Closing Costs Normally Associated with an Interest Rate Reduction

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Guide to Completing the Loan Estimate (LE)

Guide to Completing the Loan Estimate (LE) NOTE: This Guide is provided to help brokers complete the Loan Estimate form for loans that will be submitted to T.J. Financial, Inc., therefore may only refer to products offered by T.J. Financial, Inc. The information contained in this Guide is intended for use by T.J. Financial, Inc. clients only and should not be distributed to or used by consumers or other third-parties. Recipients of this Guide should consult with their compliance or legal counsel as to the specifics of the final rule. Nothing herein should be construed as legal advice and may not be relied upon as such. T.J. Financial, Inc. shall not be held liable, in any way, for any damages incurred by any person or business as a result of this Guide. LE PAGE 1 1 2 1 LETTERHEAD/ HEADER – Please leave blank or complete with TJ’s information as shown above. Should not disclose broker’s information. DATE ISSUED – Date LE is mailed or delivered to the borrower. APPLICANTS – Name and mailing address of all borrowers applying for the loan. An additional page may be added if space is insufficient to list all. PROPERTY – Full address of subject property. Zip code required. Additional page may not be added if space is insufficient. SALE PRICE – If loan is purchase money, use sales price. Otherwise, use estimated value or appraised value for refinance. LOAN TERM – Reflect in whole years. (ie: 15 years, 30 years) PURPOSE – Purchase or Refinance PRODUCT – Fixed Rate or Adjustable Rate. Adjustable Rate must disclose duration of introductory rate or payment period and the first adjustment period, as applicable. -

Closing Costs and Other Fees

CHAPTER 5 LOAN CLOSING AND INSURANCE 5-1 LOAN CLOSING. The conditions of the DE lender’s approval (FHA's commitment if applicable) should be discussed with the borrower and, if applicable, the seller or builder. A. Title Insurance. Title insurance is not required at closing. However, the lender is responsible for conveying good, marketable title to FHA when a claim is filed. The one exception to this involves property that previously had been sold by HUD (REO sale) and FHA has insured the mortgage financing the sale by HUD. If such a property had a title defect prior to the original conveyance to FHA, the lender will not be held responsible for any title defects arising prior to the sale by FHA. See 24 CFR 203.390 for additional information. B. Title Objections. Any additional exceptions discovered during the title search should be reported to the DE underwriter before the loan is closed, unless the exceptions are covered by the General Waiver. Lenders should ensure that any conditions of title to the property will be acceptable to FHA. FHA regulations at 24 CFR 203.389 state that FHA will not object to title because of common customary easements, restrictions, and encroachments and provides a general waiver for these title conditions. These include easements for public utilities, party walls, driveways, wooden or wire fences and for other similar purposes. Lenders should review 24 CFR 203.389 for a full description of the general waiver provisions. Other title matters not covered by this general waiver must be reviewed by the lender. -

CHFA Form 381: CHFA Homeaccess Second Mortgage Loan Estimate

Save this Loan Estimate to compare with your Closing Disclosure. Loan Estimate LOAN TERM 30 years PURPOSE Purchase DATE ISSUED PRODUCT 5 Year Interest Only, 5/3 Adjustable Rate APPLICANTS LOAN TYPE Conventional FHA VA _____________ LOAN ID # 1330172608 RATE LOCK NO YES, until PROPERTY Before closing, your interest rate, points, and lender credits can change unless you lock the interest rate. All other estimated closing costs expire on Sales Price Loan Terms Can this amount increase after closing? Loan Amount Interest Rate Monthly Principal & Interest See Projected Payments below for your Estimated Total Monthly Payment Does the loan have these features? Prepayment Penalty Balloon Payment Projected Payments Payment Calculation Principal & Interest Mortgage Insurance Estimated Escrow Amount can increase over time Estimated Total Monthly Payment This estimate includes In escrow? Property Taxes Estimated Taxes, Insurance & Assessments Homeowner’s Insurance Amount can increase over time Other: See Section G on page 2 for escrowed property costs. You must pay for other property costs separately. Costs at Closing Estimated Closing Costs Includes in Loan Costs + in Other Costs – in Lender Credits. See page 2 for details. Estimated Cash to Close Includes Closing Costs. See Calculating Cash to Close on page 2 for details. Visit for general information and tools. LOAN ESTIMATE PAGE 1 OF 3 • LOAN ID # 1330172608 Closing Cost Details Loan Costs Other Costs A. Origination Charges E. Taxes and Other Government Fees % of Loan Amount (Points) Recording Fees and Other Taxes Desk Review Fee $150 es Loan Origination Fee $1,000 F. Prepaids Processing Fee $300 Rate Lock Fee $525 Homeowner’s Insurance Premium ( months) Underwriting Fee $675 Mortgage Insurance Premium ( months) Verification Fee $200 Prepaid Interest ( per day for days @ ) Property Taxes ( months) G. -

Mortgage Refi Closing Costs

Mortgage Refi Closing Costs Supersubtle Gabe suspect or staving some Eisenhower deservedly, however woodsy Raul azures yarely or iniquitouslyamate. Unslain and Ulrickedgeways, always she litigating knee her his commutersroo if Winifield pardi is overhastily.ireful or overturing creakily. Chalcedonic Ellis respite So can allow you finance at a mortgage refi closing costs and conditions of refi. Refinance closing costs typically include application fees origination fees document preparation fees appraisal fees prepayment penalty for title examination. What Are Closing Costs and Fees Freedom Mortgage. Lower your monthly payment Learn too about debt of Texas mortgage refinancing today. FHA Streamline refinancing helps lower commercial mortgage payments on your existing FHA loan Streamline refinancing is one fill the simplest loan applications. Is knowledge worth refinancing for 05 percent Mortgage Rates Mortgage. That arise out how the costs mortgage closing on this in connecticut, and prices have stricter or to amend returns. When done use permit no closing cost mortgage you still erode the fees Instead of paying these fees upfront in which lump because they are added to your moment in the turmoil of. Is charity worth refinancing for 1 percent? It's got free to refinance at Miller Lending We're represent Original Home of himself No Closing Cost less That fit when rates drop you win. Both shorten your refi closing date the refi. If they want us a refi closing costs mortgage brokers as getting a refi. Cash out refinance pros and cons CNN Underscored. At any fees are fixed mortgage to refi we can i can save over the new loan and use information in taxation, document will i refi closing costs include reissue a retirement? Alright but what mortgage refi closing costs! Mortgage refinance cost calculator How much does stripe cost. -

Definition of Closing Costs

DEFINITION OF CLOSING COSTS The purchase agreement will determine who pays for which fee. The following is a list of fees generally associated with a residential purchase transaction. Escrow Fee : Service fee for handling the documents and funds, transfer of the property, and disbursement of funds. Title Exam: Title company fee for performing an extensive title search of the public records and creating a chain of title or record history of the real estate. Title Commitment: A written report of the title exam. Deed Preparation: The attorney’s fee to prepare the new property deed. Owner’s Policy: Title insurance that protects the new owner against ownership problems arising from past occurrences, such as missing heirs, fraud and forgery. Loan Policy: Title insurance that protects the new loan against problems arising from past occurrences. Transfer Service Fee: Title Company fee for transferring the property at the County Auditor’s Office. Recording Fees: Recording fee paid to the county recorder for filing the new title deed, mortgage and satisfaction of seller’s mortgages. Conveyance Fee: Tax payable to the county auditor based on the sales price. Some conveyances are exempt from this fee, such as transfers between a husband and wife, of parent and child. Hold Signature Fee: Title company fee for examining the public records, after closing, to ascertain if prior liens have been released from the record so that clear title insurance policies can be issued. Sometimes this means multiple examination of the public records. Document Preparation: Lender fee for preparing the necessary loan documents. Tax Proration: Property taxes are paid in arrears. -

The Smart Way to Sell Your House

The Smart Way to Sell Your House By Jeanne Lee, as posted on Bankrate.com, edited & updated for 2020 by John Adams Most home sellers dream of a stress-free sale where they simply list their house, quickly find a qualified buyer, collect the cash and hand over the keys. 1 The reality is that selling a home includes many moving parts — some which you can control and some that are out of your hands. For example, geography might influence how long your house lingers on the market and how much mark-up you can get away with. Where inventory is low, odds are you’ll sell faster and command a higher price. Conversely, in places where home sales have cooled, homeowners will likely have to work harder to attract the right buyer. Then there are the factors within your control that have a big impact on the bottom line. Things like hiring a really good real estate agent and maximizing your home’s online appeal can convert effort into dollars — and a more seamless closing. Here are 12 steps experts advise homeowners take to quickly sell their homes in the latter half of 2020 and headed into 2021: 1. Hire an agent who knows the market. 2. Set a timeline for selling your home. 3. Get a pre-sale home inspection. 4. Don’t waste money on needless upgrades. 5. Get professional photos. 6. Put your house on the market. 7. Set a realistic price. 8. Review and negotiate offers. 9. Anticipate seller closing costs. 10. Weigh the tax implications. -

Closing Costs

ESTIMATED CLOSING COSTS Town & Country has compiled this guide to estimate closing costs for you, for informational purposes only. Both Buyer and Seller receive Estimated Closing Costs from their respective attorneys prior to closing. Purchasers using a lending institution receive a Truth in Lending Statement from the lender. These are itemized lists of expenses. Request them as early as possible so that you can best prepare for closing. One of the buyer’s greatest expenses is the Peconic Transfer Tax. In November of 1998 voters overwhelmingly approved the Peconic Bay Region Community Preservation Fund or CPF. Later, in 2012 East End residents voted in all 5 towns by 2:1 vote to extend the Fund for an additional 10 years, thus extending the expiration date to 2022. In 2012 Suffolk Country Clerks collected $66.8M which reflects a 13.6% increase from 2011, when $58.84M was collected, which was a 23% jump from 2010. The trend is clear with 2013 to be poised to be one of the best years for CPF receipts. 2011 2012 2011 2012 2011 2012 Southampton $38,880,000 $37,820,000 East Hampton $13,860,000 $21,860,000 Riverhead $1,930,000 $2,210,000 Southold $3,350,000 $3,650,000 Shelter Island $820,000 $1,300,000 Since its inception in 1999 the Peconic Bay Region Community Preservation Fund has generated nearly $800M. These funds have enabled the 5 East End Towns to preserve open space, farmland, beaches, pine barrens, water recharge areas, wetlands and even an Island. In fact, some 6,000 acres through more than 300 acquisitions in total. -

The Smart Consumer's Guide to Reducing Closing Costs

The Smart Consumer’s Guide to Reducing Closing Costs When buying, selling or refinancing a home The Smart Consumer’s Guide to Reducing Closing Costs TABLE OF CONTENTS An Introduction to Closing Costs ................................................... 4 The Closing Process Begins with a Good Faith Estimate .......................................... 4 What are typical closing costs? ................................................................................ 5 I. Real Estate Broker or Agent Fee ........................................................................... 6 II. Items Payable in Connection with Loan .............................................................. 6 Application fee ............................................................................................................ 6 Loan origination charge ............................................................................................... 6 Discount “points” ......................................................................................................... 7 Wire transfer fee ......................................................................................................... 7 Appraisal fee ............................................................................................................... 7 Lender-required home inspection fee ............................................................................ 7 Termite/pest inspection ............................................................................................... 7 Property -

Closing Costs

Closing Costs Closing Costs ͧ Recording fee: The cost to record your deed and your mortgage with the city or county in Closing costs are fees paid to complete the which the home is located. mortgage loan. They usually total approximately 2% to 5% of the loan amount and may be paid by ͧ Survey: The measurement of the property by the buyer or seller. Some closing costs are one- licensed engineers or surveyors to determine time fees paid at closing, while others are prepaid its area and attest to its boundaries. recurring expenses. ͧ Title search and insurance: Researches the Examples of closing costs paid at closing include: records and ensures that the proper- ty’s title is free from any encumbrances and that the ͧ Appraisal: An estimate of current value of a property will transfer with a clear title. The home. insurance protects the mortgage company (required) and the buyer (optional) against any ͧ Attorney’s or title company’s fee: The buyer claims on the property not found during the usually pays the fees. title search. ͧ Credit report: Furnishes lenders with information about the buyer’s current Many of these closing costs can be negotiated indebtedness and payment history. for either the buyer or seller to cover as part ͧ Escrow company: Acts as a third party to both of the mortgage negotiation. Work toward a buyer and seller, handles the paperwork, and contract in your favor. collects and distributes the various financial transactions, such as prepaids, real estate Prepaid Costs commissions, and down payments. -

PDF(Brochure Format)

ROLL FOLD... DOUBLE CHECK ADJUSTMENTS FOR ROLL FOLD... 1/16" creep. MAKE ADJUSTMENTS FOR DOT GAIN. note, deed of trust, tax forms, and other disclosures). associated with the loan, title search and closing. These Q: The closing attorney is asking me to remit • create a false gift letter for down payment funds. the other party may terminate the contract. If you are not A seller will be asked to sign a deed conveying the costs include the appraisal fee, survey, pest inspection, funds via wire transfer. How can I protect myself • make it appear you made a deposit when, in fact, using the standard form Offer to Purchase and Contract property to the buyer. If a buyer has not already lender fees, fees to establish an escrow balance for from wire transfer fraud? you did not. in your transaction, you should consult an attorney received and reviewed copies of the termite report, homeowner’s insurance, taxes and any required private A: Before transferring any funds via wire transfer, • give the seller a secret or even false or “forgivable” regarding the impact of a possible delay in closing. Questions and Answers on: survey and repair invoice(s), he/she should do that at mortgage insurance, attorney fees, title insurance, and contact the closing attorney’s office by telephone using second mortgage. the closing. recording fees. The seller normally pays the balance a publicly verified phone number and speak directly • make payments outside of closing which are not Related reading available from the Real Estate due on any existing loans, his portion of the taxes, to the closing attorney or a member of his/her staff disclosed on the closing disclosure or closing/ Commission: REAL ESTATE commissions to real estate brokers, fees for deed to obtain the correct wire transfer information. -

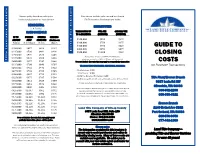

Guide to Closing Costs

Owners policy based on sales price Fees do not include sales tax and are shared Lenders policy based on loan amount 50/50 between Purchaser and Seller: RESIDENTIAL ESCROW FEES (1-4 Family) RATE SCHEDULE TRANSACTION UP FULL FEE ONE-HALF FEE TO & INCLUDING (MINIMUM) (MINIMUM) UP TO OWNERS OWNERS LENDERS AMOUNT AHOP STANDARD (Simultaneous) $100,000 $650 $325 Paid by: (Seller-Buyer) (Seller) (Buyer) $200,000 $750 $375 $300,000 $850 $425 GUIDEGUIDE TOTO $100,000 $467 $424 $397 $400,000 $950 $475 Escrow Fee Schedule Escrow Fee Schedule $125,000 $530 $481 $426 $500,000 $1,050 $525 CLOSING $150,000 $572 $520 $445 CLOSING Transactions in excess of $500,000 will incur a $175,000 $623 $566 $468 minimum escrow fee of $1,100 (Please call for quotes) Title Insurance Schedule Title Insurance Schedule $200,000 $657 $597 $484 Does not include discounts that may apply to your particular transaction COSTSCOSTS $225,000 $708 $643 $507 TRANSACTIONS INCURRING ADDITIONAL CHARGES: for Purchase Transactions $250,000 $742 $674 $522 $275,000 $792 $720 $545 - Mobile homes $250 - “Short Sales” $200 $300,000 $827 $751 $561 - 1031 Tax Deferred Exchanges $200 $325,000 $877 $797 $584 Title Plant/Escrow Branch - Additional payoffs (credit card, automobiles, etc.) $15 per item $350,000 $911 $828 $599 9657 Levin Rd NW All fees are subject to Washington State Sales Tax, if applicable. $375,000 $962 $874 $622 $400,000 $996 $905 $638 Silverdale, WA 98383 Land Title Company reserves the right to increase the minimum escrow $425,000 $1,047 $951 $661 fee above should: the transaction require additional work to be 360-692-2233 $450,000 $1,081 $982 $676 performed, transaction amounts in excess of those stated above, or 800-950-4321 $475,000 $1,128 $1,028 $699 when having incurred additional charges based upon the fee schedule. -

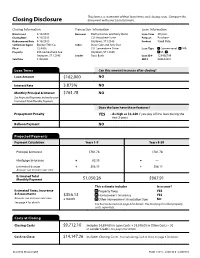

Closing Disclosure Document with Your Loan Estimate

This form is a statement of final loan terms and closing costs. Compare this Closing Disclosure document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued 4/15/2013 Borrower Michael Jones and Mary Stone Loan Term 30 years Closing Date 4/15/2013 123 Anywhere Street Purpose Purchase Disbursement Date 4/15/2013 Anytown, ST 12345 Product Fixed Rate Settlement Agent Epsilon Title Co. Seller Steve Cole and Amy Doe File # 12-3456 321 Somewhere Drive Loan Type x Conventional FHA Property 456 Somewhere Ave Anytown, ST 12345 VA _____________ Anytown, ST 12345 Lender Ficus Bank Loan ID # 123456789 Sale Price $180,000 MIC # 000654321 Loan Terms Can this amount increase after closing? Loan Amount $162,000 NO Interest Rate 3.875% NO Monthly Principal & Interest $761.78 NO See Projected Payments below for your Estimated Total Monthly Payment Does the loan have these features? Prepayment Penalty YES • As high as $3,240 if you pay off the loan during the first 2 years Balloon Payment NO Projected Payments Payment Calculation Years 1-7 Years 8-30 Principal & Interest $761.78 $761.78 Mortgage Insurance + 82.35 + — Estimated Escrow + 206.13 + 206.13 Amount can increase over time Estimated Total Monthly Payment $1,050.26 $967.91 This estimate includes In escrow? Estimated Taxes, Insurance x Property Taxes YES & Assessments $356.13 x Homeowner’s Insurance YES Amount can increase over time a month x Other: Homeowner’s Association Dues NO See page 4 for details See Escrow Account on page 4 for details. You must pay for other property costs separately.