The Business Value of BIM in Australia and New Zealand: How Building Information Modeling Is Transforming the Design and Construction Industry

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Case Study Grocon Group

Case Study Grocon Group Case Study Grocon Group » Beyond the technology, Fujitsu has provided a real human touch. It’s not just about vision; it’s about ensuring total customer satisfaction. Fujitsu has given us the confidence to think big « Rebecca Brockett, CIO, Grocon Group The customer Grocon is the largest privately owned development, construction and investment management company in Australia. It specializes in large scale projects, be they commercial office spaces for premium clients such as ANZ and Freehills, or Public Private Partnerships such as the new Victorian Comprehensive Cancer Centre for the Federal and Victorian Governments. Grocon’s core values of safety, sustainability, community and innovation drive everything it does and are demonstrated through projects such as Pixel in Melbourne, currently considered the greenest building in Australia. The Challenge Grocon was looking for a cost effective and scalable solution for the agile management of IT services as part of a wider back office infrastructure renewal initiative. The existing infrastructure was THE CUSTOMER nearing the end of its lifecycle so the company was keen to look at new Country: Australia solutions that would be more flexible and cost-effective. Industry: Construction Founded: 1950s “We were looking for a partner to take us to the next level. We found Employees: 500 that partner in Fujitsu,” explains Rebecca Brockett, CIO, Grocon Group. Website: www.grocon.com “The company presented us with a radical vision and we jumped on board because innovation is part of our corporate DNA.” CHALLENGE Grocon wanted to replace its existing ageing legacy infrastructure Fujitsu suggested migrating to a cloud platform which would deliver with a more innovative approach to delivering applications in order to all the functionality Grocon needed without compromising security or reduce costs, improve productivity and increase performance. -

EMPORIUM REDEVELOPMENT, LONSDALE and LITTLE BOURKE 12 April 2011 STREETS, MELBOURNE: TREE REMOVAL

Page 1 of 7 FUTURE MELBOURNE (PLANNING) Agenda Item 5.1 COMMITTEE REPORT EMPORIUM REDEVELOPMENT, LONSDALE AND LITTLE BOURKE 12 April 2011 STREETS, MELBOURNE: TREE REMOVAL Presenter: Angela Meinke, Manager Planning and Building Purpose and background 1. This matter is presented to the Committee at the request of Councillor Clarke. 2. The purpose of this report is to advise the Committee of a request by Colonial First State (CFS) to allow the removal of two street trees located within the Lonsdale Street median strip. Key issues 3. The key issue for consideration is whether the existing street trees should be retained or permitted for removal. 4. The Minister for Planning issued a planning permit for the redevelopment of the Emporium site which included the requirement to retain the historic eight storey building façade. In investigating design options to enable this it was determined by the project engineers (on the basis of safety, practicality and certainty) that an external retention system was most appropriate. This option was presented by CFS to a stakeholder group facilitated by the Department of Innovation, Industry and Regional Development that included the Council officers, VicRoads and the Department of Transport. CFS also engaged at this time in detailed discussions with Council officers on the approach they proposed to adopt for the retention of the façade. 5. CFS’s representatives were advised by Council’s Urban Landscapes branch that Council would consider the removal of trees if there was no viable alternative. Council officers provided advice to CFS on the value to remove each tree and the need for CFS to pay all associated costs. -

Commonwealth Property Office Fund

Commonwealth Property Office Fund Retail Entitlement Offer 18 November 2010 DETAILS OF A 1 FOR 15 NON-RENOUNCEABLE PRO-RATA ENTITLEMENT OFFER OF UNITS IN THE COMMONWEALTH PROPERTY OFFICE FUND AT AN OFFER PRICE OF $0.86 PER NEW UNIT THIS ENTITLEMENT OFFER CLOSES AT 5.00PM (AEDT) ON 8 DECEMBER 2010 This is an important document which is accompanied by an Entitlement and Acceptance Form and both documents should be read in their entirety. Please call your professional adviser or the CPA Entitlement Offer Information Line if you have any questions. NOT FOR DISTRIBUTION OR RELEASE IN THE UNITED STATES For personal use only Responsible Entity: Commonwealth Managed Investments Limited ABN 33 084 098 180 AFSL 235384 Registered Address: Ground Floor, Tower 1, 201 Sussex Street, Sydney NSW 2000 Contents 1 Chairman’s letter 1 2 Details of the Entitlement Offer 2 3 How to apply 4 4 Important information 7 5 ASX offer documents 12 – Equity raising launch announcement 12 – Investor presentation 16 – Placement and Institutional Entitlement Offer completion announcement 44 6 Glossary 46 7 Corporate directory 49 Important information This Retail Offer Booklet is not a product disclosure This Retail Offer Booklet, including the ASX statement, prospectus or other disclosure document announcements produced in it and the Entitlement and has not been lodged with ASIC. It does not and Acceptance Form do not constitute an offer contain all the information that an investor would to sell, or the solicitation of an offer to buy, any find in a product disclosure statement, prospectus or securities in the United States or in any other other disclosure document or on which an investor jurisdiction in which, or to any person to whom, would expect to make an informed decision as to such an offer or sale would not be lawful. -

AAMI PARK the Roof Structure Allows Internal Space to Be More Efficiently Used, with Unobstructed Sight Lines

AAMI PARK The roof structure allows internal space to be more efficiently used, with unobstructed sight lines. The roof geometry is also ARCHITECTURAL STEEL DESIGN AWARD 2010 driven by the requirement to maximise natural light and NATIONAL AND STATE WINNER (VIC + TAS) ventilation, both for spectator comfort and the health of the STRUCTURAL ENGINEERING STEEL DESIGN AWARD 2010 playing surface. NATIONAL AND STATE WINNER (VIC + TAS) The structural concept and geometry allows the roof to be ARUP, Cox Architects + Planners delivered with approximately 50% of the steel required, compared to similar stadium roofs. Further, the shell concept allows the roof to work with a single layer of structure, where the façade is fixed directly to the structural frame, eliminating secondary steelwork. Parametric modelling allowed variations in geometry to be tested quickly to provide the most structurally efficient form. The roof structure is formed from 273mm diameter tubes, rigidly connected to form shells. Each shell is bounded by a 508mm diameter edge and front edge members, and a 457mm diameter back edge member. The structure is clad in a combination of aluminium, glass and louvres. The roof structure also supports four light towers on the corners of the stadium, with additional lighting fixtures and services suspended below the main canopy. Architectural merit AAMI Park (The Melbourne Rectangular Stadium) is a purpose built rectangular pitch stadium designed to accommodate 31,000 fans, and will host soccer, rugby league and rugby union matches. The stadium is a world-class facility, featuring a sports campus, elite training centre and sports administration complex. The brief called for the stadium to achieve world standards, and Practicality in fabrication + erection be extraordinary in terms of structure, atmosphere and spectator experience. -

Australian Cbd Office Supply & Development Maps December 2015

RESEARCH AUSTRALIAN CBD OFFICE SUPPLY & DEVELOPMENT MAPS DECEMBER 2015 After a hiatus in office completions in 2014, new supply Key Facts rebounded in 2015, with feasibility supported by the steady 560,500m² of new office decline in prime yields; albeit many schemes have and will supply will be completed in continue to divert to residential or alternate uses. 2015, up 75% on 2014. The 2015 calendar year will deliver completing in 2016. Melbourne is nearing Gross supply is anticipated approximately 560,500m² of new and the end of a long supply cycle, however new to rise by another 9% in refurbished stock to the major Australian supply will still total 108,000m² in 2016. 2016 to 610,800m², driven CBD markets, which is up 75% on the Perth, Adelaide and Canberra will all have predominantly by Sydney. 321,000m² recorded during 2014 and slightly benign supply over the next few years, higher than the 10 year average (538,000m²). which will assist in cushioning generally Pipeline for additional The CBDs with the greatest supply during weak demand conditions. The pipeline for supply in 2017 and 2018 is 2015 were Sydney (182,929m²), Perth supply additions in 2017 and 2018 is benign, with only Sydney (134.556m²) and Melbourne (130,214m²), currently very benign nationally. adding materially to stock. with the least amount of supply added in Feasibility for construction of new space has Canberra (11,945m²). Many office schemes are been supported by steady declines in prime being altered to residential Following the hiatus in office completions in yields, particularly for fund through use, but increasingly hotel and 2014, with many developers/owners actively developments with strong pre-commitment. -

JAMES L. Williamspty

James L. WIllIams PTY LTD From Gas Lights to Skyscrapers Australia’s Most Experienced and Respected Mechanical Services Contractor James L. Williams is Australia’s longest established Mechanical Services Contractor. Since 1875 James L. Williams has faithfully served the plumbing and engineering industry of Victoria and Australia. The success of the company is both a legacy of and a tribute to the energies and visions of its founder. His vision and his commitment have been continued, enlarged and reinvigorated by successive generations of Williams’ in an unbroken line of family management spanning over 130 years. With small beginnings at Errol Street, Melbourne, James L. Williams has developed to become an industry leader with offices in Melbourne, Sydney, Brisbane, Gold Coast and Sunshine Coast. Each branch has its own unique style and personality, yet the companies core values of quality, a skilled and happy work force and high levels of customer satisfaction is preserved. Working in a tough and competitive environment, Williams continues to display the same characteristics of innovation and personal attention that so much marked the success of JL himself. Through its modern sheetmetal factory in Melbourne and with its association through G.J. Walker with Efatar Engineering in China, James L. Williams has manufactured, installed, commissioned and serviced many of Australia’s landmark buildings. Victorian Landmark Projects 737 AGSO BHP-Billiton Casey Bourke Street Canberra Q.V.3 Hospital Client: Equiset Client: Baulderstone Hornibrook Client: Grocon Client: Multiplex Building Value: $85 million Building Value: $160 million Building Value: $120 million (BHP-B) Building Value: $90 million Year: 2007-2008 Year: 1997 Building Value: $50 million (Q.V.3) Year: 2003-2004 737 Bourke St is an 11 level office The largest geothermal system Year: 2002-2004 The first public hospital built tower. -

Rectangle Stadium, Melbourne, Australia.Indd

Bringing structures to life Melbourne Rectangular Stadium Client: Victoria State Government Contractor: Grocon Constructors Pty Ltd Location: Melbourne, Australia Products: Alshor Plus / Megashor Case Study RMD Australia puts its Olympic stadium experience to the test in Melbourne, “By focusing on these core deliverables, we were able to demonstrate how using a combination of Alshor Plus and Megashor to support the construction our equipment and design could meet the clients need for a versatile, labour of the impressive Melbourne Rectangular Stadium saving solution. Our fi rst challenge was to support the reinforced concrete beams ranging up to 950mm deep by 1,800mm wide in the podium slab areas. With a whole range of top class sports teams in need of a world-class venue to play football, rugby league and rugby union, in May 2007, the Victorian State “In turn these beams carried additional loads from precast hollowcore Government commissioned the design of the 31,000 capacity, AUD$267.5 slabs used to form a base for the main facilities and seating areas. In order million venue currently known as the Melbourne Rectangular Stadium (MRS). to support the installation of these slabs, we designed and supplied our lightweight Alshor Plus aluminium shoring, which was used to support our Located in the Olympic Park Precinct, on Olympic Boulevard in Melbourne, aluminium Albeam and Alform primary and secondary beams. Victoria, the new stadium will be home to football teams, Melbourne Victory and Melbourne Storm. “Thanks to the high leg capacity of Alshor Plus, which is able to withstand pressures of up to 120kN/m2, our design was able to cater for the high loads, As a key centrepiece for the development of the Melbourne Olympic Park, whilst providing the advantage of fast erection and safe dismantling of the the MRS is set to combine cutting-edge design and architecture with practical falsework. -

1 Bligh Street – Sydney’S First High Rise Office Tower to Incorporate Blackwater Technology

Media release 1 Bligh Street – Sydney’s first high rise office tower to incorporate blackwater technology DEXUS and co-owners DWPF and Cbus Property announced that NSW Water Minister, Phil Costa today awarded the first combined private network and retailer’s water recycling licence to the 1 Bligh St development, making it Sydney CBD’s first high rise commercial office tower to incorporate blackwater recycling technology. Minister Costa said construction is under way on a recycled treatment plant in the basement of the new development to treat waste water for use in the building’s toilets and cooling towers. “This licence is the first of its kind to be granted to a Sydney high rise and will save 100,000 litres of precious drinking water a day,” Minister Costa said. “This licence, granted under the Water Industry Competition Act 2006 is part of a NSW Government strategy to secure Sydney’s drinking water by attracting private investment in recycled water projects.” Under the project: Wastewater is mined from the nearby sewer main and the base building Wastewater will then be treated to the highest standards approved by NSW Health at the recycled water plant in the basement Water is then distributed around the building for non-drinking purposes, with 75,000 litres used for cooling towers and 25,000 litres will be used for flushing toilets. “Recycling is an important part of our Metropolitan Water Plan to secure Sydney’s drinking supplies, along with key initiatives including desalination, water efficiency, and dam upgrades,” Minister Costa said. “It is vital we attract private investment into water recycling to ensure we meet our target of recycling 12 per cent of Sydney’s water needs by 2015. -

MAIN CONSTRUCTION COMPANY : Grocon DEVELOPER : Major

rocon is one of Australia’s leading development and construction important for the marketing of the stadium on a global level, both by of a combination of glass metal and louvers. The metal panels are The stadium is one of Grocon’s biggest jobs at present – Grocon has groups. Founded in the 1950s by Luigi Grollo and growing to a attracting spectators and corporate sponsors for the tenant teams as made with a urethane core sandwiched between steel outer casings offices in Victoria, NSW and Queensland. The Melbourne Rectangular major building company of the 1980s with his son Bruno at the helm, well as assisting Melbourne to be more favourably positioned in a highly and coated in a ‘whisper white’ custom produced colour sealant. Stadium will add to an already globally renowned sporting and event Grocon has continued to grow strongly into the new millennium headed competitive global sports and events market. The distinctive roof line Rainwater will be harvested from the roof and stored in tanks. The precinct with a technologically advanced, environmentally friendly and by Daniel, son of Bruno and grandson of Luigi. The inspiration behind continues and advances the present architectural lineage of the precinct water system will be installed with low-use water fittings further highly sculptured organic design structure attracting national interest and the privately owned, multi-generational organization has always been seen in the surrounding sports stadiums. reducing the volume of water used on the grounds and surrounding international recognition. a dream of excellence. And it is this reputation of excellence in the environs. -

Industrial Relations a Competitive Advantage Through Strategic Workplace Relations

INDUSTRIAL RELATIONS A COMPETITIVE ADVANTAGE THROUGH STRATEGIC WORKPLACE RELATIONS Employers seeking to obtain a competitive advantage need to strike a balance between labour productivity, employment costs and staff engagement. We understand that a strong industrial relations strategy is critical to achieving this balance. Our industrial relations service assists clients to: integrate workplace arrangements with operational objectives diagnose impediments to operational outcomes devise appropriate strategies to overcome impediments comply with legal obligations mitigate industrial relations risks We provide practical, solutions-based advice that enables our clients to navigate the procedurally complex industrial relations regulatory regimes, and to achieve their commercial objectives while minimising legal and reputational risk. We partner with clients in all areas of workplace relations including: business restructures and workplace reform industrial action, picketing and dispute management drafting and implementing individual and collective employment agreements union and individual workplace rights emerging workplace issues including drug and alcohol testing, sham contracting and the interaction of social media and the workplace obligations towards employee representatives, including information and consultation obligations In the current environment, many employers are faced with litigation in response to initiatives they have taken. For others, litigation may be necessary to protect the business from debilitating industrial action. -

50 Carrington Street Sydney

DEXUS Property Group (ASX: DXS) ASX release 24 October 2012 September 2012 quarterly update and Sydney CBD office tour DEXUS Property Group is hosting a quarterly update presentation and Sydney CBD office tour today for institutional investors and brokers and provides the attached ASX release, presentation and tour booklet. For further information please contact: Investor Relations Media Relations David Yates T: +61 2 9017 1424 Emma Parry T: +61 2 9017 1133 M: 0418 861 047 M: 0421 000 329 E: [email protected] E: [email protected] About DEXUS DEXUS’s vision is to be globally recognised as the leading real estate company in Australia, with market leadership in office, and has $13 billion of assets under management. DEXUS invests in high quality Australian office and industrial properties and, on behalf of third party clients, is a leading manager and developer of industrial properties and shopping centres in key markets. The Group’s stock market trading code is DXS and more than 18,000 investors from 15 countries invest in the Group. At DEXUS we pride ourselves on the quality of our properties and people, delivering world-class, sustainable workspaces and service excellence to our tenants and delivering enhanced returns to our investors. DEXUS is committed to being a market leader in Corporate Responsibility and Sustainability. www.dexus.com DEXUS Funds Management Ltd ABN 24 060 920 783, AFSL 238163, as Responsible Entity for DEXUS Property Group (ASX: DXS) For personal use only DEXUS Property Group (ASX:DXS) ASX release 24 October 2012 September 2012 quarter portfolio update DEXUS Property Group today announced its portfolio update for the quarter ended 30 September 2012. -

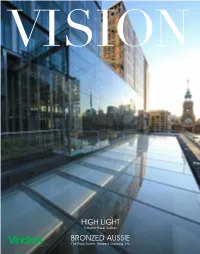

High Light Bronzed Aussie

HIGH LIGHT 5 Martin Place, Sydney BRONZED AUSSIE The Plaza Tavern, Hoppers Crossing, VIC VISION 26 Twitter Blog Subscribe Submit VISION welcomes project submissions to our editorial team, CONTENTS please submit ideas and projects clicking the icon above. CLICK TO VISIT HIGH LIGHT CLICK TO VISIT BRONZED THE PLAZA TAVERN 5 MARTIN PLACE 5 Martin Place, Sydney One of Sydney’s newest towers reflects a AUSSIE quiet workplace revolution. It’s home to The Plaza Tavern, Hoppers Crossing, VIC design that brings history into the present Viridian Bronze EVantage™ is pivotal to in a thoroughly modern light. At 5 Martin the glass and steel envelope of the Plaza 04 Place, a mid-level atrium draws daylight 20 Tavern, Hopper’s Crossing. With super solar deep into the building and distributes it as performance, many of the double-glazed a great social connector. A new generation units comprise acoustic glass for the of Viridian performance glazing covers a in-demand nightclub component. cathedral-like void – not as wasted space, On a streetscape, or highway more but pathway towards a switched on, vibrant commonly home to warehouses and workplace. discounted shopfronts, this beckons with a cool sophistication. VISION 26 Twitter Blog Subscribe Submit VISION welcomes project submissions to our editorial team, CONTENTS please submit ideas and projects clicking the icon above. CLICK TO VISIT HIGH LIGHT CLICK TO VISIT BRONZED THE PLAZA TAVERN 5 MARTIN PLACE 5 Martin Place, Sydney One of Sydney’s newest towers reflects a AUSSIE quiet workplace revolution. It’s home to The Plaza Tavern, Hoppers Crossing, VIC design that brings history into the present Viridian Bronze EVantage™ is pivotal to in a thoroughly modern light.