ES River and Mercantile UK Recovery Fund

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

May CARG 2020.Pdf

ISSUE 30 – MAY 2020 ISSUE 30 – MAY ISSUE 29 – FEBRUARY 2020 Promoting positive mental health in teenagers and those who support them through the provision of mental health education, resilience strategies and early intervention What we offer Calm Harm is an Clear Fear is an app to Head Ed is a library stem4 offers mental stem4’s website is app to help young help children & young of mental health health conferences a comprehensive people manage the people manage the educational videos for students, parents, and clinically urge to self-harm symptoms of anxiety for use in schools education & health informed resource professionals www.stem4.org.uk Registered Charity No 1144506 Any individuals depicted in our images are models and used solely for illustrative purposes. We all know of young people, whether employees, family or friends, who are struggling in some way with mental health issues; at ARL, we are so very pleased to support the vital work of stem4: early intervention really can make a difference to young lives. Please help in any way that you can. ADVISER RANKINGS – CORPORATE ADVISERS RANKINGS GUIDE MAY 2020 | Q2 | ISSUE 30 All rights reserved. No part of this publication may be reproduced or transmitted The Corporate Advisers Rankings Guide is available to UK subscribers at £180 per in any form or by any means (including photocopying or recording) without the annum for four updated editions, including postage and packaging. A PDF version written permission of the copyright holder except in accordance with the provision is also available at £360 + VAT. of copyright Designs and Patents Act 1988 or under the terms of a licence issued by the Copyright Licensing Agency, Barnard’s Inn, 86 Fetter Lane, London, EC4A To appear in the Rankings Guide or for subscription details, please contact us 1EN. -

Morning Wrap

Morning Wrap Today ’s Newsflow Equity Research 19 Jul 2019 08:16 BST Upcoming Events Select headline to navigate to article Paper and Packaging Stora Enso reports weak Q2, Company Events flagging lower box prices 19-Jul Close Brothers Group; Q419 Trading Update Stora Enso ; Q219 Results Building Materials US non-residential forecasts are 23-Jul Paragon Banking; Q319 Trading Update revised down 24-Jul Britvic; Q319 Trading Update Kindred Group; Q219 Results UK Banks CBG issues a disappointing pre-close trading Marston's; Q319 Trading Update Metro Bank; Q219 Results update – NIM in focus 25-Jul AIB Group; Q219 Results Bankinter; Q219 Results Breedon Group; Interim results Howden Joinery; H1 results International Paper; Q219 Results Permanent TSB; Q219 Results Tyman; H1 results Unilever PLC; Q219 Results Wizz Air; Q120 Results Economic Events Ireland 22-Jul PPI June19 Wholesale Price Index June19 26-Jul Retail Sales June19 United Kingdom 23-Jul CBI Industrial Trends July19 25-Jul CBI Distributive Trades July19 United States Europe This document is intended for the sole use of Goodbody Stockbrokers and its affiliates Goodbody Capital Markets Equity Research +353 1 6419221 Equity Sales +353 1 6670222 Bloomberg GDSE<GO> Goodbody Stockbrokers UC, trading as “Goodbody”, is regulated by the Central Bank of Ireland. In the UK, Goodbody is authorised and subject to limited regulation by the Financial Conduct Authority. Goodbody is a member of the Irish Stock Exchange and the London Stock Exchange. Goodbody is a member of the FEXCO group of companies. For the attention of US clients of Goodbody Securities Inc, this third-party research report has been produced by our affiliate, Goodbody Stockbrokers Goodbody Morning Wrap Paper and Packaging Stora Enso reports weak Q2, flagging lower box prices Stora Enso has reported Q2 results to the end of June. -

Annual Report and Accounts for the Year Ended 31 December 2020

Tyman plc Annual report and accounts TYMAN PLC for the year ended 31 December 2020 Annual report and accounts for the year ended 31 December 2020 Annual report and accounts for the year The expert touch that transforms Tyman is a leading international supplier of engineered fenestration components and access solutions to the construction industry. Highlights • Strong recovery from COVID-19 in H2 saw growth of 5% against £572.8m 1.1× 4.0p £100.6m H2 2019; full year LFL revenue down 6% Revenue Leverage* Dividend per share Adjusted net debt* • Cost reductions and benefits of self-help initiatives mitigated the full (2019: £613.7m) (2019: 1.7×) (2019: 3.9p) (2019: £164.5m) year revenue shortfall, resulting in adjusted operating margin slightly ahead of 2019 and LFL adjusted operating profit down only 6% • Good progress on self-help measures: £80.3m 27.2p £47.6m 19.1p − Encouraging level of North American customer wins Adjusted operating profit* Adjusted earnings per share* Profit before taxation Basic earnings per share − Successful execution of planned footprint realignments (2019: £85.4m) (2019: 27.5p) (2019: £24.8m) (2019: 9.1p) − Momentum gained with continuous improvement activities • Strategic initiatives continued to bear fruit, driving market share gains across the Group • Reduction in safety incidents of 22% indicative of operational excellence progress • Strong cash generation with cash conversion of 131% and reduction in leverage to 1.1x, achieving low-end of new target range • Repayment in December 2020 of £2.3m received under -

Parker Review

Ethnic Diversity Enriching Business Leadership An update report from The Parker Review Sir John Parker The Parker Review Committee 5 February 2020 Principal Sponsor Members of the Steering Committee Chair: Sir John Parker GBE, FREng Co-Chair: David Tyler Contents Members: Dr Doyin Atewologun Sanjay Bhandari Helen Mahy CBE Foreword by Sir John Parker 2 Sir Kenneth Olisa OBE Foreword by the Secretary of State 6 Trevor Phillips OBE Message from EY 8 Tom Shropshire Vision and Mission Statement 10 Yvonne Thompson CBE Professor Susan Vinnicombe CBE Current Profile of FTSE 350 Boards 14 Matthew Percival FRC/Cranfield Research on Ethnic Diversity Reporting 36 Arun Batra OBE Parker Review Recommendations 58 Bilal Raja Kirstie Wright Company Success Stories 62 Closing Word from Sir Jon Thompson 65 Observers Biographies 66 Sanu de Lima, Itiola Durojaiye, Katie Leinweber Appendix — The Directors’ Resource Toolkit 72 Department for Business, Energy & Industrial Strategy Thanks to our contributors during the year and to this report Oliver Cover Alex Diggins Neil Golborne Orla Pettigrew Sonam Patel Zaheer Ahmad MBE Rachel Sadka Simon Feeke Key advisors and contributors to this report: Simon Manterfield Dr Manjari Prashar Dr Fatima Tresh Latika Shah ® At the heart of our success lies the performance 2. Recognising the changes and growing talent of our many great companies, many of them listed pool of ethnically diverse candidates in our in the FTSE 100 and FTSE 250. There is no doubt home and overseas markets which will influence that one reason we have been able to punch recruitment patterns for years to come above our weight as a medium-sized country is the talent and inventiveness of our business leaders Whilst we have made great strides in bringing and our skilled people. -

Announcing: Finalists Circle for the Prestigious M&A

GLOBAL MAJOR MARKETS CONGRATULATIONS to all the OUTSTANDING FINALISTS of the YEAR, 2014 ANNUAL AWARDS GALA DINNER June 12, 2014, New YORK, USA. Global M&A Network congratulates the distinguished group of finalists nominees for the one and only, GLOBAL MAJOR MARKETS, M&A ATLAS AWARDS. Prestigious awards exclusively honors excellence from all corners of the globe for executing M&A transactions valued above a billion dollars as always in the categories of: 40 Deal, 7 Outstanding Firm and 4 Global M&A Dealmakers of the Year awards. In a highly competitive process, a total of 185 transactions closed during January 2013 to January 31, 2014 were evaluated. From the pool of 185 deals, 106 deals are included in the finalists list. Eventually, only 40 deals will win at the annual awards gala. Prestige: Winning the M&A ATLAS AWARDS conveys a resounding message that the winner has accomplished the highest performance and excellence standards, worldwide. As always, the winners are selected independently for closing the best value-generating and game- changing transformational transactions based on identifiable criteria such as deal novelty/structure, sector/jurisdiction/market complexities, synergies/rationale/style, financial value, brand competitiveness, leadership, tenacity, resourcefulness and additional related metrics. Winners Circle Celebration: Winners are honored at the awards dinner trophy presentation ceremony held on June 12, 2014 at the Harvard Club of New York. WHAT to DO if you are among the coveted group of distinguished finalists? If you submitted nominations, please confirm your guest attendance for the annual Awards Gala Dinner, held on the evening of June 12, 2014, NY. -

Herbert Smith Freehills Boosts London Corporate Capability with Ecm Partner Hire

HERBERT SMITH FREEHILLS BOOSTS LONDON CORPORATE CAPABILITY WITH ECM PARTNER HIRE 23 June 2020 | London Firm news Leading global law firm Herbert Smith Freehills has hired Michael Jacobs to join its market leading Global Corporate practice as an Equity Capital Markets partner in London. Michael joins the firm from Allen & Overy where he was a partner. He returns to London from Hong Kong, where he has spent the last three years. Michael is an equity capital markets specialist and has represented listed companies, underwriters and investors on initial public offerings, secondary offerings and other strategic equity transactions. He also regularly advises listed corporates on the equity capital markets implications of public and private M&A transactions and restructurings. Prior to relocating to Hong Kong, Michael acted on the initial public offerings of Worldpay, Virgin Money, Hastings Insurance, Neinor Homes and The Gym Group and secondary capital raises by companies including Great Portland Estates, Sirius Minerals, Ophir Energy, Capitec Bank, GKN, Vedanta Energy and the recapitalisation and consensual bail in of the Co- operative Bank. Michael is recommended by Legal 500 for equity capital markets transactions. Michael also has considerable experience across mainstream corporate finance transactions, including public and private M&A, board-level corporate advisory work, restructurings and regulatory advice for clients including advising on cross-border deals which span a wide range of sectors, including financial institutions, fintech and growth capital. His M&A experience includes advising on Banco de Sabadell’s takeover of TSB Banking Group and the acquisition of Northern Rock by Virgin Money, as well as on transactions for Ping An, Go-Jek, Discovery Capital and Roivant Sciences during his time in Hong Kong. -

Annual Report 2019

Synthomer plc Annual Report 2019 BUILDING GLOBAL DIFFERENTIATION Synthomer plc We continue to make good progress towards our strategic objectives despite challenging market conditions in 2019. The acquisition of the highly complementary OMNOVA Solutions Inc will extend our geographic reach, expand our global platform and allow us to further differentiate our business. Our successful capital investment expansion programme in 2018/2019 positions us well to capture higher-than-market growth and extend our leadership positions in our core markets. Who we are Industrial Specialities is focused on our speciality Synthomer is a speciality chemicals company and chemical additives and non-water-based one of the world’s leading suppliers of water-based chemistry for a broad range of applications from polymers. With strong geographic and end market polymer additives and monomers to emerging diversity combined with product differentiation, materials and technologies. Synthomer holds leadership positions in a wide Our culture range of markets including coatings, construction, Synthomer is fully committed to building a textiles, paper and healthcare. business where the people, purpose, culture Our purpose and values of the Group are fully aligned. Revenue As a global leader in water-based polymer Synthomer is a diverse global company with an 43% chemistry, our purpose is to continually innovate inclusive culture which embodies meritocracy, 42% 15% to meet the needs of our customers and society openness, fairness and transparency. in a sustainable way. 3 Our values What we do Synthomer has five core values. At the heart We operate through three global businesses – of our business is SHE (Safety, Health and 1 Performance Elastomers (PE); Environmental) – we always have time to work Functional Solutions (FS); and safely. -

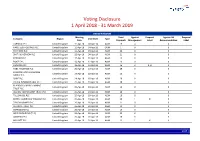

Global Voting Activity Report to March 2019

Voting Disclosure 1 April 2018 - 31 March 2019 UNITED KINGDOM Meeting Total Against Proposal Against ISS Proposal Company Region Vote Date Type Date Proposals Management Label Recommendation Label CARNIVAL PLC United Kingdom 11-Apr-18 04-Apr-18 AGM 19 0 0 HANSTEEN HOLDINGS PLC United Kingdom 11-Apr-18 04-Apr-18 OGM 1 0 0 RIO TINTO PLC United Kingdom 11-Apr-18 04-Apr-18 AGM 22 0 0 SMITH & NEPHEW PLC United Kingdom 12-Apr-18 04-Apr-18 AGM 21 0 0 PORVAIR PLC United Kingdom 17-Apr-18 10-Apr-18 AGM 15 0 0 BUNZL PLC United Kingdom 18-Apr-18 12-Apr-18 AGM 19 0 0 HUNTING PLC United Kingdom 18-Apr-18 12-Apr-18 AGM 16 2 3, 8 0 HSBC HOLDINGS PLC United Kingdom 20-Apr-18 13-Apr-18 AGM 29 0 0 LONDON STOCK EXCHANGE United Kingdom 24-Apr-18 18-Apr-18 AGM 26 0 0 GROUP PLC SHIRE PLC United Kingdom 24-Apr-18 18-Apr-18 AGM 20 0 0 CRODA INTERNATIONAL PLC United Kingdom 25-Apr-18 19-Apr-18 AGM 18 0 0 BLACKROCK WORLD MINING United Kingdom 25-Apr-18 19-Apr-18 AGM 15 0 0 TRUST PLC ALLIANZ TECHNOLOGY TRUST PLC United Kingdom 25-Apr-18 19-Apr-18 AGM 10 0 0 TULLOW OIL PLC United Kingdom 25-Apr-18 19-Apr-18 AGM 16 0 0 BRITISH AMERICAN TOBACCO PLC United Kingdom 25-Apr-18 19-Apr-18 AGM 20 1 8 0 TAYLOR WIMPEY PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 21 0 0 ALLIANCE TRUST PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 13 0 0 SCHRODERS PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 19 0 0 WEIR GROUP PLC (THE) United Kingdom 26-Apr-18 20-Apr-18 AGM 23 0 0 AGGREKO PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 20 0 0 MEGGITT PLC United Kingdom 26-Apr-18 20-Apr-18 AGM 22 1 4 0 1/47 -

Fund Holdings

Wilmington International Fund as of 7/31/2021 (Portfolio composition is subject to change) ISSUER NAME % OF ASSETS ISHARES MSCI CANADA ETF 3.48% TAIWAN SEMICONDUCTOR MANUFACTURING CO LTD 2.61% DREYFUS GOVT CASH MGMT-I 1.83% SAMSUNG ELECTRONICS CO LTD 1.79% SPDR S&P GLOBAL NATURAL RESOURCES ETF 1.67% MSCI INDIA FUTURE SEP21 1.58% TENCENT HOLDINGS LTD 1.39% ASML HOLDING NV 1.29% DSV PANALPINA A/S 0.99% HDFC BANK LTD 0.86% AIA GROUP LTD 0.86% ALIBABA GROUP HOLDING LTD 0.82% TECHTRONIC INDUSTRIES CO LTD 0.79% JAMES HARDIE INDUSTRIES PLC 0.78% DREYFUS GOVT CASH MGMT-I 0.75% INFINEON TECHNOLOGIES AG 0.74% SIKA AG 0.72% NOVO NORDISK A/S 0.71% BHP GROUP LTD 0.69% PARTNERS GROUP HOLDING AG 0.65% NAVER CORP 0.61% HUTCHMED CHINA LTD 0.59% LVMH MOET HENNESSY LOUIS VUITTON SE 0.59% TOYOTA MOTOR CORP 0.59% HEXAGON AB 0.57% SAP SE 0.57% SK MATERIALS CO LTD 0.55% MEDIATEK INC 0.55% ADIDAS AG 0.54% ZALANDO SE 0.54% RIO TINTO LTD 0.52% MERIDA INDUSTRY CO LTD 0.52% HITACHI LTD 0.51% CSL LTD 0.51% SONY GROUP CORP 0.50% ATLAS COPCO AB 0.49% DASSAULT SYSTEMES SE 0.49% OVERSEA-CHINESE BANKING CORP LTD 0.49% KINGSPAN GROUP PLC 0.48% L'OREAL SA 0.48% ASSA ABLOY AB 0.46% JD.COM INC 0.46% RESMED INC 0.44% COLOPLAST A/S 0.44% CRODA INTERNATIONAL PLC 0.41% AUSTRALIA & NEW ZEALAND BANKING GROUP LTD 0.41% STRAUMANN HOLDING AG 0.41% AMBU A/S 0.40% LG CHEM LTD 0.40% LVMH MOET HENNESSY LOUIS VUITTON SE 0.39% SOFTBANK GROUP CORP 0.39% NOVARTIS AG 0.38% HONDA MOTOR CO LTD 0.37% TOMRA SYSTEMS ASA 0.37% IMCD NV 0.37% HONG KONG EXCHANGES & CLEARING LTD 0.36% AGC INC 0.36% ADYEN -

Tyman Plc Annual Report and Accounts 2016 Accounts and Report Annual

Tyman plc Tyman Annual Report and Accounts 2016 A year of growth Tyman plc Annual Report and Accounts 2016 Further progress and growth through acquisitions Tyman is a leading international supplier of engineered components to the door and window industry. At 31 December 2016 the Group had 23 manufacturing sites in eight countries along with a further 18 sourcing and distribution sites across North America, Europe, South America, Asia and Australasia with its products being found in homes and buildings worldwide. Operational highlights Financial highlights • Year of profitable growth assisted by contributions from strategic acquisitions and favourable exchange rates Revenue Dividend per share • Integration of the three acquisitions completed in the year now well advanced £457.6m 10.50p 2015: £353.4m +29% 2015: 8.75p +20% • Synergy targets for both Giesse and Bilco now expected to be achieved by the end of 2017 - significantly ahead of schedule Underlying operating profit Underlying net debt • Strong cash generation and tight control over working £69.8m £176.7m capital taking Leverage back below 2.00x at the year end 2015: £51.4m +36% 2015: £83.2m (112)% • Dividend increased by 20.0 per cent to reflect improved cash generation and profitability Profit before taxation Leverage • Continued margin progression in AmesburyTruth despite limited volume growth £29.4m 1.89x 2015: £15.6m +89% 2015: 1.35x • Stronger second half for ERA with UK markets holding up better than expected post the EU Referendum Underlying earnings per share Return on capital -

MI Chelverton UK Equity Income Fund

MI Chelverton UK Equity Income Fund Investment Objective and Policy Monthly Fact Sheet The objective of the Fund is to provide a progressive income stream and achieve long-term capital growth by investing primarily in a portfolio of fully listed and AIM traded UK equities. The Fund will 31 May 2021 invest in UK companies which aim to provide a high initial dividend, progressive dividend payments and long term capital appreciation. Launch Date 4 December 2006 Monthly Manager Commentary Fund Size £527m A relatively quiet month in terms of corporate results and news flow was dominated by Q1 trading Historic Yield 2.32% updates. Pleasingly these were generally positive and have served to underpin the ‘recovery’ trade in a wide range of our holdings. Having been overly pessimistic a year or so ago, analysts are firmly in ‘upgrade’ The historic yield reflects distributions over the mode as profit expectations are being revised upwards, generating positive share price momentum. We past 12 months as a percentage of the price of the B share class as at the date shown. It does hope to see this bounce in current earnings gradually start to be reflected in improving dividend payments not include any initial charge and investors may as Boards confidence in their trading outlook starts to improve. For the moment investors are happy to be subject to tax on their distributions. look through any potential changes in the government’s roadmap back to normality and appear sanguine about any short term volatility in domestic macro numbers. The consensus is still that any pick up in inflation will only be temporary although we are less convinced on this front and will be looking for any Share Price (as at 31.05.21) signs of sustained wage inflation which may undermine this view. -

List of Public Interest Entities

www.pwc.co.uk/transparencyreport List of public interest entities List of public interest entities to accompany Transparency Report Year ended 30 June 2014 2 PricewaterhouseCoopers LLP UK Transparency Report FY14 List of public interest entities Please note – this list includes those 258 audit clients, for whom we issued an audit opinion between 1 July 2013 and 30 June 2014, who have issued transferable securities on a regulated market (as defined in the Statutory Auditors (Transparency) Instrument 2008 (POB 01/2008). 4IMPRINT GROUP PLC BOS (SHARED APPRECIATION MORTGAGES) NO. 1 PLC ABERFORTH GEARED INCOME TRUST PLC BOS (SHARED APPRECIATION MORTGAGES) NO. 2 PLC AFRICAN BARRICK GOLD PLC BOS (SHARED APPRECIATION MORTGAGES) NO.3 PLC AGGREKO PLC BOS (SHARED APPRECIATION MORTGAGES) NO.4 PLC AMLIN PLC BOS (SHARED APPRECIATION MORTGAGES) NO.6 PLC ARKLE MASTER ISSUER PLC BRADFORD & BINGLEY PLC ARM HOLDINGS PLC BRAMMER PLC ASIA RESOURCE MINERALS Plc (formerly BUMI Plc) BRISTOL & WEST PLC ASIAN TOTAL RETURN INVESTMENT COMPANY PLC BRITISH AMERICAN TOBACCO PLC (formerly Henderson Asian Growth Trust Plc) BRITISH TELECOMMUNICATIONS PLC AVIVA PLC BT GROUP PLC AVON RUBBER PLC BURBERRY GROUP PLC BABCOCK INTERNATIONAL GROUP PLC CAIRN ENERGY PLC BAGLAN MOOR HEALTHCARE PLC CAMELLIA PLC BAILLIE GIFFORD JAPAN TRUST PLC CAPITAL & COUNTIES PROPERTIES PLC BAILLIE GIFFORD SHIN NIPPON PLC CAPITAL GEARING TRUST PLC BANK OF SCOTLAND PLC CARNIVAL PLC BARCLAYS BANK PLC CARPETRIGHT PLC BARCLAYS PLC CARR’S MILLING INDUSTRIES PLC BERENDSEN PLC CATLIN UNDERWRITING BIRMINGHAM