Supplement to Objection of Interested Party Independent Insurance Group, LLC, Together with the Affidavit of Edward W

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Neuberger Berman/New Jersey Custom Investment Fund II (“NB/NJ Custom Fund II”)

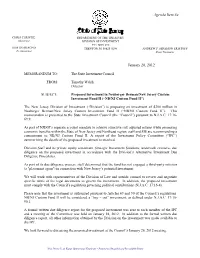

Agenda Item 5a CHRIS CHRISTIE DEPARTMENT OF THE TREASURY Governor DIVISION OF INVESTMENT P.O. BOX 290 KIM GUADAGNO TRENTON, NJ 08625-0290 ANDREW P. SIDAMON-ERISTOFF Lt. Governor State Treasurer January 20, 2012 MEMORANDUM TO: The State Investment Council FROM: Timothy Walsh Director SUBJECT: Proposed Investment in Neuberger Berman/New Jersey Custom Investment Fund II (“NB/NJ Custom Fund II”) The New Jersey Division of Investment (“Division”) is proposing an investment of $200 million in Neuberger Berman/New Jersey Custom Investment Fund II (“NB/NJ Custom Fund II”). This memorandum is presented to the State Investment Council (the “Council”) pursuant to N.J.A.C. 17:16- 69.9. As part of NJDOI’s separate account mandate to achieve attractive risk adjusted returns while promoting economic benefits within the State of New Jersey and Northeast region, staff and SIS are recommending a commitment to NB/NJ Custom Fund II. A report of the Investment Policy Committee (“IPC”) summarizing the details of the proposed investment is attached. Division Staff and its private equity consultant, Strategic Investment Solutions, undertook extensive due diligence on the proposed investment in accordance with the Division’s Alternative Investment Due Diligence Procedures. As part of its due diligence process, staff determined that the fund has not engaged a third-party solicitor (a "placement agent") in connection with New Jersey’s potential investment. We will work with representatives of the Division of Law and outside counsel to review and negotiate specific terms of the legal documents to govern the investment. In addition, the proposed investment must comply with the Council’s regulation governing political contributions (N.J.A.C. -

Objection to Plan of Rehabilitation by Interested Party Independent Insurance Group, with a Certificate of Service Attached Thereto

' ;; Douglas J, Austin Thaddeus E. Morgan Jared A. Roberts Retired FraserTrebilcocK Michael E. ·Cavanaugh Brian P. Morley David J. Houston Donald A. Hlnes LAWYERS Darr-ell A. Lindman Jennifer Utter Heston Melisa M. W. Mysliwiec John J. loose Gary C. Rogers Marlalne C. Teahan Shaina A. Reed Michael H. Perry Mark E. Kellogg Archie C. Fraser Thomas J. Waters Ryan K. Kauffman (1902-1998) 124 West Allegan Street, Suite 1000 Miohael 8. Ashton Paula J. Manderlield Of COUNSEL Everett A. Trebilcock {1918-2002) H. Kirby Albright Paul V. McCord David S. Marvin Lansing, Michigan 48933 E. James A. Davis T (517) 482-5800 F (517} 482-0887 Graham K. Crabtree Brian T. Gallagher Stephen L. Burlingame {1918-2005} www.fraserlawfirm.com Michael P. Donnelly Jonathan T. Walton, Jr. Mark A. Bush Ronald R. Pentecost Edward J. Castellani Laura S. Faussi0 Brandon W. Zuk (1932·2008} Mark R. Fox Jonathan E. Raven Norbert T. Madison, Jr. Davids. Fry (1953·2011) Peter D. Houk Aaron L. Davis Thomas L. Sparks Elizabeth H. Latchana Paul C. Mallon, Jr. Max A. Hoffman Peter L. Dunlap, P.C. [email protected] (517) 377-0816 October 4, 2019 VIA HAND DELIVERY Clerk of the Court Ingham County Circuit Court 313 W. Kalamazoo Street Lansing, MI 48901 Re: Fox v Pavonia Life Insurance Company of Michigan Case No. 19-504-CR Dear Clerk: Enclosed for filing please find the original and "Judge's copy" of the Objection to Plan of Rehabilitation by Interested Party Independent Insurance Group, with a Certificate of Service attached thereto. Thank you for your assistance. -

20191003-NT-A1-EPA Grant Saves Small Business

We appreciate Brenda Hartley and all of our readers. SPORTS Fun at CCC&TI’s Fan Fest Page B1 PROUD TO BE CALDWELL COUNTY’S LOCAL NEWS SOURCE SINCE 1875 THURSDAY, OCTOBER 3, 2019 WWW.NEWSTOPICNEWS.COM $1.25 EPA grant saves small business BY VIRGINIA ANNABLE for an affordable price and N.C. Department of Envi- “(The property) was a VANNABLENEWSTOPICNEWS.COM finally had a place to call ronmental Quality. They good deal, but we didn’t Douglas Guerra saved his own. said he had to clean up the know what we were get- his money for over a “We always wanted to property by removing two ting in to,” Guerra said. “I decade. have our own building,” leftover underground gaso- was really worried about it Year by year while build- Guerra said. “I used to rent line tanks, which would cost ing Douglas Custom Paint- all the time, but I think ... tens of thousands of dollars. SEE GRANT/PAGE A5 ing, he stashed his savings, (owning) is a good oppor- waiting until he could buy tunity for my business to his own building for his grow.” Douglas Guerra, owner of Douglas Sutom Painting, business. Then the bottom fell bought the former Jo Ja’s gas station on U.S. 321-A Early this year, the time out. this year only to nd out it had old gas tanks that came. He bought the old Two months after the had to be removed — a costly process. Jo Ja’s gas station on U.S. deal closed, Guerra start- 321-A just north of Hudson ed getting letters from the VIRGINIA ANNABLE | NEWS-TOPIC Sheri ’s o c e , school to honor students BY KARA FOHNER KFOHNERNEWSTOPICNEWS.COM The Caldwell County Sher- iff’s Offi ce has partnered with Gamewell Elementary School to honor one fifth grade stu- dent each month for their per- formance. -

2011 Conference Program

Tuesday, August 9, 2011 (as of Wednesday, June 29, 2011) 8 am to 5 pm / 001 Advertising Division Advertising Teaching Workshop Session: Strategic Solutions at the Intersection of Content and Channel Moderating/Presiding: Peggy Kreshel, Georgia Karie Hollerbach, Southeast Missouri State Featured Panelist: Media: From Chaos to Clarity. Making Sense of a Messy Media World Judy Franks, founder & president, The Marketing Democracy, Chicago, IL Peer Presentations: The Media Class: Changing Channels Amy Falkner, Syracuse Michelle Nelson, Illinois The Campaigns Class: You’ve Arrived Karie Hollerbach, Southeast Missouri State Heidi Hennink-Kaminski, North Carolina at Chapel Hill Teri Henley, Alabama 8:30 am to 2:30 pm / 002 Association for Education in Journalism and Mass Communication Business Meeting: Board of Directors Meeting Moderating/Presiding: Jan Slater, Illinois, 2010-2011 AEJMC President 9 am to Noon / 003 International Communication and Law and Policy Divisions Panel Sessions: Freedom of Information Around the World Panel I: Freedom of Information as a Human Right 9 a.m. to 9:50 a.m. Moderating/Presiding: Charles Davis, Missouri Panelists: Cheryl Ann Bishop, Quinnipiac Tuesday, August 9, 2011 2011 AEJMC Conference Program Copy 1 Jane Kirtley, Minnesota Gregory Magarian, Washington University in St. Louis Panel II: Comparative/Foreign Law Approach to Freedom of Information 10 a.m. to 10:50 a.m. Moderating/Presiding: Jeannine Relly, Arizona Panelists: Europe and Eurasia Jane Kirtley, Minnesota India Nikhil Moro, North Texas India and Singapore Sundeep Muppidi, Asian Media Information & Communication Center Nigeria and the African continent Fassy Yusuf, Lagos Panel III: The Diffusion of Freedom of Information Legislation in Latin America 11 a.m. -

Capital Markets

U.S. DEPARTMENT OF THE TREASURY A Financial System That Creates Economic Opportunities Capital Markets OCTOBER 2017 U.S. DEPARTMENT OF THE TREASURY A Financial System That Creates Economic Opportunities Capital Markets Report to President Donald J. Trump Executive Order 13772 on Core Principles for Regulating the United States Financial System Steven T. Mnuchin Secretary Craig S. Phillips Counselor to the Secretary Staff Acknowledgments Secretary Mnuchin and Counselor Phillips would like to thank Treasury staff members for their contributions to this report. The staff’s work on the report was led by Brian Smith and Amyn Moolji, and included contributions from Chloe Cabot, John Dolan, Rebekah Goshorn, Alexander Jackson, W. Moses Kim, John McGrail, Mark Nelson, Peter Nickoloff, Bill Pelton, Fred Pietrangeli, Frank Ragusa, Jessica Renier, Lori Santamorena, Christopher Siderys, James Sonne, Nicholas Steele, Mark Uyeda, and Darren Vieira. iii A Financial System That Creates Economic Opportunities • Capital Markets Table of Contents Executive Summary 1 Introduction 3 Scope of This Report 3 Review of the Process for This Report 4 The U.S. Capital Markets 4 Summary of Issues and Recommendations 6 Capital Markets Overview 11 Introduction 13 Key Asset Classes 13 Key Regulators 18 Access to Capital 19 Overview and Regulatory Landscape 21 Issues and Recommendations 25 Equity Market Structure 47 Overview and Regulatory Landscape 49 Issues and Recommendations 59 The Treasury Market 69 Overview and Regulatory Landscape 71 Issues and Recommendations 79 -

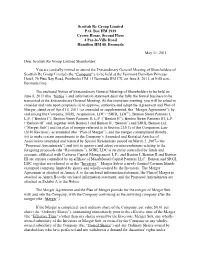

SRGL 2011 Information Statement

Scottish Re Group Limited P.O. Box HM 2939 Crown House, Second Floor 4 Par-la-Ville Road Hamilton HM 08, Bermuda May 11, 2011 Dear Scottish Re Group Limited Shareholder: You are cordially invited to attend the Extraordinary General Meeting of Shareholders of Scottish Re Group Limited (the “Company”), to be held at the Fairmont Hamilton Princess Hotel, 76 Pitts Bay Road, Pembroke HM 11 Bermuda HM CX, on June 8, 2011, at 9:00 a.m., Bermuda time. The enclosed Notice of Extraordinary General Meeting of Shareholders to be held on June 8, 2011 (the “Notice”) and information statement describe fully the formal business to be transacted at the Extraordinary General Meeting. At this important meeting, you will be asked to consider and vote upon proposals (i) to approve, authorize and adopt the Agreement and Plan of Merger, dated as of April 15, 2011 (as amended or supplemented, the “Merger Agreement”), by and among the Company, SGRL Acquisition, LDC (“SRGL LDC”), Benton Street Partners I, L.P. (“Benton I”), Benton Street Partners II, L.P. (“Benton II”), Benton Street Partners III, L.P. (“Benton III” and, together with Benton I and Benton II, “Benton”) and SRGL Benton Ltd. (“Merger Sub”) and the plan of merger referred to in Section 233(3) of the Companies Law (2010 Revision), as amended (the “Plan of Merger”), and the merger contemplated thereby, (ii) to make certain amendments to the Company’s Amended and Restated Articles of Association (amended and restated by Special Resolutions passed on March 2, 2007) (the “Proposed Amendments”) and (iii) to approve and adopt certain resolutions relating to the foregoing proposals (the “Resolutions”). -

John Bussian RALEIGH, NC 27601

Ongoing coverage of N.C. General Assembly ONLINE and health care, reforming state ABC FOR DAILY UPDATES VISIT CAROLINAJOURNAL.COM AN AWARD-WINNING JOURNAL OF NEWS, ANALYSIS, AND OPINION FROM THE JOHN LOCKE FOUNDATION CAROLINAJOURNAL.COM VOL. 28 • NO. 5 • MAY 2019 • STATEWIDE EDITION A PUBLIC DECISION SCHOOL CHOICE HAS A LONG HISTORY IN NORTH CAROLINA LINDSAY MARCHELLO ASSOCIATE EDITOR aleigh Charter High School is one of the top schools in the country, but it’s not what one would call a typical public school. RThe school doesn’t have a caf- eteria or an auditorium. Students don’t have a gym or sports facilities, though students can still participate in athletic activities at a neighbor- ing park. The school building itself on Glenwood Avenue is fairly dat- ed; it certainly isn’t what someone would call a 21st-century, state-of- the-art facility. Yet despite all real or perceived — or esthetic — shortcomings, stu- dents at Raleigh Charter are per- forming better than most students in the state. Supporters of school choice say it’s that choice that empowers par- ents to pick the best place for their children to attend school. Critics ar- gue school-choice programs, like charter schools, siphon money and resources from traditional public schools. The Republican Party enjoyed a veto-proof supermajority in the General Assembly for years, and CJ PHOTO BY DON CARRINGTON DON BY PHOTO CJ SCHOOL CHOICE IN N.C. Lisa Huddleston, principal at Raleigh Charter High School, which ranks among the best high schools in the state and nation. continued PAGE 10 CAROLINA JOURNAL Interview: 200 W. -

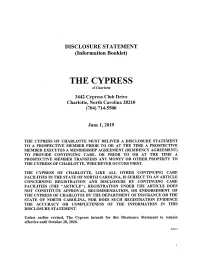

The-Cypress-Of-Charlotte-2019 0.Pdf

DISCLOSURE STATEMENT (Information Booklet) THE CYPRESS of Charlotte 3442 Cypress Club Drive Charlotte, North Carolina 28210 (704) 714-5500 June 1, 2019 THE CYPRESS OF CHARLOTTE MUST DELIVER A DISCLOSURE STATEMENT TO A PROSPECTIVE MEMBER PRIOR TO OR AT THE TIME A PROSPECTIVE MEMBER EXECUTES A MEMBERSHIP AGREEMENT (RESIDENCY AGREEMENT) TO PROVIDE CONTINUING CARE, OR PRIOR TO OR AT THE TIME A PROSPECTIVE MEMBER TRANSFERS ANY MONEY OR OTHER PROPERTY TO THE CYPRESS OF CHARLOTTE, WHICHEVER OCCURS FIRST. THE CYPRESS OF CHARLOTTE, LIKE ALL OTHER CONTINUING CARE FACILITIES IN THE STATE OF NORTH CAROLINA, IS SUBJECT TO AN ARTICLE CONCERNING REGISTRATION AND DISCLOSURE BY CONTINUING CARE FACILITIES (THE "ARTICLE"). REGISTRATION UNDER THE ARTICLE DOES NOT CONSTITUTE APPROVAL, RECOMMENDATION, OR ENDORSEMENT OF THE CYPRESS OF CHARLOTTE BY THE DEPARTMENT OF INSURANCE OR THE STATE OF NORTH CAROLINA, NOR DOES SUCH REGISTRATION EVIDENCE THE ACCURACY OR COMPLETENESS OF THE INFORMATION IN THIS DISCLOSURE STATEMENT. Unless earlier revised, The Cypress intends for this Disclosure Statement to remain effective until October 28, 2020. 816211 TABLE OF CONTENTS Page Introduction .................................................................................................................... 4 I. THE PEOPLE Overview ............................................................................................................ 5 The Cypress Group, LLC ................................................................................... 5 The Cypress of Charlotte, -

The Rise of Private Equity Media Ownership in the United States: a Public Interest Perspective

City University of New York (CUNY) CUNY Academic Works Publications and Research Queens College 2009 The Rise of Private Equity Media Ownership in the United States: A Public Interest Perspective Matthew Crain CUNY Queens College How does access to this work benefit ou?y Let us know! More information about this work at: https://academicworks.cuny.edu/qc_pubs/171 Discover additional works at: https://academicworks.cuny.edu This work is made publicly available by the City University of New York (CUNY). Contact: [email protected] International Journal of Communication 2 (2009), 208-239 1932-8036/20090208 The Rise of Private Equity Media Ownership in the United States: ▫ A Public Interest Perspective MATTHEW CRAIN University of Illinois, Urbana-Champaign This article examines the logic, scope, and implications of the influx of private equity takeovers in the United States media sector in the last decade. The strategies and aims of private equity firms are explained in the context of the financial landscape that has allowed them to flourish; their aggressive expansion into media ownership is outlined in detail. Particular attention is paid to the public interest concerns raised by private equity media ownership relating to the frenzied nature of the buyout market, profit maximization strategies, and the heavy debt burdens imposed on acquired firms. The article concludes with discussion of the challenges posed by private equity to effective media regulation and comparison of private equity and corporate media ownership models. The media sector in the United States is deeply and historically rooted in the capitalist system of private ownership. The structures and demands of private ownership foundationally influence the management and operation of media firms, which must necessarily serve the ultimate end of profitability within such a system. -

Investment Committee Memorandum NB PA Co-Investment Fund LP

Investment Committee Memorandum NB PA Co-investment Fund LP Private Equity Asset Class February 25, 2020 Page 1 PA SERS Private Equity Investment Recommendation Investment Recommendation SERS’ Investment Office Staff recommend that the State Employees’ Retirement System Investment Committee, subject to further legal due diligence, interview Neuberger Berman Alternative Advisors, LLC (“Neuberger Berman”, “NB” or the “Firm”) at the February 25, 2020 Investment Committee Meeting to consider a potential investment of up to $200 million to a separately managed account named the NB PA Co-investment Fund LP (“the SMA”, or the “Partnership”). SERS has not previously held an investing relationship with Neuberger Berman. As this SMA has been directly negotiated to have a custom investment mandate for SERS, it is a fund of one and the proposed commitment will be the fund size. Furthermore, there is no firm closing schedule, but SERS has agreed to target completing legal due diligence and closing by June 30, 2020 should approval be attained. Investment Rationale Staff identified NB PA Co-investment Fund as a strong candidate for SERS’ capital commitment as it offers: ➢ SMA strategy represents meaningful step forward in achieving funding objectives set out in PPMAIRC report; ➢ Bespoke co-investment solution crafted to satisfy numerous SERS objectives; ➢ Partnership with a top performing co-investment intermediary; ➢ High level of coverage with SERS’ existing core PE managers determined by cross checking Neuberger Berman track record and reference calls with SERS’ PE managers. SERS will benefit from joining with Neuberger Berman’s existing capacity, relationship history and negotiating power; ➢ Extendibility of partnership to other parts of Neuberger Berman’s platform including secondaries and private credit. -

Failing Early & Failing Often by Greg Lindberg

FAILING EARLY FAILING &OFTEN HOW TO TURN YOUR ADVERSITY INTO ADVANTAGE by Greg E. Lindberg Failing Early Failing &Often How To Turn Your Adversity Into Advantage by Greg E. Lindberg Copyright © 2020 by Global Growth, LLC All Rights Reserved. Cover image © AndreaA/depositphotos.com ISBN: 9798694941365 Printed in the United States Published by Global Growth, LLC Global Growth, LLC. Worldwide Headquarters 2222 Sedwick Road, Durham, NC 27713 www.globalgrowth.com ii | Failing Early and Failing Often This book is dedicated to my mother. ACKNOWLEDGEMENTS I would not be here if it weren’t for the kindness and generosity of thousands of people who have encouraged me and coached me along the way, including my parents, teachers, coaches, fellow employees, lawyers, accountants, lenders, friends, family and others too numerous to mention. I hesitate to list anyone here for fear of missing someone. I am sincerely grateful for everyone who has had faith in me. I am also sincerely grateful for the work of those whom I have cited here. I would not be the person I am today if it weren’t for people such as Napoleon Hill, Jim Collins and numerous others. For this book in particular, a special thanks to Carolyn Tetaz, Skip Press, Bridgett Hurley, Jacqui Dawson, Jessica Henry, Amy Maclean, Brenda Lynch and Randy Nelson for their help in writing and publishing this book. Carolyn did the lion’s share of the work and turned the manuscript around in very short order. How to Turn Your Adversity Into Advantage | iii TABLE OF CONTENTS Part One: Start Failing, Keep Failing . -

Falcons Acquisition Corp

FOR IMMEDIATE RELEASE Investor Group to Acquire Financial Guaranty Insurance Company for $2.16 Billion from General Electric Capital Corporation New York, NY, August 4, 2003 -- An investor group consisting of The PMI Group, Inc. (“PMI”), The Blackstone Group (“Blackstone”), The Cypress Group (“Cypress”) and CIVC Partners L.P. (“CIVC”), collectively the “Investor Group,” announced today that it has signed a definitive agreement to acquire Financial Guaranty Insurance Company (“FGIC”) from General Electric Capital Corporation (“GE”) in a transaction valued at approximately $2.16 billion. FGIC is a leading triple-A rated monoline bond insurer with approximately $202 billion of insured par outstanding. FGIC provides financial guaranty policies for public finance and structured finance obligations issued by clients in both the public and private sectors. Financial guaranty insurance policies written by FGIC generally guaranty payment when due of the principal and interest on the guaranteed obligation. On completion of the transaction, FGIC will operate as an independent company. PMI will be the largest shareholder in FGIC with 42% ownership. Blackstone and Cypress will each own 23%. CIVC will own 7% of the new company and GE will maintain approximately a 5% stake. The purchase price will be funded with approximately $1.44 billion of equity, $225 million of senior debt, $235 million of mandatorily convertible participating preferred equity held by GE and a pre- closing dividend of approximately $260 million. In highlighting the growth plan for FGIC, the Investor Group noted that the Company will continue to be a leading participant in its core municipal bond market business and that FGIC’s strong platform will be the base for expansion into markets it does not currently serve, including certain areas of the municipal bond market, the structured finance market, and the international bond markets.