Janus Henderson UK & Europe Funds

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Morning Wrap

Morning Wrap Today ’s Newsflow Equity Research 19 Jul 2019 08:16 BST Upcoming Events Select headline to navigate to article Paper and Packaging Stora Enso reports weak Q2, Company Events flagging lower box prices 19-Jul Close Brothers Group; Q419 Trading Update Stora Enso ; Q219 Results Building Materials US non-residential forecasts are 23-Jul Paragon Banking; Q319 Trading Update revised down 24-Jul Britvic; Q319 Trading Update Kindred Group; Q219 Results UK Banks CBG issues a disappointing pre-close trading Marston's; Q319 Trading Update Metro Bank; Q219 Results update – NIM in focus 25-Jul AIB Group; Q219 Results Bankinter; Q219 Results Breedon Group; Interim results Howden Joinery; H1 results International Paper; Q219 Results Permanent TSB; Q219 Results Tyman; H1 results Unilever PLC; Q219 Results Wizz Air; Q120 Results Economic Events Ireland 22-Jul PPI June19 Wholesale Price Index June19 26-Jul Retail Sales June19 United Kingdom 23-Jul CBI Industrial Trends July19 25-Jul CBI Distributive Trades July19 United States Europe This document is intended for the sole use of Goodbody Stockbrokers and its affiliates Goodbody Capital Markets Equity Research +353 1 6419221 Equity Sales +353 1 6670222 Bloomberg GDSE<GO> Goodbody Stockbrokers UC, trading as “Goodbody”, is regulated by the Central Bank of Ireland. In the UK, Goodbody is authorised and subject to limited regulation by the Financial Conduct Authority. Goodbody is a member of the Irish Stock Exchange and the London Stock Exchange. Goodbody is a member of the FEXCO group of companies. For the attention of US clients of Goodbody Securities Inc, this third-party research report has been produced by our affiliate, Goodbody Stockbrokers Goodbody Morning Wrap Paper and Packaging Stora Enso reports weak Q2, flagging lower box prices Stora Enso has reported Q2 results to the end of June. -

Annual Report and Accounts for the Year Ended 31 December 2020

Tyman plc Annual report and accounts TYMAN PLC for the year ended 31 December 2020 Annual report and accounts for the year ended 31 December 2020 Annual report and accounts for the year The expert touch that transforms Tyman is a leading international supplier of engineered fenestration components and access solutions to the construction industry. Highlights • Strong recovery from COVID-19 in H2 saw growth of 5% against £572.8m 1.1× 4.0p £100.6m H2 2019; full year LFL revenue down 6% Revenue Leverage* Dividend per share Adjusted net debt* • Cost reductions and benefits of self-help initiatives mitigated the full (2019: £613.7m) (2019: 1.7×) (2019: 3.9p) (2019: £164.5m) year revenue shortfall, resulting in adjusted operating margin slightly ahead of 2019 and LFL adjusted operating profit down only 6% • Good progress on self-help measures: £80.3m 27.2p £47.6m 19.1p − Encouraging level of North American customer wins Adjusted operating profit* Adjusted earnings per share* Profit before taxation Basic earnings per share − Successful execution of planned footprint realignments (2019: £85.4m) (2019: 27.5p) (2019: £24.8m) (2019: 9.1p) − Momentum gained with continuous improvement activities • Strategic initiatives continued to bear fruit, driving market share gains across the Group • Reduction in safety incidents of 22% indicative of operational excellence progress • Strong cash generation with cash conversion of 131% and reduction in leverage to 1.1x, achieving low-end of new target range • Repayment in December 2020 of £2.3m received under -

Fund Profile

Janus Henderson Tactical Income Fund With a focus on delivering a stable return profile and capital preservation, Janus Henderson’s highly experienced Australian Fixed Interest Team have the flexibility to actively change asset allocations in order to take full advantage of the interest rate cycle and credit environments. FUND Objective Stage 3: Implementation Implement the strategy by investing in a range of The Janus Henderson Tactical Income Fund cash, fixed interest and higher yielding securities. (“Fund”) seeks to achieve a total return By investing in the Fund, the following key after fees that exceeds the total return of the investment decisions are managed by the Team: Bloomberg AusBond Bank Bill Index and PROFILE Bloomberg AusBond Composite 0+ Yr Index • Interest rates: Determine when to hold longer (equally weighted) (“Benchmark”), by investing dated fixed rate assets (e.g. government bonds in a diversified portfolio of predominantly are typically cheap when interest rates peak in Australian income producing assets. an economic cycle) and when to hold shorter dated floating rate exposure. About the Fund • Sectors: Consider the right proportion of The Fund is an integrated and diversified fixed government securities versus non- interest solution, designed to make tactical government securities, dependent on the investment decisions between cash, longer adequacy of compensation to investors for duration fixed interest securities and higher the additional risk. yielding securities, throughout every step of the investment cycle. • Securities: Determine which non-government securities have stable to improving credit Investment philosophy quality. Of these securities, understand which offer an appropriate return for the The Fund is designed to leverage the considerable underlying risk. -

ES River and Mercantile UK Recovery Fund

ES River and Mercantile UK Recovery Fund Quarterly Report to 30 September 2020 UK Equity Unconstrained Fund I Monthly Report Month 2008 UK Recovery For unitholders only0 ES R&M UK Recovery Fund Quarter 3, 2020 Fund Objective The investment objective of the Fund is to grow the value of your investment (known as “capital growth”) in excess of the MSCI United Kingdom Investable Market Index (IMI) Net Total Return (the “Benchmark”) over a rolling 5 year period, after the deduction of fees. Performance (net of fees) B share class Benchmark Difference 3 Months -1.4% -3.6% 2.2% 1 Year -17.1% -18.5% 1.4% 3 Years p.a. -5.9% -4.1% -1.8% 5 Years p.a. 3.8% 3.0% 0.8% 10 Years p.a. 7.8% 4.6% 3.1% Since Inception p.a. 12.6% 7.9% 4.7% 20% 10% 0% -10% -20% -30% 3 Months 1 Year 3 Years 5 Years 10 Years Since Inception p.a. p.a. p.a. p.a. ES R&M UK Recovery Fund B Shares MSCI UK IM Index Performance (gross of fees) Z class Z share class Benchmark Difference 3 Months -1.2% -3.6% 2.4% 1 Year -16.2% -18.5% 2.3% 3 Years p.a. -5.0% -4.1% -0.9% 5 Years p.a. 4.8% 3.0% 1.9% 10 Years p.a. 8.9% 4.6% 4.2% Source: River and Mercantile Asset Management LLP. Benchmark is the MSCI UK Investable Market index, net GBP. -

Socially Conscious Australian Equity Holdings

Socially Conscious Australian Equity Holdings As at 30 June 2021 Country of Company domicile Weight COMMONWEALTH BANK OF AUSTRALIA AUSTRALIA 10.56% CSL LTD AUSTRALIA 8.46% AUST AND NZ BANKING GROUP AUSTRALIA 5.68% NATIONAL AUSTRALIA BANK LTD AUSTRALIA 5.32% WESTPAC BANKING CORP AUSTRALIA 5.08% TELSTRA CORP LTD AUSTRALIA 3.31% WOOLWORTHS GROUP LTD AUSTRALIA 2.93% FORTESCUE METALS GROUP LTD AUSTRALIA 2.80% TRANSURBAN GROUP AUSTRALIA 2.55% GOODMAN GROUP AUSTRALIA 2.34% WESFARMERS LTD AUSTRALIA 2.29% BRAMBLES LTD AUSTRALIA 1.85% COLES GROUP LTD AUSTRALIA 1.80% SUNCORP GROUP LTD AUSTRALIA 1.62% MACQUARIE GROUP LTD AUSTRALIA 1.54% JAMES HARDIE INDUSTRIES IRELAND 1.51% NEWCREST MINING LTD AUSTRALIA 1.45% SONIC HEALTHCARE LTD AUSTRALIA 1.44% MIRVAC GROUP AUSTRALIA 1.43% MAGELLAN FINANCIAL GROUP LTD AUSTRALIA 1.13% STOCKLAND AUSTRALIA 1.11% DEXUS AUSTRALIA 1.11% COMPUTERSHARE LTD AUSTRALIA 1.09% AMCOR PLC AUSTRALIA 1.02% ILUKA RESOURCES LTD AUSTRALIA 1.01% XERO LTD NEW ZEALAND 0.97% WISETECH GLOBAL LTD AUSTRALIA 0.92% SEEK LTD AUSTRALIA 0.88% SYDNEY AIRPORT AUSTRALIA 0.83% NINE ENTERTAINMENT CO HOLDINGS LIMITED AUSTRALIA 0.82% EAGERS AUTOMOTIVE LTD AUSTRALIA 0.82% RELIANCE WORLDWIDE CORP LTD UNITED STATES 0.80% SANDFIRE RESOURCES LTD AUSTRALIA 0.79% AFTERPAY LTD AUSTRALIA 0.79% CHARTER HALL GROUP AUSTRALIA 0.79% SCENTRE GROUP AUSTRALIA 0.79% ORORA LTD AUSTRALIA 0.75% ANSELL LTD AUSTRALIA 0.75% OZ MINERALS LTD AUSTRALIA 0.74% IGO LTD AUSTRALIA 0.71% GPT GROUP AUSTRALIA 0.69% Issued by Aware Super Pty Ltd (ABN 11 118 202 672, AFSL 293340) the trustee of Aware Super (ABN 53 226 460 365). -

Hipgnosis Songs Fund Limited

THIS DOCUMENT IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION. If you are in any doubt as to the action you should take or the contents of this Prospectus, you are recommended to seek your own independent financial advice immediately from your stockbroker, bank, solicitor, accountant, or other appropriate independent financial adviser, who is authorised under the Financial Services and Markets Act 2000 (the “FSMA”) if you are in the United Kingdom, or from another appropriately authorised independent financial adviser if you are in a territory outside the United Kingdom. A copy of this document, which comprises a prospectus relating to Hipgnosis Songs Fund Limited (the “Company”) in connection with the issue of Issue Shares in the Company and their admission to trading on the Main Market and to listing on the premium listing category of the Official List, prepared in accordance with the Prospectus Rules of the FCA made pursuant to section 73A of the FSMA, has been filed with the Financial Conduct Authority in accordance with Rule 3.2 of the Prospectus Rules. The Prospectus has been approved by the FCA, as competent authority under the Prospectus Regulation and the FCA only approves this Prospectus as meeting the standards of completeness, comprehensibility and consistency imposed by the Prospectus Regulation. Accordingly, such approval should not be considered as an endorsement of the issuer, or of the quality of the securities, that are the subject of this Prospectus; investors should make their own assessment as to the suitability of investing in the Issue Shares. The Issue Shares are only suitable for investors: (i) who understand the potential risk of capital loss and that there may be limited liquidity in the underlying investments of the Company; (ii) for whom an investment in the Issue Shares is part of a diversified investment programme; and (iii) who fully understand and are willing to assume the risks involved in such an investment programme. -

NOISE and MILITARY SERVICE Implications for Hearing Loss and Tinnitus

NOISE AND MILITARY SERVICE Implications for Hearing Loss and Tinnitus Committee on Noise-Induced Hearing Loss and Tinnitus Associated with Military Service from World War II to the Present Medical Follow-up Agency Larry E. Humes, Lois M. Joellenbeck, and Jane S. Durch, Editors THE NATIONAL ACADEMIES PRESS Washington, DC www.nap.edu THE NATIONAL ACADEMIES PRESS • 500 Fifth Street, N.W. • Washington, DC 20001 NOTICE: The project that is the subject of this report was approved by the Governing Board of the National Research Council, whose members are drawn from the councils of the National Academy of Sciences, the National Academy of Engineering, and the Insti- tute of Medicine. The members of the committee responsible for the report were chosen for their special competences and with regard for appropriate balance. This study was supported by Contract No. V101(93)P-1637 #29 between the Na- tional Academy of Sciences and the Department of Veterans Affairs. Any opinions, find- ings, conclusions, or recommendations expressed in this publication are those of the author(s) and do not necessarily reflect the view of the organizations or agencies that provided support for this project. Library of Congress Cataloging-in-Publication Data Noise and military service : implications for hearing loss and tinnitus / Committee on Noise-Induced Hearing Loss and Tinnitus Associated with Military Service from World War II to the Present, Medical Follow- up Agency ; Larry E. Humes, Lois M. Joellenbeck, and Jane S. Durch, editors. p. ; cm. Includes bibliographical references. ISBN 0-309-09949-8 — ISBN 0-309-65307-X 1. Deafness—Etiology. -

June 2017 Investment Update

Investment update As at 30 June 2017 Snapshot Pre-tax net tangible assets Gross assets $1.06 $42.0m Fully franked Performance dividend yield (p.a. since January 2008) wilsonassetmanagement.com.au 5.0% 12.6% ABN 49 126 420 719 WAM Active Limited Market overview ASX code WAA The S&P/ASX All Ordinaries Accumulation Index closed up 0.3% for the Listed Jan 2008 month, to finish the financial year up 13.1%, the best year for the market Gross assets $42.0m since 2014. The sectors that drove the advance during FY2017 were Market cap $42.7m materials (+20.6%), utilities (+14.7%), banks (+11.9%) and healthcare Share price (WAA) $1.10 (+11.8%). Option price (WAAO) $0.015 NTA before tax $1.06 Global equity markets ended the month down as central banks Shares on issue 38,802,828 foreshadowed the end of easy monetary policy. The US Federal Reserve Options on issue 31,680,247 raised interest rates for the third consecutive time to between 1% to 1.25% Annualised fully franked 5.5c in response to improving confidence in the US economy. interim dividend (FY2017) Fully franked dividend yield 5.0% In Australia, the unemployment rate fell to a lower than expected 5.5% from 5.7% the previous month, the lowest level since February 2013. The political Investment objectives attack on banks continued with the South Australian Government • Deliver shareholders a regular income announcing it would introduce a bank tax in addition to the Federal stream via fully franked dividends Government’s levy. -

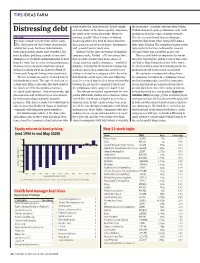

Distressing Debt Seek out Shares in the Lowest Quality Companies; Verdad Compared Equity Performance with Credit the Worst-Of-The-Worst, If You Like

TIPS IDEAS FARM want to play the ‘dash for trash’ should simply the issue price. A similar story was found when Distressing debt seek out shares in the lowest quality companies; Verdad compared equity performance with credit the worst-of-the-worst, if you like. However, quality based on the scores of rating agencies. ALGY HALL ignoring ‘quality’ when it comes to buying Here the research found share performance t’s been a tough time for short sellers lately. beaten-up stocks (the kind of shares found on started to deteriorate when ratings fell below a IThe ‘dash for trash’ that I wrote about in this these pages in our tables of shorts, downgrades high single B rating. The annualised equity return column last week, has been indiscriminate. and 52-week lows) is rarely wise. from stocks in the least creditworthy category Even real no-hoper shares have benefited. The Intrigued by the price movement of bankrupt- (CC and below) was a negative 34 per cent. most headline-grabbing example of investors’ company stocks, Verdad – a US investment firm This research holds an important lesson for willingness to overlook all fundamentals in their that specialises in investing in the shares of investors targeting the grubbier end of this recov- hunt for ‘trash’ has been the strong performance cheap, indebted, smaller companies – trawled its ery. Rather than buying the worst-of-the-worst, of shares in US companies that have already database. It looked for the long-term relationship it’s the best-of-the-worst that should provide the declared bankruptcy or are about to (Hertz, JC between share price performance and the level optimal trade-off between risk and reward. -

DATABANK INSIDE the CITY SABAH MEDDINGS the WEEK in the MARKETS the ECONOMY Consumer Prices Index Current Rate Prev

10 The Sunday Times November 11, 2018 BUSINESS Andrew Lynch LETTERS “The fee reflects the cleaning out the Royal Mail Send your letters, including food sales at M&S and the big concessions will be made for Delia’s fingers burnt by online ads outplacement amount boardroom. Don’t count on it SIGNALS full name and address, supermarkets — self-service small businesses operating charged by a major company happening soon. AND NOISE . to: The Sunday Times, tills. These are hated by most retail-type operations, but no Delia Smith’s website has administration last month for executives at this level,” 1 London Bridge Street, shoppers. Prices are lower at such concessions would been left with a sour taste owing hundreds of says Royal Mail, defending London SE1 9GF. Or email Lidl and other discounters, appear to be available for after the collapse of Switch thousands of pounds to its the Spanish practice. BBC friends [email protected] but also you can be served at businesses occupying small Concepts, a digital ad agency clients. Delia, 77 — no You can find such advice Letters may be edited a checkout quickly and with a industrial workshop or that styled itself as a tiny stranger to a competitive for senior directors on offer reunited smile. The big supermarkets warehouse units. challenger to Google. game thanks to her joint for just £10,000 if you try. Eyebrows were raised Labour didn’t work in the have forgotten they need Trevalyn Estates owns, Delia Online, a hub for ownership of Norwich FC — Quite why the former recently when it emerged 1970s, and it won’t again customers. -

JH Inv Funds Series I OEIC AR 05 2021.Indd

ANNUAL REPORT & ACCOUNTS For the year ended 31 May 2021 Janus Henderson Investment Funds Series I Janus Henderson Investment Funds Series I A Who are Janus Henderson Investors? Global Strength 14% 13% £309.6B 55% 45% 31% 42% Assets under Over 340 More than 2,000 25 Over 4,300 management Investment professionals employees Offi ces worldwide companies met by investment teams in 2020 North America EMEA & LatAm Asia Pacifi c Source: Janus Henderson Investors, Staff and assets under management (AUM) data as at 30 June 2021. AUM data excludes Exchange-Traded Note (ETN) assets. Who we are Janus Henderson Investors (‘Janus Henderson’) is a global asset manager off ering a full suite of actively managed investment products across asset classes. As a company, we believe the notion of ‘connecting’ is powerful – it has shaped our evolution and our world today. At Janus Henderson, we seek to benefi t clients through the connections we make. Connections enable strong relationships based on trust and insight aswell as the fl ow of ideas among our investment teams and our engagement with companies. These connections are central to our values, to what active management stands for and to the long-term outperformance we seek to deliver. Our commitment to active management off ers clients the opportunity to outperform passive strategies over the course of market cycles. Through times of both market calm and growing uncertainty, our managers apply their experience weighing risk versus reward potential – seeking to ensure clients are on the right side of change. Why Janus Henderson Investors At Janus Henderson, we believe in linking our world-class investment teams and experienced global distribution professionals with our clients around the world. -

Download Valuing Radio

Valuing Radio How commercial radio contributes to the UK A report by the All-Party Parliamentary Group on Commercial Radio The data within Valuing Radio is largely drawn from a 2018 survey of Radiocentre members. It is supplemented by additional research which is sourced individually. Contents 01 Introduction 03 Overview and recommendations 05 The public value of commercial radio • News and information • Economic value • Charity and community 21 Commercial radio people 27 Future of radio Introduction The APPG on Commercial Radio helps provide this important industry with a voice in parliament. With record audiences and more ways to listen than ever before, the impact of the industry should not be underestimated. While the challenges facing the sector have changed over the years, the steadfast commitment of stations to provide public value content every day remains. This new report, the first of its kind produced by the APPG, showcases the rich public value content that commercial radio provides to listeners for free. Valuing Radio explores the impact made by stations up and down the country, over and above the music and entertainment output that audiences expect. It looks particularly at radio’s role in providing news and information, the sector’s significant support for both charitable fundraising and education, in addition to work to improve diversity within the industry. Alongside this important public value content is a significant economic contribution to local economies across the UK. For the first time we have analysis on the impact of local advertising and the return on investment (ROI) that this generates for particular nations and regions of the UK.