Jumbo Group(JUMBO SP)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Dine and Win Mall & Restaurant List 23March.Indd

AL GHURAIR CENTRE TIM HORTONS CAFÉ AND BAKE SHOP ALL THE PERKS ESPRESSO CAFÉ UMAMI BASKIN ROBBINS WENDY’S BESTOON SAMAD WING.STOP BIKANERVALA STAR RESTAURANT YAKITATE BUBEE DRINKS CAFFE NERO AL KHAIL GATE COMMUNITY CENTRE CHARLEY’S GRILLED SUBS ARABIAN GRILL RESTAURANT CO. CHIC BOY RESTAURANT CAFETERIA AL KHAIL EXPRESS CHINESE PALACE CHENNAI CURRY PALACE RESTAURANT CHOWKING ORIENT RESTAURANT KFC CINNABON & SEATTLE’S BEST COFFEE LIMS CAFE DENNY’S MADRAS KITCHEN RESTAURANT DIN TAI FUNG RESTAURANT NEW ALBAYAN RESTAURANT - CHICKING DQ GRILL & CHILL QASR ANTAR CAFETERIA FARSI RESTAURANT HAPPY LEMON IL FORNO UNO ARABIAN CENTRE IRVINS BASKIN ROBINS JOLLIBEE BOMBAY CHOWPATHY KFC CHINESE PALACE KRISPY KREME COSTA COFFEE LEMON BAR GLORIA JEAN’S COFFEES MANOUSHE STREET HARDEES MARU UDON HATAM RESTAURANT MCDONALD’S JUNGLE JUICE MCDONALD’S KFC MUKALLA HADHRAMI HONEY MADFOON AL SADDA PAPA JOHNS (JAWAD RESTAURANT) MCDONALD’S PAPPAROTI NEW YORK FRIES PAUL BOULANGERIE PATTISSERIE PIZZA HUT PIZZA HUT SECOND CUP RETRO 7 CAFÉ STARBUCKS COFFEE SHOP STARBUCKS SULTAN BABA EXPRESS TONY ROMAS TAPA KING VANELLIS TERIYAKI BOY / SIZZLIN’ STEAK VIVEL THE CHOCO MONARCH COFFEE SHOP YALLA SAJ BAY AVENUE NJOY CHOCOLATIER & CAFÉ ATTIBASSI OAKBERRY BASKIN ROBBINS PAUL CAFÉ BIKANERVALA PIZZA HUT BURGER KING SARAVANAA BHAVAN CAFÉ FUNKIE TOWN STARBUCKS 25 MAR - 17 APR CARIBOU SUBWAY COSTA UNCLE DEEK ENSO RESTAURANT WHEEL 35 FARSI RESTAURANT YELLOW CHILLI FILLI CAFÉ GAZEBO SHOROOQ COMMUNITY HOT & SPICY CENTRE KABABJI CIRCLE RESTAURANT KAMAT KABABJI KCAL MISTER BAKER KFC PROJECT KUNAFA CAFE KULFILICIOUS STARBUCKS LA BRIOCHE LA FRAGOLA THE MALL MALAK AL TWOOK ARABIAN TEA HOUSE METRO FALCON BURGER KING MOSAIC GOURMET COSTA COFFEE MOTI MAHAL NOODLE EXPRESS RESTAURANT UPTOWN MIRDIFF PAPA JOHNS AL HAKAWATI PIZZA HUT AL ARAB RESTAURANT RAJU OMLET AL SAYER RETAIL EST. -

(Awarded in 6X STAR$®) with the American Express® Capitacard

Earn up to 3% rebate (Awarded in 6X STAR$®) with The American Express® CapitaCard Participating Merchants at CapitaLand Malls in town (S$1 spend = 30 STAR$®, T&Cs Apply) Updated as of 1 July 2021 Important Notes Please visit amex.co/capitacardterms for the full terms and conditions for earning STAR$® with your American Express® CapitaCard. Please note that under the terms and conditions: 1. Additional 25 STAR$® will be awarded, on top of the base 5 STAR$, on eligible purchases of goods and services, in blocks of S$1, on a cumulative basis at the end of every calendar month, capped at S$1,200 per calendar month. 2. On top of excluded charges and purchases, the following transactions are also not eligible to earn additional 25 STAR$®: charges at pushcarts, temporary vendors/pop-up shops, events, roadshows, SISTIC, SAM machines and AXS machines within CapitaLand Malls in town. American Express International Inc (UEN S68FC1878J) 1 Marina Boulevard #22-00, One Marina Boulevard, Singapore 018919. americanexpress.com.sg. Incorporated with Limited Liability in the State of Delaware, U.S.A ®Registered Trademark of American Express Company. © Copyright 2021 American Express Company. AXP Public 1 American Express® CapitaCard Participating Merchants @ Bugis Junction 200 Victoria Street Singapore 188021 Participating Merchant Name 6IXTY8IGHT Hi-Tec Mobile Polar Puffs & Cakes Action City HLH SABER LILY Pop Mart adidas HoneyMoon Dessert Premier Football Ajisen Ramen Honguo Purpur Akihabara HP By AddOn Q & M Dental Centre (Bugis) Alcoholiday HUAWEI Raffles -

Largest International F&B Showcase in Asia

31 MAR TO 03 APR 2020 SINGAPORE EXPO www.fhaFnB.com DISCOVER THE LARGEST INTERNATIONAL F&B SHOWCASE IN ASIA SECURE YOUR CHOICE LOCATION TODAY! Organiser Join us on Food&HotelAsia #FHA Featuring the most exceptional line-upFeaturing of globalthe most food exceptional & Join line-up theof global largestFeaturingfood & theJoin most international exceptional the line-uplargest of global foodinternational & beverage companies, FHA-Foodbeverage & Beverage companies, is a major FHA-Food & Beverage is abeverage major companies, FHA-Food & Beverage is a major event where industry professionalsevent in Asia where source industry F&Bprofessionals showcase in Asia sourceeventF&B where in industry Asiashowcase professionals in Asia sourcein Asia conveniently from around the worldconveniently in one place. from Evolved around the world in one place.conveniently Evolved from around the world in one place. Evolved from the highly successful Food&HotelAsiafrom the highly (FHA), successful this is Food&HotelAsiato cater (FHA), tofrom this thetheis highlyto region’s successful cater Food&HotelAsia to the (FHA), region’s this is the platform for international suppliersthe platform to establish for international their suppliers to establishthe their platform for international suppliers to establish their presence, launch new products presence,and harness launch the newever-growing products and harness the presence,ever-growing and launch new products and harness and the promising business opportunitiespromising in Asia market business to opportunities in -

Din Tai Fung As a Global Shanghai Dumpling House Made in Taiwan Haiming Liu

Flexible Authenticity Din Tai Fung as a Global Shanghai Dumpling House Made in Taiwan Haiming Liu Haiming Liu, “Flexible Authenticity: Din Tai Fung as a Global known in Taiwan, Hong Kong, or mainland China. Chinese Shanghai Dumpling House Made in Taiwan,” Chinese America: food in America reflected the racial status of Chinese Ameri- History & Perspectives —The Journal of the Chinese Histori- cans. The Chinese restaurant business, like the laundry busi- cal Society of America (San Francisco: Chinese Historical Soci- ness, was a visible menial-service occupation for Chinese ety of America with UCLA Asian American Studies Center, 2011), immigrants and their descendants. 57–65. Ethnic food also reflects immigration history. After the 1965 immigration reform, new waves of Chinese immigrants arrived. Between 1965 and 1984, an estimated 419,373 Chi- CHANGES IN THE CHINESE AMERICAN nese entered the United States.5 Post-1965 Chinese immi- REstaURANT BUSINESS grants were far more diverse in their class and cultural back- grounds than the earlier immigrants had been. Many were n December 4, 2007, the Taiwan government spon- educated professionals, engineers, technicians, or exchange sored Din Tai Fung, a steamed dumpling house in students. Their arrival fostered a new, booming Chinese res- Taipei, to hold a gastronomic demonstration in Paris taurant business in America, especially in regions such as O 1 as a diplomatic event to promote its “soft power.” Though the San Gabriel Valley in Southern California and Queens in the cooking show was held by a pro-independence regime, New York, where Chinese populations concentrated. the restaurant actually featured Shanghai cuisine rather than Accordingly, food in Chinese restaurants in Amer- native Taiwanese food. -

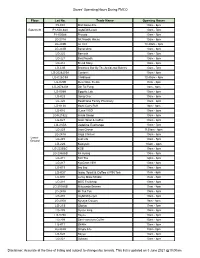

Tenant Ops Hours CMCO 14-27 Oct 20

Stores' Operating Hours During MCO 2.0 Floor Lot No. Trade Name Opening Hours P2-K01 Mail Boxes Etc 10am - 9pm P1-K02,3&4 myNEWS.com 10am - 8pm P1-K05&6 Pressto 10am - 7pm LG-231A AK Noodle House LG-K11 Ambon Boenda 11am - 8pm LG-203B An Viet LG-C7 Any+Wear 11am - 8pm LG-C1 Backley 10am - 8pm LG-243B Bananabro 11am - 7pm LG-225 Barcook 10am - 8pm LG-221 Boat Noodle 10am - 8pm LG-228 Bottles2 10am - 8pm LG-212 Bread Story 10am - 8pm LG-C3B Brownies Bar By The Accidental Bakers 10am - 8pm LG-202&203A Canton-i LG-C8&C9 Childhood 9.45am - 7pm LG-C2&C3A Cold Stone Creamery . 12pm - 8pm LG-K25B Delectable Treats LG-207&208 Din Tai Fung LG-K08A Eggette Lab 10am - 7pm LG-K23 Gong Cha LG-220 Healthlane Family Pharmacy 10am - 10pm LG-K13A Homi Curry Puff 10am - 8pm LG-K19 llao llao 11am - 9pm LG-K16 I Love YOO! LG-K21&22 Inside Scoop LG-K27 Issac Toast & Coffee X Pin Tea 10am - 8pm LG-237A Jadeline Exchange 10am - 8pm Lower Ground LG-241A Jinjja Chicken 10am - 10pm LG-245 Just Life 10am - 7pm LG-226 Kakiyuki 11am - 8pm LG-236A&B Ko Hyang 10am - 8pm LG-211 KOI The 12pm - 8pm LG-217 KyoChon 1991 LG-K01 Lucky Mala Noodle 11am - 9pm LG-218 MBG Fruitshop LG-201A&B Mitsuyado Seimen 10am - 8pm LG-243A Mr Tuk Tuk 10am - 9pm LG-238 myNEWS.com 10am - 8pm LG-230A Nyonya Colours 10am - 9pm LG-215 Oloiya 10am - 8pm LG-235 Oyster King 10am - 8pm LG-K25A Royce 11am - 8pm LG-C10 Pin & Petals 10am - 7pm LG-206 Purple Cane Tea House 10am - 10pm LG-239 San Francisco Coffee 7.30am - 8pm LG-K17 Shihlin 10am - 10pm LG-232A Simple Life 10am - 8pm LG-K28 Soyya 11am - 8pm LG-227 Subway 10am - 10pm LG-241B Taimal Herbs 10am - 8pm LG-K09 Tealive LG-213 The Chicken Rice Shop LG-223 The Fish Bowl Disclaimer: Accurate at the time of listing and subject to changes by tenants. -

Something Old

Need Past Issues? LOVE US, “LIKE US” WEEKENDER WK11B / MICA (P) 144/08/2012 www.facebook.com/ www.facebook.com/ weekendersgp weekendersgp DECEMBER 14 - 20, 2012 YOUR INSPIRATION TO A WEEKEND FILLED WITH FUN AND HAPPINESS DELIVERED FREE TO YOUR HOME INSIDE... >> 06 TASTES LIKE SOMETHING OLD, CHRISTMAS Gourmet roasts, coffee baby pork ribs, and fusion desserts - check out some of this festive season’s SOMETHING yummiest offerings. 08 HERE’s HOSSAN! Comedian Hossan Leong reveals his proudest NEW achievements this year, and DIRECTORS ROYSTON TAN, VICTRIC the perennial importance of THNG AND EVA TANG PRESENT THE char kway teow. DOCUMENTARY OLD ROMANCES, a love letter to singapore’s 10 GOING FOR DISAPPEARING HISTORIES GOLD BY CHERYL CHIA National sprinter Gary Yeo tells us more about the hurdles and triumphs of his sporting career, and the medals he’s got his eye on. 12 HOLIDAY AT HOME Sentosa’s Palawan Beach is the perfect island getaway if you’re looking for an easy, breezy staycation with fun activities for the kiddies. Like our page on: • Continues on page 3... facebook.com/weekendersgp For a pdf copy visit: www.facebook.com/weekendersgp 02 • WEEKENDER • DECEMBER 14 - 20, 2012 YOUR INSPIRATION TO A WEEKEND FILLED WITH FUN AND HAPPINESS For a pdf copy of Weekender = FREE VENTS visit: www.facebook.com/weekendersgp All events are correct at time of print. ATTRACTIONS Encounter: When E MUST the virtuosos of East SEE meet West GLITZ 18 Dec, 7.30pm, $25 AND GLAMOUR NEX Lions RESORTS WORLD SENTOSA CELEBRATES ITS GRAND OPENING Cup ending THEIR 2012 season on a special note, Ding Yi Music Company will be collaborating 14 & 16 Dec, various times, $5 - $40 with leading Singapore chamber group, I-Sis Singapore’S first integrated resort celebrated Trio. -

San Marino High School PTSA Scrip

San Marino High School PTSA Scrip NAME: ____________________________________________ TEL: _______________ ADDRESS: _________________________________________ DATE:______________ Make checks payable to SMHS PTSA SCRIP. Credit cards are accepted for amounts over $2000. Credit Card Number: _________________________________ Expiration Date: _____________ *** See Reverse Side for contact details *** STORE DENOM TOTAL STORE DENOM TOTAL AMC Theatres $25 Jamba Juice $10 American Eagle $25 JCPenney $25 Baja Fresh $25 JoAnn Fabrics $20 Barnes & Noble $25 Johnny Rockets $5 Baskin Robbins $2 KFC $5 Bath & Body Works $10 L.L. Bean $25 $25 Macy’s $25 Bed Bath & Beyond $25 Marie Callendar’s $25 Best Buy $25 Marshalls $25 Blockbuster $10 Office Depot $25 B-Man’s $25 Olive Garden $25 Borders $10 Orvis $25 $25 Peet’s Coffee $20 Boston Market $10 Pier 1 Imports $25 Bristol Farms $20 Pizza Hut $10 Buca di Beppo $25 Pottery Barn $25 Burger King $10 Quiznos $5 California Pizza Kitchen $10 Ranch 99 $20 Carl’s Jnr $5 Ritz-Carlton Hotels $50 Chili’s/Corner Bakery $20 Ross $25 Claim Jumper $25 Sears $25 Coffee Bean $25 $100 CompUSA $25 See’s Candies $14.10 Crate & Barrel $25 Sharper Image $50 CVS Pharmacy $25 Smart & Final $25 Dave & Busters $25 $100 Denny’s $5 Souplantation $10 Din-Tai Fung House $10 Staples $25 Domino’s Pizza $5 Starbucks $10 Eddie Bauer $25 $25 El Torito $25 TGI Fridays $20 Gap/Old Navy/Banana $25 Tony’s Pizza $5 Rep Home Depot $25 Wendy’s $10 Honey Baked Ham $10 Whole Foods $50 Hong Kong Market $20 Williams Sonoma $25 Howies $20 Zono Sushi $10 How’s $10 $25 Islands Restaurant $25 iTunes $15 TOTAL: You can place your order in the following ways: 1. -

Ras Announces Finalists for Ras Epicurean Star Award

MEDIA ADVISORY FOR IMMEDIATE RELEASE RAS ANNOUNCES FINALISTS FOR RAS EPICUREAN STAR AWARD 2015 An all-time high of 21 awards to be presented at the RAS Epicurean Star Award Gala Dinner on 18 November 2015 Singapore, 30 September 2015 – Conceptualised in 2006 as RAS Industry Night, the RAS Epicurean Star Award honours F&B establishments that have tabled unique concepts, inspired culinary innovation, and consistently rendered top-notch food and service. The 10th instalment of the annual awards ceremony to be held on 18 November 2015 will see awards doled out in 18 categories – the most ever – such as Best New F&B Establishment, Best Buffet Caterer and Best Gastro-Pub; in addition, three outstanding restaurants will also receive Best of the Best laurels, a category that is not open for nominations. The Epicurean Star Award is not just a hallmark achievement for finalists; it is also an encouragement from RAS to spur them on in a continual effort to improve the quality of the local F&B scene for discerning diners. WHAT’S NEW THIS YEAR While Chinese, Western and Asian Restaurant nominees were previously divided into just two sub- categories; ‘Fine Dining’ and ‘Casual Dining’, a third sub-category ‘Chain’ has been introduced this year. The Best Cafe category also sees a new split to distinguish the ‘Local Traditional’ outfits. Making its inaugural debut is the Best Ice Cream Parlour category, which sees home-grown darlings Udders Ice Cream and Tom’s Palette scoring nominations. Other notable first-timers among this year’s finalists include Bread Street Kitchen, Gordon Ramsay’s pioneer foray into Singapore, and The Carvery, a meat-centric all-you-can-eat concept at Park Hotel Alexandra; both will be competing against five others to clinch the title of Best New F&B Establishment. -

Store Operating List.Xlsx

Stores' Operating Hours During FMCO Floor Lot No. Trade Name Opening Hours P2-K01 Mail Boxes Etc. 10am - 8pm Basement P1-K02,3&4 myNEWS.com 10am - 7pm P1-K05&6 Pressto 10am - 7pm LG-231A AK Noodle House 10am - 8pm LG-203B An Viet 10.30am - 8pm LG-243B Bananabro 10am - 8pm LG-225 Barcook 10am - 7pm LG-221 Boat Noodle 10am - 8pm LG-212 Bread Story 10am - 8pm LG-C3B Brownies Bar By The Accidental Bakers 10am - 7pm LG-202&203A Canton-i 10am - 8pm LG-C2&C3A Childhood 10.45am - 8pm LG-K25B Delectable Treats 11am - 8pm LG-207&208 Din Tai Fung 8am - 8pm LG-K08A Eggette Lab 10am - 8pm LG-K23 Gong Cha 10am - 8pm LG-220 Healthlane Family Pharmacy 10am - 8pm LG-K13A Homi Curry Puff 9am - 8pm LG-K16 I Love YOO! 10am - 8pm LG-K21&22 Inside Scoop 10am - 8pm LG-K27 Isaac Toast & Coffee 10am - 8pm LG-237A Jadeline Exchange 10am - 7pm LG-229 Jaya Grocer 9:30am - 8pm LG-241A Jinjja Chicken 10am - 8pm Lower LG-245 Just Life 10am - 5pm Ground LG-226 Kakiyuki 10am - 8pm LG-232B&C KGB 10am - 8pm LG-236A&B Ko Hyang 10am - 8pm LG-211 KOI The 12pm - 8pm LG-217 KyoChon 1991 10am - 8pm LG-K19 llao llao 10am - 8pm LG-K27 Isaac Toast & Coffee x PIN Tea 11am - 6pm LG-K01 Lucky Mala Noodle 11am - 8pm LG-218 MBG Fruitshop 10am - 8pm LG-201A&B Mitsuyado Seimen 11am - 8pm LG-243A Mr Tuk Tuk 10am - 8pm LG-238 myNEWS.com 10am - 8pm LG-230A Nyonya Colours 9am - 8pm LG-215 Oloiya 11am - 7pm LG-235 Oyster King 10am - 8pm LG-K25A Royce 10am - 8pm LG-239 San Francisco Coffee 10am - 8pm LG-K17 Shihlin 10am - 8pm LG-232A Simple Life 10am -8pm LG-K28 Soyya 10am - 8pm LG-227 Subway 10am - 8pm Disclaimer: Accurate at the time of listing and subject to changes by tenants. -

Warta Kerajaan Warta Kerajaan

M A L A Y S I A Warta Kerajaan S E R I P A D U K A B A G I N D A DITERBITKAN DENGAN KUASA HIS MAJESTY’S GOVERNMENT GAZETTE PUBLISHED BY AUTHORITY Jil. 56 TAMBAHAN No. 25 6hb Disember 2012 TMA No. 47 No. TMA 79. AKta CAP DAGANGAN 1976 (Akta 175) PENGIKLanan PERMOHOnan UntUK MEndaFtaRKan CAP DAGANGAN Menurut seksyen 27 Akta Cap Dagangan 1976, permohonan-permohonan untuk mendaftarkan cap dagangan yang berikut telah disetujuterima dan adalah dengan ini diiklankan. Jika sesuatu permohonan untuk mendaftarkan disetuju terima dengan tertakluk kepada apa-apa syarat, pindaan, ubahsuaian atau batasan, syarat, pindaan, ubahsuaian atau batasan tersebut hendaklah dinyatakan dalam iklan. Jika sesuatu permohonan untuk mendaftarkan di bawah perenggan 10(1)(e) Akta diiklankan sebelum penyetujuterimaan menurut subseksyen 27(2) Akta itu, perkataan-perkataan “Permohonan di bawah perenggan 10(1)(e) yang diiklankan sebelum penyetujuterimaan menurut subseksyen 27(2)” hendaklah dinyatakan dalam iklan itu. Jika keizinan bertulis kepada pendaftaran yang dicadangkan daripada tuanpunya berdaftar cap dagangan yang lain atau daripada pemohon yang lain telah diserahkan, perkataan-perkataan “Dengan Keizinan” hendaklah dinyatakan dalam iklan, menurut peraturan 33(3). WARTA KERAJAAN PERSEKUTUAN WARTA KERAJAAN PERSEKUTUAN 11924 [6hb Dis. 2012 6hb Dis. 2012] PB Notis bangkangan terhadap sesuatu permohonan untuk mendaftarkan suatu cap dagangan boleh diserahkan, melainkan jika dilanjutkan atas budi bicara Pendaftar, dalam tempoh dua bulan dari tarikh Warta ini, menggunakan Borang CD 7 berserta fi yang ditetapkan. TRADE MARKS ACT 1976 (Act 175) ADVERTISEMENT OF APPLICATION FOR REGISTRATION OF TRADE MARKS Pursuant to section 27 of the Trade Marks Act 1976, the following applications for registration of trade marks have been accepted and are hereby advertised. -

Master Pledge Signers Database.Xlsx

10,031 organisations have signed the Employer' Pledge Updated as of 31 May 2020 Organisation Industry "K" Line (Singapore) Pte Ltd Transportation and Storage "K" Line Pte Ltd Transportation and Storage *Prestiou* S*olution*s* Pte. Ltd. Other Service Activities *Prestiou*S*olution*s*(Starhub Centre) Pte Ltd Other Service Activities *Prestiou*S*olution*s*Rendezvous Gallery Private Limited Other Service Activities *SCAPE Co., Ltd. Health and Social Activities @bsolute Cleaning Pte. Ltd. Administrative and Support Service Activities 01 Studio Private Limited Arts, Entertainment and Recreation 1 Fusion Telecom Pte. Ltd. Wholesale and Retail Trade 1 Play Sports Pte. Ltd. Information and Communications 101 Digital Pte. Ltd. Information and Communications 122 Middle Investment Pte. Ltd. Financial and Insurance Activities 123 Works Arts, Entertainment and Recreation 1238 Information and Communications 138 Pte. Ltd. Transportation and Storage 1588 Le Pte .Ltd. Wholesale and Retail Trade 18 Degrees Celsius Pte. Ltd. Information and Communications 18.COM Electronics Pte Ltd Wholesale and Retail Trade 1CARE Global Pte. Ltd. Other Service Activities 1-Garage Pte. Ltd. Accommodation and Food Service Activities 1-Garden Pte. Ltd. Accommodation and Food Service Activities 1-Net Singapore Pte Ltd Information and Communications 1-Production Pte. Ltd. Accommodation and Food Service Activities 1S Staffing Services Administrative and Support Service Activities 1-Soleil Pte. Ltd. Accommodation and Food Service Activities 1st Goldsmith Pte. Ltd. Manufacturing 20Eleven Pte. Ltd. Professional, Scientific and Technical Activities 21st Century Employment Pte. Ltd. Administrative and Support Service Activities 23 Film Company Pte. Ltd. Information and Communications 24 Owlsgroup Pte. Ltd. Professional, Scientific and Technical Activities 24 Pte. -

Tokyo Retail Guide

TOKYO Cushman & Wakefield Global Cities Retail Guide Cushman & Wakefield | Tokyo | 2019 0 Born of commerce and complexity, Tokyo is the very definition of a metropolis. Twenty-three wards, 39 municipalities, and 13.6 million people join to form Japan’s capital. Include the 3 surrounding prefectures of Kanagawa, Saitama and Chiba, and you have a population base that exceeds 36 million people. Above the city’s busy streets, Japan’s economic engine occupies the office spaces of the seemingly endless metropolitan sprawl. Tokyo is the premier portal to world business in this part of the globe and it is one of the largest cities globally in terms of economic size as it has an estimated GDP of USD 973 billions. Tokyo is also home to 51 Fortune Global 500 companies and over 600 headquarters. Currently, Japan is enjoying the most stable political environment seen since Prime Minister Koizumi was in power. Prime Minister Shinzo Abe and his 3 arrows of aggressive monetary policy, flexible fiscal policy and growth strategy, including structural reform, have helped drive economic growth in the short term and the outlook for the economy under his leadership is positive. These policies and the anticipation of the 2020 Olympic and TOKYO Para-Olympic games are contributing to the record numbers of international tourists and the value of commercial and residential real estate in Japan’s larger OVERVIEW markets. Cushman & Wakefield | Tokyo | 2019 1 TOKYO KEY RETAIL STREETS & AREAS GINZA OMOTESANDO Ginza, comprising Chuo Dori Avenue and Harumi Dori Omotesando offers some of the most awe-inspiring Avenue, is the long established retail leader in Tokyo and flagships and an aesthetically pleasing avenue that makes is globally recognized area as one of the world’s top this trade area comparable to the likes of Champ-Elysees performing and most expensive (rent per sq ft) retail in Paris.