Report of the Comptroller and Auditor General of India on Public Sector Undertakings

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

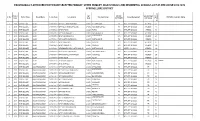

Physical Science 15 ------9493511572

SSC PUBLIC EXAMINATIONS, MARCH - 2015 :: SPOT VALUATION :: TENTATIVE SENIORITY LIST :: SPSR NELLORE DISTRICT SUBJECT :- PHY.SCI. No of Years Handling Whether in dealing X Class if yes, X Class DESIGNATION S/NO Name of the MANDAL NAME OF THE SCHOOL NAME OF THE TEACHER WITH SURNAME (including HM) in the present handling CELL NO REMARKS (with Subject) academic year subject SA CADRE LP CADRE (2014-2015) 1 OZILI APRS CHILAMANCHENU B. Vidyasagar PGT-PS Yes PS 24 9490413938 2 SYDAPURAM MMLWO HS TALUPUR I SREEDHAR SA-PS YES SCIENCE 22 0 9493525449 3 SULLURPET GHS SULLURPET G MADHUSUDHAN BABU SA-PS YES PS 21 9440994826 4 KAVALI MPL HS VR NAGAR B.Madhusudhana Raju SA-PS YES PS 20 9000390788 5 VAKADU PJN GHS VAKADU Smt A Nagamani SA-PS YES SCIENCE 19 9550640930 6 ALLUR RKJC ALLUR P.Sambaiah SA-PS YES PHYSICS 19 9441937729 7 VENKATAGIRI APSWRS GIRLS VENKATAGIRI C, Konaiah SA-PS Yes PS 18 18 9550930197 8 KAVALI APRS THUMMALAPENTA M.RAMESHCHANDRA PGT-PS YES PS 18 18 9493922110 9 OZILI ZPPHS KURUGONDA G MURALI SA-PS YES PS 17 9491448505 10 Nellore BVS Mpl Corp Girls High School, Nawabpet, NelloreM.Venkateswarlu SA-PS Yes P.S. 17 2 9866045253 11 SYDAPURAM MMLWO HS KALICHEDU V V RAMANAIAH SA-PS YES SCIENCE 16 0 9441539390 12 CHILLAKUR ZPPHS PCV PALEM B Srinivasulu SA-PS YES PS 15 8985939395 13 VENKATAGIRI RVM HS VENKATAGIRI K V USHAHARINI SA-PS yes PS 15 9492937007 14 Kodavalur APTW JR.COLLEGE (G), C S PURAM Paleti.Venkateswara rao PGT-PS Yes Physical science 15 ------ 9493511572 15 Indukurpet GAHS, MYPADU Devarapalli Ravindra Babu SA-PS YES PS 15 0 16 CHILLAKUR ZPPHS CHILLAKUR V VIMALA SA-PS YES PS 14 9866226754 17 SULLURPET ZPPHS MANNARPOLUR A RAMESH SA-PS Yes PS 14 9989123204 18 BUCHIREDDYPALEM ZPHS, Damaramadugu P.V. -

P.UMA MAHESWARI Gogonenipuram ,Nellatur Post, Gudur Mandalam,SPSR Nellore District

Application for Prior Environmental Clearance (Form – 1) For Proposed 14.77 Hect of Mica,Quartz & Feldspar Mine Sy. No: 28/P of Nandivai Village, Podalakur Mandal, S.P.S.R Nellore District, Andhra Pradesh. ________________________________________________________________________ Submitted To State Expert Appraisal Committee (SEAC), State Environmental Impact Assessment Authority, A.P. Submitted By ________________________________________________________________________________ P.UMA MAHESWARI Gogonenipuram ,Nellatur Post, Gudur Mandalam,SPSR Nellore District. 524101 FORM 1 (I) Basic Information Sl.No. Item Details 1. Name of the project 14.77 Ha of Mica, Quartz, & Feldspar mine of P.UMA MAHESWARI 2. S.No. in the schedule 1 (a) 3. Proposed capacity / tonnage to be handled /lease Proposed production is 8730 TPA of area Feldspar and 9930 TPA of Quartz over an extent of 14.77 Ha. 4. New/Expansion/Modernization Existing 5. Existing Capacity/Area etc. 14.77 Ha 6. Category of Project i.e. ‘A’ or ‘B’ B2 7. Does it attract the general condition? If yes, please No specify. 8. Does it attract the specific condition? If yes, please No specify. 9. Location Plot/Survey/Khasra No. Sy. No: 28/P Village Nandivai Village, Tehsil Podalakur Mandal , District SPSR Nellore District, State Andhra Pradesh 10. Nearest railway station/airport along with distance in The nearest Railway station is located at kms. Gudur at a distance of 45 km from the applied area. 11. Nearest Town, city, district Headquarters along with Podalakur (Mandal Head Quarter) is at distance in kms. a distance of 7 km from the applied area. 12. Village Panchayats, Zilla Parishad, Municipal P.Uma Maheswari Corporation, Local body (complete postal addresses Lessee with telephone nos. -

List of Teachers Working in Sri Potti Sriramulu Nellore District - Mp/Zp Management - Community - Sc

LIST OF TEACHERS WORKING IN SRI POTTI SRIRAMULU NELLORE DISTRICT - MP/ZP MANAGEMENT - COMMUNITY - SC S.N o district subject) Surname Sub-Caste Community which DSC) which Date of Birth Date present cadre In which cadre In which Placeofworking specify the subject) specify GO orGO other than the Name of the Mandal Date of joining in the in of joining Date Date of joining in this this in of joining Date Treasury Authorities) Name of the Teacher Management which in By promotion orBy direct He/She first appointed He/She Year of Year recruitment (in Designation (if SA / LP. / LP. (if SA Designation Employee ID (Givern ID by Employee present post(Specify the present post(Specify Transfer made was under Inter District InterTransfer District / 610 Appointed in which District which in Appointed 1 S.R.PURAM 0831801 GOLLAPALLI G.V.Ramanaiah PSHM MPPS S.R.Nagar 01/01/1960 SC Madiga MP/ZP 1985 Nellore PSHM promotion 11/07/2003 2 S.R.PURAM 0823074 KALIVELA K.Vijayababu PSHM MPUPS Devamma Cheruvu 04/04/1963 SC Madiga MP/ZP 1986 Nellore PSHM promotion 02/12/2009 3 S.R.PURAM 0822538 THIRUVAIPATHI T. Sanjeevarao PSHM MPUPS N.R.Peta 15/06/1959 SC Mala MP/ZP 1984 Nellore PSHM promotion 18/07/2009 4 S.R.PURAM 0823046 JYOTHI J. Mala Kondaiah PSHM MPPS Pandrangi 15/07/1961 SC Mala MP/ZP 1985 Nellore PSHM promotion 02/12/2009 5 KONDAPURAM0818486 CHITTURI Karunakumari Chitturi PSHM MPPS Saipeta Main 01/03/1962 SC ADIANDHARA MP/ZP 1988 Nellore PSHM promotion 02/02/2009 6 KONDAPURAM0829294 MOCHERLA Venkataramanamma Mocherla PSHM MPPS Kovivaripalli 15/08/1960 SC HARIJANA -

State Bank of India - 4388 1 P

SOUVENIR - 2017 STATE BANK OF INDIA - 4388 1 P . DAST AGIRI REDDY NANDY AL 76 S. B. RAMA KRISHNA ADONI 151 R. SHARSCHANDRA ALLAGADDA 2 P . GOWRI NANDY AL 77 N. DHARANI ADONI 152 P . SRINIV ASULU ALLAGADDA 3 K. DIVY A RAGHA VENDRA A. KODUR 78 K. HARI PRASAD ADONI 153 E. NARASIMHAM ALLAGADDA 4 TEEGA RAMADEVI A.MUPP ALLA 79 KOMALA BHARA TH KUMAR ADONI 154 K. INDRAJA ALLAGADDA 5 S. CHANDRA SEKHAR A.P ALLI 80 M.P . LA V ANY A ADONI 155 G . VISWESW ARAIAH ALLAGADDA 6 MA T ALA YERRINAIDU A.PURAM 81 M. CHOLARAJU ADONI 156 P . SUDHAKAR REDDY ALLAGADDA 7 RASAD DHARAMIREDDY A.PURAM 82 N. SRIDHAR ADONI 157 B. VIJA Y A LAKSHMI ALLAGADDA 8 KOLA GOV ARDHAN ABBASAHEBPET A 83 B. RA VINDRA ADONI 158 M. RAMANA REDDY ALLAGADDA 9 G . CHANDRA SEKAR REDDY ACHAMPET 84 S. AMARNA THA REDDY ADONI 159 B. NAGABHUSHANAM ALLAP ADU 10 T . ESMAIL ACHAMPET 85 S. RA VI KUMAR ADONI 160 K. SOWJANY A RANI ALLUR V ARIP A TNAM 1 1 K. YELLA SWAMY ACHAMPET 86 SURE KRISHNA ADONI 161 KELLA MURTHI ALUGOLU 12 CHIKKUDU SHEKHAR ACHAMPET 87 S. RIZWANA ADONI 162 V . KOTESW ARA REDDY ALUR 13 SURESH MUDA V A TH ACHAMPET 88 B. VEERESHAMMA ADONI 163 K. CHINNA BABU ALUR 14 M. BHASKAR ACHAMPET 89 C. PRAKASH ADONI 164 B. RAJA SEKHARA REDDY ALUR 15 P . PAR THASARADHI ACHAMPET 90 N. USHA RANI ADONI 165 H.B. RA VIKUMAR GOUD ALUR 16 M. P . CHAKRA V AR THY ACHAMPET 91 B. -

PROVISIONALLY APPROVED FIRST PHASE SELECTED PRIMARY, UPPER PRIMARY, HIGH SCHOOLS and RESIDENTIAL SCHOOLS LIST AS PER U-DISE 2018-19 in SPSR NELLORE DISTRICT T N E

PROVISIONALLY APPROVED FIRST PHASE SELECTED PRIMARY, UPPER PRIMARY, HIGH SCHOOLS AND RESIDENTIAL SCHOOLS LIST AS PER U-DISE 2018-19 IN SPSR NELLORE DISTRICT t n e l m District LGD SCHOOL Selected Dept a t e Sl. No. District Name Mandal Name School Code School Name Panchayat Name School Management l REMARKS ( Selected criteria) o o Code Code CATEGORY with Mandal T r n E 1 2819 SPSR NELLORE ALLUR 28191501305 MPPS BEERAMGUNTA MAIN 208252 BEERANGUNTA PS MPP_ZPP SCHOOLS APEWIDC 34 2 2819 SPSR NELLORE ALLUR 28191500503 MPPS WEST GOGULAPALLI GC 208262 WESTGOGULAPALLI PS MPP_ZPP SCHOOLS APEWIDC 48 3 2819 SPSR NELLORE ALLUR 28191501208 MPUPS PURINI 208260 PURINI UPS MPP_ZPP SCHOOLS APEWIDC 59 4 2819 SPSR NELLORE ALLUR 28191500802 MPPS BATRAKAGOLLU 208251 BATRAGAGALLU PS MPP_ZPP SCHOOLS APEWIDC 60 GRADDGUNTA 5 2819 SPSR NELLORE ALLUR 28191500702 MPUPS GRADDAGUNTA 208255 UPS MPP_ZPP SCHOOLS APEWIDC 65 6 2819 SPSR NELLORE ALLUR 28191501001 MPPS NORTH MOPUR MAIN 208259 NORTH MOPUR PS MPP_ZPP SCHOOLS APEWIDC 83 7 2819 SPSR NELLORE ALLUR 28191501103 MPUPS INDUPURU 208256 INDUPUR UPS MPP_ZPP SCHOOLS APEWIDC 95 8 2819 SPSR NELLORE ALLUR 28191500204 MPUPS SINGAPETA 208261 SINGA PET UPS MPP_ZPP SCHOOLS APEWIDC 102 9 2819 SPSR NELLORE ALLUR 28191500909 MJPAPBCWRS GIRLS NORTH AMULUR 208258 NORTH AMULUR UPS APREI Society Schools APEWIDC 129 10 2819 SPSR NELLORE ALLUR 28191500506 MPUPS EAST GOGULAPALLI 208253 EAST GOGULAPALLI UPS MPP_ZPP SCHOOLS APEWIDC 141 11 2819 SPSR NELLORE ALLUR 28191500411 MPPS ISKAPALLI PATTUPALEM 209095 ISAKAPALLE PS MPP_ZPP SCHOOLS -

1 Anantapur PEDDAPAPPUR 1 AMMALADINNE 2 Anantapur

SLBC OF AP CONVENOR:ANDHRA BANK ANDHRAPRAGATHI GRAMEENA BANK HEAD OFFICE: KADAPA PLANNING AND DEVELOPMENT DEPARTMENT Financial Inclusion Plan Villages allotted to the Bank under Financial Inclusion Plan (District wise) Name of the S. No District Name of block/MANDAL S No Name of the unbanked village 1 Anantapur PEDDAPAPPUR 1 AMMALADINNE 2 Anantapur PEDDAPAPPUR 2 MUCHUKOTA 3 Anantapur PUTLUR 3 KADAVAKAL 4 Anantapur PUTLUR 4 CHERLOPALLI 5 Anantapur PUTLUR 5 KUMMANAMALA 6 Anantapur AGALI 6 INGALORE 7 Anantapur AGALI 7 KODIHALLI 8 Anantapur AGALI 8 NARASAMBUDI 9 Anantapur AMADAGUR 9 CHINAGANIPALLI 10 Anantapur AMADAGUR 10 THUMMALA 11 Anantapur TALUPULA 11 KURLI 12 Anantapur TALUPULA 12 LAKKASAMUDRAM 13 Anantapur TALUPULA 13 ODULAPALLI 14 Anantapur NARPALA 14 BANDLAPALLI 15 Anantapur NARPALA 15 SIDDARACHERLA 16 Anantapur RAPTADU 16 MARUR 17 Anantapur RAPTADU 17 PALACHERLA 18 Anantapur TADIMARRI 18 M.AGRAHARAM 19 Anantapur TADIMARRI 19 C.C.REVU 20 Anantapur RAYADURG 20 JUNJURAMPALLI 21 Anantapur RAYADURG 21 VEPARALLA 22 Anantapur BRAHMASAMUDRAM 22 KANNEPALLI 23 Anantapur CHILAMATHUR 23 SETTIPALLI 24 Anantapur GORANTLA 24 VADIGEPALLI Name of the S. No District Name of block/MANDAL S No Name of the unbanked village 25 Anantapur PEDDAPAPPUR 25 NARASAPURAM 26 Anantapur YADIKI 26 NITTURU 27 Anantapur YADIKI 27 VEMULAPADU 28 Anantapur TADPATRI 28 BRAMHANAPALLI 29 Anantapur D.HIRCHAL 29 OBULAPURAM 30 Anantapur TADIMARRI 30 PEDDAKOTLA 31 Anantapur CHENNE KOTHAPALLE 31 PYADINDI 32 Anantapur DHARMAVARAM 32 CHINGICHERLA 33 Anantapur KAMBADUR 33 PALLUR -

SPOT AE CES WORK.Xlsx

SSC SPOT VALUATION - APRIL - 2013 :: PROVISIONAL SENIORITY LIST OF CHIEF EXAMINERS / ASST. EXAMINERS (HEADMASTERS) SUBJECT : - HEADMASTERS Whether dealing X Class in Sno Name of the Teacher Designation SUBJECT MEDIUM Place of Working MANDAL the present academic SA CADRE Division year (2012-2013) 1 S.V. SUBBAMMA HM BS TEL ZP HIGH SCHOOL, NARASAPURAM YES 32 Nellore 2 N.V.NARAYANA RAO HM BS TEL ZPHS,V.R.NAGAR UDAYAGIRI YES 23 Kavali 3 P. VENKATESWARLU HM BS TEL ZP HIGH SCHOOL, BRAHMADEVAM YES 21 Nellore 4 SK. NOOR AHAMED HM BS TEL GOVT HIGH SCHOOL, KOVUR YES 20 Nellore 5 SK MASTHANAMMA HM BS TEL ZPHS, Vindur GUDUR YES 20 Gudur 6 G. VENKATESWARLU HM BS TEL MCHS M.G. NAGAR, NELLORE YES 17 Nellore 7 DARAPANENI VENGAIAH HM BS TEL ZPHS,DUBAGUNTA A.S. PETA Yes 15 Kavali 8 MA.RAHEEM HM BS TEL ZPHS,APPASAMUDRAM UDAYAGIRI YES 15 Kavali 9 M DILEEP KUMAR HM BS TEL ZPHS, NELLATUR Gudur YES 15 Gudur 10 SK ANWAR HUSSAIN HM BS TEL ZPHS, PENUBARTHI RAPUR YES 15 Gudur 11 D ROBERT PAUL HM BS TEL ZPHS, MULAPADAVA VAKADU YES 15 Gudur 12 M.SREENIVASULU HM BS TEL ZPHS,CHILAKALAMARRI ANANTASAGARAM YES 14 Kavali 13 S RAJYALAKSHMAMMA HM BS TEL ZPHS, THIKKAVARAM CHILLAKUR YES 14 Gudur 14 N. Paranjyothi HM BS TEL CSM HS, GUDUR Gudur YES 14 Gudur 15 Smt T. Prasuna HM BS TEL ZPHS, BV PALEM MANUBOLU YES 14 Gudur 16 K.P.PREMALATHA HM BS TEL ZPHS, KALLURU D V SATRAM YES 13 Gudur 17 K VENKATARAYULU HM BS TEL ZPBHS, PODALAKUR PODALAKUR YES 12 Gudur 18 Y. -

Annual Report 2008 – 09 RRDS, Maruthi Nagar, Nellatur Post, Gudur

Annual Report 2008 – 09 RRDS, Maruthi Nagar, Nellatur Post, Gudur Mandal -524 102 Nellore District, A.P, South India, Ph: 91-08624-222589, E-mail: [email protected], [email protected] Contents Introduction Programs 1. Integrated Management for Tackling Moisture Stress in Dry land Agriculture(report available) 2. Andhra Pradesh Community Based Tank Management Project 3. APSACS (proposal and data available) 4. Tsunami Rehabilitation Program Introduction: Rural Reconstruction Development Society (RRDS) is a registered non-governmental organization working for the development of Dalith, Adivasi, Women, Children, Physically challenged people and people living with HIV- Aids. Community based organizations have been formed and strengthened to bring social justice and to work s as a tool in order to the set objectives. RRDS has strong Institutional base with committed human resources. It is committed to work with Dalits, Tribes and fisher folk for reduction of poverty through people institutions which will empower poorest of poor community towards sustainable development . Vision: Improving the livelihoods and of livelihood, education health and social justice of the marginalized Communities Goal: Empowerment of oppressed and depressed Communities Mission: To create self confidence among the Dalit, Adivasi, Fishermen and Minorities, women and other deprived sections of the society by facilitating to develop their inherent skills. RRDS Approach: Participatory stakeholder centered community development is a right based approach in which their families and communities are active and leading in their own development. It enhances their capacity and opportunity to work together with others to address the structural RRDS – AREAS OF SERVICES Irrigation & RRDS Women Agriculture & Children & Community Youth based Organizations’ HIV & Aids Health Migrants Project Tsunami Dalit Rehabilitation Adivasi Area of operation Name of the No. -

Response Bulletin Andhra Pradesh Floods, 2015

RESPONSE BULLETIN ANDHRA PRADESH FLOODS, 2015 VOL- 1 JANUARY ISSUE, 2016 ANDHRA PRADESH FLOODS After the deep depression in Bay of Bengal shifted towards Andhra Pradesh on 18th November, unprecedented heavy rainfall has been received after a long years. The major affected districts are Nellore, Kadappa, Chittor and East Prakasam where the incessant rains led to inundation of low-lying areas in towns and villages. Moderate rains are expected at isolated places of Guntur, Krishna and West Godavari during the next two days. As per IMD Weather warning, there may be moderate to rather heavy rainfall at isolated places over south coastal Andhra Pradesh and Rayalaseema in the next 24 to 48 hours. The Pennar River is the major river flowing through the District into Bay of Bengal from Somasila Reservoir. The other rivers flowing in the District are Swarnamukhi, Pambaleru, Kalangi, Tsallakalva, Royyala kalva and Venkatagiri-yeru. Tributaries to Penna like Kandaleru and Boggeru serve the remaining area. Due to the rivers flowing in spate many lakes and small reservoirs have been breached and have cause much damage to property and loss of life. Including Nellore city, where other major towns in Nellore district and far most count of numerous villages were deadly affected by the cyclone effect and all backwater areas got drowned in the down coast areas of villages and were fully submerged. Nellore, Chittor, Kadappa & East Worst Affected Districts Prakasam Population died 33 approx. Population Affected 18 Lakh approx. Village Affected 1193 approx. Villages fully inundated 146 Milch Animal Affected 740 The National Highway (NH-5) (Golden Quadrilateral) between Nellore and Gudur has been washed away in two places near Manubolu effectively cutting off all connections. -

Joint Needs Assessment Report on Andhra Pradesh Floods, 2015

Joint Needs Assessment Report on Andhra Pradesh Floods, 2015 Joint Needs Assessment Report – Phase 25th November to 25th December 2015 This report contains the compilation of the JNA –Phase 01 actions in the state of Andhra Pradesh , India in the aftermath of heavy rainfall caused due to the depression in Bay of Bengal resulted severe flooding across South India. Tamil Nadu state was severely affected by floods. Government, Civil Societies and community were overwhelmed with the unprecedented rainfall. Joint Needs Assessment Report: Andhra Pradesh Floods 2015 Disclaimer: The interpretations, data, views and opinions expressed in this report are collected from Inter- agency field assessments (RJNA), District Administration, individual aid agencies assessments and from media sources are being presented in the Document. It does not necessarily carry the views and opinion of individual aid agencies, NGOs or Sphere India platform (Coalition of humanitarian organisations in India) directly or indirectly. Note: The report may be quoted, in part or full, by individuals or organisations for academic or Advocacy and capacity building purposes with due acknowledgements. The material in this Document should not be relied upon as a substitute for specialized, legal or professional advice In connection with any particular matter. The material in this document should not be construed as legal advice and the user is solely responsible for any use or application of the material in this document. Page 1 of 43 | December 2015 Joint Needs Assessment Report: -

Sgt Adjustment

ADJUSTMENT OF SECONDARY GRADE TEACHERS OF HIGH SCHOOLS IN CLEAR VACANCIES IN PRIMARY/UPPER PRIMARY ANNEXURE - A Designat Name of the School in which Teacher Name of the Sl.No. Name of the Teacher Place of Working Name of the Mandal ion Adjusted Adjusted MANDAL 1 J.V.S.SASTRY SGT ZPHS,A.S PETA A.S.PETA MPUPS, TELLAPADU A.S.PET 2 K.SURYA BABU SGT ZPHS,A.S PETA A.S.PETA MPPS, A.S.PET HW A.S.PET 3 PDWEENA SGT ZPHS,A.S PETA A.S.PETA MPPS, TELLAPADU SC A.S.PET 4 CH.SRINIVASULU SGT ZPHS,A.S PETA A.S.PETA MPPS, CHIRAMANA MAIN A.S.PET 5 U.SARADHA SGT ZPHS,SRIKOLANU A.S.PETA MPPS, CHIRAMANA MAIN A.S.PET 6 N.SRINIVASULU SGT ZPHS,SRIKOLANU A.S.PETA MPPS, SRIKOLANU MAIN A.S.PET 7 CH.SUBBA NAIDU SGT MPPS,KUPPURUPADU (M) A.S.PETA MPUPS, RAJAVOLU A.S.PET 8 M.HAZARATHAIAH SGT MPPS,GUDIPADU (S.C) A.S.PETA MPPS, DOOBAGUNTA A.S.PET 9 K.JYOTHI SGT MPPS,SRIKOLANU (B.C) A.S.PETA MPPS, GOLLAMITTA DPEP A.S.PET 10 R.V.MADHUSUDHANA RAO SGT MPPS,RANGANAPADU A.S.PETA MPUPS, RAJAVOLU A.S.PET A.S.PETA Count 10 Page 1 of 52 ADJUSTMENT OF SECONDARY GRADE TEACHERS OF HIGH SCHOOLS IN CLEAR VACANCIES IN PRIMARY/UPPER PRIMARY ANNEXURE - A Designat Name of the School in which Teacher Name of the Sl.No. Name of the Teacher Place of Working Name of the Mandal ion Adjusted Adjusted MANDAL 1 Y.VENKATA RAMANAIAH SGT ZPHS,ANANTHASAGARAM A.SAGARAM MPPS, K.R.PADU MAIN A.SAGARAM 2 Sd.ABDUL MAJEED SGT-U ZPHS,ANANTHASAGARAM A.SAGARAM MPUPS, VENKATARAO PALI ATMAKUR 3 Sd.ARIFULLA SGT-U ZPHS,ANANTHASAGARAM A.SAGARAM MPPS, GUDIPADU A.S.PET 4 V.CHANDRA SEKHAR SGT ZPHS,REVURU A.SAGARAM MPPS, -

Narayana Engineering College, Gudur

NARAYANA ENGINEERING COLLEGE:: GUDUR Department of Electrical & Electronics Engineering FEB- 2019 Events Summary S. Involved DATE NAME OF THE EVENT LOCATION Resource Person N by O Industrial Visit to Transformer Repair & Maintenance and Mr.Uday kumar 33/11 KV SS SPM Section, II & III A.E ,APSPDCL 1. 02.02.2019 APSPDCL Goginenipuram, Year Nellatur Nellatur Nellaturu, Students Venkatagiri – Gudur Road, SPSR Nellore (DT),A.P I,II, III & EEE Seminar 2. 16.02.2019 “ASSOCIATION DAY “ Mr.SK.Althaf IV Year Hall A.D.E ,APSPDCL Students 1.Mr.Sk.Shageer II & III 2.Ms.A.Dhana Lakshmi 18-02-2019 Certificate Course on Year 3.Ms.R.Yoga Priyanka 3. to “PROGRAMMABLE Students CP LAB-I 23-02-2019 LOGIC CONTROLLER” 4.Ms.K.Indumathi APSSDC , Vijayawada 1. Industrial visit at Transformer Repair & Maintenance and 33/11 KV SS SPM Section, APSPDCL Goginenipuram, Nellaturu, 02.02.2019 The third year and second year students of EEE department went for an Industrial Visit to Transformer Repair & Maintenance and 33/11 KV SS SPM Section, APSPDCL Goginenipuram, Nellaturu, on 02.02.2019. The students were studying transformers in the current semester .The industrial visit to this transformer manufacturing unit was very informative and students could actually see the assembly of cores, primary and secondary windings, the various types of insulation used in the windings, types of protection used, testing, etc., 33/11kv air cooled and oil cooled transformers. 2. “ASSOCIATION DAY “ 16.02.2019 In this regard we invited students from various colleges to participate in poster presentation, project/model expo, paper presentation, quiz competition and circuit worksheet challenge .It‘s a platform to the students to exhibit their innovative ideas ,talents and to share their knowledge.