various Dates, and the Prospectus Dated April 20, 2020 Exchange Traded Notes, Each Linked to a Different Equity Index This prospectus addendum relates to several issuances of outstanding exchange traded notes that Bank of Montreal has issued. We will use this prospectus addendum and the applicable pricing supplement and prospectus supplement, each dated as of various dates, in connection with the continuous offering of these notes. These notes were initially registered, and all or a portion of them were initially offered and sold, under registration statements that we previously filed. When we initially registered each of these notes, we prepared a prospectus supplement, each referred to as the “original prospectus supplement” relating to the applicable notes, and in some cases, a product supplement (each referred to as the “original product supplement”). The applicable original prospectus supplement (and product supplement, if applicable) is accompanied by a “base” prospectus. We have prepared a new “base” prospectus dated April 20, 2020. This new base prospectus replaces the applicable previous base prospectus relating to each of the notes. Because the terms of each series of notes otherwise have remained the same, we are continuing to use the original prospectus supplement (and if applicable, the original product supplement). Accordingly, you should read the original prospectus supplement (and any applicable product supplement) for the applicable notes, together with the new base prospectus. When you read these documents, please note that all references in the original prospectus supplement or product supplement to the base prospectus dated as of a date prior to April 20, 2020 or to any sections of the prior base prospectus, should refer instead to the new base prospectus, or to the corresponding section of that new base prospectus. -

Assessing Securities Lending Risk-Return Performance in a Portfolio Context

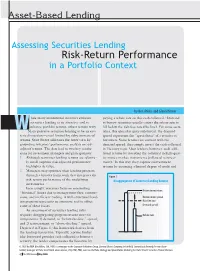

Asset-Based Lending Assessing Securities Lending Risk-Return Performance in a Portfolio Context by Ben Atkins and Glenn Horner hile many institutional investors embrace paying a rebate rate on this cash collateral.1 Demand securities lending as an attractive tool to to borrow securities usually causes the rebate rate to enhance portfolio returns, others remain wary. fall below the risk-free rate (the line). For some secu- WMany perceive securities lending to be an eso- rities, this spread is quite substantial; the demand teric distraction—a tool limited by risky, immaterial spread represents the “specialness” of a security to returns. State Street addresses the latter view by borrowers. Some lenders are content with the grounding investors’ performance analysis on risk- demand spread; they simply invest the cash collateral adjusted returns. The data lead to two key conclu- in Treasury repo. Most lenders, however, seek addi- sions for investment managers and plan sponsors: tional returns by investing the collateral in high-qual- 1. Although securities lending returns are relative- ity money market instruments (collateral reinvest- ly small, superior risk-adjusted performance ment).2 In this way, they capture reinvestment highlights its value. returns by assuming a limited degree of credit and 2. Managers may optimize their lending program through a broader framework that integrates the Figure 1 risk-return performance of the underlying Disaggregation of Securities Lending Returns investments. Increasingly, investors focus on minimizing Reinvestment return “frictional” losses due to management fees, commis- sions, and inefficient trading. A well-structured lend- Reinvestment spread ing program represents an attractive tool to offset Risk-free rate some of these losses. -

Aligning the Enterprise Risk Management Framework to the Personal Financial-Planning Domain

Aligning the Enterprise Risk Management Framework to the Personal Financial-Planning Domain Vinay Kumar Dutta Presented at the: 2013 Enterprise Risk Management Symposium April 22-24, 2013 © 2013 Casualty Actuarial Society, Professional Risk Managers’ International Association, Society of Actuaries Page 1 of 28 Aligning the Enterprise Risk Management Framework to the Personal Financial Planning Domain Vinay Kumar Dutta* Abstract Individuals face many risks during different phases of their financial life cycle. These risks in turn have major financial implications on their wealth creation, wealth preservation, and wealth distribution aspirations. Traditionally risk taking is viewed negatively in relation to the personal financial-planning domain. In fact, most of the studies linking risk management to personal financial-planning focus primarily on investment- and insurance-related risks. In contrast, enterprise risk management takes a portfolio view of risks right from the personal level to the organization level. However, the existing literature on enterprise risk management is seen as an essential feature of corporate world. Even risk management experts acknowledge that there is not much literature available that explicitly addresses the issue of aligning the enterprise risk management framework to the whole spectrum of personal financial planning. In this backdrop, it seems logical to develop an in-depth study on aligning an enterprise risk framework to a personal financial-planning domain. Accordingly, this conceptual paper, avoiding mathematical jargon, extensively examines the extent to which enterprise risk management can be aligned to the personal financial-planning domain. The study concludes by suggesting how individuals should identify, aggregate, evaluate, and address risks across the whole spectrum of the personal financial-planning domain. -

A Glossary of Securities and Financial Terms

A Glossary of Securities and Financial Terms (English to Traditional Chinese) 9-times Restriction Rule 九倍限制規則 24-spread rule 24 個價位規則 1 A AAAC see Academic and Accreditation Advisory Committee【SFC】 ABS see asset-backed securities ACCA see Association of Chartered Certified Accountants, The ACG see Asia-Pacific Central Securities Depository Group ACIHK see ACI-The Financial Markets of Hong Kong ADB see Asian Development Bank ADR see American depositary receipt AFTA see ASEAN Free Trade Area AGM see annual general meeting AIB see Audit Investigation Board AIM see Alternative Investment Market【UK】 AIMR see Association for Investment Management and Research AMCHAM see American Chamber of Commerce AMEX see American Stock Exchange AMS see Automatic Order Matching and Execution System AMS/2 see Automatic Order Matching and Execution System / Second Generation AMS/3 see Automatic Order Matching and Execution System / Third Generation ANNA see Association of National Numbering Agencies AOI see All Ordinaries Index AOSEF see Asian and Oceanian Stock Exchanges Federation APEC see Asia Pacific Economic Cooperation API see Application Programming Interface APRC see Asia Pacific Regional Committee of IOSCO ARM see adjustable rate mortgage ASAC see Asian Securities' Analysts Council ASC see Accounting Society of China 2 ASEAN see Association of South-East Asian Nations ASIC see Australian Securities and Investments Commission AST system see automated screen trading system ASX see Australian Stock Exchange ATI see Account Transfer Instruction ABF Hong -

Understanding and Managing Risk in Public Investing

CDIAC/CMTA Advanced Public Funds Investing Workshop Session Three: Understanding and Managing Risk in Public Investing Presented by: Sarah Meacham, Managing Director January 15, 2020 PFM Asset 601 S. Figueroa Street, Suite 4500 Management LLC Los Angeles, CA 90017 www.pfm.com 213.489.4075 © PFM 1 TYPES OF FIXED INCOME INVESTMENT RISK Inflation Interest rate Topics Liquidity Reinvestment Credit HOW TO MANAGE AND MITIGATE RISK Investment policy development Diversification Discipline to long-term strategy Performance measurement © PFM 2 “Risk is inherent throughout the investment process. There is investment risk associated with any investment activity and opportunity risk related to inactivity.” ~Local Agency Investment Guidelines, CDIAC January 1, 2019 © PFM 3 Types of Fixed Income Investment Risk © PFM 4 Types of Fixed Income Investment Risk Inflation Risk Liquidity Risk Credit Risk Loss of purchasing Inability to sell portfolio Risk of default or power over time as a holdings at a competitive decline in security value result of inflation price due to issuer’s financial strength Reinvestment Risk Interest Rate Risk The risk that a security’s Variability of return/price cash flow will be related to changes in reinvested at a lower interest rates rate of return © PFM 5 Inflation Risk © PFM 6 Inflation (Purchasing Power) Risk Loss of purchasing power over time as a result of inflation Real interest rate is after inflation; nominal is before inflation • Real = nominal – inflation • Nominal = real + inflation • Inflation = nominal -

Currency Risk Management

• Foreign exchange markets • Internal hedging techniques • Forward rates Foreign Currency Risk • Forward contracts Management 1 • Money market hedging • Currency futures 00 M O NT H 00 100 Syllabus learning outcomes • Assess the impact on a company to exposure in translation transaction and economic risks and how these can be managed. 2 Syllabus learning outcomes • Evaluate, for a given hedging requirement, which of the following is the most appropriate strategy, given the nature of the underlying position and the risk exposure: (i) The use of the forward exchange market and the creation of a money market hedge (ii) Synthetic foreign exchange agreements (SAFE's) (iii) Exchange-traded currency futures contracts (iv) Currency options on traded futures (v) Currency swaps (vi) FOREX swaps 3 Syllabus learning outcomes • Advise on the use of bilateral and multilateral netting and matching as tools for minimising FOREX transactions costs and the management of market barriers to the free movement of capital and other remittances. 4 Foreign Exchange Risk (FOREX) The value of a company's assets, liabilities and cash flow may be sensitive to changes in the rate in the rate of exchange between its reporting currency and foreign currencies. Currency risk arises from the exposure to the consequences of a rise or fall in the exchange rate A company may become exposed to this risk by: • Exporting or importing goods or services • Having an overseas subsidiary • Being a subsidiary of an overseas company • Transactions in overseas capital market 5 Types of Foreign Exchange Risk (FOREX) Transaction Risk (Exposure) This relates to the gains or losses to be made when settlement takes place at some future date of a foreign currency denominated contract that has already been entered in to. -

Value at Risk for Linear and Non-Linear Derivatives

Value at Risk for Linear and Non-Linear Derivatives by Clemens U. Frei (Under the direction of John T. Scruggs) Abstract This paper examines the question whether standard parametric Value at Risk approaches, such as the delta-normal and the delta-gamma approach and their assumptions are appropriate for derivative positions such as forward and option contracts. The delta-normal and delta-gamma approaches are both methods based on a first-order or on a second-order Taylor series expansion. We will see that the delta-normal method is reliable for linear derivatives although it can lead to signif- icant approximation errors in the case of non-linearity. The delta-gamma method provides a better approximation because this method includes second order-effects. The main problem with delta-gamma methods is the estimation of the quantile of the profit and loss distribution. Empiric results by other authors suggest the use of a Cornish-Fisher expansion. The delta-gamma method when using a Cornish-Fisher expansion provides an approximation which is close to the results calculated by Monte Carlo Simulation methods but is computationally more efficient. Index words: Value at Risk, Variance-Covariance approach, Delta-Normal approach, Delta-Gamma approach, Market Risk, Derivatives, Taylor series expansion. Value at Risk for Linear and Non-Linear Derivatives by Clemens U. Frei Vordiplom, University of Bielefeld, Germany, 2000 A Thesis Submitted to the Graduate Faculty of The University of Georgia in Partial Fulfillment of the Requirements for the Degree Master of Arts Athens, Georgia 2003 °c 2003 Clemens U. Frei All Rights Reserved Value at Risk for Linear and Non-Linear Derivatives by Clemens U.