Woolworths Limited/Lowe's Companies, Inc

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

For Personal Use Only Use Personal For

WOOLWORTHS LIMITED A.B.N 88 000 014 675 25 September 2009 The Manager, Companies Australian Stock Exchange Limited Company Announcements Office Level 4 20 Bridge Street SYDNEY NSW 2000 Dear Sir/Madam RE: Woolworths Limited – Annual Report 2009 – Listing Rule 4.5.1 Attached is a copy of the Woolworths Annual Report 2009. Printed copies of the Annual Report and Notice of Meeting for the Annual General Meeting to be held on 26 November 2009 will be mailed to shareholders shortly. For and on behalf of WOOLWORTHS LIMITED PETER J HORTON COMPANY SECRETARY For personal use only 1 Woolworths Way, Bella Vista, NSW 2153 PO Box 8000, Baulkham Hills, NSW 2153 Australia Telephone (02) 8885 0000 Facsimile (02) 8888 0001 WOOLWORTHS LIMITED ABN 88 000 014 675 ANNUAL REPORT 2009 For personal use only Page CONTENTS Chairman’s Report 7 Managing Director’s Report 9 The results in brief 12 Supermarkets 14 General Merchandise 19 Hotels 22 Capital management 24 Strategy and growth 26 Board of directors 29 Directors’ Statutory Report 32 Remuneration Report 36 Auditor’s Declaration 56 Corporate Governance 57 Financial Report to Shareholders 68 Shareholder information 174 For personal use only 2 HIGHLIGHTS • 12.8% NPAT growth at upper end of target range • Sales of $49,595 million, up 7.5% on a comparable 52 week basis. Excluding petrol sales increase 8.5% • Total sales for 52 weeks this year compared with 53 weeks last year up 5.4% to $49,595 million • 11.5% increase in Earnings Before Interest, Tax, Depreciation and Amortisation • 11.3% increase in Earnings Before -

ANNUAL REPORT 2009 Chairman’S Report

outside back cover 6mm outside front cover ANNUAL REPORT ABN 88 000 014 675 WOOL W ORTHS LIMITED ANNU LIMITED ORTHS A L L R EPORT 2009 EPORT inside front cover 6mm inside back cover contents aboUT this report COMPANY DIRECTORY Woolworths Limited Company Secretary Principal registered office in Australia Peter Horton 1 Woolworths Way Bella Vista NSW 2153 Share Registrar Tel: (02) 8885 0000 Computershare Investor Services Pty Limited Web: www.woolworthslimited.com.au Level 3 60 Carrington Street BIG W Sydney NSW 2000 Web: www.bigw.com.au Tel: 1300 368 664 Fax: (02) 8234 5050 Woolworths maintained National Supermarkets Web: www.computershare.com.au 2 Chairman’s its confidence and Web: www.woolworths.com.au Report certainty in the Auditor Australian economy Woolworths Petrol Deloitte Touche Tohmatsu 4 Managing during the year and remains very optimistic Tel: 1300 655 055 Director’s Grosvenor Place about the country’s Web: www.woolworthspetrol.com.au 225 George Street Report ability to withstand the Sydney NSW 2000 extraordinary fiscal events BWS 6 Highlights that have taken place. Tel: (02) 9322 7000 Web: www.beerwinespirits.com.au By continuing to grow Web: www.deloitte.com.au 10 The Results our company, create in brief employment and deliver Dan Murphy’s choice and value to 789 Heidelberg Road 12 Supermarkets customers, we will be Alphington VIC 3078 well positioned to reach Tel: (03) 9497 3388 18 General our 100th birthday Merchandise in 2024 as a vibrant, Fax: (03) 9497 2782 strong and dynamic Web: www.danmurphys.com.au MICHAEL LUSCOMBE Australian company. -

Woolworths Limited A.B.N 88 000 014 675

WOOLWORTHS LIMITED A.B.N 88 000 014 675 9 September 2010 The Manager, Companies Australian Securities Exchange Limited Company Announcements Office Level 4 20 Bridge Street SYDNEY NSW 2000 Dear Sir/Madam RE: Woolworths Limited – Annual Report 2010 – Listing Rule 4.5.1 Attached is a copy of the Woolworths Annual Report 2010. Printed copies of the Annual Report and Notice of Meeting for the Annual General Meeting to be held on 18 November 2010 will be mailed to shareholders shortly. For and on behalf of WOOLWORTHS LIMITED PETER J HORTON COMPANY SECRETARY 1 Woolworths Way, Bella Vista, NSW 2153 PO Box 8000, Baulkham Hills, NSW 2153 Australia Telephone (02) 8885 0000 Facsimile (02) 8888 0001 WOOLWORTHS LIMITED ABN 88 000 014 675 ANNUAL REPORT 2010 1 Page CONTENTS Highlights 3 Chairman‟s Report 4 Managing Director‟s Report 6 The results in brief 13 Supermarkets 15 General Merchandise 20 Hotels 26 Home Improvement 27 Capital management 28 Performance targets 32 Board of directors 33 Directors‟ Statutory Report 37 Remuneration Report 41 Auditor‟s Declaration 62 Corporate Governance 63 2 HIGHLIGHTS Sales of $51,694 million, up 4.8% excluding Petrol (including Petrol, up 4.2%) 9.4% increase in Earnings Before Interest, Tax, Depreciation and Amortisation 9.5% increase in Earnings Before Interest and Tax to $3,082.1 million 10.1% increase in Net Profit After Tax to $2,020.8 million attributable to equity holders of the parent entity 8.8% increase in Earnings Per Share to 164.0 cents 10.6% increase in fully franked Dividend to 115 cents per share Solid increase in operating cash flows Announcement of an off-market share Buy-Back to return $700 million to shareholders bringing capital returns in the 2010 year to over $1 billion 3 CHAIRMAN’S REPORT FROM STRENGTH TO STRENGTH The Board and management team of Woolworths Limited are delighted to report on another strong result by our company. -

Cold Hard Facts 3

Cold Hard Facts 3 Prepared for the Department of the Environment and Energy September 2018 Phone Web +61 3 9592 9111 www.expertgroup.com.au Table of Contents Glossary ..................................................................................................................................... 7 Abbreviations........................................................................................................................... 13 1 Executive summary ............................................................................................................ 15 2 Introduction ....................................................................................................................... 18 2.1 Structure of Cold Hard Facts 3 ................................................................................................................................ 19 3 Taxonomy of a technology ................................................................................................. 21 4 The stock of equipment ...................................................................................................... 23 4.1 The scale of events ....................................................................................................................................................... 23 4.2 Stationary air conditioning ....................................................................................................................................... 24 4.3 Mobile air conditioning ............................................................................................................................................. -

Woolworths Limited ATTN:ASSISTANT

Woolworths Limited Trademarks Matching '"Woolworths Limited"' by Service. IPMonitorTrademarks www.ipmonitor.com.au Contents Alerts 3 "Woolworths Limited" 3 Terms and Conditions 47 General 47 Disclaimer of warranty and limitation of liability 47 Copyright 47 Arbitration 47 www.ipmonitor.com.au Alerts "Woolworths Limited" More than 500 results matching '"Woolworths Limi...' by Service. Number Mark Owner Service 401288 John Danks & Son Pty Ltd ACN: Woolworths Limited Assistant 004037049 414 Lower Company Secretary PO Box Dandenong Road BRAESIDE 8000 BAULKHAM HILLS VIC 3195 AUSTRALIA NSW 2153 AUSTRALIA 1035964 Woolworths Limited Woolworths Limited Attn: C ACN/ARBN 000 014 675 Hesford PO Box Q70 QUEEN VICTORIA BUILDING NSW 1230 1000749 Woolworths Limited ACN: Woolworths Limited PO Box 000014675 8000 BAULKHAM HILLS NSW 2153 AUSTRALIA 922486 VINPAC Vinpac International Pty Ltd Woolworths Limited Assistant ACN: 008266779 Company Secretary PO Box 800 BAULKHAM HILLS NSW 2153 AUSTRALIA 943076 FRESH MAGAZINE Woolworths Limited ACN: Woolworths Limited PO Box 000014675 8000 BAULKHAM HILLS NSW 2153 AUSTRALIA 1037596 BIG W Vision Centre Woolworths Limited Woolworths Limited Attn: C ACN/ARBN 000 014 675 Hesford PO Box Q70 QVB Post Shop SYDNEY NSW 1230 1037677 FINISHING TOUCHES Woolworths Limited Woolworths Limited Attn: C ACN/ARBN 000 014 675 Hesford PO Box Q70 QVB Post Shop SYDNEY NSW 1230 1037782 Woolworths Limited Woolworths Limited Attn: C ACN/ARBN 000 014 675 Hesford PO Box Q70 QUEEN VICTORIA BUILDING NSW 1230 650374 TOLLEY Cellarmaster Wines Pty -

Annual Report 2010 2010 Inside Front Cover 6Mm Inside Back Cover

outside back cover 6mm outside front cover woolworths limited limited woolworths annual report 2010 annual report 2010 inside front cover 6mm inside back cover Company Directory Contents Chairman’s Report 2 sales of Managing Director’s Report 5 Highlights 7 $51.7 Supermarkets 12 billion, up General Merchandise 18 Woolworths Limited ALH Group Pty Ltd Hotels 24 2.1 billion Principal registered office in Australia – Registered Office 1 Woolworths Way 1 Woolworths Way Home Improvement 25 Bella Vista NSW 2153 Bella Vista NSW 2153 Capital Management 26 or 4.2% Tel: (02) 8885 0000 Tel: (02) 8885 0000 Web: www.woolworthslimited.com.au Web: www.alhgroup.com.au Board of Directors 30 (excluding petrol up 4.8%) – Victorian Office BIG W Directors’ Statutory Report 34 Ground Floor Web: www.bigw.com.au Remuneration Report 37 16–20 Claremont Street South Yarra VIC 3141 9.4% increase in National Supermarkets Auditor’s Declaration 57 Tel: (03) 9829 1000 Web: www.woolworths.com.au Corporate Governance Statement 58 earnings before – Queensland Office Level 1 Woolworths Petrol Financial Report to Shareholders 70 152 Oxford Street interest, tax, Tel: 1300 655 055 Bulimba QLD 4171 Shareholder Information 163 Web: www.woolworthspetrol.com.au depreciation and Tel: (07) 3909 4800 BWS Company Secretary amortisation Web: www.beerwinespirits.com.au Peter Horton Dan Murphy’s Share Registrar 789 Heidelberg Road Computershare Investor Services Pty Limited Alphington VIC 3078 Level 4 Tel: (03) 9497 3388 60 Carrington Street Fax: (03) 9497 2782 Sydney NSW 2000 Web: www.danmurphys.com.au -

Half Year Results HY10

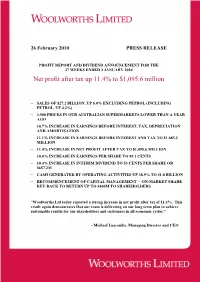

26 February 2010 PRESS RELEASE PROFIT REPORT AND DIVIDEND ANNOUNCEMENT FOR THE 27 WEEKS ENDED 3 JANUARY 2010 Net profit after tax up 11.4% to $1,095.6 million − SALES OF $27.2 BILLION, UP 6.0% EXCLUDING PETROL (INCLUDING PETROL, UP 4.2%) − 3,500 PRICES IN OUR AUSTRALIAN SUPERMARKETS LOWER THAN A YEAR AGO − 10.7% INCREASE IN EARNINGS BEFORE INTEREST, TAX, DEPRECIATION AND AMORTISATION − 11.1% INCREASE IN EARNINGS BEFORE INTEREST AND TAX TO $1,683.2 MILLION − 11.4% INCREASE IN NET PROFIT AFTER TAX TO $1,095.6 MILLION − 10.0% INCREASE IN EARNINGS PER SHARE TO 89.1 CENTS − 10.4% INCREASE IN INTERIM DIVIDEND TO 53 CENTS PER SHARE OR $657.2M − CASH GENERATED BY OPERATING ACTIVITIES UP 38.9% TO $1.8 BILLION − RECOMMENCEMENT OF CAPITAL MANAGEMENT – ON-MARKET SHARE BUY-BACK TO RETURN UP TO $400M TO SHAREHOLDERS “Woolworths Ltd today reported a strong increase in net profit after tax of 11.4%. This result again demonstrates that our team is delivering on our long term plan to achieve sustainable results for our shareholders and customers in all economic cycles.” - Michael Luscombe, Managing Director and CEO Page 1 Summary of Results The Board of Woolworths Limited today approved and released the interim profit and dividend announcement of Woolworths Limited and its controlled entities for the 27 weeks ended 3 January 2010. Woolworths Limited Managing Director and CEO, Michael Luscombe said, “This is a strong result given the economic challenges of cycling the prior year stimulus package and the significant decline in food inflation. -

Corporate Responsibility Report 2010 Inside Front Cover Inside Back Cover

outside back cover 6.5mm outside front cover woolworths limited limited woolworths corporate responsibility report 2010 corporate responsibility report 2010 inside front cover inside back cover Contact Details Contents Scope of the Report Unless otherwise stated, this report covers all our operations in Australia and New Zealand Statement from the Chairman for the 2010 financial year (1 July 2009 to 30 June 2010). Our environmental targets are and CEO 2 based on projected growth through additional new stores in our existing businesses Our Approach to Corporate as at the 2007 financial year. These projections do not account for the impact of future Responsibility and Sustainability 4 acquisitions. Should we acquire new businesses of significant scale, the baseline data would be adjusted accordingly. The environmental data in this report does not cover Croma, Understanding our stakeholders Woolworths Limited ALH Group Pty Ltd our consumer electronics joint venture with the TATA Group in India, where we provide and what is important to them 8 Principal registered office in Australia Registered Office wholesale services to 50 retail stores. Nor are our global sourcing offices in Hong Kong and 1 Woolworths Way 1 Woolworths Way Issues of Public Interest 12 Shanghai included. These operations are small and not deemed to be material in the overall Bella Vista NSW 2153 Bella Vista NSW 2153 context. Energy and climate change data only has been collected for hardware distributor Our business 16 Tel: (02) 8885 0000 Tel: (02) 8885 0000 Danks Holdings Limited, which Woolworths completed its acquisition of during the year. Web: w w w.woolworthslimited.com.au Our people 20 Macro Wholefoods was incorporated into Thomas Dux and all data has been collected Victorian Office as part of this division. -

Carboxy Pty Ltd Takeover Offer for Danks Holdings Limited - Supplementary Bidder's Statement

22 October 2009 Company Announcements Office Australian Securities Exchange Dear Sir or Madam Carboxy Pty Ltd takeover offer for Danks Holdings Limited - supplementary bidder's statement Pursuant to section 647(3)(b) of the Corporations Act 2001 (Cth), we enclose, on behalf of Carboxy Pty Ltd (Carboxy), a supplementary bidder's statement. Yours faithfully Peter Horton Company Secretary Enclosure Carboxy Pty Ltd ACN 138 990 584 Takeover offer for shares in Danks Holdings Limited First Supplementary Bidder's Statement 1. Introduction This document is the first supplementary bidder's statement (First Supplementary Bidder's Statement) lodged with the Australian Securities and Investments Commission (ASIC) on 22 October 2009 and is given by Carboxy Pty Ltd (Bidco) to Danks Holdings Limited ABN 81 004 295 532 under section 643 of the Corporations Act 2001 (Cth). This First Supplementary Bidder's Statement supplements and is to be read together with the bidder's statement dated 2 September 2009 (Original Bidder's Statement), a copy of which was given to the Australian Securities Exchange on 2 September 2009. Unless the context requires otherwise, capitalised terms in this First Supplementary Bidder's Statement which are not defined have the meanings given to those terms in the Original Bidder's Statement. ASIC takes no responsibility for the content of this First Supplementary Bidder's Statement. 2. ACCC review of the proposed acquisition 2.1 Statement of Issues On 16 October 2009 the Australian Competition & Consumer Commission issued a statement of issues in relation to the proposed acquisition of Danks by Bidco pursuant to the Offer (Statement of Issues). -

The Proposed Acquisition

16 May 2012 Statement of Issues — Woolworths Limited and Lowe's Companies Inc (Joint Venture) – proposed acquisition of G Gay & Co hardware stores in Ballarat 1. Outlined below is the Statement of Issues released by the Australian Competition and Consumer Commission (ACCC ) in relation to the proposed acquisition of the assets of three hardware stores owned by G Gay & Co by Woolworths Limited ( Woolworths ) and Lowe's Companies Inc ( Lowe’s ) ( Joint Venture ) (Proposed Acquisition) . 2. A Statement of Issues published by the ACCC is not a final decision about a Proposed Acquisition, but provides the ACCC’s preliminary views, drawing attention to particular issues of varying degrees of competition concern, as well as identifying the lines of further inquiry that the ACCC wishes to undertake. 3. In line with the ACCC’s Merger Review Process Guidelines (available on the ACCC’s website at www.accc.gov.au) the ACCC has established a secondary timeline for further consideration of the issues. The ACCC anticipates completing further market inquiries by 1 June 2012 and anticipates making a final decision by 5 July 2012. However, the anticipated timeline can change in line with the Merger Review Process Guidelines . To keep abreast of possible changes in relation to timing and to find relevant documents, market participants should visit the Mergers Register on the ACCC's website at www.accc.gov.au/mergersregister . 4. A Statement of Issues provides an opportunity for all interested parties (including customers, competitors, shareholders and other stakeholders) to ascertain and consider the primary issues identified by the ACCC. It is also intended to provide the merger parties and other interested parties with the basis for making further submissions should they consider it necessary. -

Bidder's Statement As Updated in Accordance with That Class Order

7 September 2009 Company Announcements Office Australian Securities Exchange Dear Sir or Madam Carboxy Pty Ltd takeover offer for Danks Holdings Limited (ASX: DKS) On behalf of Carboxy Pty Ltd (Carboxy), a subsidiary of Woolworths Limited (ASX: WOW), we enclose a notice under item 8 of section 633(1) of the Corporations Act 2001 (Cth). Pursuant to paragraph 8 of ASIC Class Order 01/1543, we also enclose a copy of Carboxy's bidder's statement as updated in accordance with that class order. Yours faithfully Peter Horton Company Secretary Enclosure For personal use only Notice that bidder's statement and offers have been sent Pursuant to item 8 of section 633(1) of the Corporations Act 2001 (Cth), Carboxy Pty Ltd (ACN 138 990 584) hereby gives notice that its bidder's statement and offers have been sent as required by item 6 of section 633(1) of the Corporations Act. Dated: 7 September 2009 Peter Horton Company Secretary Carboxy Pty Ltd For personal use only Legal\110421131.1 Bidder’s Statement recommended cash offer of $13.50 per share to acquire all of your shares in Danks Holdings Limited ABN 81 004 295 532 from Carboxy Pty Ltd ACN 138 990 584 a company jointly owned by Woolworths Limited ABN 88 000 014 675 and Lowe’s Companies, Inc. For personal use only If you have any questions about the Offer or this document, or about how to accept the Offer, please contact the Offer information line on 1800 243 528 (toll free) within Australia or +61 3 9415 4663 (normal charges apply) from outside Australia. -

The Royal Gazette Gazette Royale

The Royal Gazette Gazette royale Fredericton Fredericton New Brunswick Nouveau-Brunswick ISSN 0703-8623 Vol. 162 Wednesday, December 1, 2004 / Le mercredi 1er décembre 2004 1943 Important Notice Avis Important Please note changes in regular deadlines affecting the following Veuillez prendre note du changement de l’heure de tombée des publications: éditions suivantes : Edition Revised Deadline Édition Nouvelle heure de tombée December 22, 2004 Monday, December 13, 2004, 12 noon Le 22 décembre 2004 Le lundi 13 décembre 2004 à 12 h December 29, 2004 Thursday, December 16, 2004, 12 noon Le 29 décembre 2004 Le jeudi 16 décembre 2004 à 12 h January 5, 2005 Tuesday, December 21, 2004, 12 noon Le 5 janvier 2005 Le mardi 21 décembre 2004 à 12 h For more information, please contact the Royal Gazette Coordinator at Pour de plus amples renseignements, veuillez communiquer avec la 453-8372. Coordonnatrice de la Gazette royale au 453-8372. _________________ __________________ Effective June 1, 2004, new Pricelist Nouvelle liste de prix à partir du 1er juin 2004 _________________ __________________ We are happy to offer the free official on-line Royal Gazette Je suis heureuse de vous annoncer que nous offrirons, gratuite- each Wednesday beginning January 7, 2004. This free on-line ment et en ligne, la version officielle de la Gazette royale, cha- service will take the place of the printed annual subscription que mercredi, à partir du 7 janvier 2004. Ce service gratuit en service. The Royal Gazette can be accessed on-line at: ligne remplace le service