NASCAR 2017 Review – 2018 Preview

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Busch's Battle Ends in Glory

8 – THE DERRICK. / The News-Herald Wednesday, December 09, 2015 QUESTIONS & ATTITUDE Compelling questions... and maybe a few actual answers What will I do for NASCAR news? It’s as close as we get to NASCAR hanging a “Gone fishing” sign on the door. Now what? After 36 races, a goodbye to Jeff Gordon and con- SPEED FREAKS gratulations to Kyle Busch, and with only about A couple questions Mission accomplished two months until the engines crank at Daytona, we had to ask — you need more right now? These days, this is the ourselves closest thing NASCAR has to a dark season. But there’ll be news. What sort of news? Danica Patrick’s NASCAR’s corner-office suits are huddling with newest Busch’s battle the boys in legal to find a feasible way to turn its race teams into something resembling fran- GODSPEAK: Third chises, which would break from the independent- crew chief in contractor system that served the purposes four years. Crew since the late-’40s. Well, it served NASCAR’s ends in glory purposes, along with owners and drivers who chief No. 1, Tony Gibson, took ran fast enough to escape creditors. But times Kurt Busch to the have changed; you’ll soon be reading a lot about men named Rob Kauffman and Brent Dewar and Chase this year. something called the Race Team Alliance. KEN’S CALL: It’s starting to take on Will it affect the race fans and the the feel of a dial- racing? a-date, isn’t it? Nope. So maybe you shouldn’t pay attention. -

Towns County Sports Towns County’S Leader in Sports

Page 11A THE TOWNS COUNTY HERALD August 15, 2012 Towns County Sports Towns County’s Leader In Sports www.townscountyherald.net • E-mail: [email protected] 15, 2012 THE TOWNS COUNTY HERALD Page 11A continued from page 10A Chatuge Shores Blairsville School of Dance to Fly-In... Ladies Golf news offer free Cardio Hip Hop Class Most have a good sense of avid water skiers and the old only to have the desire to try On Aug. 7, the Chatuge camaraderie and look forward knees get a little tender after a and a love of the water to enjoy Shores Ladies Golf Asso- On Thursday, August 16, dance and is excited to begin to sharing their sport. They are day of water-skiing. hydrofoil- this sport. ciation challenged the golf Blairsville School of Dance this program at BSoD. She course's pro, Matt Liss. Now, will offer its Cardio Hip Hop also teaches ballet technique, typically a little older than the ing is very easy on the body. If this sounds like some- of course, there were some diehard water-skiers or wake- Also, the sport is relatively thing you would like to be class for free to kick off its new pointe, lyrical and jazz classes parameters set for this tour- program. The Cardio Hip Hop at BSoD and is a fitness in- boarders and they are usually expensive so you have to be involved in then make plans to nament. Matt played his attend the Ninth Annual event class, which is for teens and structor at Hiwassee Valley open to sharing their boats and able to afford it.” scratch golf game while the adults, will be held on Thurs- Pool and Wellness Center in equipment with other Hydro- The jumps and tricks at the Ridges Resort and ask "Chatugettes" played their net days at 5:30 p.m. -

KEVIN HARVICK: Track Performance History

KEVIN HARVICK: Track Performance History ATLANTA MOTOR SPEEDWAY (1.54-mile oval) Year Event Start Finish Status/Laps Laps Led Earnings 2019 Folds of Honor 500 18 4 Running, 325/325 45 N/A 2018 Folds of Honor 500 3 1 Running, 325/325 181 N/A 2017 Folds of Honor 500 1 9 Running, 325/325 292 N/A 2016 Folds of Honor 500 6 6 Running, 330/330 131 N/A 2015 Folds of Honor 500 2 2 Running, 325/325 116 $284,080 2014 Oral-B USA 500 1 19 Running, 325/325 195 $158,218 2013 AdvoCare 500 30 9 Running, 325/325 0 $162,126 2012 ×AdvoCare 500 24 5 Running, 327/327 101 $172,101 2011 AdvoCare 500 21 7 Running, 325/325 0 $159,361 2010 ×Kobalt Tools 500 35 9 Running, 341/341 0 $127,776 Emory Healthcare 500 29 33 Vibration, 309/325 0 $121,026 2009 ×Kobalt Tools 500 10 4 Running, 330/330 0 $143,728 Pep Boys Auto 500 18 2 Running, 325/325 66 $248,328 2008 Kobalt Tools 500 8 7 Running, 325/325 0 $124,086 Pep Boys Auto 500 6 13 Running, 325/325 0 $144,461 2007 Atlanta 500 36 25 Running, 324/325 1 $117,736 ×Pep Boys Auto 500 34 15 Running, 329/329 1 $140,961 2006 Golden Corral 500 6 39 Running, 313/325 0 $102,876 †Bass Pro Shops 500 2 31 Running, 321/325 9 $123,536 2005 Golden Corral 500 36 21 Running, 324/325 0 $106,826 Bass Pro Shops/MBNA 500 31 22 Running, 323/325 0 $129,186 2004 Golden Corral 500 8 32 Running, 318/325 0 $90,963 Bass Pro Shops/MBNA 500 9 35 Engine, 296/325 0 $101,478 2003 Bass Pro Shops/MBNA 500 I 17 19 Running, 323/325 0 $87,968 Bass Pro Shops/MBNA 500 II 10 20 Running, 324/325 41 $110,753 2002 MBNA America 500 8 39 Running, 254/325 0 $85,218 -

Teen Stabbing Questions Still Unanswered What Motivated 14-Year-Old Boy to Attack Family?

Save $86.25 with coupons in today’s paper Penn State holds The Kirby at 30 off late Honoring the Center’s charge rich history and its to beat Temple impact on the region SPORTS • 1C SPECIAL SECTION Sunday, September 18, 2016 BREAKING NEWS AT TIMESLEADER.COM '365/=[+<</M /88=C6@+83+sǍL Teen stabbing questions still unanswered What motivated 14-year-old boy to attack family? By Bill O’Boyle Sinoracki in the chest, causing Sinoracki’s wife, Bobbi Jo, 36, ,9,9C6/Ľ>37/=6/+./<L-97 his death. and the couple’s 17-year-old Investigators say Hocken- daughter. KINGSTON TWP. — Specu- berry, 14, of 145 S. Lehigh A preliminary hearing lation has been rampant since St. — located adjacent to the for Hockenberry, originally last Sunday when a 14-year-old Sinoracki home — entered 7 scheduled for Sept. 22, has boy entered his neighbors’ Orchard St. and stabbed three been continued at the request house in the middle of the day members of the Sinoracki fam- of his attorney, Frank Nocito. and stabbed three people, kill- According to the office of ing one. ily. Hockenberry is charged Magisterial District Justice Everyone connected to the James Tupper and Kingston case and the general public with homicide, aggravated assault, simple assault, reck- Township Police Chief Michael have been wondering what Moravec, the hearing will be lessly endangering another Photo courtesy of GoFundMe could have motivated the held at 9:30 a.m. Nov. 7 at person and burglary in connec- In this photo taken from the GoFundMe account page set up for the Sinoracki accused, Zachary Hocken- Tupper’s office, 11 Carverton family, David Sinoracki is shown with his wife, Bobbi Jo, and their three children, berry, to walk into a home on tion with the death of David Megan 17; Madison, 14; and David Jr., 11. -

Daniel Suarez

DANIEL SUÁREZ No. 96 T-TEN Toyota Team Report Race 28 of 36 – Federated Auto Parts 400 – Richmond Car No.: 96 – T-TEN Toyota Camry PR Contact: Laz Denes, True Speed Communication (704) 875-3388 ext. 806 or [email protected]) Primary Team Members: Driver: Daniel Suárez Crew Chief: Dave Winston Hometown: Monterrey, Mexico Hometown: Miami, Florida Technical Director: Nick Ollila Car Chief: Mark Hillman Hometown: Warren, Michigan Hometown: Lockport, New York Engine Builder: Toyota Racing Development Engine Specialist: Kirk Butterfield Headquarters: Costa Mesa, California Hometown: Carrollton, Ohio Spotter: Steve Barkdoll Hometown: Garrison, Iowa Over-The-Wall Crew Members: Gas Man: Cory White Front Tire Changer: Jason Charles Hometown: Vinson, Iowa Hometown: Rochester, New York Jackman: Bailey Walker Rear Tire Changer: Brandon Traino Hometown: Myrtle Beach, South Carolina Hometown: Cherry Hill, New Jersey Windshield: Mark Hillman Tire Carrier: Mason Harris Hometown: Lockport, New York Hometown: Fort Oglethorpe, Georgia Richmond Notes of Interest: After piloting the No. 19 NASCAR Cup Series Toyota for Joe Gibbs Racing in 2017 and 2018, then the No. 41 Cup Series entry for Stewart-Haas Racing in 2019, Suárez joined the single-car No. 96 Toyota Camry effort for Gaunt Brothers Racing (GBR) for the full 2020 season. Suárez has made 134 career NASCAR Cup Series starts. He has career totals of eight top-five finishes, 32 top-10s and 261 laps led with an average start of 18.7 and an average finish of 18.8. He also has qualified on the pole twice. In his most recent Cup Series appearance, Sunday night’s Cook Out Southern 500 at Darlington (S.C.) Raceway, Suárez started 28th and finished 25th. -

THREE THINGS to WATCH Larson Said

8 - THE DERRICK. / The News-Herald Wednesday, February 14, 2018 The Daytona Beach News-Journal’s Godwin Kelly & Ken Willis have covered NASCAR for nearly 60 years combined. NASCAR THIS WEEK [email protected] [email protected] SPEED FREAKS QUESTIONS & ATTITUDE A few questions we had to ask ourselves Compelling questions ... and maybe a few actual answers Alex Bowman starts up front for DAYTONA the 500: can he be there at the 16-second pit stops? end? THREE THINGS WE LEARNED GODSPEAK: The slipping and Sure, back in your dad’s day, sliding 500? Sorry, I don’t think they couldn’t get in and out in it will happen. Maybe next year. 16 seconds unless they only KEN’S CALL: Gotta say no. It’s took two tires. But in modern a lot of laps in a lot of traffic NASCAR, 16 seconds would with a lot that can go wrong for feel like a wait at the DMV. But a guy not accustomed to being cutting pit crews from six to there. five members has lengthened the stops and given the teams Does the Clash win make Kesel- plenty to study and test as owski a Daytona 500 favorite? they look to shave time in the GODSPEAK: Yes, just based on pits. the fact his Daytona confidence level is through the roof right Is this a good thing? now. KEN’S CALL: He’s always among Yes! Frankly, four guys would the favorites at Daytona. Now be even better. Do I hear that he’s broken his Speed- three? Anything that adds weeks winless skid, even more to the human element and so. -

Official Report

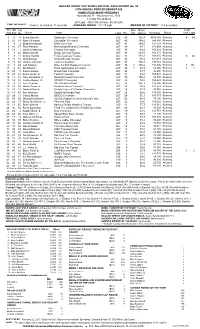

NASCAR SPRINT CUP SERIES OFFICIAL RACE REPORT No. 36 16TH ANNUAL FORD ECOBOOST 400 HOMESTEAD-MIAMI SPEEDWAY Homestead, FL - November 16, 2014 1.5-Mile Paved Oval 267 Laps - 400.5 Miles Purse: $5,382,636 TIME OF RACE: 3 hours, 16 minutes, 31 seconds AVERAGE SPEED: 122.28 mph MARGIN OF VICTORY: 0.5 second(s) Fin Str Car Bns Driver Lead Pos Pos No Driver Team Laps Pts Pts Rating Winnings Status Tms Laps 1 5 4 Kevin Harvick Budweiser Chevrolet 267 43 132.7 $346,498 Running 4 54 2 21 31 Ryan Newman Caterpillar Chevrolet 267 42 108.2 249,850 Running 3 4 2 Brad Keselowski Miller Lite Ford 267 41 104.5 231,758 Running 4 16 27 Paul Menard Richmond/Menards Chevrolet 267 40 87.1 172,664 Running 5 19 1 Jamie McMurray Cessna Chevrolet 267 39 84.9 165,239 Running 6 3 20 Matt Kenseth Dollar General Toyota 267 38 101.5 160,151 Running 7 8 11 Denny Hamlin FedEx Express Toyota 267 37 118.7 108,315 Running 5 50 8 6 15 Clint Bowyer 5-hour Energy Toyota 267 36 97.2 127,481 Running 9 12 48 Jimmie Johnson Lowe's Chevrolet 267 35 105.7 135,001 Running 10 1 24 Jeff Gordon Drive To End Hunger Chevrolet 267 36 2 138.2 148,826 Running 8 161 11 2 41 Kurt Busch Haas Automation Chevrolet 267 34 1 85.8 82,340 Running 1 1 12 23 5 Kasey Kahne Great Clips Chevrolet 267 32 91.7 96,640 Running 13 27 42 Kyle Larson # Target Chevrolet 267 31 88.5 109,085 Running 14 11 88 Dale Earnhardt Jr National Guard Chevrolet 267 30 100.4 88,890 Running 15 14 51 Justin Allgaier # BRANDT Chevrolet 267 29 74.0 108,523 Running 16 9 22 Joey Logano Shell Pennzoil Ford 267 28 105.1 116,356 Running -

Fedex Racing Press Materials 2013 Corporate Overview

FedEx Racing Press Materials 2013 Corporate Overview FedEx Corp. (NYSE: FDX) provides customers and businesses worldwide with a broad portfolio of transportation, e-commerce and business services. With annual revenues of $43 billion, the company offers integrated business applications through operating companies competing collectively and managed collaboratively, under the respected FedEx brand. Consistently ranked among the world’s most admired and trusted employers, FedEx inspires its more than 300,000 team members to remain “absolutely, positively” focused on safety, the highest ethical and professional standards and the needs of their customers and communities. For more information, go to news.fedex.com 2 Table of Contents FedEx Racing Commitment to Community ..................................................... 4-5 Denny Hamlin - Driver, #11 FedEx Toyota Camry Biography ....................................................................... 6-8 Career Highlights ............................................................... 10-12 2012 Season Highlights ............................................................. 13 2012 Season Results ............................................................... 14 2011 Season Highlights ............................................................. 15 2011 Season Results ............................................................... 16 2010 Season Highlights. 17 2010 Season Results ............................................................... 18 2009 Season Highlights ........................................................... -

Newsletter of the Northern California Chapter Oldsmobile Club of America President/Show Chair

The Oldsletter Sept/Oct 2013 Last Call for Micke Grove, Don’t Miss Out On The Fun- Registration Deadline is Aug. 20th. See The Last Oldsletter or Our Club Website For Registration Form Inside This Issue: l National Show Coverage l Micke Grove Show Info l Other Outings & Shows Newsletter of the Northern California Chapter Oldsmobile Club of America President/Show Chair. Ken Van Gundy III (916)Officers 784-3271 and Representatives1818 Woodacre 2013 Way [email protected] Cal Olds Club Website: www.norcalolds.comRoseville, CA 95661 President (acting) Pat Kennedy (916) 655-1588 3061 Amoruso Way [email protected] Roseville, CA 95747 Treasurer/Membership Dan Haggerty (408) 268-7904 6208 Balderstone Dr [email protected] San Jose, CA 95120 Secretary and Health & Welfare Linda Sutherland (209) 833-3413 1460 Velasquez Lane [email protected] Tracy, CA 95377 Newsletter Editor Larry Ewing Technical Librarian 3330 Henriette Ct (408) 528-9770 San Jose, CA 95135 [email protected] Public Relations Mike Barentson 916-435-1340 3136 Strand Road [email protected] Rocklin, CA 95765-4315 Club Historian Bob Griffith (209) 366-2807 2434 Grenoble [email protected] Lodi, CA 95242 Acting Show Car Chair Jon Manji 916-386-1642 2257 Moorbrook Way [email protected] Sacramento, CA 95826 Pacific S.W. Zone Directors Don Joe Varley, 14908 E. Dale Lane Sutherland Scottsdale, AZ 85262 Nor Cal Olds (480) 998-1449 Webmaster [email protected] Jon Manji, 2257 Moorbrook Way (209) 833-3413 Sacramento, CA 95826 [email protected] 916-386-1642 1460 Velasquez Lane [email protected] Tracy, CA 95377 2 President’s Message Hi everyone, The Nationals have come and gone and I am happy to learn that Jon Manji is our new Zone Director. -

ABQ Dragway Nascar History Off Season Moves 2 Nmmotorsportsreport.Com New Mexico May 2016 Volume 1 Issue 1

NEW MEXICO MAY 2016 VOL #1 ISSUE #1 new mexico R E P O R T Report 58TH ANNUAL daYTONA 500 TRICKS OF THE TRADE ABQ DRAGWAY NASCAR HISTORY OFF SEASON MOVES 2 NMMotorsportsReport.com new mexico MAY 2016 VOLUME 1 ISSUE 1 R E P O R T Denny Hamlin wins the 58th Daytona 500 by .010 over Martin Truex. Story by David Swope Publisher RaDine William, LLC Editor Dominic Aragon Design & Layout David Lansa DL Graphic Design NASCAR’s off-season moves. Photographers Story by Dominic Aragon Getty Images Corey Ringo David Swope Editorial Contributors Dominic Aragon Jim Costa Lyle Greenburg David Swope Publication Sponsors ABQ Dragway ABQ Dragway, A Family Affair Car Crafters form the first green light. NAPA Auto Parts Story by Lyle Greenburg Unser Racing Museum Yearwood Performance NM Motorsports Report copyright 2016®. All contents of this magazine are copyrighted by NM Motorsports Report, alls rights reserved. Reproduction of any articles, advertisement or material from this issue is forbidden without permission of the publisher. Publisher assumes no responsibility and is not to be held liable for errors beyond the cost of the space occupied by advertisers. Proposed legislation may limit your options “hot rodding” your car. Story by Jim Costa NMMotorsportsReport.com • 3 RStory by David SwopeI S I N G DAYTONA BEACH, Fla.—Daytona Inter- qualifying races (the Can- national Speedway started a $400 million Am Duels) finalize the line- reimagining, dubbed “Daytona Rising” in July up for the Great American of 2013. The project was completed before the Race on the Thursday be- 2016 Rolex 24 at Daytona and was on full dis- fore Sunday’s Main Event. -

Nascar This Week 8 - the Derrick

NASCAR THIS WEEK 8 - THE DERRICK. / The News-Herald Wednesday, September 5, 2018 SPEED FREAKS QUESTIONS & ATTITUDE A few questions we had to ask INDIANAPOLIS ourselves Compelling questions ... and maybe a few actual answers Last year it was Kasey Kahne. THREE THINGS TO WATCH Who could be this year’s sur- So now the Brickyard goes up prise Brickyard winner? If everything against the NFL? GODSPEAK: Daniel Suarez is goes terribly my pick to upend the NASCAR wrong at To hopefully inject new life into apple cart at Indianapolis. Indianapolis, the Brickyard 400, NASCAR and KEN’S CALL: Jamie McMurray Jimmie Indy moved it from mid-summer showed some life at Darlington Johnson to September, where it becomes and he’s racing for his future ... (right) might the regular-season finale. Good but I’ll say Paul Menard. He’s become just move, in theory. Unfortunately, this done it before. a cheerleader not only puts it up against Week for Chase 1 of the NFL season, but right up Jimmie Johnson suggests he Elliott (left) in against the Indianapolis Colts, who can do well if he just makes the NASCAR are opening at home against the sure he’s in the playoffs. playoffs. Bengals. That’s a pool of 70,000 Believe him? Johnson has fans, from which the Brickyard will GODSPEAK: Yes, but that ESP made every surely lose a certain percentage. voice in my head is saying playoff field Johnson will somehow fall out since 2004. Who’s to blame? of the playoffs Sunday. It’s just [AP/RALPH been that kind of season for FRESO] Taylor Swift, kinda-sorta. -

Video Name Track Track Location Date Year DVD # Classics #4001

Video Name Track Track Location Date Year DVD # Classics #4001 Watkins Glen Watkins Glen, NY D-0001 Victory Circle #4012, WG 1951 Watkins Glen Watkins Glen, NY D-0002 1959 Sports Car Grand Prix Weekend 1959 D-0003 A Gullwing at Twilight 1959 D-0004 At the IMRRC The Legacy of Briggs Cunningham Jr. 1959 D-0005 Legendary Bill Milliken talks about "Butterball" Nov 6,2004 1959 D-0006 50 Years of Formula 1 On-Board 1959 D-0007 WG: The Street Years Watkins Glen Watkins Glen, NY 1948 D-0008 25 Years at Speed: The Watkins Glen Story Watkins Glen Watkins Glen, NY 1972 D-0009 Saratoga Automobile Museum An Evening with Carroll Shelby D-0010 WG 50th Anniversary, Allard Reunion Watkins Glen, NY D-0011 Saturday Afternoon at IMRRC w/ Denise McCluggage Watkins Glen Watkins Glen October 1, 2005 2005 D-0012 Watkins Glen Grand Prix Festival Watkins Glen 2005 D-0013 1952 Watkins Glen Grand Prix Weekend Watkins Glen 1952 D-0014 1951-54 Watkins Glen Grand Prix Weekend Watkins Glen Watkins Glen 1951-54 D-0015 Watkins Glen Grand Prix Weekend 1952 Watkins Glen Watkins Glen 1952 D-0016 Ralph E. Miller Collection Watkins Glen Grand Prix 1949 Watkins Glen 1949 D-0017 Saturday Aternoon at the IMRRC, Lost Race Circuits Watkins Glen Watkins Glen 2006 D-0018 2005 The Legends Speeak Formula One past present & future 2005 D-0019 2005 Concours d'Elegance 2005 D-0020 2005 Watkins Glen Grand Prix Festival, Smalleys Garage 2005 D-0021 2005 US Vintange Grand Prix of Watkins Glen Q&A w/ Vic Elford 2005 D-0022 IMRRC proudly recognizes James Scaptura Watkins Glen 2005 D-0023 Saturday