Opinions on Ministerial Notifications

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Dean Nalder by Appointment Your Liberal for Alfred Cove

MELVILLE CITY HERALD Volume 24 No 8 Melville City’s own INDEPENDENT newspaper 41 Cliff Street, Fremantle Saturday February 23, 2013 Letterboxed to Applecross, Alfred Cove, Ardross, Attadale, Bicton, Booragoon, Ph: 9430 7727 Fax 9430 7726 Applecross to Bicton Edition Brentwood, Melville, Mt Pleasant, Myaree and Palmyra. Email: [email protected] Locals ramp up protest by CARMELO AMALFI BEACH lovers drew a line in the sand this week against Fremantle sailing club’s plans to build a new boat ramp off South Beach. Locals say the ramp, planned for junior and disabled sailors, involves building a 75m spur off the existing groyne. The club has three launching jetties, two of which have silted up, and locals say it should redevelop existing facilities rather than encroach further on public land. On its website the council notes, “there is no current access to the water for people with a disability and junior sailors currently navigate through the • Mike Kenny draws a line in • continued page 2 the sand, making it clear he opposes Fremantle Sailing Visit the council’s website Club’s bid to develop a boat before February 28 to have ramp. Photo by Carmelo Amalfi your say. SaveFreo out of its economic and our• the decline of the arts; lack of transparency city with plans for by BRENDAN FOSTER cultural doldrums. • the West End becoming a Fremantle—what’s going on with Find the Fake Ad THIRTY Fremantle men and Mr Longley says the genesis ghost town; and, those plans? for G4F is regular but informal • the lack of linkage between “Who is making them at local & WIN a Chance women, amongst them a gatherings for coff ee, where the the port city’s separate precincts. -

Western Australia State Election 2017

RESEARCH PAPER SERIES, 2017–18 18 SEPTEMBER 2017 Western Australia state election 2017 Rob Lundie Politics and Public Administration Section Contents Introduction ................................................................................................ 2 Background ................................................................................................. 2 Electoral changes ................................................................................................ 2 2013 election ...................................................................................................... 2 Party leaders ....................................................................................................... 3 Aftermath for the WA Liberal Party ................................................................... 5 The campaign .............................................................................................. 5 Economic issues .................................................................................................. 5 Liberal/Nationals differences ............................................................................. 6 Transport ............................................................................................................ 7 Federal issues ..................................................................................................... 7 Party campaign launches .................................................................................... 7 Leaders debate .................................................................................................. -

Extract from Hansard [ASSEMBLY — Tuesday, 26 November 2019

Extract from Hansard [ASSEMBLY — Tuesday, 26 November 2019] p9281a-9287a Mr Dean Nalder; Mr Bill Marmion; Mr Simon Millman; Mr David Templeman; Dr Tony Buti; Mr Ben Wyatt PUBLIC WORKS AMENDMENT (WA BUILDING MANAGEMENT AUTHORITY ABOLITION) BILL 2019 Second Reading Resumed from 26 September. MR D.C. NALDER (Bateman) [7.01 pm]: I stand to make my contribution to the second reading debate on the Public Works Amendment (WA Building Management Authority Abolition) Bill 2019. By way of background, I acknowledge that the Building Management Authority was established in 1984 to facilitate capital raising for public works. Funds were only ever borrowed on two occasions—approximately $285 million in 1984 and $55 million in 1996. Both of these amounts were fully repaid by 2008. We know that an amendment act has basically made this authority redundant, and that it has been financially dormant since 2009. Annual reports indicate that there are no assets or liabilities, employees, bank accounts or investments. The opposition agrees with the government and supports the carriage of this bill for the abolition of these works. [Quorum formed.] Mr D.C. NALDER: Nonetheless, given that there are no liabilities, there is a precautionary measure, which I acknowledge is generally taken in cases like this. The amending legislation includes a provision that any assets, rights, liabilities or obligations of the Western Australian Building Management Authority will be assigned to the Minister for Works on behalf of the state. On that basis, we feel very comfortable that this bill has taken into consideration all the necessary things to make sure that it is enacted correctly. -

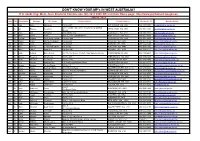

DON't KNOW YOUR MP's in WEST AUSTRALIA? If in Doubt Ring: West

DON'T KNOW YOUR MP's IN WEST AUSTRALIA? If in doubt ring: West. Aust. Electoral Commission (08) 9214 0400 OR visit their Home page: http://www.parliament.wa.gov.au HOUSE : MLA Hon. Title First Name Surname Electorate Postal address Postal Address Electorate Tel Member Email Ms Lisa Baker Maylands PO Box 907 INGLEWOOD WA 6932 (08) 9370 3550 [email protected] Unit 1 Druid's Hall, Corner of Durlacher & Sanford Mr Ian Blayney Geraldton GERALDTON WA 6530 (08) 9964 1640 [email protected] Streets Dr Tony Buti Armadale 2898 Albany Hwy KELMSCOTT WA 6111 (08) 9495 4877 [email protected] Mr John Carey Perth Suite 2, 448 Fitzgerald Street NORTH PERTH WA 6006 (08) 9227 8040 [email protected] Mr Vincent Catania North West Central PO Box 1000 CARNARVON WA 6701 (08) 9941 2999 [email protected] Mrs Robyn Clarke Murray-Wellington PO Box 668 PINJARRA WA 6208 (08) 9531 3155 [email protected] Hon Mr Roger Cook Kwinana PO Box 428 KWINANA WA 6966 (08) 6552 6500 [email protected] Hon Ms Mia Davies Central Wheatbelt PO Box 92 NORTHAM WA 6401 (08) 9041 1702 [email protected] Ms Josie Farrer Kimberley PO Box 1807 BROOME WA 6725 (08) 9192 3111 [email protected] Mr Mark Folkard Burns Beach Unit C6, Currambine Central, 1244 Marmion Avenue CURRAMBINE WA 6028 (08) 9305 4099 [email protected] Ms Janine Freeman Mirrabooka PO Box 669 MIRRABOOKA WA 6941 (08) 9345 2005 [email protected] Ms Emily Hamilton Joondalup PO Box 3478 JOONDALUP WA 6027 (08) 9300 3990 [email protected] Hon Mrs Liza Harvey Scarborough -

WA Ministerial Arrangements Further Information

Barton Deakin Brief: WA Ministry 26 September 2016 The Premier of Western Australia, the Hon Colin Barnett MLA, has announced several changes to the WA Ministry. These changes were required after the resignation of two former ministers, Minister for Agriculture and Food and Minister for Transport, Hon Dean Nalder MLA and the Minister for Minister for Local Government, Minister for Community Services, Minister for Seniors and Volunteering, and Minister for Youth, the Hon Tony Simpson MLA. WA Ministerial Arrangements The changes to the WA Ministry are outlined below: The Hon Mark Lewis MLC, Member of the Legislative Council for Mining and Pastoral Region, is the new Minister for Agriculture and Food; The Hon Paul Miles MLA, Member for North Metropolitan Region, is the new Minister for Local Government in addition to his existing role as Minister for Community Services, Minister for Seniors and Volunteering and Minister for Youth; The Hon Bill Marmion MLA, in addition to his role as Minister for State Development and Innovation, adds Transport; The Hon Sean L’Estrange MLA retains the Mines and Petroleum as well as Small Business and adds Finance. The new Ministers were sworn into their new positions by the Governor of Western Australia, HE the Hon Kerry Sanderson AO on Friday. A full list of the WA Ministry is enclosed. The next WA State Election will be held on Saturday 11 March 2017. Further Information The media release from the Premier which summarises the changes to the WA Ministry can be read here. For more information please contact Eacham Curry on +61 428 933 130 or Jessica Yu on +61 2 9191 7888. -

![Extract from Hansard [ASSEMBLY — Thursday, 16 August 2018] P4759b](https://docslib.b-cdn.net/cover/7070/extract-from-hansard-assembly-thursday-16-august-2018-p4759b-2347070.webp)

Extract from Hansard [ASSEMBLY — Thursday, 16 August 2018] P4759b

Extract from Hansard [ASSEMBLY — Thursday, 16 August 2018] p4759b-4781a Mr Paul Papalia; Mr Ben Wyatt; Dr Mike Nahan; Mr Dean Nalder; Mr Bill Marmion; Mr Peter Katsambanis; Mr Vincent Catania; Acting Speaker DUTIES AMENDMENT (ADDITIONAL DUTY FOR FOREIGN PERSONS) BILL 2018 Second Reading Resumed from 15 August. MR P. PAPALIA (Warnbro — Minister for Tourism) [10.16 am]: I have a contribution to make on the Duties Amendment (Additional Duty for Foreign Persons) Bill 2018. At the outset I make an observation about the extraordinary position the Liberal and National Party scallywags are taking on another revenue-raising opportunity that I thought everyone in Western Australia would support—that is, the opportunity to ensure that foreign property speculators contribute to education outcomes for Western Australians. What a wonderful policy and incredible opportunity. As I understand it, the opposition’s objections lie somewhere around the suggestion that mirroring the same rate of additional levy on foreign investors as every other jurisdiction in the country is somehow perverse and wrong—it is an extraordinary suggestion; a ridiculous idea—and that somehow we will drive foreign investors away and that will have a terrible impact on the Western Australian housing construction market. I think that is where the opposition is going. Is it housing construction or just the general property market? I am not really sure, shadow Treasurer. Mr D.C. Nalder: The general property market. Mr P. PAPALIA: It is the general property market. Based on the 2016–17 -

P7906a-7921A Dr Tony Buti

Extract from Hansard [ASSEMBLY — Thursday, 12 November 2020] p7906a-7921a Dr Tony Buti; Mr Dean Nalder; Mr Simon Millman; Mrs Lisa O'Malley; Mr Peter Rundle; Mr David Michael; Mr John McGrath; Mr Mick Murray; Mr Bill Marmion; Mr Peter Katsambanis; Ms Rita Saffioti; Mr Shane Love PUBLIC ACCOUNTS COMMITTEE Seventeenth Report — “More Than Just a Game: The Use of State Funds by the WA Football Commission” — Tabling DR A.D. BUTI (Armadale) [10.27 am]: I present for tabling the seventeenth report of the Public Accounts Committee titled “More Than Just a Game: The Use of State Funds by the WA Football Commission”. I also present for tabling the submissions to the inquiry. [See papers 3980 and 3981.] Dr A.D. BUTI: Football, or Aussie Rules, has played a significant role in the lives of Western Australians for more than 130 years. As former Premier Dr Geoff Gallop remarked, “No sport has had such a critical impact on our social and cultural development as Australian Football.” Football is a game that develops tribal loyalties and arouses passions, but it is also more than just a game. As noted by Dr Neale Fong, a former chair of the West Australian Football Commission, the history of football in Western Australia is not only about footballers, clubs and supporters, it also involves relationships with networks of politicians, governments, businesses and personalities involved in the game. The West Australian Football Commission, established in 1989, is the body charged with responsibility for the overall development and strategic direction of football in this state. The creation of the West Australian Football Commission is unique to WA. -

The March 2013 Western Australian Election

106 The March 2013 Western Australian election: first fixed election date delivers a resounding victory for the Barnett government 1 Harry Phillips Harry Phillips is a Parliamentary Fellow (Education) at the Parliament of WA, and Honorary 3URIHVVRUDW(GLWK&RZDQ8QLYHUVLW\DQGDQ$GMXQFW3URIHVVRUDW&XUWLQ8QLYHUVLW\/L].HUULV the Clerk Assistant (Committees) in the WA Legislative Assembly Historically, the pattern in Western Australia (WA) has been for respective governments to serve their full terms. In August 2008, Premier Alan Carpenter broke with tradition and FDOOHGDQHOHFWLRQVRPHVL[PRQWKVHDUO\ZKLFKFRQWULEXWHGWRDQDOOSDUW\FDOOIRUÀ[HG term governments. Carpenter’s Labor government lost power at that election, and in a ¶KXQJSDUOLDPHQW·WKHQHZ/LEHUDO3DUW\3UHPLHU&ROLQ%DUQHWWEHJDQWKHTXHVWIRUÀ[HG term elections in WA. Complications around the entrenchment provisions in the relevant OHJLVODWLRQPHDQWDÀ[HGHOHFWLRQGDWHZDVHDVLHUWRDFKLHYHWKDQDÀ[HGIRXU\HDUWHUP &RQVHTXHQWO\WKHDPHQGPHQWVÀ[HGWKHGDWHIRU/HJLVODWLYH&RXQFLOHOHFWLRQVWRRFFXURQ the second Saturday in March every four years, beginning 9 March 2013, and provided for DFRQMRLQWJHQHUDOHOHFWLRQWRRFFXUZKHQWKH/HJLVODWLYH$VVHPEO\LVGLVVROYHGRUH[SLUHV after 1 November in the prior year. Hence, the second Saturday in March from 2013 was WKHDJUHHGGDWHIRUWKHÀUVWHOHFWLRQXQGHUWKHQHZSURYLVLRQV:LGHVSUHDGVSHFXODWLRQ RFFXUUHGDVWRKRZDÀ[HGGDWHZRXOGDOWHUWKHFDPSDLJQVWUDWHJLHVRIWKHSROLWLFDO parties. The Premier contended the campaign would not begin until after Australia Day, 26 January 2013, but the parliamentary parties were -

Extract from Hansard [ASSEMBLY

Extract from Hansard [ASSEMBLY — Tuesday, 13 August 2019] p5381b-5440a Mrs Alyssa Hayden; Mr Sean L'Estrange; Ms Libby Mettam; Mr Kyran O'Donnell; Dr Mike Nahan; Mr Stephen Price; Ms Jessica Shaw; Ms Lisa Baker; Mr John Carey; Ms Janine Freeman; Mr Yaz Mubarakai; Mrs Liza Harvey; Mr Zak Kirkup; Mr Peter Katsambanis; Mr Dean Nalder; Mr Tony Krsticevic; Mr Paul Papalia; Dr Tony Buti; Mr David Templeman SMALL BUSINESS DEVELOPMENT CORPORATION AMENDMENT BILL 2019 Second Reading Resumed from 12 June. MRS A.K. HAYDEN (Darling Range) [4.45 pm]: It is my pleasure to stand today and say I will be the lead speaker for the Liberal Party opposition on the Small Business Development Corporation Amendment Bill 2019. At the start I would like to say that the Liberal Party opposition supports this bill in principle. It supports any legislation to protect and support our small business community. As a Liberal opposition we completely understand the importance of the small business sector. We will always stand up and support the sector. We understand how much it contributes to our state. I want to put on the record that the Liberal Party opposition fully supports any amendments that will assist small businesses and subcontractors. Before I go on, I would also like to make a special mention to the minister’s policy adviser, Emma Roebuck, who has been extremely helpful and professional. I want to thank her and show my gratitude for all her help. She has worked extremely hard and I appreciate it. Mr P. Papalia: She is very good, isn’t she? Mrs A.K. -

2018 State of the State

2018 State of the State Keynote speaker: The Hon. Mark McGowan MLA, Premier of Western Australia; WA Minister for Public Sector; State Development; Jobs and Trade; Federal-State Relations Thursday, 6 December 2018, 12.00pm to 2.00pm BelleVue Ballroom 1, Perth Convention and Exhibition Centre EVENT SPONSOR www.ceda.com.au agenda 11.45am Registrations 12.00pm Welcome to Country Barry McGuire, Managing Director, Redspear Safety 12.10pm Welcome Melinda Cilento, Chief Executive Officer, CEDA 12.15pm Introduction of the Premier of Western Australia Jeff Connolly, Chairman and Chief Executive Officer, Siemens 12.20pm Keynote address The Hon. Mark McGowan MLA, Premier of Western Australia; WA Minister for Public Sector; State Development; Jobs and Trade; Federal-State Relations 12.40pm Lunch 1.05pm Introduction of panel Deborah Terry AO, Vice-Chancellor, Curtin University 1.10pm Facilitated panel discussion and Q&A with Jessica Strutt, Chief State Political Reporter, ABC The Hon. Mark McGowan MLA, Premier of Western Australia; WA Minister for Public Sector; State Development; Jobs and Trade; Federal-State Relations The Hon. Simone McGurk MLA, Minister for Child Protection; Women’s Interests; Prevention of Family and Domestic Violence; Community Services The Hon. Benjamin Wyatt MLA, Treasurer; Minister for Finance; Energy; Aboriginal Affairs 1.50pm Vote of thanks Emil Ismayilov, Managing Director – Exploration and Production Australia, BP Australia 1.55pm Closing comments Paula Rogers, State Director, CEDA 2.00pm Event close sponsors Event major sponsor BP Australia Twitter: @BP_Australia BP is a global energy company with operations in more than 70 countries across six continents. It is proud to have been operating in Australia for nearly 100 years and will celebrate its Australian centenary in 2019. -

Dr Mike Nahan; Ms Mia Davies; Mrs Michelle Roberts; Mr John Mcgrath; Mr David Templeman; Mr Peter Rundle; Mr Mick Murray; Mr Dean Nalder; Mr Zak Kirkup; Speaker

Extract from Hansard [ASSEMBLY — Tuesday, 26 June 2018] p3834b-3844a Mr Mark McGowan; Dr Mike Nahan; Ms Mia Davies; Mrs Michelle Roberts; Mr John McGrath; Mr David Templeman; Mr Peter Rundle; Mr Mick Murray; Mr Dean Nalder; Mr Zak Kirkup; Speaker ARTHUR MARSHALL, OAM Condolence Motion MR M. McGOWAN (Rockingham — Premier) [2.01 pm] — without notice: I move — That this house records its sincere regret at the death of Mr Arthur Dix Marshall and tenders its deep sympathy to his family. I start by acknowledging the members of Arthur’s family who are here in the gallery today: his wife, Helen; his children Scott and Dixie; their partners, Megan and Luke; and his grandchildren Tom, Abby, Jack, Matilda and Charlie. Arthur Marshall was elected to this place in 1993 as the member for Murray. He is a member whom all sides of this chamber remember fondly. Born in 1934 in East Fremantle to parents, Horrie and Eunice, Arthur was for most of his life prior to his election a sportsman, and he descended from sporting stock. His father, Horrie, was a champion cyclist; his mother, Eunice, was club champion at East Fremantle Bowling Club; and grandfather Arthur was reportedly one of the top footballers in the goldfields until he was lured to East Fremantle Football Club for two shillings and sixpence a game plus a job on the wharf. Arthur, although known as a tennis player, also excelled as a footballer for East Fremantle and played table tennis and pennant squash. However, he excelled at tennis, and following some time on the European tour, qualified for Wimbledon in 1955, and again in 1956, when he made it to the third round. -

Power Lines Cook a Burra

FREMANTLE Ho ERALD Volume 23 N 1 Fremantleʼs own INDEPENDENT newspaper 41 Cliff Street, Fremantle Saturday January 7, 2012 Letterboxed to Fremantle, Beaconsfi eld, East Fremantle, Hilton, North Fremantle, Ph: 9430 7727 Fax 9430 7726 www.fremantleherald.com O’Connor, Samson, South Fremantle and White Gum Valley Email: [email protected] FIGHT THAT FLAB! Power STICK to that new year’s resolution and look and feel fab in 2012 with the Herald. Take on a delivery lines round and watch as your body tones and fi rms up. By next Christmas you’ll look and feel terrifi c! Lovely cook a Marie King has vacancies throughout Freo, Cockburn and Melville—there’s bound burra to be a round close to you! Call Marie today on 9430 7727. by BRAD JEFFERIES A KOOKABURRA came THE beach front at the old to a sad end in Bateman South Fremantle power Wednesday, electrocuting station site should be fenced itself on powerlines and off to the public because sparking a fi ve-hour blackout it is contaminated with to 1800 homes. cancer-causing chemicals, Western Power workers would environmentalists warn. Full normally just switch the power story, page 9 back on but because there’s a total fi re ban on they had to visually inspect the line, which took about an hour. Complicating matters was a passer-by speaking little english who saw the bird get fried and Taxpayers’ $17m who repeatedly yelled “shock! shock!” at a well-meaning local. The samaritan, assuming the by CARMELO AMALFI woman had been shocked, called an ambulance which scooted SOME $17 million of taxpayers’ the bewildered woman and her money has been handed to rescuer off to emergency.