RISING to the FOOD WASTE CHALLENGE © Mercadona © Marks and Spencer’S CONTENTS

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Retail Alliances

EUROPEAN COMMISION DG AGRI WORKSHOP ON RETAIL ALLIANCES Ignacio Larracoechea Manufacturer perspective Brussels, 4 - 5 November, 2019 « FAIRNESS MATTERS » «Running your business in a way that is fair to your competitors, fair to your business partners, and above all fair to consumers» «I believe that companies, and individual business people, have a responsibility to foster trust in the markets – trust in a system that works for all - by playing by the rules when they do business in the EU» 2 Commissioner Vestager speech at Copenhagen Business School 3 September 2018 Why Fairness matters, International Commerce Review, 7(2):92-102, December 2007, Ludo Van Der Heyden, INSEAD OVERVIEW 1. Imbalances in Power between Retailers and Suppliers in the Food Supply Chain 2. Retail Alliances – Who are they? How do they operate? 3. Disruption of the food supply chain ? 4. Conclusions CONFIDENTIAL 3 RETAILERS - GATEKEEPERS TO CONSUMERS EU CONSUMERS Retailers represent 20% of suppliers’ Business whilst 17/8 RETAILERS/ suppliers represent less GROUPS than 2% (or even 1%) of Retailers´ business INDUSTRIAL SUPPLIERS 1.000 FARMS (cerca 1.000.000) CONFIDENTIAL Sources: ESADE, INE y CNMC (Informe 2011) 4 COMPARISON BETWEEN THE 10 LARGEST RETAILERS, INDUSTRIAL SUPPLIERS AND COOPERATIVES ( 2015 - M€) CONFIDENTIAL 5 “Retailers only want talk The Czech Office for the Protection of Competition about price. While the salmon (ÚOHS) issued verdict for leading retailer which RETAILERS - price has increased by 60% in asked more than 200 suppliers to change the basic a year, that the raw material purchase price of their products, otherwise represents 75% of the finished GATEKEEPERS Farmers threatening to delist 30% of their product product, some retailers portfolio” – 21.08.2017 TO 10.8 Million threaten the cooperatives of Wholesalers delisting their products .. -

Company Rankings TIER

2 - 1 - 6 - 5 - 4 - 3 - 2: Figure SUMMARY EXECUTIVE TIER 23 18 18 2012 (68 companies) 6 3 0 23 14 16 10 2 5 2013 (70 companies) Agenda thatontheBusiness No Evidence ofImplementation Evidence butLimited Agenda On theBusiness onImplementation Making Progress beDone to ButWork Established Strategy Business to Integral Leadership 21 19 16 14 3 2014 (80 companies) 7 19 17 27 16 4 2015 (90 companies) 7 Company Rankings Company 18 24 22 22 7 2016 (99 companies) 6 Autogrill ABF Ahold Delhaize Arla Foods BRF Coop Group Casino Albertsons 2 Sisters Food Group Barlilla Cargill (Switzerland) Charoen Pokphand Camst Aldi Nord Danish Crown Co-op (UK) Cranswick Domino’s Pizza Chick-fil-A Aldi Süd Ferrero Greggs Marks & Spencer Group Plc ConAgra Aramark FrieslandCampina McDonald’s Migros E Leclerc Darden Carrefour Groupe Danone Tesco Noble Foods El Cortes Inglés Restaurants Chipotle Hormel Foods Unilever Waitrose Gategroup Dunkin’ Brands Mexican Grill J Sainsbury Groupe Auchan Edeka Zentrale Compass Group JBS Groupe Lactalis Elior Costco Wholesale Kaufland Henan Zhongpin Gruppo Cremonini Dean Foods Metro JD Wetherspoon Gruppo Veronesi Fonterra Mitchells & Butlers Kraft Heinz ICA Gruppen General Mills Nestlé Mercadona Les Mousquetaires Kroger Premier Foods Müller Group Mars Inc Lidl Sodexo Olav Thon New Hope Liuhe Loblaw Subway Gruppen OSI Group Marfrig Sysco Corp Quick Publix Mondelēz Tyson Foods Umoe Gruppen Restaurant Brands Panera Bread Vion Food Group Yonghui International Rewe Group Wm Morrison Superstores SSP Group WH Group Walmart Starbucks Whitbread Wendy’s Target Woolworths Terrena Group (Austrailia) Wesfarmers Yum! Brands New company New atleast1tier Down Up atleast1tier Non-mover 2016 REPORT. -

Euroc Response to Draft Paper on Regulatory Technical Standards

EuroCommerce response to the EBA’s consultation paper on Draft Regulatory Technical Standards on separation of payment card schemes and processing entities under Article 7 (6) of Regulation (EU) 2015/71 EuroCommerce would like to thank the EBA for the opportunity to comment on the consultation paper relating to Draft Regulatory Standards on separation of payment card schemes and processing entities under Article 7 (6) of Regulation (EU) 2015/71. EuroCommerce is the principal European organisation representing the retail and wholesale sector. It embraces national associations in 31 countries and 5.4 million companies, both leading multinational retailers such as Carrefour, Ikea, Metro and Tesco and many small family operations. Retail and wholesale provide a link between producers and 500 million European consumers over a billion times a day. It generates 1 in 7 jobs, providing a varied career for 29 million Europeans, many of them young people. It also supports millions of further jobs throughout the supply chain, from small local suppliers to international businesses. Section 5.2 of the Draft Regulatory Standards asked 4 specific questions before a more generic final question. After consultation with our Members, EuroCommerce would like to submit the following responses to each question in turn. Question 1. Do you agree with the proposals outlined in Section 1 of the draft RTS regarding General provisions? A. EuroCommerce Members agree. Question 2. Do you agree with the proposals outlined in Section 2 of the draft RTS regarding Accounting? A. EuroCommerce Members feel that the Payment Services Provider in the ‘terminal to acquirer’ domain should be excluded from this section. -

Iacarrefoura2000ieng.Pdf

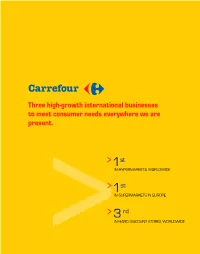

Three high-growth international businesses to meet consumer needs everywhere we are present. > 1st IN HYPERMARKETS WORLDWIDE > 1st IN SUPERMARKETS IN EUROPE > 3 rd >IN HARD DISCOUNT STORES WORLDWIDE MESSAGEMESSAGE FROM THE CHAIRMAN > At the end of January, the European Commission cleared our mer- ger with Promodès. We decided on the rapid consolidation of all our hyper- markets under the Carrefour trade name, and all our supermarkets under a common trade name in each country. > In 87 hypermarkets and 490 supermarkets in France, and 117 hypermarkets and 109 supermarkets in Spain, Italy, Greece, Turkey, Indonesia, China and Korea, the current teams in Continent, Pryca, Continente, Euromercato, Stoc, Maxor and Supeco stores transform- ed those stores and reopened under the Carrefour or Champion name by the end of the year (January in Italy). > This was a major undertaking since the changes involved more than the name of the store or shelf displays. The changes meant train- ing men and women in new working methods and harmonizing product lines. Inevitably, this effort resulted in some disruption, which explains the year-end drop or slowdown in sales revenue in France and Spain. Sometimes custo- mers could not immediately find products in their usual place, sometimes products were not available in the store for short periods due to system changes. In the first half of 2001, all these stores should steadily return to normal operating conditions. > We plan to continue these changes in other countries. In Belgium, 60 hypermarkets will transfer to the Carrefour trade name by the end of 2001. In France and Spain, we will continue to make progress in pooling logistics, creating synergies over the long term. -

Continente Online: Building a Success Story in the Food Retail Business

Continente Online: Building a Success Story in the Food Retail Business Case Author: Winnie Ng Picoto & Rita Fuentes Henriques Online Pub Date: January 02, 2018 | Original Pub. Date: 2018 Subject: Competitive Strategy, E-Commerce Level: Intermediate | Type: Direct case | Length: 6619 words Copyright: © Winnie Ng Picoto and Rita Fuentes Henriques 2018 Organization: Continente Online | Organization size: Large Region: Western Europe | State: Industry: Retail trade, except of motor vehicles and motorcycles Originally Published in: Publisher: SAGE Publications: SAGE Business Cases Originals DOI: http://dx.doi.org/10.4135/9781526440570 | Online ISBN: 9781526440570 SAGE SAGE Business Cases © Winnie Ng Picoto and Rita Fuentes Henriques 2018 © Winnie Ng Picoto and Rita Fuentes Henriques 2018 This case was prepared for inclusion in SAGE Business Cases primarily as a basis for classroom discussion or self-study, and is not meant to illustrate either effective or ineffective management styles. Nothing herein shall be deemed to be an endorsement of any kind. This case is for scholarly, educational, or personal use only within your university, and cannot be forwarded outside the university or used for other commercial purposes. 2020 SAGE Publications Ltd. All Rights Reserved. This content may only be distributed for use within CQ PRESS. http://dx.doi.org/10.4135/9781526440570 Continente Online: Building a Success Story in the Food Retail Business Page 2 of 18 SAGE SAGE Business Cases © Winnie Ng Picoto and Rita Fuentes Henriques 2018 Abstract The online marketplace has grown exponentially during the last decade and today most click- and-mortar businesses have developed Internet sales channels. The online food industry, and more specifically groceries, presents a huge challenge for managing operations online. -

Report on the Relations Between Manufacturers and Retailers in the Food Sector Report on the Relations Between Manufacturers and Retailers in the Food Sector

Report on the relations between manufacturers and retailers in the food sector Report on the relations between manufacturers and retailers in the food sector Contents Report on the relations between manufacturers and retailers in the food sector Executive summary 4 1. Introduction 10 2. Grocery retailing in Spain 14 2.1. Concentration in grocery retailing 17 2.2. Retailing formats 28 2.3. Retailer own brands 34 2.4. The bargaining power of retailers 56 3. Commercial practices in retailing 76 3.1. Context 77 3.2. Analysis of commercial practices not based on prices 78 3.3. Competition risks posed by each of the practices identified 84 3.4. Iniciatives in other countries 114 4. Regulatory barriers in conditions for opening setting up and operating retail outlets 118 4.1. Analysis of the barriers of Department Sotores (DSs) 120 4.2. Effects of the barriers 127 5. Conclusions 130 6. Recommendations 138 Bibliography 142 Annex 1. Regional retail regulations 146 Index of graphs and tables 158 4 Comisión Nacional de la Competencia Executive summary Report on the relations between manufacturers and retailers in the food sector 5 Retail distribution is the final link between manufacturers and consumers. Retailers perform an essential function for consumers. For one, they select, stock and store the goods produced. And second, they facilitate purchasing decisions by providing information on the goods sold. As in other countries, food retailing in Spain has undergone a sweeping change in recent decades, which has been mainly characterised by the pre- vious model based on the traditional commercial format being replaced by another one in which large-scale retailers have firmly established themselves and supermarkets and hypermarkets have achieved a clear predominance. -

Continente Online: Starting a One to One Marketing Program

CONTINENTE ONLINE: STARTING A ONE TO ONE MARKETING PROGRAM Joana Filipa Castro de Amorim Project submitted as partial requirement for the conferral of Master of Science in Business Administration Supervisor: Professor Eduardo Baptista Correia, Assistant Professor, ISCTE Business School Marketing, Operations and General Management Department Co-supervisor: Sara Bettencourt Teixeira, Customer Management, Continente Online - Sonae MC April 2013 To my Parents, Thank you for everything. Starting a One to One Marketing Program Acknowledges First of all I must say that this page is not only to thanks to all the people who helped me during the process of writing this thesis, but above all is a thank you to all the people who had an important and crucial role on my academic life. With this thesis I close seventeen years of studies and it seems to me a wonderful opportunity to write an overall acknowledge to everyone who have been by my side all these years. Thank you. Now, and trying being more specific, my first and biggest thank you is to my parents who always provided me all the things I ever needed. Thank you for all the effort you had paying my tuitions, I promise that I will compensate you with some future gifts and with some success (hopefully). Moreover, I must to thank Professor Eduardo Correia. Without his contribution this work would be certainly poorer. Thank you Sara Teixeira for having welcomed me so well in the Continente Online, and for all the help provided. Without it this thesis would not be possible. Thank you Sonae for the opportunity given which in the end made my thesis something much more exciting and challenging. -

Kantar Retail's 2017 Top 50 Global Retailers

Kantar Retail’s 2017 Top 50 Global Retailers (USD) 2017E Sales Sales % Retail Sales Global Home Global Retail 2017E CAGR CAGR Outside Rank^ Retailer/Parent Company Country Sales ($MM) Global Stores (‘12-’17E) (‘17E-’22E) Home Market 1 Walmart US $511,366 11,978 2% 3% 27% 2 Amazon.com US $138,020 10 19% 14% 32% 3 Costco US $120,892 744 4% 7% 26% 4 Schwarz Group Germany $116,020 12,417 6% 8% 64% 5 Kroger US $115,404 3,852 5% 4% 0% 6 Carrefour France $102,016 12,764 -2% 2% 61% 7 Aldi Germany $98,433 11,257 5% 7% 69% 8 Home Depot US $97,662 2,284 6% 5% 9% 9 Walgreens Boots Alliance US $97,189 13,884 7% 5% 15% 10 Tesco United Kingdom $89,530 7,082 -3% 3% 26% 11 Seven & I Japan $86,429 35,310 -2% 4% 28% 12 CVS US $80,746 9,790 5% 5% 1% 13 Auchan France $74,149 3,908 1% 5% 67% 14 Ahold Delhaize Netherlands $73,846 6,851 -4% 3% 78% 15 Target US $71,310 1,826 0% 4% 0% 16 Aeon Japan $70,276 13,311 0% 5% 9% 17 Lowe’s US $68,491 2,399 6% 4% 8% 18 Albertsons Companies US $58,925 2,421 74% 3% 0% 19 Casino France $55,488 13,481 -2% 6% 57% 20 Edeka Germany $52,433 12,108 -1% 4% 0% 21 Wesfarmers Australia $48,597 3,950 0% 2% 8% 22 JD.com1 China $47,629 N/A 49% 20% 0% 23 Rewe Group Germany $46,870 10,778 -1% 4% 32% 24 IKEA Sweden $46,433 413 5% 10% 95% 25 Leclerc France $44,571 2,983 0% 4% 4% 26 Apple US $44,433 501 10% 9% 12% 27 Metro AG2 Germany $43,119 7,896 -6% 3% 70% 28 Sainsbury’s United Kingdom $42,673 2,311 3% 3% 0% 29 Intermarché France $42,340 3,823 -2% 1% 12% 30 Woolworths Limited (Aus) Australia $42,121 2,990 -5% 3% 14% 31 Best Buy US $38,804 1,557 -3% 2% 11% 32 FamilyMart UNY Japan $34,960 23,522 -6% 3% 8% 33 Publix US $34,700 1,376 5% 5% 0% 34 TJX US $34,503 4,043 6% 5% 22% 35 Loblaw Canada $33,246 2,466 5% 4% 0% 36 H&M Sweden $30,653 4,568 11% 7% 97% 37 A.S. -

List of Participants.Pdf

First Name Last Name Position Organisation Sophie Amoros Public Affairs Intern Carrefour Başak Babaoglu Manager EU Affairs METRO AG François Barry Consultant Cambre Associates Head of Funding Vienna Christian Bartik City of Vienna Business Agency Lithuanian Permanent Representation to Jolita Bociaroviene Internal Market Attache the EU Eric Bos Chair Groningen City Club Julien Bouyeron Policy advisor FCD Annemiek Brontsema Policy officer City of Groningen Ilya Bruggeman Adviser, Single Market EuroCommerce Maurits Bruggink Secretary-General EMOTA Real Estate & Hans-Joachim Bruschke IKEA Retail Germany Development Manager Nele Bzdega Deputy Property Manager IKEA Retail Germany Permanent Representation of the Rinalds Celmiņš Counsellor Republic of Latvia to the European Union European Affairs Delphine Chilese-Lemarinier Edenred Delegate Senior Policy and Legal Francesco Cisternino Confcommercio Advisor Barbara Dallinger Policy Advisor WKÖ Job de Visser Trainee European Retail Round Table Director, Competitiveness Christel Delberghe EuroCommerce & Commercial Relations Jan Delfosse Director General Comeos Femke den Hartog Advisor INretail European Public Affairs Guillaume Dumoulin Carrefour Manager Pieter Faber Head of EU Office Cities Northern Netherlands Géraldine Fages Senior Expert DG GROWTH Veronica Favalli Policy Advisor Confcommercio-Imprese per l'Italia Johannes Ferber Property Manager IKEA Retail Germany Christian Gieseke Attorney Lenz-Johlen Andy Godfrey Public Policy Manager Wallgreen Boots Alliance Mathilde Godichaud Consultant -

1 IS WALMART GOOD for AMERICA? Approved

Is Walmart Good for America? 1 IS WALMART GOOD FOR AMERICA? Approved: ___________________________ Date: _____________________ Is Walmart Good for America? 2 IS WALMART GOOD FOR AMERICA? A Seminar Paper Presented to The Graduate Faculty University of Wisconsin-Platteville In Partial Fulfillment Of the Requirement for the Degree Master of Science in Integrated Supply Chain Management By Rana Nazzal 2013 Acknowledgments Is Walmart Good for America? 3 I would like to thank all of whom supported me in my journey to ultimately complete my Master’s program and Supply Chain research project. Thanks to members of the University of Wisconsin at Platteville for their guidance, quality teaching and constant supervision in completing the Master’s requirements and developing my final research project. Also, special thanks and gratitude to my family members who supported me every step of the way over the past two years to get to where I am today. Finally, deep appreciation to Professor Wendy Brooke for the support and exceptional guidance and learning experience during the course of my research project. Table of Contents Subject Pages Abstract 5 Is Walmart Good for America? 4 A Glimpse at WMT History 5 Table (1) Walmart Growth by Decade 6 Figure (1) Walmart Quarterly Earnings Since 2005 7 Table (2) Comparison of Retailers Sales in 2006 7 People Make the Difference 8 Supply Chain Management 8 The Merchandising Strategy 8 Technology – the Ultimate Change Agent 9 POS, UPC and EDI 9 Radio Frequency Identification (RFID) 10 Retail Link Data Base 12 Figure -

Lojas Continente Aderentes

Listagem de lojas Continente com garrafas de gás Galp LOJAS MORADA CONTINENTE AMADORA Estrada Nacional, 249-1, Venteira, 2724-510 Amadora CONTINENTE ARRÁBIDA Avenida dos Escultores, 199, Canidelo, 4404-504 Vila Nova de Gaia CONTINENTE AVEIRO Estrada Taboeira, Quinta Simão Sul, Esgueira, 3800 Aveiro CONTINENTE BARREIRO Rua Cândido de Oliveira e Rua D. João I - Verderena - 2830 Barreiro CONTINENTE BEJA Rua Zeca Afonso, 7800-522 Beja CONTINENTE BRAGA Avenida Robert Smith - Fraião, 4710-249 Braga CONTINENTE BRAGA NOVA ARCADA Avenida do Cávado 134, 4700-084 Braga CONTINENTE CASCAIS Estrada Nacional, 9, 2645-543 Alcabideche CONTINENTE COIMBRASHOPPING Avenida Dr. Mendes da Silva, 211-251, Sta. António dos Olivais, 3030-153 Coimbra CONTINENTE COLOMBO Avenida Lusíada, Centro Comercial Colombo, 1500-392 Lisboa CONTINENTE COVILHÃ Serra Shopping , Quinta do Pinheiro, 6200 Covilhã CONTINENTE ÉVORA Quinta do Moniz - Zona Industrial - Freguesia da Sé - 7000-172 Évora CONTINENTE GAIASHOPPING Rua Particular de Santo António, Santa Marinha, 4404-501 Vila Nova de Gaia CONTINENTE GUIMARÃES Alameda Dr. Mariano Felgueiras, Creixomil, 4835-075 Guimarães CONTINENTE LEIRIA Estrada Nacional 1, Alto do Vieiro , 2403-002 Leiria CONTINENTE LOULÉ Vale das Râs, São Clemente, 8100-616 Loulé CONTINENTE MAFRA Quinta da Bacoreira, Freguesia de Mafra, 2640 Mafra CONTACTOSCONTINENTE MAIA JARDIM Rua Agostinho da Silva Rocha, S/N - Nogueira - 4475-451 Maia CONTINENTE CONTINENTE MAIA SHOPPING Lugar de Ardegães, Apartado 1009, Águas Santas CONTINENTE MATOSINHOS Rua João Mendonça, 505, 4464-503 Senhora da Hora CONTINENTE MONTIJO Zona Industrial Pau Queimado, Rua da Azinheira - Afonsoeiro, 2870-500 Montijo CONTINENTE OVAR Sportsfórum- Centro Comercial, Av. D. Manuel I - Zona Ind. de Ovar, 3880-109 Ovar CONTINENTE PORTIMÃO 2 Rua das Papoilas Cabeço do Mocho, 8500-313 Potimão CONTINENTE S.J. -

International Retail Marketing Dedication

International Retail Marketing Dedication Michael, Sarah and Matthew Carter To Mrs Moore – thanks for fish suppers To Chloe International Retail Marketing A Case Study Approach Edited by Margaret Bruce, Christopher M. Moore and Grete Birtwistle AMSTERDAM BOSTON HEIDELBERG LONDON NEW YORK OXFORD PARIS SAN DIEGO SAN FRANCISCO SINGAPORE SYDNEY TOKYO Elsevier Butterworth-Heinemann Linacre House, Jordan Hill, Oxford OX2 8DP 200 Wheeler Road, Burlington, MA 01803 First published 2004 Copyright © 2004, Elsevier Ltd. All rights reserved No part of this publication may be reproduced in any material form (including photocopying or storing in any medium by electronic means and whether or not transiently or incidentally to some other use of this publication) without the written permission of the copyright holder except in accordance with the provisions of the Copyright, Designs and Patents Act 1988 or under the terms of a licence issued by the Copyright Licensing Agency Ltd, 90 Tottenham Court Road, London, England W1T 4LP. Applications for the copyright holder’s written permission to reproduce any part of this publication should be addressed to the publisher Permissions may be sought directly from Elsevier’s Science & Technology Rights Department in Oxford, UK: phone: (ϩ44) 1865 843830, fax: (ϩ44) 1865 853333, e-mail: [email protected]. You may also complete your request on-line via the Elsevier homepage (http://www.elsevier.com), by selecting ‘Customer Support’ and then ‘Obtaining Permissions’ British Library Cataloguing in Publication Data A catalogue record for this book is available from the British Library Library of Congress Cataloguing in Publication Data A catalogue record for this book is available from the Library of Congress ISBN 0 7506 5748 0 For information on all Elsevier Butterworth-Heinemann publications visit our web site at http://books.elsevier.com Typeset by Charon Tec Pvt.