DMCI Annual Report 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Diversification Strategies of Large Business Groups in the Philippines

Philippine Management Review 2013, Vol. 20, 65‐82. Diversification Strategies of Large Business Groups in the Philippines Ben Paul B. Gutierrez and Rafael A. Rodriguez* University of the Philippines, College of Business Administration, Diliman, Quezon City 1101, Philippines This paper describes the diversification strategies of 11 major Philippine business groups. First, it reviews the benefits and drawbacks of related and unrelated diversification from the literature. Then, it describes the forms of diversification being pursued by some of the large Philippine business groups. The paper ends with possible explanations for the patterns of diversification observed in these Philippine business groups and identifies directions for future research. Keywords: related diversification, unrelated diversification, Philippine business groups 1 Introduction This paper will describe the recent diversification strategies of 11 business groups in the Philippines. There are various definitions of business groups but in this paper, these are clusters of legally distinct firms with a managerial relationship, usually by virtue of common ownership. The focus on business groups rather than on individual firms has to do with the way that business firms in the Philippines are organized and managed. Businesses that are controlled and managed by essentially the same set of principal owners are often organized as separate corporations, not as separate divisions within the same firm, as is often the case in American corporations like General Electric, Procter and Gamble, or General Motors (Echanis, 2009). Moreover, studies on emerging markets have pointed out that business groups often occupy dominant positions in the business landscape in markets like India, Korea, Indonesia, Thailand, and the Philippines (Khanna & Palepu, 1997; Khanna & Yafeh, 2007). -

Sec 17-A Fy 2018

12. Check whether the issuer: (a) has filed all reports required to be filed by Section 17 of the SRC and SRC Rule 17 thereunder or Section 11 of the RSA and RSA Rule 11(a)-1 thereunder, and Sections 26 and 141 of The Corporation Code of the Philippines during the preceding twelve (12) months (or for such shorter period that the registrant was required to file such reports); Yes [ X ] No [ ] (b) has been subject to such filing requirements for the past ninety (90) days. Yes [ X ] No [ ] 13. State the aggregate market value of the voting stock held by non-affiliates of the registrant. P1,931,103,029 as of December 31, 2018 APPLICABLE ONLY TO ISSUERS INVOLVED IN INSOLVENCY/SUSPENSION OF PAYMENTS PROCEEDINGS DURING THE PRECEDING FIVE YEARS: 14. Check whether the issuer has filed all documents and reports required to be filed by Section 17 of the Code subsequent to the distribution of securities under a plan confirmed by a court or the Commission. Yes [ ] No [X] DOCUMENTS INCORPORATED BY REFERENCE 15. If any of the following documents are incorporated by reference, briefly describe them and identify the part of SEC Form 17-A into which the document is incorporated: Consolidated Financial Statements as of and for year ended December 31, 2018 (Incorporated as reference for Item 7 to 12 of SEC Form 17-A) ________________________________________________________________________ CENTURY PROPERTIES GROUP INC. Page 2 of 84 SEC Form 17-A TABLE OF CONTENTS PART I. BUSINESS AND GENERAL INFORMATION 4 Item 1 Business……………………………………………………………………………………………... 4 Item 1.1 Overview…………………………………………………………………………. -

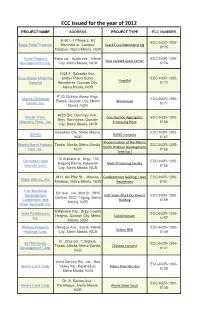

ECC Issued for the Year of 2012

ECC Issued for the year of 2012 PROJECT NAME ADDRESS PROJECT TYPE ECC NUMBER B-50 L-1 Phase 3. E2 ECC-NCR-1205- Eagle Food Products Martiniko st., Longos, Snack Food Manufacturing 0175 Malabon, Metro Manila, NCR Ayala Property Edsa cor., Ayala ave., Makati ECC-NCR-1205- Edsa Carpark Ayala Center Management Corp. City, Metro Manila, NCR 0174 1025 F. Salvador Ave., Cruz-Dalida Maternity Jordan Plains Subd., ECC-NCR-1205- Hospital Hospital Novaliches, Quezon City, 0172 Metro Manila, NCR #125 Quirino Hiway, Brgy. Manila Chemical ECC-NCR-1205- Baesa, Quezon City, Metro Warehouse Center, Inc. 0171 Manila, NCR #220 Sto. Domingo Ave., Pacific Paint Construction Aggregates ECC-NCR-1205- Brgy. Baringasa, Quezon (Boysen) Phils., Inc. Processing Plant 0168 City, Metro Manila, NCR Kalookan City, Metro Manila, ECC-NCR-1205- DSWD DSWD Complex NCR 0167 Modernization of the Manila Manila North Harbour Tondo, Manila, Metro Manila, ECC-NCR-1205- North Harbour Development Port, Inc. NCR 0166 Terminal I 116 Arellano st., Brgy. 135, Bernabest food ECC-NCR-1205- Bagong Barrio, Kalookan Meat Processing Facility Housse Corp. 0165 City, Metro Manila, NCR M.H. del Pilar St. , Maysilo, Condominium Building / Juez ECC-NCR-1205- Major Homes, Inc, Malabon, Metro Manila, NCR Residences 0161 Fort Bonifacio 5th Ave., cor. 30th St., BHS Development East Super Block Northwest ECC-NCR-1205- Central, BGC, Taguig, Metro Corporation and Building 0159 Manila, NCR Store Specialist Inc. Katipunan Ave., Brgy. Loyola Vista Residences, ECC-NCR-1205- Heights, Quezon City, Metro Condominium Inc. 0157 Manila, NCR Phinma Property Villongco Ave., Sucat, Makati ECC-NCR-1205- Solano Hills Holdings Corp. -

Quarterly Economic Update

DSI Wealth Management Group Presents: QUARTERLY ECONOMIC UPDATE A review of 1Q 2014 QUOTE OF THE THE QUARTER IN BRIEF QUARTER Bulls didn’t quite trample bears in the opening quarter of 2014. The S&P 500 slid “If there is no 3.56% in January, advanced 4.31% in February and gained another 0.69% in March. struggle, there is no Still, Q1 ended with the Dow in the red YTD and only minor YTD gains for the progress.” Nasdaq, S&P and Russell 2000; the broad commodities market outperformed the stock market. Some fundamental economic indicators were unimpressive during the – Frederick Douglass quarter, and analysts wondered if a ferocious winter was partly to blame. The Federal Reserve kept tapering QE3 as Ben Bernanke handed the reins to Janet QUARTERLY TIP Yellen. Unrest and currency problems hit some key emerging-market economies. Given the choice Home prices kept rising as home sales leveled off. Wall Street hoped the year 1 between a great wouldn’t mimic the quarter. lifestyle today and financial freedom DOMESTIC ECONOMIC HEALTH tomorrow, many The quarter ended with a major jump in consumer confidence. The Conference people opt to live for Board’s index reached 82.3 in March, up 4.0 points in a month. Consumer spending today – but no one improved too, rising 0.2% in January and 0.3% in February. (In a contrasting note, becomes wealthy by the University of Michigan’s consumer sentiment index slipped 2.5 points across the spending or living on quarter to a final March mark of 80.0.)2,3 margin. -

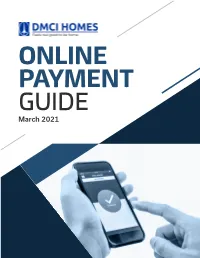

ONLINE PAYMENT GUIDE March 2021 Online Transactions Reference 3

ONLINE PAYMENT GUIDE March 2021 Online Transactions Reference 3 BDO 4 BPI 6 Eastwest Bank 8 Metrobank 12 UnionBank 14 Robinsons Bank 15 For concerns and clarifications, you may contact Customer Care through the following channels: Phone: Manila (02) 8555.7700 • (0918) 918.3465 • (0917) 811.5268 Davao (082) 297.0447 • (0998) 592.4529 Chat: dmcihomes.com or facebook.com/dmcihomesofficial Email: [email protected] • [email protected] Disclaimer: The details in this manual are subject to change without prior notice. DMCI Homes Online Payment Guide | March 2021 Online Transactions Reference Enjoy convenient and secured ways to pay your amortization, property tax, and other fees via Systems Information Desk (SID) or bills payment thru online banking using your debit or credit card. Available Payment Gateway via Online Banking Systems Information Desk (SID) Bills Payment Bills and Dues (DMCI Project eghl Global Payments Developers, Inc.) Reservation Fee ✔ ✔ ✔ Closing Fee ✔ - ✔ Down Payment ✔ - ✔ Full Payment ✔ - ✔ Loan Difference ✔ - ✔ Monthly Amortization ✔ - ✔ Storage Fee ✔ - ✔ Transfer of Ownership ✔ - ✔ Transfer of Unit Fee ✔ - ✔ Real Property Tax* for Unit ✔ - ✔ Other Admin Fees ✔ - ✔ Notes: *RPT in common areas is paid directly to Condo Corp. Only billings that are ✔ Available - Not Available payable under DMCI Project Developers, Inc. are applicable for online payment transactions. A convenience fee will be charged by your chosen payment gateway for every transaction. Your payment is debited from your account in real-time. However, depending on the merchant’s policy, your payment will be reflected on the merchant’s record within 1-5 banking days from your transaction date. Online Banking and Online Payment Partners Note: Contact Customer Care to get your Remitter’s Code. -

November 4, 2019

November 4, 2019 Global equities advanced over the week amid strong corporate earnings from the US and reduced risk over a no-deal Brexit. Meanwhile, US Treasury yields, German bund yields, and Japanese bond yields fell on the back of uncertainties surrounding the US-China trade talks. Global oil prices decreased due to the rise in oil production from the US and OPEC. Global Equities US equities advanced week-on-week on the back of strong third quarter US corporate earnings and the policy rate cut by the Federal 2.0% Reserve last Wednesday. Among the companies whose reported earnings exceeded expectations include Apple, Starbucks, and 1.50% 1.44% 1.47% Facebook. The DJIA closed at 27,347.36 (+1.44% WoW), while the 1.32% S&P closed at 3,066.91 (+1.47% WoW). Asian equities went up despite resurfacing doubts regarding the US-China trade negotiations. The APEC Summit in Chile where 1.0% President Trump and President Xi were scheduled to meet for trade talks was cancelled due to transport protests. During the latter part of the week, optimism surrounded the market amid the anticipated rate 0.30% cut by the Fed and the creation of a potential bloc between ASEAN countries, Australia, Japan, New Zealand and South Korea. The 0.0% MSCI APxJ closed at 524.97 (+1.50% WoW). MSCI MSCI MSCI Asia DJIA S&P 500 European equities rose over the week as strong corporate earnings World Europe ex-Japan led by the automative sector and reduced risk of a no-deal Brexit lifted investors' sentiment. -

Uncovered Equity “Disparity” in Emerging Markets

City Research Online City, University of London Institutional Repository Citation: Fuertes, A-M. ORCID: 0000-0001-6468-9845, Phylaktis, K. ORCID: 0000-0001- 9392-1682 and Yan, C. (2019). Uncovered Equity “Disparity” in Emerging Markets. Journal of International Money and Finance, doi: 10.1016/j.jimonfin.2019.102066 This is the accepted version of the paper. This version of the publication may differ from the final published version. Permanent repository link: https://openaccess.city.ac.uk/id/eprint/22585/ Link to published version: http://dx.doi.org/10.1016/j.jimonfin.2019.102066 Copyright: City Research Online aims to make research outputs of City, University of London available to a wider audience. Copyright and Moral Rights remain with the author(s) and/or copyright holders. URLs from City Research Online may be freely distributed and linked to. Reuse: Copies of full items can be used for personal research or study, educational, or not-for-profit purposes without prior permission or charge. Provided that the authors, title and full bibliographic details are credited, a hyperlink and/or URL is given for the original metadata page and the content is not changed in any way. City Research Online: http://openaccess.city.ac.uk/ [email protected] Journal of International Money & Finance, forthcoming Uncovered Equity “Disparity” in Emerging Markets Ana-Maria Fuertes, Kate Phylaktis*, Cheng Yan 11th July 2019 The portfolio-rebalancing theory of Hau and Rey (2006) yields the uncovered equity parity (UEP) prediction that local-currency equity return appreciation is offset by currency depreciation. Vector autoregressive model estimation and tests for eight Asian emerging markets using daily data reveal instead a positive nexus between equity returns and currency returns. -

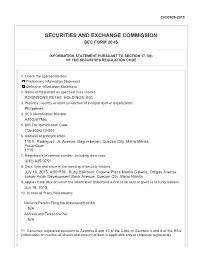

Securities and Exchange Commission Sec Form 20-Is

CR03839-2015 SECURITIES AND EXCHANGE COMMISSION SEC FORM 20-IS INFORMATION STATEMENT PURSUANT TO SECTION 17.1(b) OF THE SECURITIES REGULATION CODE 1. Check the appropriate box: Preliminary Information Statement Definitive Information Statement 2. Name of Registrant as specified in its charter ROBINSONS RETAIL HOLDINGS, INC. 3. Province, country or other jurisdiction of incorporation or organization Philippines 4. SEC Identification Number A200201756 5. BIR Tax Identification Code 216-303-212-000 6. Address of principal office 110 E. Rodriguez, Jr. Avenue, Bagumbayan, Quezon City, Metro Manila Postal Code 1110 7. Registrant's telephone number, including area code (632) 635-0751 8. Date, time and place of the meeting of security holders July 16, 2015, 4:00 P.M., Ruby Ballroom, Crowne Plaza Manila Galleria, Ortigas Avenue corner Asian Development Bank Avenue, Quezon City, Metro Manila 9. Approximate date on which the Information Statement is first to be sent or given to security holders Jun 18, 2015 10. In case of Proxy Solicitations: Name of Person Filing the Statement/Solicitor N/A Address and Telephone No. N/A 11. Securities registered pursuant to Sections 8 and 12 of the Code or Sections 4 and 8 of the RSA (information on number of shares and amount of debt is applicable only to corporate registrants): Title of Each Class Number of Shares of Common Stock Outstanding and Amount of Debt Outstanding Common shares 1,385,000,000 13. Are any or all of registrant's securities listed on a Stock Exchange? Yes No If yes, state the name of such stock exchange and the classes of securities listed therein: Robinsons Retail Holdings, Inc.’s common stock is listed on the Philippine Stock Exchange. -

CHAPTER 1 INTRODUCTION 1.1. Object Overview 1.1.1 Indonesia

CHAPTER 1 INTRODUCTION 1.1. Object Overview 1.1.1 Indonesia Composite Stock Price Index The Composite Stock Price Index is usually abbreviated as IHSG in English is also commonly called the Indonesia Composite Index, ICI, or IDX Composite. The definition of a Composite Stock Price Index (CSPI) or the meaning of JCI is one of several stock market indices (stock markets) used by the Indonesia Stock Exchange (BEI; formerly the Jakarta Stock Exchange (BEJ). The IHSG was first introduced on April 1, 1983, the function of the stock price index acts as an indicator that reflects the share price movements in the JSX in general (Oktarina, 2016). 1.1.2 Thailand Composite Stock Price Index The SET Index is a Thailand composite stock market index which is calculated from the prices of all common stocks (including unit trusts of property funds) on the main board of the Stock Exchange of Thailand (SET), except for stocks that have been suspended for more than one year. It is a market capitalization- weighted price Index which compares the current market value of all listed common shares with its value on the base date of April 30, 1975, which was when the Index was established and set at 100 point/ The SET Index calculation is adjusted in line with modifications in the values of stocks resulting from changes in the number of stocks due to various events, e.g., public offerings, exercised warrants, or conversions of preferred to common shares, in order to eliminate all effects other than price movements from the Index (Sutheebanjard and Premchaiswadi, 2010). -

7 Trends Shaping Philippine Real Estate in 2020

Report 7 Trends Shaping Philippine Real Estate santosknightfrank.com/research in 2020 he beginning of 2020 has been marked by a series of unexpected events that continue to affect the global economy. Despite the impact of COVID-19 and downturn in international stock markets, the Philippine real estate industry continues to have reasons to be optimistic, according to leading real estate service company, Santos Knight Frank. This is due to various drivers, including the roll out of REITs, continuous expansion of BPO companies, and strong consumer demand. (Since 1985, household consumption has accounted for 70-75% of Philippine GDP). Santos Knight Frank identifies the seven key trends that will be shaping the real estate industry this 2020. Media inquiries — Paolo Abellanosa Santos Knight Frank Research Reports are available [email protected] at santosknightfrank.com/market-reports 1. The year for REITs More property companies have expressed interest in Real Estate Investment Trusts (REITs) after regulators unveiled the revised rules in January. Property giant Ayala Land recently filed its application for its own REIT subsidiary, AREIT, while DoubleDragon Properties Corp is looking at raising PHP 11 billion annually over a six- year period via REITs. Companies such as Megaworld, SM Prime Holdings Inc., Robinsons Land, and Ortigas & Co. have also expressed interests on REITs. Asia-Pacific REIT markets Australia, Japan, and Singapore have all performed well in 2019, producing higher dividend yields than listed property companies, according to Santos Knight Frank. In addition to the impressive performance of dividend yields in the three markets, REITs in Hong Kong and Japan have delivered higher total returns versus listed property companies during the year. -

Durations of Trade in the Philippine Stock Market: an Application of the Markov-Switching Multi-Fractal Duration (Msmd) Model

DURATIONS OF TRADE IN THE PHILIPPINE STOCK MARKET: AN APPLICATION OF THE MARKOV-SWITCHING MULTI-FRACTAL DURATION (MSMD) MODEL Jennifer E. Hinlo1 and Agustina Tan-Cruz2 ABSTRACT This study examined the durations of trade in the Philippine Stock Market using the Markov Switching Multi-Fractal Duration (MSMD) Model using tick data from 20 frequently traded stocks in the Philippine Stock Market. Results revealed that higher duration results to lower trading intensity because of low information of traders about the stocks during the period. The lesser attention paid to the stock, the more likely that trade will not happen. The higher trading intensity is a result of shorter trade durations, this means that the interval from one trading transaction to another is smaller. The higher the trading intensity implies higher price impact of trades and faster price adjustment to new trade-related information. Information flow affects intensities but it does not trigger trading automatically because investors have limited attention, and they need to allocate attention to process all kinds of information before making a trading decision. Keywords: Markov Switching Multi-Fractal Duration (MSMD) Model, Philippine Stock Market, Trade Durations EXECUTIVE SUMMARY This study examined the durations of trade in the Philippine Stock Exchange (PSE) using the Markov Switching Multi-Fractal Duration (MSMD) Model using top twenty (20) randomly selected active firms listed in the PSE. Tick-by-tick intra-day trading of the equities in the PSE were used, from May 2 to 31, 2013, from 9:00 – 3:30pm (where the PSEI has recorded its 31st all-time high index). -

Asia Bond Monitor—November 2016 Was Prepared by the Asianbondsonline (ABO) Team

Asia Bond Monitor November 2016 This publication reviews recent developments in East Asian local currency bond markets along with the outlook, risks, and policy options. It covers the 10 members of the Association of Southeast Asian Nations plus the People’s Republic of China; Hong Kong, China; and the Republic of Korea. About the Asian Development Bank ADB’s vision is an Asia and Pacific region free of poverty. Its mission is to help its developing member countries reduce poverty and improve the quality of life of their people. Despite the region’s many successes, it remains home to half of the world’s extreme poor. ADB is committed to reducing poverty through inclusive economic growth, environmentally sustainable growth, and regional integration. Based in Manila, ADB is owned by 67 members, including 48 from the region. Its main instruments for helping its developing member countries are policy dialogue, loans, equity investments, guarantees, grants, and technical assistance. ASIA BOND MONITOR NOVEMBER 2016 ASIAN DEVELOPMENT BANK 6 ADB Avenue, Mandaluyong City 1550 Metro Manila, Philippines ASIAN DEVELOPMENT BANK www.adb.org The Asia Bond Monitor (ABM) is part of the Asian How to reach us: Bond Markets Initiative (ABMI), an ASEAN+3 initiative Asian Development Bank supported by the Asian Development Bank. This report Economic Research and Regional Cooperation is part of the implementation of a technical assistance Department project funded by the Investment Climate Facilitation 6 ADB Avenue, Mandaluyong City Fund of the Government of Japan under the Regional 1550 Metro Manila, Philippines Cooperation and Integration Financing Partnership Tel +63 2 632 6688 Facility.