Bwin.Party Digital Entertainment Annual Report & Accounts 2012

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

How We Learned to Cheat in Online Poker: a Study in Software Security

How we Learned to Cheat in Online Poker: A Study in Software Security Brad Arkin, Frank Hill, Scott Marks, Matt Schmid, Thomas John Walls, and Gary McGraw Reliable Software Technologies Software Security Group Poker is card game that many people around the world enjoy. Poker is played at kitchen tables, in casinos and cardrooms, and, recently, on the Web. A few of us here at Reliable Software Technologies (http://www.rstcorp.com) play poker. Since many of us spend a good amount of time on-line, it was only a matter of time before some of us put the two interests together. This is the story of how our interests in online poker and software security mixed to create a spectacular security exploit. The PlanetPoker Internet cardroom (http://www.planetpoker.com) offers real-time Texas Hold'em games against other people on the Web for real money. Being software professionals who help companies deliver secure, reliable, and robust software, we were curious about the software behind the online game. How did it work? Was it fair? An examination of the FAQs at PlanetPoker, including the shuffling algorithm (which was ironically published to help demonstrate the game's integrity), was enough to start our analysis wheels rolling. As soon as we saw the shuffling algorithm, we began to suspect there might be a problem. A little investigation proved this intuition correct. The Game In Texas Hold'em, each player is dealt two cards (called the pocket cards). The initial deal is followed by a round of betting. After the first round of betting, all remaining cards are dealt face up and are shared by all players. -

Hearing on the Report of the Chief Justice of Gibraltar

[2009] UKPC 43 Privy Council No 0016 of 2009 HEARING ON THE REPORT OF THE CHIEF JUSTICE OF GIBRALTAR REFERRAL UNDER SECTION 4 OF THE JUDICIAL COMMITTEE ACT 1833 before Lord Phillips Lord Hope Lord Rodger Lady Hale Lord Brown Lord Judge Lord Clarke ADVICE DELIVERED ON 12 November 2009 Heard on 15,16, 17, and 18 June 2009 Chief Justice of Gibraltar Governor of Gibraltar Michael Beloff QC Timothy Otty QC Paul Stanley (Instructed by Clifford (Instructed by Charles Chance LLP) Gomez & Co and Carter Ruck) Government of Gibraltar James Eadie QC (Instructed by R J M Garcia) LORD PHILLIPS : 1. The task of the Committee is to advise Her Majesty whether The Hon. Mr Justice Schofield, Chief Justice of Gibraltar, should be removed from office by reason of inability to discharge the functions of his office or for misbehaviour. The independence of the judiciary requires that a judge should never be removed without good cause and that the question of removal be determined by an appropriate independent and impartial tribunal. This principle applies with particular force where the judge in question is a Chief Justice. In this case the latter requirement has been abundantly satisfied both by the composition of the Tribunal that conducted the initial enquiry into the relevant facts and by the composition of this Committee. This is the advice of the majority of the Committee, namely, Lord Phillips, Lord Brown, Lord Judge and Lord Clarke. Security of tenure of judicial office under the Constitution 2. Gibraltar has two senior judges, the Chief Justice and a second Puisne Judge. -

Testimony Opposing House Bill 1389 Mark Jorritsma, Executive Director Family Policy Alliance of North Dakota March 15, 2021

Testimony Opposing House Bill 1389 Mark Jorritsma, Executive Director Family Policy Alliance of North Dakota March 15, 2021 Good morning Madam Chair Bell and honorable members of the Senate Finance and Taxation Committee. My name is Mark Jorritsma and I am the Executive Director of Family Policy Alliance of North Dakota. We respectfully request that you render a “DO NOT PASS” on House Bill 1389. Online poker is not gambling. This bill says so itself, and more importantly, in August of 2012, a federal judge in New York ruled in US v. Dicristina that internet poker was not gambling.1 So that is settled. But is it really? While online poker does not appear to meet the legal definition of gambling, consider these facts. • In the same ruling referenced above, Judge Weinstein acknowledged that state courts that have ruled on the issue are divided as to whether poker constitutes a game of skill, a game of chance, or a mixture of the two.2 • Online poker, which allows players to play multiple tables at once, resulting in almost constant action, is a fertile ground for developing addiction. Some sites allow a player to open as many as eight tables at a time, and the speed of play is three times as fast as live poker.3 • …online poker has a rather addictive nature that often affects younger generations. College age students are especially apt to developing online poker addictions.4 • Deposit options will vary depending on the state, but the most popular method is to play poker for money with credit card. -

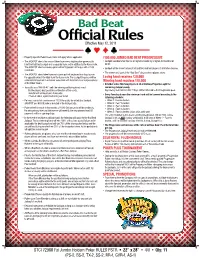

Official Rules Effective May 12, 2011

Bad Beat Official Rules Effective May 12, 2011 • Property Specific Poker Room Rules will apply where applicable. $100,000 JUMBO BAD BEAT PROGRESSIVE • The JACKPOT rake is the amount taken from every eligible poker game pot to • Jackpot awarded when four 6s or higher is beaten by a higher 4-Of-A-Kind or fund the Bad Beat Jackpot and is separate from and in addition to the House rake. better. $ The JACKPOT rake from every game will be 10 percent of the pot with a 1.00 • Jackpot will be shared amongst all qualified Hold’em players at all Station Casinos. maximum. • The winner and loser of the “Bad Beat” also receive a players share. • The JACKPOT rakes taken from each game pot will be placed in a drop box on the opposite side of the table from the house rake. The Jackpot Drop box will be Losing hand receives $30,000 collected and counted in a manner consistent with the internal control procedures Winning hand receives $20,000 of the Poker Room. • All other active Hold'em players at all of Stations Properties split the • To qualify as a “BAD BEAT” both the winning and losing hands must: remaining Jackpot evenly. Be the player’s best possible combination of five cards. Any money not claimed after 7 Days will be returned to the Progressive pool. Include both of the player’s hole cards: • Every Tuesday at noon the minimum hand will be lowered according to the If four of a kind, a pair must be in your hand. -

Part 05.Indd

PART MISCELLANEOUS 5 TOPICS Awards and Honours Y NATIONAL AWARDS NATIONAL COMMUNAL Mohd. Hanif Khan Shastri and the HARMONY AWARDS 2009 Center for Human Rights and Social (announced in January 2010) Welfare, Rajasthan MOORTI DEVI AWARD Union law Minister Verrappa Moily KOYA NATIONAL JOURNALISM A G Noorani and NDTV Group AWARD 2009 Editor Barkha Dutt. LAL BAHADUR SHASTRI Sunil Mittal AWARD 2009 KALINGA PRIZE (UNESCO’S) Renowned scientist Yash Pal jointly with Prof Trinh Xuan Thuan of Vietnam RAJIV GANDHI NATIONAL GAIL (India) for the large scale QUALITY AWARD manufacturing industries category OLOF PLAME PRIZE 2009 Carsten Jensen NAYUDAMMA AWARD 2009 V. K. Saraswat MALCOLM ADISESHIAH Dr C.P. Chandrasekhar of Centre AWARD 2009 for Economic Studies and Planning, School of Social Sciences, Jawaharlal Nehru University, New Delhi. INDU SHARMA KATHA SAMMAN Mr Mohan Rana and Mr Bhagwan AWARD 2009 Dass Morwal PHALKE RATAN AWARD 2009 Actor Manoj Kumar SHANTI SWARUP BHATNAGAR Charusita Chakravarti – IIT Delhi, AWARDS 2008-2009 Santosh G. Honavar – L.V. Prasad Eye Institute; S.K. Satheesh –Indian Institute of Science; Amitabh Joshi and Bhaskar Shah – Biological Science; Giridhar Madras and Jayant Ramaswamy Harsita – Eengineering Science; R. Gopakumar and A. Dhar- Physical Science; Narayanswamy Jayraman – Chemical Science, and Verapally Suresh – Mathematical Science. NATIONAL MINORITY RIGHTS MM Tirmizi, advocate – Gujarat AWARD 2009 High Court 55th Filmfare Awards Best Actor (Male) Amitabh Bachchan–Paa; (Female) Vidya Balan–Paa Best Film 3 Idiots; Best Director Rajkumar Hirani–3 Idiots; Best Story Abhijat Joshi, Rajkumar Hirani–3 Idiots Best Actor in a Supporting Role (Male) Boman Irani–3 Idiots; (Female) Kalki Koechlin–Dev D Best Screenplay Rajkumar Hirani, Vidhu Vinod Chopra, Abhijat Joshi–3 Idiots; Best Choreography Bosco-Caesar–Chor Bazaari Love Aaj Kal Best Dialogue Rajkumar Hirani, Vidhu Vinod Chopra–3 idiots Best Cinematography Rajeev Rai–Dev D Life- time Achievement Award Shashi Kapoor–Khayyam R D Burman Music Award Amit Tivedi. -

Site Review: Innovation

Site Review: Website: www.americascardroom.eu Americas Cardroom has brought the excitement of online poker back to the USA! Americas Cardroom has grown rapidly over the past several years, bringing players back to the glory days of online poker in the US through unique incentives and promotions. They are the only US facing site to offer The Million Dollar Sunday $1,000,000 GTD poker tournaments while hosting a weekly progressive rake race for both cash game and Sit & Go players. Americas Cardroom is truly living up to its name as being the online poker site that US players can trust. As the flagship skin of the Winning Poker Network, Americas Cardroom has already grown into one of the top communities for US poker players thanks to its no-nonsense deposits, quick payouts and high tournament guarantees. Reasons to join America’s Cardroom - Rated fastest Payouts in the industry - US players Accepted - WSOP Qualifiers - Million Dollar Sundays $1,000,000 GTD Tournaments - The only site with weekly progressive rake races for sit & go’s and cash games - Now accepts Bitcoin for Deposits and Withdrawals Poker Network: THE WINNING POKER NETWORK (WPN) Innovation $1,000,000 GTD Million Dollar Sundays -Americas Cardroom brought back the glory days of poker to the US market in 2015 with $1,000,000 GTD Million Dollar Sunday tournaments. More are on tap for 2016 with the next one scheduled for April 24th at 4pm ET. They are the only US facing network to offer tournaments close to this magnitude. Tournament Series-Americas Cardroom runs numerous online poker tournament series throughout each year. -

Ronaldo, Legenda Brazylijskiego Futbolu, W Barcelonie Na Największym Hiszpańskim Festiwalu Pokerowym

RONALDO, LEGENDA BRAZYLIJSKIEGO FUTBOLU, W BARCELONIE NA NAJWIĘKSZYM HISZPAŃSKIM FESTIWALU POKEROWYM BARCELONA, Hiszpania – 9 września 2013 – Legenda brazylijskiej piłki nożnej, Ronaldo Nazario, odwiedził w tym tygodniu Barcelonę, aby wziąć udział w specjalnym turnieju w ramach największego corocznego festiwalu pokerowego w Hiszpanii, European Poker Tour (EPT). Ronaldo, który od niedawna występuje jako ambasador marki internetowego serwisu PokerStars, zasiadł do gry Texas Hold'em z Jose Luisem Saezem z Madrytu i Manuelem Correasem z Kordoby, zwycięzcami turnieju online na PokerStars, który umożliwił im zmierzenie się z legendą futbolu. W rywalizacji wzięli też udział członkowie Teamu PokerStars Pro: Vanessa Selbst, Leo Margets, Andre Akkari, Bertrand „ElkY” Grospellier i Jonathan Duhamel. Ostatecznie, po godzinie gry, zwyciężczynią okazała się Selbst. Człowiek znany powszechnie jako „Ronaldo” jest uważany za jednego z najlepszych piłkarzy wszech czasów. W ciągu 19-letniej kariery zawodowej zdobył imponującą liczbę tytułów. Teraz dołączył do grupy gwiazd sportu, które ostatnio podjęły się gry w pokera, takich jak hiszpańska gwiazda tenisa Rafael Nadal, holenderska hokeistka olimpijska Fatima Moreira de Melo czy zdobywca złotego medalu podczas igrzysk olimpijskich, szwedzki narciarz Marcus Hellner. W rozgrywkach pokerowych znajdują oni tak samo ambitnych przeciwników i podobne wyzwania jak w wybranych dyscyplinach sportowych. „Zawsze staram się dać z siebie wszystko, zarówno w piłce, jak i w życiu. Poker to dla mnie kolejne, ekscytujące wyzwanie”, powiedział Ronaldo. „Widzę liczne podobieństwa pomiędzy piłką nożną i pokerem – obie dziedziny wymagają ogromnej samodyscypliny, ćwiczeń i treningów.“ Blisko 3000 graczy z całego świata zjechało się do Barcelony, aby wziąć udział w 13- dniowym festiwalu pokerowym i zagrać o ponad €14.000.000. Kilka dni wcześniej Turniej Główny Estrellas przyciągnął rekordową liczbę 1798 uczestników, przez co został największym dotychczasowym hiszpańskim turniejem i największym turniejem z wpisowym €1000 rozegranym poza Las Vegas. -

Commentary on the Bangalore Principles of Judicial Conduct

COMMENTARY ON THE BANGALORE PRINCIPLES OF JUDICIAL CONDUCT THE JUDICIAL INTEGRITY GROUP March 2007 2 CONTENTS PREFACE … 5 ACKNOWLEDGMENTS … 7 DRAFTING HISTORY … 9 PREAMBLE … 19 Value 1: INDEPENDENCE … 35 Value 2: IMPARTIALITY … 53 Value 3: INTEGRITY … 73 Value 4: PROPRIETY … 79 Value 5: EQUALITY … 111 Value 6: COMPETENCE AND DILIGENCE … 119 IMPLEMENTATION … 131 DEFINITIONS … 133 Appendix: CULTURAL AND RELIGIOUS TRADITIONS … 135 SELECT BIBLIOGRAPHY … 147 INDEX … 151 3 4 PREFACE A judiciary of undisputed integrity is the bedrock institution essential for ensuring compliance with democracy and the rule of law. Even when all other protections fail, it provides a bulwark to the public against any encroachments on its rights and freedoms under the law. These observations apply both domestically within the context of each nation State and globally, viewing the global judiciary as one great bastion of the rule of law throughout the world. Ensuring the integrity of the global judiciary is thus a task to which much energy, skill and experience must be devoted. This is precisely what the Judicial Group on Strengthening Judicial Integrity (The Judicial Integrity Group) has sought to do since it set out on this task in 2000. It commenced as an informal group of Chief Justices and Superior Court Judges from around the world who combined their experience and skill with a sense of dedication to this noble task. Since then, its work and achievements have grown to a point where they have made a significant impact on the global judicial scene. The principles tentatively worked out originally have received increasing acceptance over the past few years from the different sectors of the global judiciary and from international agencies interested in the integrity of the judicial process. -

Download This Report

Report GIBRALTAR A ROCK AND A HARDWARE PLACE As one of the four island iGaming hubs in Europe, Gibraltar’s tiny 6.8sq.km leaves a huge footprint in the gaming sector Gibraltar has long been associated with Today, Gibraltar is self-governing and for duty free cigarettes, booze and cheap the last 25 years has also been electrical goods, the wild Barbary economically self sufficient, although monkeys, border crossing traffic jams, the some powers such as the defence and Rock and online gaming. foreign relations remain the responsibility of the UK government. It is a key base for It’s an odd little territory which seems to the British Royal Navy due to its strategic continually hover between its Spanish location. and British roots and being only 6.8sq.km in size, it is crammed with almost 30,000 During World War II the area was Gibraltarians who have made this unique evacuated and the Rock was strengthened zone their home. as a fortress. After the 1968 referendum Spain severed its communication links Gibraltar is a British overseas peninsular that is located on the southern tip of Spain overlooking the African coastline as GIBRALTAR IS A the Atlantic Ocean meets the POPULAR PORT Mediterranean and the English meet the Spanish. Its position has caused a FOR TOURIST continuous struggle for power over the CRUISE SHIPS AND years particularly between Spain and the British who each want to control this ALSO ATTRACTS unique territory, which stands guard over the western Mediterranean via the Straits MANY VISITORS of Gibraltar. FROM SPAIN FOR Once ruled by Rome the area fell to the DAY VISITS EAGER Goths then the Moors. -

The Role of Skill Versus Luck in Poker: Evidence from the World Series of Poker

NBER WORKING PAPER SERIES THE ROLE OF SKILL VERSUS LUCK IN POKER: EVIDENCE FROM THE WORLD SERIES OF POKER Steven D. Levitt Thomas J. Miles Working Paper 17023 http://www.nber.org/papers/w17023 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge, MA 02138 May 2011 We would like to thank Carter Mundell for truly outstanding research assistance. The views expressed herein are those of the authors and do not necessarily reflect the views of the National Bureau of Economic Research. NBER working papers are circulated for discussion and comment purposes. They have not been peer- reviewed or been subject to the review by the NBER Board of Directors that accompanies official NBER publications. © 2011 by Steven D. Levitt and Thomas J. Miles. All rights reserved. Short sections of text, not to exceed two paragraphs, may be quoted without explicit permission provided that full credit, including © notice, is given to the source. The Role of Skill Versus Luck in Poker: Evidence from the World Series of Poker Steven D. Levitt and Thomas J. Miles NBER Working Paper No. 17023 May 2011 JEL No. K23,K42 ABSTRACT In determining the legality of online poker – a multibillion dollar industry – courts have relied heavily on the issue of whether or not poker is a game of skill. Using newly available data, we analyze that question by examining the performance in the 2010 World Series of Poker of a group of poker players identified as being highly skilled prior to the start of the events. Those players identified a priori as being highly skilled achieved an average return on investment of over 30 percent, compared to a -15 percent for all other players. -

An Evolution in Gambling

Gaming plc Realms Annual ReportAnnual 2014 & Accounts An Evolution in Gambling Gaming Realms plc Annual Report & Accounts 2014 Strategic Report The Group hopes to 01 Highlights 02 Gaming Realms at a Glance 04 Chairman’s Statement become a market leader 06 Market Positioning 08 Our Strategy in the mobile-led casual 10 Chief Executive’s Review 12 Principal Risks and Uncertainties gambling market forecast Corporate Governance 14 Board and Executive to be worth $100bn Management 16 Directors’ Report 17 Statement of Directors’ worldwide in 2 years. Responsibilities 18 Corporate Governance Financial Statements 19 Independent Auditors’ Report 20 Consolidated Statement of Profit and Loss and Other Comprehensive Income 21 Consolidated Statement of Financial Position 22 Consolidated Statement of Cash Flows 23 Consolidated Statement of Changes in Equity 24 Notes to the Consolidated Financial Statements 47 Parent Company Balance Sheet 48 Notes to Parent Company Financial Statements 52 Company Information www.gamingrealms.com Highlights Strategic Report Strategic Operational highlights › Increase of 635% in new real money › Completion of new in-house scalable gambling depositors compared to the platform which includes a feature set previous financial period. to enhance conversion, retention and › Increase of 338% in average daily players monetisation of real money gambling compared to previous financial period. players. › Acquisition of QuickThink Media Limited › Obtained licences from the Alderney and Blueburra Holdings Limited. Gambling Control Commission -

Fanduel Group Mobile Sportsbook Launches in Virginia and Michigan

FanDuel Group Mobile Sportsbook Launches in Virginia and Michigan Virginia Lottery Decision Makes FanDuel First and Only Provider Live In Commonwealth London – January 25, 2021 – FanDuel Group, part of Flutter Entertainment plc, and the Washington Football Team announced the first-ever market access partnership between a National Football League team and an online sports gaming platform in the U.S. Under the terms of this agreement, FanDuel and the Washington Football Team launched legal sports betting on Thursday in the Commonwealth of Virginia. The partnership combines FanDuel Group’s market-leading sports betting platform with the Washington Football Team’s strong presence in Virginia as it serves as the home for the INOVA Sports Performance Center, Richmond Training Camp, and the team headquarters. Under Virginia’s sports wagering law, the Washington Football Team was given preference for a mobile sports betting permit based on it meeting certain criteria for sports franchises headquartered in Virginia, and the option to partner with an established sports wagering operator to run the business. The Washington Football Team has chosen the FanDuel Sportsbook as its operational partner to jointly hold the permit. Commenting on the news, Matt King, Chief Executive Officer of FanDuel Group, said: “We are excited to bring America’s #1 Sportsbook to residents and visitors to the Commonwealth of Virginia. We’re honoured to partner with an iconic sports franchise and we plan to deliver the most fan-focused and secure mobile sports betting experience to the passionate sports fans of Virginia.” In addition, FanDuel becomes the official daily fantasy sports partner of the Washington Football Team and will also have prominent stadium signage at Fedex Field and offer customers unique game day experiences like a special FanDuel section on game days.