Written Evidence Submitted by Professor Stuart Cole CBE (RIW0002)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

People, Places and Policy

People, Places and Policy Set within the context of UK devolution and constitutional change, People, Places and Policy offers important and interesting insights into ‘place-making’ and ‘locality-making’ in contemporary Wales. Combining policy research with policy-maker and stakeholder interviews at various spatial scales (local, regional, national), it examines the historical processes and working practices that have produced the complex political geography of Wales. This book looks at the economic, social and political geographies of Wales, which in the context of devolution and public service governance are hotly debated. It offers a novel ‘new localities’ theoretical framework for capturing the dynamics of locality-making, to go beyond the obsession with boundaries and coterminous geog- raphies expressed by policy-makers and politicians. Three localities – Heads of the Valleys (north of Cardiff), central and west coast regions (Ceredigion, Pembrokeshire and the former district of Montgomeryshire in Powys) and the A55 corridor (from Wrexham to Holyhead) – are discussed in detail to illustrate this and also reveal the geographical tensions of devolution in contemporary Wales. This book is an original statement on the making of contemporary Wales from the Wales Institute of Social and Economic Research, Data and Methods (WISERD) researchers. It deploys a novel ‘new localities’ theoretical framework and innovative mapping techniques to represent spatial patterns in data. This allows the timely uncovering of both unbounded and fuzzy relational policy geographies, and the more bounded administrative concerns, which come together to produce and reproduce over time Wales’ regional geography. The Open Access version of this book, available at www.tandfebooks.com, has been made available under a Creative Commons Attribution-Non Commercial-No Derivatives 3.0 license. -

A New Wales Transport Strategy Consultation Response

Llwybr Newydd – a new Wales transport strategy Consultation response Introduction Transport Focus is the independent consumer watchdog promoting the interests of rail passengers throughout Great Britain; bus, coach and tram passengers across England, outside London; and users of the Strategic Road Network in England. We have a Board Member for Wales appointed by the Minister for Economy, Transport and North Wales. Transport Focus welcomes this consultation. Our response is informed both by our extensive evidence base and insight gathered through the engagement of our work in Wales. Consultation questions Do you agree with our long-term vision? The vision applies across all of Wales and is equally relevant and inclusive to both people and place, needing to recognise the differences between cities, towns and rural areas. We agree that the transport system needs to be accessible, addressing barriers and sustainable. However we would want to see the transport system defining a joined-up network enabling door-to-door journeys. Our work with bus passengers1 shows that services going to more places is their second highest priority and the top priority for non- users and both sets agree that a good bus network is important to the local area (93 per cent of users and 82 per cent of non-users agree). Rail passengers2 also want this network to be effective, placing good connections in the top half of their priorities for improvement; but the National Rail Passenger Survey3 (NRPS) shows the most recent satisfaction with transport connections for Wales and Borders is only 65 per cent. Achieving the vision will be dependent on the delivery, monitoring and evaluation of the priorities, outcomes, policies and enablers which underpin the vision. -

Low Emission Buses – Includes AQ

Lower Carbon and Cleaner Air: Opportunities for Buses Low Emission Bus Workshop Cardiff Principality Stadium, 19th July Connect | Collaborate | Influence Daniel Hayes Project Manager Low Carbon Vehicle Partnership LowCVP: A unique public-private membership organisation, building evidence and creating robust policies and innovation in the UK Government & Public Bodies Environmental & Academia Fuel Suppliers Fleet Technology Operators Suppliers Automotive Manufacturers And Many More… Low Carbon Vehicle Partnership LowCVP Activity & Policy Cycle - Robust Research, Policy and Information The LowCVP exists to Roadmaps and accelerate shift to low research carbon vehicles and fuels and stimulate UK business opportunities Identify Barriers and Market information/ Opportunities dissemination Understand and Investigate Disseminate and Stimulate Accelerate Build Market Understanding Influence Policy Develop technology Implementation Key: LowCVP activity Develop tools/policies Incubate and Influence Member organisations The Low Carbon Vehicle Partnership Current State of Play in Wales In 2016/17… • 1,500 registered PSV buses in Wales (-25% from 2006/7) • 2,100 citizens/bus, GB average is 1,600 citizens/bus • 100 million passenger journeys (-16% from 2006/7) • 32 journeys per head, GB average is 77 journeys per head • 45% of all bus journeys are concessionary fares (34% GB average) • 1 car for every two people in Wales … only NI has more cars/head Plenty of Opportunities for Growth of Bus Market in Wales! Long term transport strategy must include modal shift Bus strategy must include reduction of emissions (CO2, NOx)… The Low Carbon Vehicle Partnership National UK Bus Policy Evolution Development of evidence based bus policy over the last decade to reduce emissions… 2007-08 2009-15 2015-16 2016-2018 £30m Green Bus Defining an Fund £3m SGBF 7 Definition of a Creation of a OLEV Ultra Low Low Carbon LCEB BSOG LCEB Low Emission B.E.A.R. -

Flying Into the Future Infrastructure for Business 2012 #4 Flying Into the Future

Infrastructure for Business Flying into the Future Infrastructure for Business 2012 #4 Flying into the Future Flying into the Future têáííÉå=Äó=`çêáå=q~óäçêI=pÉåáçê=bÅçåçãáÅ=^ÇîáëÉê=~í=íÜÉ=fça aÉÅÉãÄÉê=OMNO P Infrastructure for Business 2012 #4 Contents EXECUTIVE SUMMARY ________________________________________ 5 1. GRowInG AVIATIon SUSTAInABlY ______________________ 27 2. ThE FoUR CRUnChES ______________________________ 35 3. ThE BUSInESS VIEw oF AIRpoRT CApACITY ______________ 55 4. A lonG-TERM plAn FoR GRowTh ____________________ 69 Q Flying into the Future Executive summary l Aviation provides significant benefits to the economy, and as the high growth markets continue to power ahead, flying will become even more important. “A holistic plan is nearly two thirds of IoD members think that direct flights to the high growth countries will be important to their own business over the next decade. needed to improve l Aviation is bad for the global and local environment, but quieter and cleaner aviation in the UK. ” aircraft and improved operational and ground procedures can allow aviation to grow in a sustainable way. l The UK faces four related crunches – hub capacity now; overall capacity in the South East by 2030; excessive taxation; and an unwelcoming visa and border set-up – reducing the UK’s connectivity and making it more difficult and more expensive to get here. l This report sets out a holistic aviation plan, with 25 recommendations to address six key areas: − Making the best use of existing capacity in the short term; − Making decisions about where new runways should be built as soon as possible, so they can open in the medium term; − Ensuring good surface access and integration with the wider transport network, in particular planning rail services together with airport capacity, not separately; − Dealing with noise and other local environment impacts; − Not raising taxes any further; − Improving the visa regime and operations at the UK border. -

Paris: Trams Key to Multi-Modal Success

THE INTERNATIONAL LIGHT RAIL MAGAZINE www.lrta.org www.tautonline.com JANUARY 2016 NO. 937 PARIS: TRAMS KEY TO MULTI-MODAL SUCCESS Innsbruck tramway enjoys upgrades and expansion Bombardier sells rail division stake Brussels: EUR5.2bn investment plan First UK Citylink tram-train arrives ISSN 1460-8324 £4.25 Sound Transit Swift Rail 01 Seattle ‘goes large’ A new approach for with light rail plans UK suburban lines 9 771460 832043 For booking and sponsorship opportunities please call +44 (0) 1733 367600 or visit www.mainspring.co.uk 27-28 July 2016 Conference Aston, Birmingham, UK The 11th Annual UK Light Rail Conference and exhibition brings together over 250 decision-makers for two days of open debate covering all aspects of light rail operations and development. Delegates can explore the latest industry innovation within the event’s exhibition area and examine LRT’s role in alleviating congestion in our towns and cities and its potential for driving economic growth. VVoices from the industry… “On behalf of UKTram specifically “We are really pleased to have and the industry as a whole I send “Thank you for a brilliant welcomed the conference to the my sincere thanks for such a great conference. The dinner was really city and to help to grow it over the event. Everything about it oozed enjoyable and I just wanted to thank last two years. It’s been a pleasure quality. I think that such an event you and your team for all your hard to partner with you and the team, shows any doubters that light rail work in making the event a success. -

Cardiff Auto Receivables Investor Report July 2021

Classification: Public# CARDIFF AUTO RECEIVABLES SECURITISATION 2019-1 plc INVESTOR REPORT JULY 2021 Overview Reporting Date 12 August 2021 Collection Period 22 June 2021 - 21 July 2021 Interest Payment Date 16 August 2021 Deal Overview / Trigger Events Deal Name: Cardiff Auto Receivables Securitisation 2019-1 Issuer: Cardiff Auto Receivables Securitisation 2019-1 plc 1 Bartholomew Lane, London,EC2N 2AX, United Kingdom Contact Details Name Email Address Gavin Parker [email protected] 10 Gresham Street, London, EC2V 7AE Chris Morteo [email protected] 1st Floor Alexander House, Pier Head Street, Cardiff Bay, CF10 4PB Jacqui Keith [email protected] 1st Floor Alexander House, Pier Head Street, Cardiff Bay, CF10 4PB Stephen Davies [email protected] 1st Floor Alexander House, Pier Head Street, Cardiff Bay, CF10 4PB Nelson Lirio [email protected] 1st Floor Alexander House, Pier Head Street, Cardiff Bay, CF10 4PB Key Parties/Details Rating (if applicable) Role LEI Number Name Address DBRS / S&P Originator 2138008UXJZAK9L5PE86 Black Horse Limited N/A 25 Gresham Street, London, EC2V 7HN, United Kingdom Issuer 21380029WJFUM99THL82 Cardiff Auto Receivables Securitisation 2019-1 plc N/A 1 Bartholomew Lane, London,EC2N 2AX, United Kingdom Seller 2138008UXJZAK9L5PE86 Black Horse Limited N/A 25 Gresham Street, London, EC2V 7HN, United Kingdom Servicer 2138008UXJZAK9L5PE86 Black Horse Limited N/A 25 Gresham Street, London, EC2V 7HN, United Kingdom Cash Manager 2138008UXJZAK9L5PE86 Black Horse -

The Future Development of Transport for Wales

National Assembly for Wales Economy, Infrastructure and Skills Committee The Future Development of Transport for Wales May 2019 www.assembly.wales The National Assembly for Wales is the democratically elected body that represents the interests of Wales and its people, makes laws for Wales, agrees Welsh taxes and holds the Welsh Government to account. An electronic copy of this document can be found on the National Assembly website: www.assembly.wales/SeneddEIS Copies of this document can also be obtained in accessible formats including Braille, large print, audio or hard copy from: Economy, Infrastructure and Skills Committee National Assembly for Wales Cardiff Bay CF99 1NA Tel: 0300 200 6565 Email: [email protected] Twitter: @SeneddEIS © National Assembly for Wales Commission Copyright 2019 The text of this document may be reproduced free of charge in any format or medium providing that it is reproduced accurately and not used in a misleading or derogatory context. The material must be acknowledged as copyright of the National Assembly for Wales Commission and the title of the document specified. National Assembly for Wales Economy, Infrastructure and Skills Committee The Future Development of Transport for Wales May 2019 www.assembly.wales About the Committee The Committee was established on 28 June 2016. Its remit can be found at: www.assembly.wales/SeneddEIS Committee Chair: Russell George AM Welsh Conservatives Montgomeryshire Current Committee membership: Hefin David AM Vikki Howells AM Welsh Labour Welsh Labour Caerphilly Cynon Valley Mark Reckless AM David J Rowlands AM Welsh Conservative Group UKIP Wales South Wales East South Wales East Jack Sargeant AM Bethan Sayed AM Welsh Labour Plaid Cymru Alyn and Deeside South Wales West Joyce Watson AM Welsh Labour Mid and West Wales The Future Development of Transport for Wales Contents Chair’s foreword ..................................................................................................... -

Economic Significance of Tourism and of Major Events: Analysis, Context and Policy Calvin Jones ’ UMI Number: U206081

Economic significance of tourism and of major events: analysis, context and policy Calvin Jones ’ UMI Number: U206081 All rights reserved INFORMATION TO ALL USERS The quality of this reproduction is dependent upon the quality of the copy submitted. In the unlikely event that the author did not send a complete manuscript and there are missing pages, these will be noted. Also, if material had to be removed, a note will indicate the deletion. Dissertation Publishing UMI U206081 Published by ProQuest LLC 2013. Copyright in the Dissertation held by the Author. Microform Edition © ProQuest LLC. All rights reserved. This work is protected against unauthorized copying under Title 17, United States Code. ProQuest LLC 789 East Eisenhower Parkway P.O. Box 1346 Ann Arbor, Ml 48106-1346 Ca r d if f UNIVFRSITY PR I i YSG OF CA‘ RD W BINDING SERVICES Tel +44 (0)29 2087 4949 Fax +44 (0)29 20371921 e-mail [email protected] Sum m ary The papers presented in this Thesis focus upon the analysis of recreational and sporting activity as economic phenomena. They link the analysis of tourism and sport to wider public policy and economic development debates, applying economic analytical techniques to sport and leisure in a novel manner and charting the development of new tools which enhance our understanding of the economic contribution of these important activities. A number of the papers contained here focus on the extent to which sporting and leisure activity can further regional and national governments' aspirations for economic development, and at what cost. Two of the papers refine economic impact methodologies to better account for the impacts of discrete sporting and cultural events or facilities, using a high level of primary input data, and placing of the results firmly within the local economic development context. -

Coridor-Yr-M4-O-Amgylch-Casnewydd

PROSIECT CORIDOR YR M4 O AMGYLCH CASNEWYDD THE M4 CORRIDOR AROUND NEWPORT PROJECT Malpas Llandifog/ Twneli Caerllion/ Caerleon Llandevaud B Brynglas/ 4 A 2 3 NCN 4 4 Newidiadau Arfaethedig i 6 9 6 Brynglas 44 7 Drefniant Mynediad/ A N tunnels C Proposed Access Changes 48 N Pontymister A 4 (! M4 C25/ J25 6 0m M4 C24/ J24 M4 C26/ J26 2 p h 4 h (! (! p 0 Llanfarthin/ Sir Fynwy/ / 0m 4 u A th 6 70 M4 Llanmartin Monmouthshire ar m Pr sb d ph Ex ese Gorsaf y Ty-Du/ do ifie isti nn ild ss h ng ol i Rogerstone A la p M4 'w A i'w ec 0m to ild Station ol R 7 Sain Silian/ be do nn be Re sba Saint-y-brid/ e to St. Julians cla rth res 4 ss u/ St Brides P M 6 Underwood ifi 9 ed 4 ng 5 Ardal Gadwraeth B M ti 4 Netherwent 4 is 5 x B Llanfihangel Rogiet/ 9 E 7 Tanbont 1 23 Llanfihangel Rogiet B4 'St Brides Road' Tanbont Conservation Area t/ Underbridge en Gwasanaethau 'Rockfield Lane' w ow Gorsaf Casnewydd/ Trosbont -G st Underbridge as p Traffordd/ I G he Newport Station C 4 'Knollbury Lane' o N Motorway T Overbridge N C nol/ C N Services M4 C23/ sen N Cyngor Dinas Casnewydd M48 Pre 4 Llanwern J23/ M48 48 Wilcrick sting M 45 Exi B42 Newport City Council Darperir troedffordd/llwybr beiciau ar hyd Newport Road/ M4 C27/ J27 M4 C23A/ J23A Llanfihangel Casnewydd/ Footpath/ Cycleway Provided Along Newport Road (! Gorsaf Pheilffordd Cyffordd Twnnel Hafren/ A (! 468 Ty-Du/ Parcio a Theithio Arfaethedig Trosbont Rogiet/ Severn Tunnel Junction Railway Station Newport B4245 Grorsaf Llanwern/ Trefesgob/ 'Newport Road' Rogiet Rogerstone 4 Proposed Llanwern Overbridge -

Rail Station Usage in Wales, 2018-19

Rail station usage in Wales, 2018-19 19 February 2020 SB 5/2020 About this bulletin Summary This bulletin reports on There was a 9.4 per cent increase in the number of station entries and exits the usage of rail stations in Wales in 2018-19 compared with the previous year, the largest year on in Wales. Information year percentage increase since 2007-08. (Table 1). covers stations in Wales from 2004-05 to 2018-19 A number of factors are likely to have contributed to this increase. During this and the UK for 2018-19. period the Wales and Borders rail franchise changed from Arriva Trains The bulletin is based on Wales to Transport for Wales (TfW), although TfW did not make any the annual station usage significant timetable changes until after 2018-19. report published by the Most of the largest increases in 2018-19 occurred in South East Wales, Office of Rail and Road especially on the City Line in Cardiff, and at stations on the Valleys Line close (ORR). This report to or in Cardiff. Between the year ending March 2018 and March 2019, the includes a spreadsheet level of employment in Cardiff increased by over 13,000 people. which gives estimated The number of station entries and exits in Wales has risen every year since station entries and station 2004-05, and by 75 per cent over that period. exits based on ticket sales for each station on Cardiff Central remains the busiest station in Wales with 25 per cent of all the UK rail network. -

Location, Location, Location

Focus: Luxury brands w Location, location, room for value throughout the chain... I think ARM creation of a safe social network for children. ose is probably the keystone in that process.” companies flourish because of Tech City itself. e e dotcom bubble would burst in the early 00s, community acts as an extended support group. Its location but ARM, with its strategy of forging ahead through job fairs draw thousands of hopefuls and its pubs In our ongoing series on reputation, Brittany partnerships and communications, avoided the act as real-life chatrooms for the countless businesses Golob charts the development of the British disaster that befell its contemporaries. “Have many finding their feet in tech entrepreneurship. technology industry of them sold up and become satellites of mainly US Places like Stockholm and Berlin have established firms? Yes, but that’s true elsewhere too,” Cellan- technology bases, Gaza and Glasgow boast a startup Jones adds. “It has a positive side – small UK tech culture and Kenya will develop the so-called Silicon arold Wilson stood in front of the Labour start-ups have been quick to grasp the need to go Savannah by 2030. What makes London different, Party Conference at Scarborough in global and often that means they need access to the however is something it has boasted for centuries 1963 and declared that Britain needed a kind of capital only available in the US.” – the financial industry. Both geographically and Hrevolution. Revolution in the name of capitalism, As the 20th century faded into the 21st, Britain economically, the tech startups that crowd the streets of democracy and of science, a revolution that began developing a tech industry that seems of Shoreditch and the country’s signature financial would forge a new Britain. -

Newsletter of Railfuture in Wales

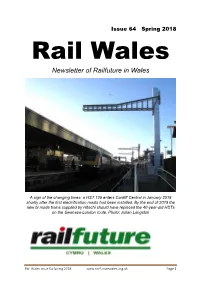

Issue 64 Spring 2018 Rail Wales Newsletter of Railfuture in Wales A sign of the changing times: a HST 125 enters Cardiff Central in January 2018 shortly after the first electrification masts had been installed. By the end of 2018 the new bi mode trains supplied by Hitachi should have replaced the 40-year-old HSTs on the Swansea-London route. Photo: Julian Langston Rail Wales issue 64 Spring 2018 www.railfuturewales.org.uk Page 1 WELCOME Rail Wales is published every six months and looking back at events since the last issue, it sometimes seems that the fast pace of significant news would require a weekly issue to keep Railfuture members up to date with the ever-evolving rail scene. Needless to say, the ongoing saga of the letting of the Wales and Borders franchise provides the main focus of attention. Shortly before the last issue of Rail Wales appeared, Arriva announced that it was withdrawing from the bidding process. This reduced the bidders to three. However, the withdrawal of a second bidder in February 2018 was not as a result of that company (Abellio) deciding to walk away but as a result of the financial collapse of its civil engineering partner, Carillion. The two bidders still standing are Keolis and MTR. With only two companies now competing, this weakens the hand of Transport for Wales (the organisation set up by the Welsh Government to undertake the selection of the new operator) to obtain the best outcome. It is hoped that the ongoing discussions, which are nearing conclusion, will result in a franchise award which provides existing and potential new rail users in Wales and adjacent areas of England with a markedly improved service in terms of service frequency, reliability, comfort and value for money.