Melco Crown Entertainment Ltd. NASDAQ: MLCO

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

City of Dreams Resort and Casino, Grand Hyatt, Hard Rock and Crown Towers Hotels

City of Dreams Resort and Casino, Grand Hyatt, Hard Rock and Crown Towers Hotels The City of Dreams Resort includes four state-of-the-art casino hotel towers with 1,622 guest rooms: the 5-star, 970-key Grand Hyatt Hotel, the 5-star, 286-key Crown Towers; and the 4-star, 366-key Hard Rock Hotel. The development is designed to accommodate conventions and conferences. Its three-floor podium includes many large ballrooms, banquet halls, meeting rooms and business facilities; a mega-casino and over 200 shopping venues and hotel guest amenities. The development has 420,000 SF (39,000 m2) of gaming space with 550 gaming tables and 1500 gaming machines, over 20 restaurants and bars, including one of the largest in the city. Included within the property is 175,000 SF (16,300 m2) of high-end retail space spread across two levels. City of Dreams was designed to the highest quality in international standards, making it the premier development and destination in the Cotai Strip of Macau and the region for leisure and entertainment. Location: Macau, China Type: Hospitality, Master Planning, Mixed-Use, Retail / Entertainment, Waterfront Services: Master Planning, Architecture, Interiors, Landscape Size: 4,107,000 sf / 382,000 m2 Awards: * Society of American Registered Architects (SARA) | Design Award of Recognition * TTG China Travel Awards | “Best Luxury Hotel in Macau” for Grand Hyatt Hotel * World Luxury Spa Awards | “Best Luxury Hotel Spa” for Crown Towers * TTG Travel Awards | Best Integrated Resort * Forbes Travel Guide | Five-Star Hotel Award * International Gaming Awards | Best Casino Interior Design * International Gaming Awards | Best Casino Operator for the Asia Pacific Region * International Gaming Awards | Best Casino VIP Room * International Property Awards | Best Leisure Development in Asia Pacific * International Property Awards | Best Leisure Development in China * Macau Environmental Protection Bureau with the collaboration of Macao Government Tourist Office | Bronze Award 2010 Macao Green Hotel Award * SGS | Indoor Environmental Quality (IEQ) Certification. -

Las Vegas Sands Corp. Annual Report 2018

Las Vegas Sands Corp. Annual Report 2018 Form 10-K (NYSE:LVS) Published: February 23rd, 2018 PDF generated by stocklight.com UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-K x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2017 or ¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission file number 001-32373 LAS VEGAS SANDS CORP. (Exact name of registrant as specified in its charter) Nevada 27-0099920 (State or other jurisdiction of (IRS Employer incorporation or organization) Identification No.) 3355 Las Vegas Boulevard South Las Vegas, Nevada 89109 (Address of principal executive offices) (Zip Code) Registrant's telephone number, including area code: (702) 414-1000 Securities registered pursuant to Section 12(b) of the Act: Title of Each Class Name of Each Exchange on Which Registered Common Stock ($0.001 par value) New York Stock Exchange Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (2) has been subject to such filing requirements for the past 90 days. -

Marina Bay Sands

3Q19 Earnings Call Presentation October 23, 2019 Forward Looking Statements This presentation contains forward-looking statements made pursuant to the Safe Harbor Provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements involve a number of risks, uncertainties or other factors beyond the company’s control, which may cause material differences in actual results, performance or other expectations. These factors include, but are not limited to, general economic conditions, competition, new development, construction and ventures, substantial leverage and debt service, fluctuations in currency exchange rates and interest rates, government regulation, tax law changes and the impact of U.S. tax reform, legalization of gaming, natural or man- made disasters, terrorist acts or war, outbreaks of infectious diseases, insurance, gaming promoters, risks relating to our gaming licenses and subconcession, infrastructure in Macao, our subsidiaries’ ability to make distribution payments to us, and other factors detailed in the reports filed by Las Vegas Sands with the Securities and Exchange Commission. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date thereof. Las Vegas Sands assumes no obligation to update such information. Within this presentation, the company may make reference to certain non-GAAP financial measures including “adjusted net income,” “adjusted earnings per diluted share,” and “consolidated adjusted property EBITDA,” which have directly comparable financial measures presented in accordance with accounting principles generally accepted in the United States of America ("GAAP"), along with “adjusted property EBITDA margin,” “hold-normalized adjusted property EBITDA,” “hold-normalized adjusted property EBITDA margin,” “hold-normalized adjusted net income,” and “hold-normalized adjusted earnings per diluted share,” as well as presenting these or other items on a constant currency basis. -

About Wynn Resorts

About Wynn Resorts About Wynn Resorts Stephen A. Wynn, the founder of Wynn Resorts, Limited, is the preeminent designer, developer and operator of Integrated Resorts globally. Wynn Resorts owns and operates two Integrated Resorts in Las Vegas, Nevada and three in the Macau Special Administrative Region of the People’s Republic of China (“Macau”). The Wynn development team envisions, designs, and builds boldly conceived Integrated Resorts that set progressively higher standards for quality, guest service and entertainment and that transformed their markets from “gaming-only” locales to diversified global tourist destinations. Wynn Integrated Resorts seamlessly integrate sophisticated architecture, luxurious interior design, and a diverse selection of amenities, including fine-dining restaurants, premium-retail offerings, a full range of 24-hour games, convention facilities, and live-performance venues. The result: unique experiences for guests of the highest quality. Guided by the simple truth that, “Only people can make people happy,” Wynn employees are devoted to delivering the Wynn promise of always exceeding guest expectations. For 40 years, resorts led by the Wynn development team have been the employer of choice in their markets. An Unparalleled Record of Market Transformation As Chairman of the Board, President and Chief Executive Officer of Mirage Resorts, Incorporated, Mr. Wynn opened The Mirage, Las Vegas’ first true Integrated Resort, in 1989. The Mirage, at that time the most expensive casino in the history of Las Vegas, was an instant success, breaking all Las Vegas records for profitability and for the first time generated more non-gaming revenue than gaming revenue for a Las Vegas resort. The Mirage not only established the concept of an Integrated Resort but also broadened the global appeal of Las Vegas, triggering an immediate $12 billion city-wide investment boom that made Las Vegas the number one tourist destination in the world. -

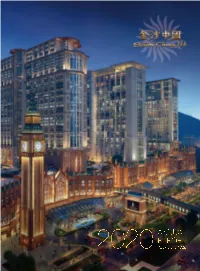

2020 Annual Report

Stock Code: 1928 and Note Stock Codes: 5140, 5141, 5142, 5725, 5727, 5733, 40246, 40247, 40584, 40585 www.sandschina.com From Luxury Duty Free Shopping, Exciting Entertainment and Fabulous Dining to World-Class Hotel Suites and MICE, Come and Discover Everything at Sands China. SANDS CHINA LTD. CONTENTS 1. OVERVIEW 4 1.1 Financial Results Summary 4 1.2 Highlights of 2020 5 1.3 Directors and Senior Management 11 2. BUSINESS REVIEW 18 2.1 Chairman’s Statement 18 2.2 Business Overview and Outlook 20 2.3 Our Properties 26 2.4 Management Discussion and Analysis 33 2.5 Priority Risk Factors 47 2.6 Stakeholder Information 59 3. CORPORATE GOVERNANCE 66 REPORT 3.1 Introduction 66 3.2 Corporate Governance Code Compliance 66 3.3 Board Governance Structure 67 3.4 The Board 68 3.5 Audit Committee 74 3.6 Remuneration Committee 76 3.7 Nomination Committee 78 3.8 Capex Committee 81 3.9 Risk Management and Internal Control 82 3.10 Shareholders 87 3.11 Compliance Disclosures and Other Matters 90 3.12 Directors’ Report 92 4. FINANCIAL STATEMENTS 113 4.1 Independent Auditor’s Report 113 4.2 Financial Statements 117 4.3 Notes to the Consolidated Financial Statements 123 4.4 Financial Summary 193 5. CORPORATE INFORMATION 194 6. CONTACT US 195 7. GLOSSARY 196 In case of any inconsistency between the English version and the Chinese version of this Annual Report, the English version shall prevail. SANDS CHINA LTD. 1.1 FINANCIAL HIGHLIGHTS 2 ANNUAL REPORT 2020 SANDS CHINA LTD. 1.1 FINANCIAL HIGHLIGHTS our Luxurious Hotel Rooms and Suites await you. -

Presentación De Powerpoint

Nuestro grupo en Europa y Asia desde 2014 Empresas locales con oficina y almacén LMA Spanish TFA Asturias LMA Asturias CM Pan Pacific Vitality Consulting Consulting Hong Kong International Limited SL Sarl Ltd Limited SL Singapur Suiza España España Hong Kong Macao Servicio logística & distribución Hong Kong, Macao & Singapur Servicio de exportación con Servicio de importación con Servicio de distribución y licencia licencia entrega • Grupaje mercancía • Colectar documentación • Organizar el almacenaje • Booking transporte • Organizar llegada envió • Recepción de pedidos • Preparación • Preparar y presentar • Preparación mercancía documentación productos documentos importación • Booking transporte local • Contacto con aduanas • Asistir a la inspección de • Envió mercancía a cliente • Solicitar y emitir la mercancía en aduanas • Alabaran de entrega certificado sanitario • Retirar la mercancía • Facturación cliente CEXGAM • Envió y almacenaje de la • Envió mercancía a destino mercancía en almacén Nuestra experiencia Exportación y importación productos gourmet y chocolates Chef Miguel Sierra • Chocolates, bombones y varios productos de repostería Chef Miguel Sierra • Productos lácteos (leche, quesos, mantequilla) y embutidos de Asturias • Miel, mermelada, aceite de oliva virgen extra, vinagre, jamón ibérico de España • Bebidas alcohólicas, vino de España, champagne de Francia Acciones comerciales, presentación Chefs, servicios de compras y distribuidores en Hong Kong, Macau, Singapur (mas de 40 viajes a Asia) • Hong Kong : Intercontinental -

Casino Boss Francis Lui Won Big in Macau, but His Next

IT DIDN’T QUITE WORK OUT THAT WAY. A partnership with an American casino operator fi zzled, so after running a couple of card clubs in other peo- ple’s hotels, his family’s irm, Galaxy Entertainment Group, built one of Macau’s new glittering casinos BY RUSSELL PEARLMAN in 2006. That and building two other incredibly successful casinos in Macau transformed Lui, 62, from the ambitious son of a wealthy Hong Kong con- struction magnate into one of the world’s richest men. In turn, Lui helped transform Macau—which over the past several hundred years has been, in turn, a waystation for refugees fl eeing the Mongols, a bustling Portuguese-run trading colony, a haven for CASINO BOSS early-20th-century gangsters and a neutral port in the storm of World War II—into its latest incarnation: the world’s biggest betting parlor. Gamblers drop more than FRANCIS LUI WON BIG $28 billion a year betting at Macau’s casinos. Las Vegas doesn’t even get one-quarter of that. But instead of sitting back and enjoying Macau’s current form, he’s at the forefront of trying to reinvent the area yet IN MACAU, BUT HIS again. He’s making a multibillion-dollar bet that Macau’s next reinvention won’t involve much gambling at all. Over the next few years, Galaxy wants to add NEXT BET BARELY 10.7 million square feet of space to its existing Galaxy Macau resort, nearly doubling its size. It potentially will include a convention center, a concert venue with INVOLVES GAMBLING. -

Annual Report 2017 1

CONTENTS Key Performance Indicators 14 Corporate Profile 16 Corporate Structure 17 Chairman & CEO’s Statement 18 Management Discussion and Analysis 20 Management Profile 34 Environmental, Social and Governance Report 38 Corporate Governance Report 54 Report of the Directors 63 Independent Auditor’s Report 93 Consolidated Statement of Profit or Loss and Other Comprehensive Income 98 Consolidated Statement of Financial Position 100 Consolidated Statement of Changes in Equity 102 Consolidated Statement of Cash Flows 105 Notes to Consolidated Financial Statements 107 Five Years Financial Summary 207 Corporate Information 208 Melco International Development Limited | Annual Report 2017 1 A TRUE LANDMARK FOR ALL OF MACAU Constantly upping its ante in the Macau integrated resort scene, our flagship property City of Dreams is heralding the start of a new era of hospitality sophistication in Macau. With the launch of the Forbes 5-Star hotel Nüwa, the rebranding and redevelopment of The Countdown, and the eagerly awaited opening of Morpheus, the cornerstone of the final phase of development for City of Dreams, the property sets a new benchmark for luxury and entertainment in Macau. A SPARKLING ENTERTAINMENT WONDERLAND Combining electrifying entertainment with Forbes 5-Star hotel, Michelin-starred dining and designer brand shopping, the cinematically-themed resort Studio City takes thrilling entertainment to a whole new level in Asia. Studio City is further embarking on a series of property upgrades to refine the entertainment offerings and improve accessibility into the resort, striving for bringing the biggest, boldest and most exciting attractions to Macau. THE WINNING HAND IN THE PHILIPPINE ENTERTAINMENT SCENE Featuring 3 luxurious hotel brands, various premium dining outlets and one-of-a-kind entertainment, the dynamic and innovative resort City of Dreams Manila is playing a key role in strengthening the depth and diversity of the Philippines’ leisure, business and tourism offerings. -

Macau's Trade with the Portuguese Speaking World Paul B

Journal of Global Initiatives: Policy, Pedagogy, Perspective Volume 11 Number 1 Examining Complex Relationships in the Article 5 Portuguese Speaking World October 2016 Macau's Trade with the Portuguese Speaking World Paul B. Spooner Macau University of Science & Technology Follow this and additional works at: https://digitalcommons.kennesaw.edu/jgi Part of the Growth and Development Commons, Peace and Conflict Studies Commons, and the Political Economy Commons This work is licensed under a Creative Commons Attribution 4.0 License. Recommended Citation Spooner, Paul B. (2016) "Macau's Trade with the Portuguese Speaking World," Journal of Global Initiatives: Policy, Pedagogy, Perspective: Vol. 11 : No. 1 , Article 5. Available at: https://digitalcommons.kennesaw.edu/jgi/vol11/iss1/5 This Article is brought to you for free and open access by DigitalCommons@Kennesaw State University. It has been accepted for inclusion in Journal of Global Initiatives: Policy, Pedagogy, Perspective by an authorized editor of DigitalCommons@Kennesaw State University. For more information, please contact [email protected]. Paul B. Spooner Journal of Global Initiatives Vol. 11, No. 1, 2016, pp. 137-162. Macau’s Trade With the Portuguese Speaking World Paul B. Spooner Macau University of Science & Technology Abstract Macau has boomed over the last decade as its gaming industry has provided the massive Chinese economy with the only legal casino gambling services in the nation. But, recent Chinese political changes have resulted in a sharp downturn in Macau’s gambling revenues despite a major expansion of its gaming facilities. This may negatively impact efforts to promote a relationship between Macau and the Portuguese Speaking World. -

Melco Presents Celine Dion in Concert for the First Time in Cyprus

Press Release [For Immediate Publication] 18 October 2019 Melco presents Celine Dion in concert for the first time in Cyprus Demonstrating Melco’s commitment to bringing world-class entertainment to the region as the event’s sole presenter Melco announces it will soon present Cyprus’ first ever Celine Dion concert as the event’s main sponsor, demonstrating the Company’s commitment to bringing world-class entertainment to the region. The award-winning French-Canadian singer’s “Celine Dion Courage World Tour, Cyprus, presented by Melco Resorts and Entertainment” will take place at GSP Stadium, Nicosia on 2 August 2020. Mr. Craig Ballantyne, Property President of City of Dreams Mediterranean and Cyprus Casinos “C2”, said: “Melco has long been dedicated to presenting world-class entertainment offerings that go beyond gaming for the premium travel segment. Achieving this through continuous collaborations with outstanding partners, we are pleased to support Celine Dion in concert for the first time in Cyprus. In alignment with the mission of the forthcoming City of Dreams Mediterranean, the first and largest Integrated Casino Resort (ICR) in Europe, to attract and excite customers from all over the world, we anticipate the concert will enthuse and draw fans from around the region, for the chance to enjoy the singer’s thrilling performance which will further enhance the local tourism industry’s appeal. We look forward to presenting many more world-class experiences and attractions when the ICR’s doors officially open in 2021.” “Courage World Tour” is the fourteenth concert tour by Celine Dion and the artist’s first world tour in over a decade. -

Oct 8, 2019 Melco Chairman & CEO Visits Zhuhai with Team of Senior

FOR IMMEDIATE RELEASE Melco Chairman & CEO visits Zhuhai with team of senior executives Part of ‘Splendors of China’ initiative, visit is the first in a series to develop in-depth understanding of the Greater Bay Area for management team Macau, Tuesday, October 8, 2019 – Melco Resorts & Entertainment Chairman & Chief Executive Officer Mr. Lawrence Ho recently paid a visit to the city of Zhuhai with a team of the company’s senior executives as part of the Melco initiative ‘Splendors of China’. The visit is the first in a series to enhance and strengthen Melco management team’s understanding of the Greater Bay Area, with further trips being planned to Shenzhen and Guangzhou in the coming months. Mr. Lawrence Ho and the team of twelve senior executives from Melco met with representatives from the Liaison Office of the Central People’s Government in the Macao SAR (Liaison Office), including Mr. Zuo Xianghua, Director of Economic Affairs Department; and Mr. Yang Yi, Deputy Director of Economic Affairs Department, as well as Zhuhai officials including Ms. Zou Hua, Director of Zhuhai Municipal Affairs Bureau of Taiwan, Hong Kong and Macao; Mr. Huang Yuan Peng; Deputy Director of Zhuhai Municipal Affairs Bureau of Taiwan, Hong Kong and Macao; Mr. Xie Liang, Director of Zhuhai Foreign Investment Service Center; and Ms. Su Cuizhu, Divison Chief of Municipal Affairs Bureau of Taiwan, Hong Kong and Macao; and was introduced to Zhuhai’s unique positioning within the Greater Bay Area and its relationship with Macau. The Melco team visited the Hengqin integrated tourism and entertainment project Novotown, visiting Lionsgate Entertainment World and National Geographic Ultimate Explorer within the complex. -

Wynn Resorts Annual Report 2020

Wynn Resorts Annual Report 2020 Form 10-K (NASDAQ:WYNN) Published: February 28th, 2020 PDF generated by stocklight.com UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2019 OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period to Commission File No. 000-50028 WYNN RESORTS, LIMITED (Exact name of registrant as specified in its charter) Nevada 46-0484987 (I.R.S. Employer (State or other jurisdiction of incorporation or organization) Identification No.) 3131 Las Vegas Boulevard South - Las Vegas, Nevada 89109 (Address of principal executive offices) (Zip Code) (702) 770-7555 (Registrant's telephone number, including area code) Securities registered pursuant to Section 12(b) of the Act: Title of Each Class Trading Symbol Name of Each Exchange on Which Registered Common Stock, par value $0.01 WYNN Nasdaq Global Select Market Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒ Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.