2020 Agribusiness Market Study

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2018 Annual Report Built Drive to Growth

BUILT TO DRIVE GROWTH 2018 ANNUAL REPORT BUILT TO DRIVE BUILT GROWTH CP 2018 ANNUAL REPORT PERFORMANCE HIGHLIGHTS $ in millions, except per share data, ratios or unless otherwise indicated 2014 2015 2016 2017 2018 EXCHANGELISTINGS FINANCIAL HIGHLIGHTS Total revenues $ 6,620 $ 6,712 $ 6,232 $ 6,554 $ 7,316 The common shares of Canadian Pacific Railway Limited are (1) Operating income 2,202 2,618 2,411 2,519 2,831 listed on the Toronto and New York stock exchanges under Adjustedoperatingincome(1)(2) 2,198 2,550 2,411 2,468 2,831 the symbol CP. Operating ratio (1) 66.7% 61.0% 61.3% 61.6% 61.3% Adjusted operating ratio (1)(2) 66.7% 62.0% 61.3% 62.4% 61.3% Net income 1,476 1,352 1,599 2,405 1,951 Adjusted income (2) 1,482 1,625 1,549 1,666 2,080 CONTACTUS Diluted earnings per share (EPS) 8.46 8.40 10.63 16.44 13.61 Investor Relations AdjusteddilutedEPS(2) 8.50 10.10 10.29 11.39 14.51 Email: [email protected] Cash from operations 2,123 2,459 2,089 2,182 2,712 Free cash (2) 969 1,381 1,007 874 1,289 Canadian Pacific Investor Relations Return on invested capital (ROIC) (2) 14.4% 12.9% 14.4% 20.5% 15.3% 7550 Ogden Dale Road S.E. Adjusted ROIC (2) 14.5% 15.2% 14.0% 14.7% 16.2% Calgary, AB, Canada T2C 4X9 Shareholder Services STATISTICAL HIGHLIGHTS(3) Email: [email protected] Revenue ton-miles (RTMs) (millions) 149,849 145,257 135,952 142,540 154,207 Canadian Pacific Shareholder Services Carloads (thousands) 2,684 2,628 2,525 2,634 2,740 Office of the Corporate Secretary Gross ton-miles (GTMs) (millions) 272,862 263,344 242,694 252,195 275,362 7550 Ogden Dale Road S.E. -

The Impact of the Agribusiness Sector on the South Carolina Economy

The Impact of the Agribusiness Sector on the South Carolina Economy Prepared for: Palmetto AgriBusiness Council South Carolina Department of Agriculture South Carolina Farm Bureau Clemson University Public Service Activities London & Associates January 2015 This report was prepared with statistics that are readily available through public sources, without any private or confidential proprietary information from any industry sector being included. For consistency, the current impact assessment for the agribusiness sector uses the same approach and data sources used in the earlier report released in 2008 using 2006 data. The current model uses 2013 data released in December 2014. Data in both studies were provided by the Minnesota Impact Group drawn from annual reports of the U.S. Department of Commerce, Bureau of Economic Analysis. Both assessments were conducted with the IMPLAN model maintained by the Minnesota Impact Group and originally developed at the U.S. Forest Service. The Impact of the Agribusiness Sector on the South Carolina Economy Palmetto AgriBusiness Council South Carolina Department of Agriculture South Carolina Farm Bureau Clemson University Public Service Activities Report Prepared by James B. London London & Associates Photograph provided by Peter Tögel, Clemson University Public Service Activities Contents PREFACE.......................................................................................................................... iv EXECUTIVE SUMMARY ................................................................................................... -

AGRO-PESSIMISM, CAPITALISM and AGRARIAN CHANGE: TRAJECTORIES and CONTRADICTIONS in SUB-SAHARAN AFRICA Carlos Oya

AGRO-PESSIMISM, CAPITALISM AND AGRARIAN CHANGE: TRAJECTORIES AND CONTRADICTIONS IN SUB-SAHARAN AFRICA Carlos Oya Chapter 10 forthcoming in the Political Economy of Africa, edited by V. Padayachee, London: Routledge, 2010, ISBN: 978-0-415-48039-0. Version before proofs. INTRODUCTION The importance of agriculture in Sub-Saharan Africa (SSA) appears to be obvious and is widely noted in the literature on African1 development. For example, the Commission for Africa (2005) states that „agriculture contributes at least 40 per cent of exports, 30 per cent of GDP, up to 30 per cent of foreign exchange earnings, and 70 to 80 per cent of employment‟. There is however wide variation across countries in the relative importance of agriculture measured in terms of its contribution to GDP and exports, as well as aggregate evidence that agriculture‟s share of GDP has declined significantly in many countries. Still, the significance of agriculture as an occupation (either as “main” or “secondary” occupation in both rural and peri-urban areas) is well established. Conventional wisdom tends to present us with two images. First, one hears that there is significant potential for agricultural development, often understood in static terms of comparative advantage.2 This informs agriculture-centred development strategies where „agricultural productivity gains must be the basis for national economic growth and the instrument for mass poverty reduction and food security‟ (World Bank 2007: 19).3 Second, this potential is regarded as severely constrained for several reasons and aggregate agricultural performance is judged to have been disappointing if not dismal. The literature on Africa, especially in the aftermath of the global recession of the 1970s, has been largely pessimistic, and despite some more nuanced assessments in recent times, „Agro-Afro- pessimism‟ continues to permeate policy discourse. -

University of Guelph-University of Guelph 2020 Food Price Report

CANADA’S FOOD PRICE REPORT 10TH EDITION 2020 AUTHORS AND ADVISORS DALHOUSIE UNIVERSITY MEMBERS Dr. Sylvain Charlebois Dr. Andrea Giusto Hyejung (Cathy) Bae (Lead Author and Project Lead for Department of Economics Applied Research, Nova Scotia Dalhousie University) [email protected] Community College Agri-Food Analytics Lab [email protected] Kathleen Kevany [email protected] Faculty of Agriculture Emon Majumder Eamonn McGuinty [email protected] Applied Research, Nova Scotia Agri-Food Analytics Lab Community College Don Fiander [email protected] [email protected] DalAnalytics Dr. Vlado Keselj [email protected] Jay Harris Faculty of Computer Science Schulich School of Business, York Joon Son [email protected] University IBM Canada [email protected] Janet Music [email protected] Agri-Food Analytics Lab [email protected] UNIVERSITY OF GUELPH MEMBERS Dr. Simon Somogyi Paul Uys Dr. Jess Haines (Project Lead for University Ontario Agricultural College Family Relations and Applied of Guelph) (OAC) Nutrition Gordon S. Lang School of [email protected] [email protected] Business and Economics Dr. Francis Tapon Dr. Graham Taylor [email protected] Gordon S. Lang School of School of Engineering Dr. Erna Van Duren Business and Economics [email protected] Gordon S. Lang School of [email protected] Alexander Moksyakov Business and Economics School of Engineering [email protected] [email protected] Canada’s Food Price Report 2020 is a collaborative effort between Dalhousie University, led by the Faculties of Management -

The Scope and Importance of Agribusiness

The Scope and Importance of Agribusiness MERICANS enjoy a high standard of Aliving because of the abundance of inexpensive agricultural products. Most Americans do not have to worry about having enough food to eat or clothes to wear because of an agribusiness system that is the best in the world. Objective: þ Describe agribusiness, and determine the scope of the agriculture industry. Key Terms: Ñ agribusiness exports private sector agribusiness input gross domestic product production sector imports production agriculture agribusiness output input production efficiency sector marketing public agriservices agriservice output public sector agriservices sector private agriservices value-added products Agribusiness and Society Agribusiness includes all the activities within the agricultural food and natural resource industry involved in the production of food and fiber. Individual agribusinesses may sell items to farmers for production; provide services to other agricultural businesses; or be engaged in the marketing, transportation, processing, and distribution of agricultural products. Agriservice is activities of value to the user or buyer. The activities are an intangible product. Marketing is providing the products and services that people want when and where they want them. Agribusiness provides people with food, clothing, and shelter. It also provides jobs for mil- lions of people in science, research, engineering, education, advertisement, government agen- E-unit: The Scope and Importance of Agribusiness Page 1 u www.MyCAERT.com Copyright © by CAERT, Inc. — Reproduction by subscription only. E060001 cies, trade organizations, and commodity organizations. Agribusiness pertains to the public and private sectors. The public sector is the economic and administrative functions of dealing with the delivery of goods and services by and for the government. -

Market Index Uniflex 10%

Investment and retirement 5% 10% Market Index Uniflex 10% 25% Main Product Features 25% 6-year term (not redeemable before maturity) Guarantee of principal on maturity of 100% Low management fees of 1% per year 10% 15% $500 minimum deposit An easy way to diversify Cut-off age: 64 y/o (registered) and 70 y/o (non-registered) Even under a scenario where the return of each share is negative, this product may produce a global positive return Sector diversification of the Market Index Uniflex How it works On the settlement date, a starting level will be determined for each Canadian share included in the portfolio. On the maturity date, a ratio of the closing level over the starting level for each share will be computed. The 8 best performing shares during the 6-year term will be automatically assigned a fixed return of 60%, regardless of whether the actual return was positive or negative. The remaining 12 shares will be assigned their actual return. The global return (maximum 60%) will be calculated by averaging these 20 returns. The value at maturity will be the highest value between: the initial deposit; or the initial deposit PLUS global return (maximum 60%) Exposure to 20 Canadian companies included in the S&P/TSX 60 Index Company Sector Company Sector Metro Inc. Scotiabank Consumer staples Loblaw Companies Limited The Toronto-Dominion Bank Royal Bank of Canada Financial services Bank of Montreal Enbridge Inc. Sun Life Financial Inc. TransCanada Corporation Cenovus Energy Inc. Energy Canadian Natural Resources Limited Canadian National Railway Industrials Suncor Energy Inc. -

Johne's Disease Prevention and Control on Organic Dairy Farms in Ontario, Canada

Johne’s Disease Prevention and Control on Organic Dairy Farms in Ontario, Canada by Laura Pieper A Thesis presented to The University of Guelph In partial fulfilment of requirements for the degree of Doctor of Philosophy in Population Medicine Guelph, Ontario, Canada © Laura Pieper, July, 2014 ABSTRACT JOHNE’S DISEASE PREVENTION AND CONTROL ON ORGANIC DAIRY FARMS IN ONTARIO, CANADA Laura Pieper Advisor: University of Guelph, 2014 Professor David F. Kelton This thesis investigates Johne’s disease (JD) risk factors and control strategies on organic and conventional dairy farms in Ontario, Canada. The JD Risk Assessment and Management Plan (RAMP) was evaluated and used for the comparison of JD control between both farming types. Attitudes about JD control among organic producers and veterinarians were further investigated. RAMP data and JD milk or serum ELISA results from herds voluntarily participating in the Ontario Johne’s Education and Management Assistance Program (OJEMAP) were used for the first three research chapters. Individual interviews and focus groups with organic producers and veterinarians were used in the last two research chapters to understand attitudes about JD prevention and control, as well as about organic farming and the veterinarian-producer relationship. The veterinarian conducting the RAMP greatly influenced the RAMP scores and the recommendations that were given to the producers. However, the RAMP was considered useful in determining the between-herd and within-herd JD transmission risk and in identifying recommendations for JD control for the producers. Organic and conventional farms had a similar herd-level ELISA test-positive prevalence, but affected organic herds had a higher within-herd prevalence than affected conventional herds. -

Types of Jobs Available for Agribusiness & Agricultural Economics Graduates

TYPES OF JOBS AVAILABLE FOR AGRIBUSINESS & AGRICULTURAL ECONOMICS GRADUATES EMPLOYER POSITION(S) AAA Claims Representative Agrilogic Research Analyst AgriNorthwest Market Analyst Agri-Vision Operations Manager Alamo Title Escrow Agent Allen, Williford & Seale Real Estate Appraiser Animal Health International Outside Sales Representative Attebury Grain Grain Merchandiser Augusta National Golf Club Marketing Consultant BASF Corporation Agro Development & Programs BCI Broker Blue Bell Creameries Production Supervisor; Purchasing Agent BNSF Management Trainee Capital Farm Credit Credit Analyst Capital One Operations Analyst Operations Associate; Commodities Trader; Cargill Procurement Chevron Fundamental Analyst Citibank Dallas Credit Analyst Cold Creek Construction Project Coordinaotr Coldwell Banker Agent Assistant Collier Construction Project Coordinator Concierge Magazine Media Sales Conoco Estimator Constellation Energy Data Analyst Continuum Health Care Financial Department Dean Foods Management Trainee Dow AgroSciences Sales Trainee Ducks Unlimited, Inc. Regional Director Dupre Energy Services Sales Representative E&J Gallo Winery Management Development Edward Jones Financial Advisor Elanco Sales Representative FDIC FIS Trainee Federal Energy Regulation Commission Economist Food & Drug Administration Economist Frac-Tech International Research Associate Sales Management Trainee; Traffic Resource; Frito Lay Associate Analyst Glazer's Sales Trainee Graaves Mechanical Bidder Halliburton Associate Technical Professional School of Retail -

Agribusiness Interest in a Supervised Agricultural Experience (S AE)

Agribusiness Interest In A Supervised Agricultural Experience (S AE) Ideas for developing an agribusiness-related SAE Agribusiness Overview • According to the National Council for Agricultural Education, Agribusiness Systems (ABS) is described as: … the principles and techniques for the development and management of a business. • A wide range of technical skills and supports nearly all other areas of interest. • Sometimes agribusiness projects are either (1) Products or (2) Service Summary Of Skills Associated With Agribusiness • Business development through applying principles of supply and demand • Developing a business plan (SAE plan) • Management of resources (ex: land, labor, capital and management) • Record keeping, fnancial statements and inventory management • Cost of production and measurement of proft • Marketing and brand development • Risk management techniques and strategy • Other skills in technology and math Connect Your Interests To Your Project Entrepreneurship Placement Research Foundational An agribusiness learning A business or An agribusiness work A research project related experience or career for-profit venture experience to a business decision planning Time (Money, if applicable) Time is invested Time is invested Time is invested are invested Money is invested & Provides opportunity to at risk; Provides opportunity to Provides opportunity to learn about agribusiness or Provides opportunity to learn learn through exploration marketing through a learn and possibly earn a & possibly earn a paycheck or job shadowing -

Management Practices and Their Potential Influence on Johne's Disease Transmission on Canadian Organic Dairy Farms—A Concept

Sustainability 2014, 6, 8237-8261; doi:10.3390/su6118237 OPEN ACCESS sustainability ISSN 2071-1050 www.mdpi.com/journal/sustainability Review Management Practices and Their Potential Influence on Johne’s Disease Transmission on Canadian Organic Dairy Farms—A Conceptual Analysis Laura Pieper 1, Ulrike Sorge 2, Ann Godkin 3, Trevor DeVries 4, Kerry Lissemore 1 and David Kelton 1,* 1 Department of Population Medicine, University of Guelph, Ontario, ON N1G 2W1, Canada; E-Mails: [email protected] (L.P.); [email protected] (K.L.) 2 Department of Veterinary Population Medicine, University of Minnesota, St. Paul, MN 55108, USA; E-Mail: [email protected] 3 Veterinary Science and Policy Group, Ontario Ministry of Agriculture and Food (OMAF), Ontario, ON NOB 1S0, Canada; E-Mail: [email protected] 4 Department of Animal and Poultry Science, University of Guelph, Ontario, ON N1G 2W1, Canada; E-Mail: [email protected] * Author to whom correspondence should be addressed; E-Mail: [email protected]; Tel.: +1-519-824-4120 (ext. 54808); Fax: +1-519-763-8621. External Editor: Marc A. Rosen Received: 2 September 2014; in revised form: 4 November 2014 / Accepted: 5 November 2014 / Published: 18 November 2014 Abstract: Johne’s disease (JD) is a chronic, production-limiting disease of ruminants. Control programs aiming to minimize the effects of the disease on the dairy industry have been launched in many countries, including Canada. Those programs commonly focus on strict hygiene and management improvement, often combined with various testing methods. Concurrently, organic dairy farming has been increasing in popularity. Because organic farming promotes traditional management practices, it has been proposed that organic dairy production regulations might interfere with implementation of JD control strategies. -

Saskatchewan's Mining Supply Chain

Saskatchewan Mining Supply Chain First in Canada and top ten in the world for mining investment the past six of seven years. Fraser Institute, Survey of Mining Companies 2019 Our Mining Industry Saskatchewan mineral sales totalled $7.9 billion in In addition, the province has deposits of copper, zinc, 2019. Natural Resources Canada (NRCan) estimates that nickel, rare earth minerals and platinum group metals Saskatchewan accounted for 14% of national sales value, third as well as various industrial minerals including sodium highest in Canada. sulphate and salt. The province is the largest potash producer in the world, Major Mining Companies Operating in Saskatchewan accounting for approximately one-third of total production • Nutrien in 2019, and hosting over half of the globe’s potash reserves. • Mosaic Company Saskatchewan is also one of the world’s largest producers of uranium, with the Athabasca Basin containing the largest • BHP Billiton Canada Inc. high-grade uranium deposits in the world. • K+S Potash Canada Saskatchewan is Canada’s third-largest producer of coal, • ORANO Canada producing an average of 10 million tonnes per year. • Cameco The province is also home to one of the world’s largest fields • Vale Limited of diamond-bearing kimberlite. This discovery has led to • Rio Tinto extensive exploration and evaluation. • Acron Saskatchewan has large underexplored areas with high gold potential. The Seabee Operation produced 112,137 ounces • Yancoal of gold in 2019, a record annual production up 17% for the previous year. saskatchewan.ca/invest -

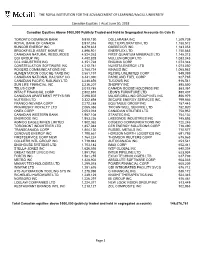

THE ROYAL INSTITUTION for the ADVANCEMENT of LEARNING/Mcgill UNIVERSITY

THE ROYAL INSTITUTION FOR THE ADVANCEMENT OF LEARNING/McGILL UNIVERSITY Canadian Equities │ As at June 30, 2018 Canadian Equities Above $500,000 Publicly Traded and Held in Segregated Accounts (in Cdn $) TORONTO DOMINION BANK 9,910,190 DOLLARAMA INC 1,209,739 ROYAL BANK OF CANADA 8,917,316 KELT EXPLORATION LTD 1,188,512 SUNCOR ENERGY INC 6,879,833 QUEBECOR INC 1,183,053 BROOKFIELD ASSET MGMT INC 4,896,921 ENERFLEX LTD 1,150,883 CANADIAN NATURAL RESOURCES 4,524,263 FIRST QUANTUM MINERALS LTD 1,145,213 CGI GROUP INC 4,482,828 MULLEN GROUP LTD 1,083,045 CCL INDUSTRIES INC 4,351,728 ENCANA CORP 1,073,348 CONSTELLATION SOFTWARE INC 4,212,781 NUVISTA ENERGY LTD 1,073,050 ROGERS COMMUNICATIONS INC 3,788,734 KINAXIS INC 1,065,983 ALIMENTATION COUCHE-TARD INC 3,581,197 RECIPE UNLIMITED CORP 949,389 CANADIAN NATIONAL RAILWAY CO 3,441,390 PARKLAND FUEL CORP 927,785 CANADIAN PACIFIC RAILWAY LTD 3,240,856 TUCOWS INC 916,541 SUN LIFE FINANCIAL INC 3,236,207 SHOPIFY INC 895,850 TELUS CORP 3,013,785 CANADA GOOSE HOLDINGS INC 883,361 INTACT FINANCIAL CORP 2,802,815 LEON'S FURNITURE LTD 880,407 CANADIAN APARTMENT PPTYS REI 2,498,502 MAJOR DRILLING GROUP INTL INC 856,979 NUTRIEN LTD 2,322,898 SECURE ENERGY SERVICES INC 799,566 FRANCO-NEVADA CORP 2,272,288 EQUITABLE GROUP INC 787,443 PRAIRIESKY ROYALTY LTD 2,065,386 TRICAN WELL SERVICE LTD 782,920 ONEX CORP 2,053,018 CANADIAN UTILITIES LTD 758,952 CANADIAN WESTERN BANK 1,987,108 STANTEC INC 754,132 ENBRIDGE INC 1,953,226 LASSONDE INDUSTRIES INC 745,893 AGNICO EAGLE MINES LIMITED 1,902,362 COGECO COMMUNICATIONS