Brookline Brief

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

March 31, 2021

Units Cost Market Value US Equity Index Fund US Equities 95.82% Domestic Common Stocks 10X GENOMICS INC 126 10,868 24,673 1LIFE HEALTHCARE INC 145 6,151 4,794 2U INC 101 5,298 4,209 3D SYSTEMS CORP 230 5,461 9,193 3M CO 1,076 182,991 213,726 8X8 INC 156 2,204 4,331 A O SMITH CORP 401 17,703 28,896 A10 NETWORKS INC 58 350 653 AAON INC 82 3,107 5,132 AARON'S CO INC/THE 43 636 1,376 ABBOTT LABORATORIES 3,285 156,764 380,830 ABBVIE INC 3,463 250,453 390,072 ABERCROMBIE & FITCH CO 88 2,520 4,086 ABIOMED INC 81 6,829 25,281 ABM INDUSTRIES INC 90 2,579 3,992 ACACIA RESEARCH CORP 105 1,779 710 ACADIA HEALTHCARE CO INC 158 8,583 9,915 ACADIA PHARMACEUTICALS INC 194 6,132 4,732 ACADIA REALTY TRUST 47 1,418 1,032 ACCELERATE DIAGNOSTICS INC 80 1,788 645 ACCELERON PHARMA INC 70 2,571 8,784 ACCO BRANDS CORP 187 1,685 1,614 ACCURAY INC 64 483 289 ACI WORLDWIDE INC 166 3,338 6,165 ACTIVISION BLIZZARD INC 1,394 52,457 133,043 ACUITY BRANDS INC 77 13,124 14,401 ACUSHNET HOLDINGS CORP 130 2,487 6,422 ADAPTHEALTH CORP 394 14,628 10,800 ADAPTIVE BIOTECHNOLOGIES CORP 245 11,342 10,011 ADOBE INC 891 82,407 521,805 ADT INC 117 716 1,262 ADTALEM GLOBAL EDUCATION INC 99 4,475 3,528 ADTRAN INC 102 2,202 2,106 ADVANCE AUTO PARTS INC 36 6,442 7,385 ADVANCED DRAINAGE SYSTEMS INC 116 3,153 13,522 ADVANCED ENERGY INDUSTRIES INC 64 1,704 7,213 ADVANCED MICRO DEVICES INC 2,228 43,435 209,276 ADVERUM BIOTECHNOLOGIES INC 439 8,321 1,537 AECOM 283 12,113 17,920 AERIE PHARMACEUTICALS INC 78 2,709 1,249 AERSALE CORP 2,551 30,599 31,785 AES CORP/THE 1,294 17,534 33,735 AFFILIATED -

NASDAQ Stock Market

Nasdaq Stock Market Friday, December 28, 2018 Name Symbol Close 1st Constitution Bancorp FCCY 19.75 1st Source SRCE 40.25 2U TWOU 48.31 21st Century Fox Cl A FOXA 47.97 21st Century Fox Cl B FOX 47.62 21Vianet Group ADR VNET 8.63 51job ADR JOBS 61.7 111 ADR YI 6.05 360 Finance ADR QFIN 15.74 1347 Property Insurance Holdings PIH 4.05 1-800-FLOWERS.COM Cl A FLWS 11.92 AAON AAON 34.85 Abiomed ABMD 318.17 Acacia Communications ACIA 37.69 Acacia Research - Acacia ACTG 3 Technologies Acadia Healthcare ACHC 25.56 ACADIA Pharmaceuticals ACAD 15.65 Acceleron Pharma XLRN 44.13 Access National ANCX 21.31 Accuray ARAY 3.45 AcelRx Pharmaceuticals ACRX 2.34 Aceto ACET 0.82 Achaogen AKAO 1.31 Achillion Pharmaceuticals ACHN 1.48 AC Immune ACIU 9.78 ACI Worldwide ACIW 27.25 Aclaris Therapeutics ACRS 7.31 ACM Research Cl A ACMR 10.47 Acorda Therapeutics ACOR 14.98 Activision Blizzard ATVI 46.8 Adamas Pharmaceuticals ADMS 8.45 Adaptimmune Therapeutics ADR ADAP 5.15 Addus HomeCare ADUS 67.27 ADDvantage Technologies Group AEY 1.43 Adobe ADBE 223.13 Adtran ADTN 10.82 Aduro Biotech ADRO 2.65 Advanced Emissions Solutions ADES 10.07 Advanced Energy Industries AEIS 42.71 Advanced Micro Devices AMD 17.82 Advaxis ADXS 0.19 Adverum Biotechnologies ADVM 3.2 Aegion AEGN 16.24 Aeglea BioTherapeutics AGLE 7.67 Aemetis AMTX 0.57 Aerie Pharmaceuticals AERI 35.52 AeroVironment AVAV 67.57 Aevi Genomic Medicine GNMX 0.67 Affimed AFMD 3.11 Agile Therapeutics AGRX 0.61 Agilysys AGYS 14.59 Agios Pharmaceuticals AGIO 45.3 AGNC Investment AGNC 17.73 AgroFresh Solutions AGFS 3.85 -

Based on Our Discussion with Radford, Management Identified Our Peer Companies to Include the Following 19 Biotechnology and Pharmaceutical Companies for 2015

Based on our discussion with Radford, management identified our peer companies to include the following 19 biotechnology and pharmaceutical companies for 2015: Ariad Pharmaceuticals Inc. Infinity Pharmaceuticals, Inc. Progenics Pharmaceuticals, Inc. Array BiopPharma, Inc. Lexicon Pharmaceuticals, Inc Repligen Corporation Celldex Therapeutics, Inc. MacroGenics, Inc. Spectrum Pharmaceuticals, Inc. CTI BioPharma Corp. Merrimack Pharmaceuticals, Inc. Synta Pharmaceuticals Corp. DepoMed Inc. NewLink Genetics Corporation XOMA Corporation Halozyme Therpeutics, Inc. OncoMed Pharmaceuticals, Inc. Immunomedics Inc. Peregrine Pharmaceuticals, Inc These peer companies were selected from among publicly-held U.S. pharmaceutical and biotechnology companies with comparable operations in mid– to late–stages of product development or small commercial products in the U.S. based on the following criteria: number and stage of development programs; number of employees; market capitalization; and number of and revenue from commercial products. The market data included information as to base salaries, cash bonuses and stock option awards. Use of Compensation Consultants Our Compensation Committee is authorized to retain its own independent advisors to assist in carrying out its responsibilities. Our Compensation Committee engaged Radford to analyze historic compensation and establish recommendations for executive compensation for 2015 and methodologies for determining compensation on an on-going basis. Benchmarking in the Context of Our Other Executive Compensation Principles Our Compensation Committee and our Board of Directors use market data as one means of evaluating and establishing executive pay. In instances where an executive officer is believed to be especially suited to our company or important to our success, the Compensation Committee may establish or recommend compensation that deviates from industry averages or other specific benchmarks. -

Guidelines with Regard to the Composition, Calculation and Management of the Index

INDEX METHODOLOGY Solactive Pharma Breakthrough Value Index Version 2.1 dated September 03, 2020 Contents Important Information 1. Index specifications 1.1 Short Name and ISIN 1.2 Initial Value 1.3 Distribution 1.4 Prices and Calculation Frequency 1.5 Weighting 1.6 Index Committee 1.7 Publication 1.8 Historical Data 1.9 Licensing 2. Composition of the Index 2.1 Selection of the Index Components 2.2 Ordinary Adjustment 2.3 Extraordinary Adjustment 3. Calculation of the Index 3.1 Index Formula 3.2 Accuracy 3.3 Adjustments 3.4 Dividends and other Distributions 3.5 Corporate Actions 3.6 Correction Policy 3.7 Market Disruption 3.8 Consequences of an Extraordinary Event 4. Definitions 5. Appendix 5.1 Contact Details 5.2 Calculation of the Index – Change in Calculation Method 2 Important Information This document (“Index Methodology Document”) contains the underlying principles and regulations regarding the structure and the operating of the Solactive Pharma Breakthrough Value Index. Solactive AG shall make every effort to implement regulations. Solactive AG does not offer any explicit or tacit guarantee or assurance, neither pertaining to the results from the use of the Index nor the Index value at any certain point in time nor in any other respect. The Index is merely calculated and published by Solactive AG and it strives to the best of its ability to ensure the correctness of the calculation. There is no obligation for Solactive AG – irrespective of possible obligations to issuers – to advise third parties, including investors and/or financial intermediaries, of any errors in the Index. -

Fidelity® Select Portfolio® Biotechnology Portfolio

Quarterly Holdings Report for Fidelity® Select Portfolio® Biotechnology Portfolio May 31, 2021 BIO-QTLY-0721 1.802156.117 Schedule of Investments May 31, 2021 (Unaudited) Showing Percentage of Net Assets Common Stocks – 97.4% Shares Value Shares Value Biotechnology – 89.4% CareDx, Inc. (a) 178,500 $ 14,351,400 Biotechnology – 89.4% Celldex Therapeutics, Inc. (a) 337,900 9,444,305 4D Molecular Therapeutics, Inc. 214,868 $ 5,706,894 Cellectis SA sponsored ADR (a) (b) 157,465 2,467,477 AbbVie, Inc. 9,829,284 1,112,674,949 Cerevel Therapeutics Holdings (a) 201,800 2,647,616 ACADIA Pharmaceuticals, Inc. (a) 199,594 4,458,930 ChemoCentryx, Inc. (a) 2,062,222 20,931,553 Acceleron Pharma, Inc. (a) 924,453 121,001,653 Chinook Therapeutics, Inc. (a) 840,646 13,870,659 ADC Therapeutics SA (a) (b) 755,238 16,350,903 Chinook Therapeutics, Inc. rights (a) (d) 115,821 5,791 Agios Pharmaceuticals, Inc. (a) 1,075,059 59,966,791 Codiak Biosciences, Inc. (b) 436,539 9,874,512 Akouos, Inc. (a) (b) 716,626 9,359,136 Coherus BioSciences, Inc. (a) 58,387 768,373 Albireo Pharma, Inc. (a) (b) 320,350 10,715,708 Connect Biopharma Holdings Ltd. ADR (a) 1,079,600 16,064,448 Aldeyra Therapeutics, Inc. (a) 1,201,911 15,047,926 Constellation Pharmaceuticals, Inc. (a) (b) 90,259 1,788,031 Alector, Inc. (a) (b) 998,482 17,772,980 ContraFect Corp. (a) (b) 456,309 1,843,488 Allakos, Inc. (a) 207,631 21,062,089 Cortexyme, Inc. -

Preclinical Evidence for and Clinical Development of XERMELO in Cancer Ranuka Iyer, M.D

April 10, 2018 Welcome and Introduction Kimberly Lee, D.O. Head of Investor Relations and Corporate Strategy Precision Science. Pioneering Medicine. Patient Driven. 0 ©Precision 2018 Lexicon Pharmaceuticals, Science. Inc. Pioneering Medicine. Patient Driven. Forward-looking Statements This presentation, including any oral presentation accompanying it, contains “forward- looking statements,” including statements about Lexicon’s strategy and operating performance and events or developments that we expect or anticipate will occur in the future, such as projections of our future results of operations or of our financial condition, the level of market acceptance and commercial success of XERMELO®, the results of and expected timing of the completion of our ongoing and future clinical trials, the expected timing and outcome of discussions with regulatory authorities regarding such trials, the expected timing of initiation of our other planned clinical trials, the expected enrollment in our ongoing and future clinical trials, our other research and development efforts, the status of activities performed under our collaborative agreements and the anticipated trends in our business. These forward-looking statements are based on management’s current assumptions and expectations and involve risks, uncertainties and other important factors that may cause Lexicon’s actual results to be materially different from any future results expressed or implied by such forward-looking statements. Information identifying such important factors is contained in our most recent annual report on Form 10-K and quarterly reports on Form 10-Q, including the sections entitled “Risk Factors,” as well as our current reports on Form 8-K, in each case filed with the Securities and Exchange Commission. -

Preliminary Healthcare Agenda 01.03X

29th Annual J.P. Morgan Healthcare Conference January 10 - 13, 2011 Westin St. Francis Hotel, San Francisco, CA Preliminary Conference Agenda SUNDAY, JANUARY 9 - Registration in Tower Salon A - 3 to 9 PM MONDAY, JANUARY 10 - Registration in Tower Salon A - 6:45 AM, Breakfast in Italian Foyer Grand Ballroom Colonial Room California West California East Elizabethan A/B Elizabethan C/D Alexandra's Breakout: Borgia Room Breakout: Georgian Room Breakout: Olympic Room Breakout: Yorkshire Room Breakout: Sussex Room Private Company Track Not-for-Profit Track 7:30 AM Opening Remarks: Doug Braunstein - Chief Financial Officer, JPMorgan Chase & Co., Grand Ballroom Astra Tech 8:00 AM Celgene Corporation Kinetic Concepts, Inc Alkermes, Inc. Biocon Limited Catalent (private company) 8:30 AM Express Scripts Inc. Agilent Technologies Inc. Beckman Coulter Inc. Bio-Rad Laboratories, Inc. Quality Systems Axcan Intermediate Holdings 9:00 AM Roche Holding AG Zimmer Holdings, Inc. Genoptix, Inc. ImmunoGen, Inc Health Net Inc. Merrimack Pharmaceuticals Inc. Vertex Pharmaceuticals Allscripts Healthcare Solutions, 9:30 AM Medicis Pharmaceutical Corp. Lonza Group Ltd Henry Schein Inc. Surgical Care Affiliates Incorporated Inc. 10:00 AM Medtronic, Inc. WellPoint, Inc. Onyx Pharmaceuticals Inc. Sigma-Aldrich Corporation Align Technology Inc.* Symphogen 10:30 AM Room Not Available Medco Health Solutions, Inc. Smith & Nephew plc* Medivation, Inc. Lexicon Pharmaceuticals, Inc. Zeltiq Aesthetics 11:00 AM Room Not Available Merck KGaA Perrigo Company Healthways Incorporated BioMimetic Therapeutics, Inc. Penumbra, Inc. 11:30 AM Room Not Available Dendreon Corporation Gen-Probe Inc. Select Medical Corporation ArthroCare Corporation PTC Therapeutics, Inc. 12:00 PM Luncheon & Keynote: Nancy-Ann DeParle - Counselor to the President and Director of the White House Office of Health Reform, Grand Ballroom Endo Pharmaceuticals Holdings 1:30 PM Room Not Available Amylin Pharmaceuticals Inc. -

Rebateable Manufacturers

Rebateable Labelers – July 2021 Manufacturers are responsible for updating their eligible drugs and pricing with CMS. Montana Healthcare Programs will not pay for an NDC not updated with CMS. Note: Some manufacturers on this list may have some NDCs that are covered and others that are not. Manufacturer ID Manufacturer Name 00002 ELI LILLY AND COMPANY 00003 E.R. SQUIBB & SONS, LLC. 00004 HOFFMANN-LA ROCHE 00006 MERCK & CO., INC. 00007 GLAXOSMITHKLINE 00008 WYETH PHARMACEUTICALS LLC, 00009 PHARMACIA AND UPJOHN COMPANY LLC 00013 PFIZER LABORATORIES DIV PFIZER INC 00015 MEAD JOHNSON AND COMPANY 00023 ALLERGAN INC 00024 SANOFI-AVENTIS, US LLC 00025 PFIZER LABORATORIES DIV PFIZER INC 00026 BAYER HEALTHCARE LLC 00032 ABBVIE INC. 00037 MEDA PHARMACEUTICALS, INC. 00039 SANOFI-AVENTIS, US LLC 00046 WYETH PHARMACEUTICALS INC. 00049 ROERIG 00051 ABBVIE INC 00052 ORGANON USA INC. 00053 CSL BEHRING L.L.C. 00054 HIKMA PHARMACEUTICAL USA, INC. 00056 BRISTOL-MYERS SQUIBB PHARMA CO. 00065 ALCON LABORATORIES, INC. 00068 AVENTIS PHARMACEUTICALS 00069 PFIZER LABORATORIES DIV PFIZER INC 00071 PARKE-DAVIS DIV OF PFIZER 00074 ABBVIE INC 00075 AVENTIS PHARMACEUTICALS, INC. 00078 NOVARTIS 00085 SCHERING CORPORATION 00087 BRISTOL-MYERS SQUIBB COMPANY 00088 AVENTIS PHARMACEUTICALS 00093 TEVA PHARMACEUTICALS USA, INC. 00095 BAUSCH HEALTH US, LLC Page 1 of 19 Manufacturer ID Manufacturer Name 00096 PERSON & COVEY, INC. 00113 L. PERRIGO COMPANY 00115 IMPAX GENERICS 00116 XTTRIUM LABORATORIES, INC. 00121 PHARMACEUTICAL ASSOCIATES, INC. 00131 UCB, INC. 00132 C B FLEET COMPANY INC 00143 HIKMA PHARMACEUTICAL USA, INC. 00145 STIEFEL LABORATORIES, INC, 00168 E FOUGERA AND CO. 00169 NOVO NORDISK, INC. 00172 TEVA PHARMACEUTICALS USA, INC 00173 GLAXOSMITHKLINE 00178 MISSION PHARMACAL COMPANY 00185 EON LABS, INC. -

CMO Summit East 2014 Brochure

CHIEF MEDICAL OFFICER SUMMIT ADDRESSING THE COMPLEX DUAL ROLE OF MANAGING R&D WHILE RAISING CAPITAL FOR BIOTECHS MAY 5 - 6, 2014 RITZ CARLTON, BOSTON COMMON, BOSTON, MA CO-CHAIR: CO-CHAIR: Lee Allen, MD, PhD Steven Zelenkofske, DO, FACC, FACOI, FCCP CMO SVP, Clinical and Medical Affairs & CMO Spectrum Pharmaceuticals Regado Biosciences FEATURED SPEAKER: FEATURED SPEAKER: FEATURED SPEAKER: Jakob Dupont, MD Ken Getz, MBA Pamela Palmer, MD, PhD SVP & CMO Director of Sponsored CMO & Co-Founder OncoMed Research AcelRX Pharmaceuticals, Tufts CSDD Inc. NEW FOR 2014 Keynote Case Study on the Life of a CMO How to Get Your Drug Positioned Pre and Post IPO for Reimbursement • • Best Practices to Position Your Drug for Career Development Opportunities for CMOs Regulatory Approval • • CEO Panel: What do CEOs look for in a Working through Complex Contracts CMO? • • Publication Strategy: Objectives, Organization How Investors Determine Valuation of and Process Biotechs Executive Sponsors Associate Sponsors Exhibitor Organized by TO REGISTER, VISIT WWW.THECONFERENCEFORUM.ORG OR CALL 646-350-2580 CHIEF MEDICAL OFFICER SUMMIT OVERVIEW Elizabeth Bard OVERVIEW Business Development Manager The Conference Forum’s Second Annual Chief Medical David Borrok Officer Summit for Emerging Life Science Companies is Business Development Manager delighted to present a truly distinctive and interactive event for CMOs. We are grateful to Dr. Elizabeth Stoner, Meredith Sands Managing Director, MPM Capital, for suggesting the idea Executive Director, Business Development and to our CMO advisers for their insights on content and agenda development. We are Dedicated to Accomplishing Two Goals SPEAKING FACULTY • To bring together CMO executives to address the unique challenges associated with directing and Lee Allen, MD, PhD managing all R&D functions with limited resources, CMO while raising capital, working and meeting with Spectrum Pharmaceuticals investors and strategizing for appropriate exits. -

2019 GCSG US Conference Attendee List

2019 GCSG US Conference Attendee List Last Name First Name Company Position Abbey Tara PRA Healthsciences Recruiter Adelakun Tosin University of Georgia Student Adenuga Femi Vertex Senior Manager, Supply Chain Alves Luis Tesaro Manager, Clinical Supply Chain Annan Ingrid Regeneron Clinical Logistics Associate II Anne Sandeep Genentech Clinical Demand and Supply Leader Cooperative Studies Apodaca Carlos Program Lab Technician Arantes Viviane Pfizer Sr Regional Manager LATAM Arora Anu Horizon Pharma Sr. Supply Chain Analyst Intercept Arredondo Frank Pharmaceuticals Clinical Supplies Asuncion Al Arena Pharmaceuticals Head, Global Supply Chain Atchley Andrew Arena Pharmaceuticals Clinical Supply Associate Au Stephanie Merck & Co., Inc Project Manager, Packaging and Labeling Bagavathinathan Sharmila Biogen Lead Bailey Scott BeiGene Director of Clinical Supply Chain Bains Cal Adiramedica Director of Business Development Baker Kevin Inceptua Account Executive Balanovsky Natalie Almac Group JIT Manufacturing Solutions Manager Balawajder Stephen Horizon Pharma Manager, Clinical Trial Supply Barnes Nicola Pfizer R&D UK Limited Senior Director Baysinger Tammy SpringWorks Sr. Manager - Drug Supply Belcher Lindsay Cryoport Business Development Director Bell Yolanda Deciphera Head of Clinical Supply Operations Bentley Renae Thermo Fisher Scientific Sr. Manager Bergonio Gregory Klus Pharma. Inc. Director, Clinical Operation Berlanga Harry Fisher Clinical Services Quality Director & QP bertrand jeff bertrand clinical label CEO Bhandari Arvind Adiramedica CEO & President Bishop Tammy Avayle CTS Partner Bliss Frank Shionogi Inc Associate Director, IMP Management blood andrea Modera Clinical Supplies Manager Bogle Heather Almac Group Supply Chain Solutions Manager Bonsu Stephen Celgene Corporation Director - Strategic Program Management Bowne Caitlin Alkermes Associate Director, Clinical Supply Chain Bracey Jonathan Tanner Pharma EVP Corporate Development Brady Tom Xerimis, Inc. -

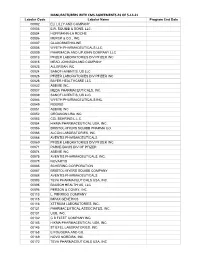

MANUFACTURERS with CMS AGREEMENTS AS of 5-14-21 Labeler Code Labeler Name Program End Date 00002 ELI LILLY and COMPANY 00003 E.R

MANUFACTURERS WITH CMS AGREEMENTS AS OF 5-14-21 Labeler Code Labeler Name Program End Date 00002 ELI LILLY AND COMPANY 00003 E.R. SQUIBB & SONS, LLC. 00004 HOFFMANN-LA ROCHE 00006 MERCK & CO., INC. 00007 GLAXOSMITHKLINE 00008 WYETH PHARMACEUTICALS LLC, 00009 PHARMACIA AND UPJOHN COMPANY LLC 00013 PFIZER LABORATORIES DIV PFIZER INC 00015 MEAD JOHNSON AND COMPANY 00023 ALLERGAN INC 00024 SANOFI-AVENTIS, US LLC 00025 PFIZER LABORATORIES DIV PFIZER INC 00026 BAYER HEALTHCARE LLC 00032 ABBVIE INC. 00037 MEDA PHARMACEUTICALS, INC. 00039 SANOFI-AVENTIS, US LLC 00046 WYETH PHARMACEUTICALS INC. 00049 ROERIG 00051 ABBVIE INC 00052 ORGANON USA INC. 00053 CSL BEHRING L.L.C. 00054 HIKMA PHARMACEUTICAL USA, INC. 00056 BRISTOL-MYERS SQUIBB PHARMA CO. 00065 ALCON LABORATORIES, INC. 00068 AVENTIS PHARMACEUTICALS 00069 PFIZER LABORATORIES DIV PFIZER INC 00071 PARKE-DAVIS DIV OF PFIZER 00074 ABBVIE INC 00075 AVENTIS PHARMACEUTICALS, INC. 00078 NOVARTIS 00085 SCHERING CORPORATION 00087 BRISTOL-MYERS SQUIBB COMPANY 00088 AVENTIS PHARMACEUTICALS 00093 TEVA PHARMACEUTICALS USA, INC. 00095 BAUSCH HEALTH US, LLC 00096 PERSON & COVEY, INC. 00113 L. PERRIGO COMPANY 00115 IMPAX GENERICS 00116 XTTRIUM LABORATORIES, INC. 00121 PHARMACEUTICAL ASSOCIATES, INC. 00131 UCB, INC. 00132 C B FLEET COMPANY INC 00143 HIKMA PHARMACEUTICAL USA, INC. 00145 STIEFEL LABORATORIES, INC, 00168 E FOUGERA AND CO. 00169 NOVO NORDISK, INC. 00172 TEVA PHARMACEUTICALS USA, INC Labeler Code Labeler Name Program End Date 00173 GLAXOSMITHKLINE 00178 MISSION PHARMACAL COMPANY 00185 EON LABS, INC. 00186 ASTRAZENECA PHARMACEUTICALS LP 00187 BAUSCH HEALTH US, LLC. 00206 WYETH PHARMACEUTICALS LLC, 00224 KONSYL PHARMACEUTICALS, INC. 00225 B. F. ASCHER AND COMPANY, INC. 00228 ACTAVIS PHARMA, INC. -

Sponsors Experience

sponsors experience Abbott Eli Lilly Merck & Co. Sano-Aventis Aegerion Emergent Biosolutions Merz Pharmaceuticals Sano-Pasteur Allergen Exact Sciences Metabasis Therapeutics Sano-Synthelabo Alpharma Forbes Medi-Tech Nabi Pharmaceuticals Schering-Plough Altana Forest NanoBio Schwarz Pharmaceuticals Amgen Furiex Neuraxon Searle Amylin G&W Labs Neurogen Shionogi Arena Pharmaceuticals Galderma Novartis Solvay Astellas Genentech Novavax Stiefel Laboratories AstraZeneca Genomic Collaboration Noven Pharmaceuticals Surface Logix Aventis Gilead Novo Nordisk Takeda Barr GlaxoSmithKline Omthera Pharmaceuticals TAP Baxter Healthcare GlaxoSmithKline Biologicals Ortho McNeil Taro Pharmaceuticals Bayer Healthcare Glaxo Wellcome Pain Therapeutics Teva Pharmaceuticals Berlex Glenmark Pharmaceuticals Palatin Therapeutics Tioga Bertek Hoechst-Marion Roussel PaxVax TorreyPintes Therapeutics Bionovo Homan LaRoche Pharmacia Triangle Biovail IDEA AG Pharmos Corporation Trimel Biopharma Boehringer Ingelheim Impax Laboratories Pzer Tylenol Bristol-Myers Squibb Insmed Pozen UCB Centocor Jazz Pharmaceuticals Procter & Gamble Vanguard Cipher Johnson & Johnson ProEthic Vaxinnate Collagenex King Pharmaceuticals Promius Pharmaceuticals Viro Pharma Covidien KOS Pharmaceuticals QLT Warner Chilcott Daiichi Sankyo KOWA Pharmaceuticals Quinnova Pharmaceuticals Watson Pharmaceuticals DepoMed Lexicon Pharmaceuticals Rhone-Poulenc Rorer Wyeth Dow Marine Polymer Technologies Roche Wyeth Ayerst Dupont Merck Meade Johnson Roche Diagnostics Xenoport Duramed Medimmune R.W.T. XOMA LTD Dynport Vaccine Company Medivir Sankyo Yamanouchi If you would like more details about a potential clinical study opportunity with Coastal Carolina Research Center please contact: Nathan Morton Director of Business Development Phone #: 843-856-3784 Fax #: 843-856-3788 Email: [email protected] Study Experience Sponsors Experience CRO Experience.