SEC Form 17-A Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Organization Name Substation Class Region 111 Paseo De Roxas Condominium Association Inc

Organization Name Substation Class Region 111 Paseo De Roxas Condominium Association Inc. Zapote CCU LUZON 20-12 Property Holdings, Inc. Sucat CCU LUZON 20-34 Property Holdings, Inc. Sucat CCU LUZON 21st Century Mouldings Corp. Quezon CCU LUZON 21st Century Steel Mill, Inc Dolores CCU LUZON 3-J Plasticworld & Manufacturing Corporation Duhat CCU LUZON 557 Feather Meal Corporation Concepcion CCU LUZON 6776 Ayala Avenue Condominium Corporation Sucat CCU LUZON A.D. Gothong Manufacturing Corporation Mandaue GIS CCU VISAYAS Abenson Inc. Zapote CCU LUZON ABS-CBN Corporation Araneta CCU LUZON AcBel Polytech Philippines, Inc. Calauan CCU LUZON Acesite (Phils.) Hotel Corporation Paco CCU LUZON ACI, Inc. (Cyberpark 2) Araneta CCU LUZON Adebe Realty Company, Inc. Zapote CCU LUZON Adriatico Consortium, Inc. Paco CCU LUZON Aeonprime Land Development Corp. (Block 45-Aeon Center) Sucat CCU LUZON Aeonprime Land Development Corporation Zapote CCU LUZON Agripacific Corporation Amadeo CCU LUZON Aichi Forge Philippines, Inc. Sta.Rosa CCU LUZON Aikawa Philippines Inc. Calauan CCU LUZON Air Liquide Philippines, Inc. Sucat CCU LUZON Air Liquide Pipeline Utilities Services, Inc. BIñan CCU LUZON Air Liquide Pipeline Utilities Services., Inc. Calung Calung CCU VISAYAS Ajinomoto Philippines Flavor Food Inc. Duhat CCU LUZON Alabang Commercial Corporation Zapote CCU LUZON ALASKA Milk Corporation Biñan CCU LUZON Albay Agro-Industrial Development Corporation Tiwi A DCU LUZON Ali Makati Hotel Property, Inc. Sucat CCU LUZON ALI-CII Development Corporation Zapote CCU LUZON Allegro MicroSystems Philippines,Inc. Sucat CCU LUZON AllHome Corp. (AllHome Libis) Dolores CCU LUZON Allied Packaging Corporation Duhat CCU LUZON Alpha Supreme Corp. Duhat CCU LUZON Alphaland Corporation (Alphaland Southgate Tower, Inc.) Zapote CCU LUZON Alphaland Makati Place, Inc. -

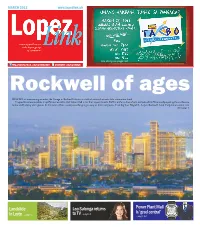

Rockwell of Ages DESPITE Its Unassuming Moniker, the Garage in Rockwell Center Is a Hub of Activity, but Not of the Automotive Kind

MARCH 2013 www.lopezlink.ph See story on page 10 http://www.facebook.com/lopezlinkonline www.twitter.com/lopezlinkph Rockwell of ages DESPITE its unassuming moniker, the Garage in Rockwell Center is a hub of activity, but not of the automotive kind. Prospective sales executives in spiffy business attire wait to be called in for their appointments. Staff in uniform dress shorts and polo shirts flit around preparing the conference rooms and looking after guests. In the inner offices, twentysomethings type away at their computers. Even big boss Miguel L. Lopez, Rockwell Land Corporation senior vice Turn to page 6 Landslide Lea Salonga returns Power Plant Mall is ‘grad central’ …page 3 to TV …page 4 in Leyte …page 12 Lopezlink March 2013 BIZ NEWS NEWS Lopezlink March 2013 At the Pinoy Media Congress Landslide in Leyte FPH to redeem and Students urged to serve, ABS-CBN: GMA’S libel declare cash dividend love country; EL launches case has no basis EDC continues search on preferred shares ABS-CBN Corporation reiterat- THE board of directors of First shares starting on the fifth an- book of speeches ed its stand that the nine-year-old Philippine Holdings Corpora- niversary of the issue date. In his keynote address, EL3 libel case filed by GMA Network tion (FPH) has approved the Additionally, the board also against it has no basis. for missing workers company’s option to redeem approved payment of a cash ABS-CBN chairman Eugenio said the media’s role is to “serve ABS-CBN chairman Eu- A landslide possibly triggered while 10 were taken to the The workers were hired by families of the casualties and all of its 43,000,000 series B dividend on the series B preferred Lopez III (leftmost) with the people no matter what the genio Lopez III (EL3) and preferred shares. -

DINING MERCHANT PARTICIPATING BRANCHE/S OFFER Wooden Horse Steakhouse G/F Molito Complex, Madrigal Ave., Cor Alabang Zapote Road

DINING MERCHANT PARTICIPATING BRANCHE/S OFFER G/F Molito Complex, Madrigal Ave., cor Alabang Zapote Road Wooden Horse Steakhouse 10% OFF on total bill Muntinlupa City SM Megamall - 2/F Mega Atruim, Julia Vargas Ave., Wack Wack 15% OFF on total bill Kichitora Mandaluyong BCG - 3/F BGC Central Sqaure, BGC Taguig City Greenbelt 3 - 3/F Greenbelt 3, Makati City 15% OFF on total bill Motorino BGC - G/F Netlima Bldg. BGC Taguig City Tappella Greenbelt 5 - G/4 Greenbelt 5 Ayala Center Makati City 10% OFF on total bill La Cabrera Glorieta Complex - 6750 Building Glorieta Complex Makati City 15% OFF on total bill Nikkei No. 111 Frabelle Bldg. Rada Street Legaspi Village Makati City 15% OFF on total bill Alimall – Araneta Centre Cubao Quezon City Alabang – Festival Mall Alabang Antipolo – Sumulong Hills Antipolo Antipolo – Robinsons Place Antipolo Baguio – SM City Baguio Cebu – SM City Cebu Congressional – Barrington Place, Congressional Ave. QC Katipunan – Katipunan Ave, Loyola Heights QC Manila – SM City Manila The Old Spaghetti House 10% OFF on total bill Market! Market! – Bonifacio Global City, Taguig Marikina – SM City Marikina – Midtown – Robinsons Place Ermita Midtown MOA – SM Mall of Asia Otis – Robinsons Place Otis Pioneer – Robinsons Place Forum SM The Block – SM City North Edsa The Block Sta Rosa – Solenad 3, Sta Rosa Laguna Valero – Paseo De Roxas Valero Street Makati Antipolo – Robinsons Place Antipolo MOA – SM City Mall of Asia Market! Market! – Bonifacio Global City, Taguig The Shrimp Shack 10% OFF on total bill Midtown – Robinsons Place Ermita Midtown SM The Block – SM North Edsa The Block Pioneer – Robinsons Place Forum Pioneer Greenhills San Juan Greenbelt 5 Diliman Torch Trinoma Mall 10% OFF on total bill BGC Alabang Olympia Venice Grand Canal Mall, McKinley Hill, Taguig Rice & Dough 10% OFF on total bill Eastwood Mall Ayala Fairview Terraces Gateway Mall Robinsons Galleria Rockwell SM City Marikina SM City North EDSA- The Block Burgoo SM Mall of Asia 10% OFF on total bill SM South Mall Solenad 3, Nuvali, Sta. -

20 October 2010 Philippine Stock Exchange Disclosures Department 3/F, Tower One and Exchange Plaza Ayala Triangle, Ayala Avenue

20 October 2010 Philippine Stock Exchange Disclosures Department 3/F, Tower One and Exchange Plaza Ayala Triangle, Ayala Avenue Makati City Attention : Ms. Janet Encarnacion Head – Disclosures Department Re : ROXAS AND COMPANY, INC. (Formerly CADP GROUP CORPORATION) ‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐‐ Gentlemen: We respectfully submit the Annual List of Stockholders of Roxas and Company, Inc. (formerly CADP Group Corporation and herein referred to as the “Company”) as of Record Date, 15 October 2010, prepared by Unionbank Stock Transfer Unit, the Company’s stock transfer agent. Very truly yours, FRITZIE P. TANGKIA‐FABRICANTE Asst. Corporate Secretary/Compliance Officer 7th Floor Cacho Gonzales Building 101 Aguirre Street, Legaspi Village 1229 Makati City Tel No.: (02) 810‐8901 www.roxascompany.com.ph ROXAS AND COMPANY, INC. List of Stockholders as of Record Date 15 October 2010 SN STOCKHOLDERS NAME ADDRESS SHARES 10082856 A. SORIANO CORPORATION SORIANO BUILDING, MAKATI CITY 2,710 10082014 ABAD AURORA C/O BANK OF ASIA, DASMARINAS MANILA 40 10071504 ABAQUIN GIL 3666-C GEN. A. LUNA ST. BANOKAL, MAKATI, MM 402 10071514 ABAQUIN LOURDES M. #6 RIZAL ST., AYALA HEIGHTS QUEZON CITY 742 10079516 ABAT NESTOR A. PASIG BOULEVARD,BARRIO PINEDA PASIG CITY 538 10082024 ABAYA AMELIA R. 153 LT., ARTIAGA, SAN JUAN, MM 3,340 10082034 ABAYA MELCHOR R. 153 LT., ARTIAGA, SAN JUAN, MM 1,560 10082044 ABAYA VICENTE R. 153 LT., ARTIAGA, SAN JUAN, MM 3,340 C/O CADP CG BUILDING, 101 AGUIRRE STREET 10079637 ABELEDA ANASTACIO 18 LEGASPI VILLAGE, MAKATI CITY C/O CADP CG BUILDING, 101 AGUIRRE STREET 10079647 ABELLERA ERNESTO 179 LEGASPI VILLAGE, MAKATI CITY C/O CADP CG BUILDING, 101 AGUIRRE STREET 10079657 ABELLERA SUSAN C. -

Standards Monitoring and Enforcement Division List Of

DEPARTMENT OF TOURISM OFFICE OF TOURISM STANDARDS AND REGULATION - STANDARDS MONITORING AND ENFORCEMENT DIVISION LIST OF OPERATIONAL HOTELS AS OF MARCH 26, 2020, 09:00 AM NATIONAL CAPITAL REGION COUNT NAME OF ESTABLISHMENT ADDRESS 1 Ascott Bonifacio Global City 5th ave. Corner 28th Street, BGC, Taguig 2 Ascott Makati Glorietta Ayala Center, San Lorenzo Village, Makati City 3 Cirque Serviced Residences Bagumbayan, Quezon City 4 Citadines Bay City Manila Diosdado Macapagal Blvd. cor. Coral Way, Pasay City 5 Citadines Millenium Ortigas 11 ORTIGAS AVE. ORTIGAS CENTER, PASIG CITY 6 Citadines Salcedo Makati 148 Valero St. Salcedo Village, Makati city Asean Avenue corner Roxas Boulevard, Entertainment City, 7 City of Dreams Manila Paranaque #61 Scout Tobias cor Scout Rallos sts., Brgy. Laging Handa, Quezon 8 Cocoon Boutique Hotel City 9 Connector Hostel 8459 Kalayaan Ave. cor. Don Pedro St., POblacion, Makati 10 Conrad Manila Seaside Boulevard cor. Coral Way MOA complex, Pasay City 11 Cross Roads Hostel Manila 76 Mariveles Hills, Mandaluyong City Corner Asian Development Bank, Ortigas Avenue, Ortigas Center, 12 Crowne Plaza Manila Galleria Quezon City 13 Discovery Primea 6749 Ayala Avenue, Makati City 14 Domestic Guest House Salem Complex Domestic Road, Pasay City 15 Dusit Thani Manila 1223 Epifanio de los Santos Ave, Makati City 16 Eastwood Richmonde Hotel 17 Orchard Road, Eastwood City, Quezon City 17 EDSA Shangri-La 1 Garden Way, Ortigas Center, Mandaluyong City 18 Go Hotels Mandaluyong Robinsons Cybergate Plaza, Pioneer St., Mandaluyong 19 Go Hotels Ortigas Robinsons Cyberspace Alpha, Garnet Road., San Antonio, Pasig City 20 Gran Prix Manila Hotel 1325 A Mabini St., Ermita, Manila 21 Herald Suites 2168 Chino Roces Ave. -

Extinguishment of Agency General Condition Revocation Withdrawal Of

Extinguishment of Agency General condition Revocation Withdrawal of agent Death of the Principal Death of the Agent CASES Republic of the Philippines SUPREME COURT Manila FIRST DIVISION G.R. No. L-36585 July 16, 1984 MARIANO DIOLOSA and ALEGRIA VILLANUEVA-DIOLOSA, petitioners, vs. THE HON. COURT OF APPEALS, and QUIRINO BATERNA (As owner and proprietor of QUIN BATERNA REALTY), respondents. Enrique L. Soriano for petitioners. Domingo Laurea for private respondent. RELOVA, J.: Appeal by certiorari from a decision of the then Court of Appeals ordering herein petitioners to pay private respondent "the sum of P10,000.00 as damages and the sum of P2,000.00 as attorney's fees, and the costs." This case originated in the then Court of First Instance of Iloilo where private respondents instituted a case of recovery of unpaid commission against petitioners over some of the lots subject of an agency agreement that were not sold. Said complaint, docketed as Civil Case No. 7864 and entitled: "Quirino Baterna vs. Mariano Diolosa and Alegria Villanueva-Diolosa", was dismissed by the trial court after hearing. Thereafter, private respondent elevated the case to respondent court whose decision is the subject of the present petition. The parties — petitioners and respondents-agree on the findings of facts made by respondent court which are based largely on the pre-trial order of the trial court, as follows: PRE-TRIAL ORDER When this case was called for a pre-trial conference today, the plaintiff, assisted by Atty. Domingo Laurea, appeared and the defendants, assisted by Atty. Enrique Soriano, also appeared. A. -

Diversification Strategies of Large Business Groups in the Philippines

Philippine Management Review 2013, Vol. 20, 65‐82. Diversification Strategies of Large Business Groups in the Philippines Ben Paul B. Gutierrez and Rafael A. Rodriguez* University of the Philippines, College of Business Administration, Diliman, Quezon City 1101, Philippines This paper describes the diversification strategies of 11 major Philippine business groups. First, it reviews the benefits and drawbacks of related and unrelated diversification from the literature. Then, it describes the forms of diversification being pursued by some of the large Philippine business groups. The paper ends with possible explanations for the patterns of diversification observed in these Philippine business groups and identifies directions for future research. Keywords: related diversification, unrelated diversification, Philippine business groups 1 Introduction This paper will describe the recent diversification strategies of 11 business groups in the Philippines. There are various definitions of business groups but in this paper, these are clusters of legally distinct firms with a managerial relationship, usually by virtue of common ownership. The focus on business groups rather than on individual firms has to do with the way that business firms in the Philippines are organized and managed. Businesses that are controlled and managed by essentially the same set of principal owners are often organized as separate corporations, not as separate divisions within the same firm, as is often the case in American corporations like General Electric, Procter and Gamble, or General Motors (Echanis, 2009). Moreover, studies on emerging markets have pointed out that business groups often occupy dominant positions in the business landscape in markets like India, Korea, Indonesia, Thailand, and the Philippines (Khanna & Palepu, 1997; Khanna & Yafeh, 2007). -

An All-Time Record 97 Buildings of 200 Meters Or Higher Completed In

CTBUH Year in Review: Tall Trends All building data, images and drawings can be found at end of 2014, and Forecasts for 2015 Click on building names to be taken to the Skyscraper Center An All-Time Record 97 Buildings of 200 Meters or Higher Completed in 2014 Report by Daniel Safarik and Antony Wood, CTBUH Research by Marty Carver and Marshall Gerometta, CTBUH 2014 showed further shifts towards Asia, and also surprising developments in building 60 58 14,000 13,549 2014 Completions: 200m+ Buildings by Country functions and structural materials. Note: One tall building 200m+ in height was also completed during 13,000 2014 in these countries: Chile, Kuwait, Malaysia, Singapore, South Korea, 50 Taiwan, United Kingdom, Vietnam 60 58 2014 Completions: 200m+ Buildings by Countr5,00y 0 14,000 60 13,54958 14,000 13,549 2014 Completions: 200m+ Buildings by Country Executive Summary 40 Note: One tall building 200m+ in height was also completed during ) Note: One tall building 200m+ in height was also completed during 13,000 60 58 13,0014,000 2014 in these countries: Chile, Kuwait, Malaysia, Singapore, South Korea, (m 13,549 2014 in these Completions: countries: Chile, Kuwait, 200m+ Malaysia, BuildingsSingapore, South byKorea, C ountry 50 Total Number (Total = 97) 4,000 s 50 Taiwan,Taiwan, United United Kingdom, Kingdom, Vietnam Vietnam Note: One tall building 200m+ in height was also completed during ht er 13,000 Sum of He2014 igin theseht scountries: (Tot alChile, = Kuwait, 23,333 Malaysia, m) Singapore, South Korea, 5,000 mb 30 50 5,000 The Council -

List of World's Tallest Buildings in the World

Height Height Rank Building City Country Floors Built (m) (ft) 1 Burj Khalifa Dubai UAE 828 m 2,717 ft 163 2010 2 Shanghai Tower Shanghai China 632 m 2,073 ft 121 2014 Saudi 3 Makkah Royal Clock Tower Hotel Mecca 601 m 1,971 ft 120 2012 Arabia 4 One World Trade Center New York City USA 541.3 m 1,776 ft 104 2013 5 Taipei 101 Taipei Taiwan 509 m 1,670 ft 101 2004 6 Shanghai World Financial Center Shanghai China 492 m 1,614 ft 101 2008 7 International Commerce Centre Hong Kong Hong Kong 484 m 1,588 ft 118 2010 8 Petronas Tower 1 Kuala Lumpur Malaysia 452 m 1,483 ft 88 1998 8 Petronas Tower 2 Kuala Lumpur Malaysia 452 m 1,483 ft 88 1998 10 Zifeng Tower Nanjing China 450 m 1,476 ft 89 2010 11 Willis Tower (Formerly Sears Tower) Chicago USA 442 m 1,450 ft 108 1973 12 Kingkey 100 Shenzhen China 442 m 1,449 ft 100 2011 13 Guangzhou International Finance Center Guangzhou China 440 m 1,440 ft 103 2010 14 Dream Dubai Marina Dubai UAE 432 m 1,417 ft 101 2014 15 Trump International Hotel and Tower Chicago USA 423 m 1,389 ft 98 2009 16 Jin Mao Tower Shanghai China 421 m 1,380 ft 88 1999 17 Princess Tower Dubai UAE 414 m 1,358 ft 101 2012 18 Al Hamra Firdous Tower Kuwait City Kuwait 413 m 1,354 ft 77 2011 19 2 International Finance Centre Hong Kong Hong Kong 412 m 1,352 ft 88 2003 20 23 Marina Dubai UAE 395 m 1,296 ft 89 2012 21 CITIC Plaza Guangzhou China 391 m 1,283 ft 80 1997 22 Shun Hing Square Shenzhen China 384 m 1,260 ft 69 1996 23 Central Market Project Abu Dhabi UAE 381 m 1,251 ft 88 2012 24 Empire State Building New York City USA 381 m 1,250 -

Private Sector-Led Vertical Urbanism in the Philippines 3

ctbuh.org/papers Title: Private Sector-Led Vertical Urbanism in the Philippines Author: Felino Palafox, Jr., Principal, Palafox Associates Subject: Urban Design Keywords: Development Vertical Urbanism Publication Date: 2012 Original Publication: CTBUH 2012 9th World Congress, Shanghai Paper Type: 1. Book chapter/Part chapter 2. Journal paper 3. Conference proceeding 4. Unpublished conference paper 5. Magazine article 6. Unpublished © Council on Tall Buildings and Urban Habitat / Felino Palafox, Jr. Private Sector-Led Vertical Urbanism in the Philippines 私营化推动菲律宾城市垂直化发展 Abstract The paper demonstrates the capacity of the private sector in initiating vertical urbanism and urban development in the Philippines. Private developers have led the successful development of the Makati Central Business District and the Rockwell Center, where the tallest buildings in the country are located. The paper hopes to draw inspiration from the urban planning done by private developers in Makati and Rockwell Center as a basis for other private developers to follow suit to create a more connected, accessible, and safe environment for mixed-income Felino Palafox and cross-generational residents. It is also aimed at creating a balance between high-density, high-rise developments and the surrounding urban sprawl by developing the latter into higher Felino Palafox density neighborhoods: from traffic and parking generators, public transit systems, to a more Palafox Associates convenient commute route for employees and executives. 11/F 6782 Ayala Avenue Makati City Keywords: Philippines, Vertical Urbanism, Cities, Urban Development, Private Sector Phillippines 1226 tel (电话): ++632.812.12.54 fax (传真): +632.893.91.97 摘要 email (电子邮箱): [email protected] www.palafoxassociates.com 本篇论文着重阐述菲律宾私营企业在发起竖向都市设计和都市开发中的作用,私营开发 Felino Palafox is an International Associate of the 商主导了马卡蒂市中心商业区(CBD)和Rockwell中心的开发,菲律宾的最高大厦就坐 American Institute of Architects, member of the Urban 落在这里。本文希望通过描述马卡蒂市CBD和Rockwell中心的开发,启发更多的私营开 Land Institute, American Planning Association, and the U.S. -

Business in Harmony Cebu Exchange

BUSINESS IN HARMONY CEBU EXCHANGE www.arthaland.com +63 917 77 ARTHA (27842) | [email protected] Visit our showroom on-site along Salinas Drive, Lahug, Cebu City CLIENT PROSPECTUS HLURB LTS No. 032788 CLIENT PROSPECTUS Salinas Drive, Lahug, Cebu City. Issued on 11 September 2017. Completion on 30 June 2021. Project Developer: Cebu Lavana Land Corporation. Project Manager: Arthaland Corporation. HLURB CVR AA-2019/01-550. Harmony… The beautiful interweaving of different elements into a singular experience. An experience so diverse, yet utterly cohesive; complete and perfectly balanced. Welcome to the Cebu Exchange. A holistic, sustainable, and highly connected work environment where harmony is not just a way of life, but a way of doing business. THE PHILIPPINE MARKET: A LANDSCAPE OF POSSIBILITIES*: AN OVERTURE • GROWTH: 6.7% GDP • OFW REMITTANCES: US$30 billion p.a. • BPO REVENUE: US$23 billion • 10-YEAR BOND YIELD: 6.3% Ranking among the top growth performers of Asia • POPULATION: 102 million in 2017*, the Philippines has cemented its position (67% below 35 years old) • MANILA at the top of the charts as one of the most • INFRASTRUCTURE SPENDING: US$160 billion (from 2016 to 2022) attractive economies in the entire region; • 3.8% Managed Inflation as of Q1 2018 attracting investors across the globe with more exciting and lucrative investment opportunities over other neighboring countries. CEBU CITY • DAVAO CITY *Sources: World Bank Group, 2017 Bangko Sentral ng Pilipinas, 2018 Contact Center Association of the Philippines, 2018 World Government Bonds, 2018 Philippine Statistics Authority, 2018 Department of Budget and Management, 2018 CEBU CITY: A DYNAMIC DESTINATION Known for its powdery white sand beaches, delicious local fare and artisan crafts, Cebu, the Queen City of the South, has always been one of the most important and influential economic centers in the Philippines and is quickly emerging as one of the most prominent IT-BPM destinations in the world. -

Power Mac in Store Promo Terms and Conditions List of Branches

Power Mac in store Promo Terms and Conditions 1. The Promo is open to all primary and supplementary HSBC Credit Cardholders (Cardholders), whose cards are issued in the Philippines, are active and in good credit standing. Corporate and debit cardholders are excluded from this promotion. For the avoidance of doubt, a card is in good credit standing if there is no reason for HSBC to restrain, suspend, cancel, withdraw or terminate the card pursuant to the HSBC Card Terms and Conditions as well as Legal and Regulatory Compliance Policy considerations. 2. Promo offer is valid until September 30, 2020 3. Under this exclusive offer, cardholders can avail of 0% installment for 36 mos in-store on the following items: a. MacBook Air 2017 b. iPhone XS c. iPhone XS Max d. new iPhone SE 4. Cardholders can avail of 0% interest on installment for 36 mos with the following minimum purchase requirement: Minimum Tenor transaction amount 36 months Php18,000 5. Cardholders must settle payment with their HSBC Credit Card to enjoy the offer. 6. The offer cannot be used in conjunction with any other discounts, promotions, discounted items and fixed-price items (unless specified). 7. The offer cannot be exchanged for cash or other products. 8. HSBC is not a supplier of the products and services for the Programme and accepts no liability for the quality of goods and services provided by the Merchant involved in this promotion. 9. All offers are bound by the terms and conditions stipulated by HSBC and the Merchant 10. In case of dispute with respect to the cardholder’s eligibility, coverage of dates, fulfillment, etc., HSBC’s decision shall prevail.