Henderson Group Plc Annual Report 2014

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Tournament Breakdown by Surface Champion Ranking Points By

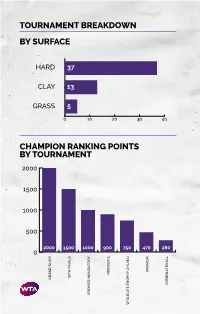

TOURNAMENT BREAKDOWN BY SURFACE HAR 37 CLAY 13 GRASS 5 0 10 20 30 40 CHAMPION RANKING POINTS BY TOURNAMENT 2000 1500 1000 500 2000 1500 1000 900 750 470 280 0 PREMIER PREMIER TA FINALS TA GRAN SLAM INTERNATIONAL PREMIER MANATORY TA ELITE TROPHY HUHAI TROPHY ELITE TA 55 WTA TOURNAMENTS BY REGION BY COUNTRY 8 CHINA 2 SPAIN 1 MOROCCO UNITED STATES 2 SWITZERLAND 7 OF AMERICA 1 NETHERLANDS 3 AUSTRALIA 1 AUSTRIA 1 NEW ZEALAND 3 GREAT BRITAIN 1 COLOMBIA 1 QATAR 3 RUSSIA 1 CZECH REPUBLIC 1 ROMANIA 2 CANADA 1 FRANCE 1 THAILAND 2 GERMANY 1 HONG KONG 1 TURKEY UNITED ARAB 2 ITALY 1 HUNGARY 1 EMIRATES 2 JAPAN 1 SOUTH KOREA 1 UZBEKISTAN 2 MEXICO 1 LUXEMBOURG TOURNAMENTS TOURNAMENTS International Tennis Federation As the world governing body of tennis, the Davis Cup by BNP Paribas and women’s Fed Cup by International Tennis Federation (ITF) is responsible for BNP Paribas are the largest annual international team every level of the sport including the regulation of competitions in sport and most prized in the ITF’s rules and the future development of the game. Based event portfolio. Both have a rich history and have in London, the ITF currently has 210 member nations consistently attracted the best players from each and six regional associations, which administer the passing generation. Further information is available at game in their respective areas, in close consultation www.daviscup.com and www.fedcup.com. with the ITF. The Olympic and Paralympic Tennis Events are also an The ITF is committed to promoting tennis around the important part of the ITF’s responsibilities, with the world and encouraging as many people as possible to 2020 events being held in Tokyo. -

Aegon Annual Report 2014

Annual Report 2014 This pdf is interactive. The content is clickable so you can navigate through this document. 1 Table of contents Strategic information Financial statements of Aegon N.V. Introduction 3 Income statement of Aegon N.V. 286 Letter of the CEO 4 Statement of financial position of Aegon N.V. 287 Composition of the Executive Board Notes to the financial statements 288 and the Management Board 6 Aegon’s strategy 8 Independent auditor’s report 301 Business overview History and development of Aegon 12 Other information Selected financial data 13 Proposal for profit appropriation 310 Business lines 16 Major shareholders 311 Results of operations 17 Worldwide 17 Americas 25 Other financial information Netherlands 44 Schedule I 314 United Kingdom 54 Schedule II 315 New Markets 63 Schedule III 317 Risk management 84 Schedule IV 319 Capital and liquidity management 87 Schedule V 320 In control statement 91 Additional information Governance Regulation and supervision 323 Report of the Supervisory Board 92 Risk factors 325 Members of the Supervisory Board 98 Property, plants and equipment 341 Remuneration Report 100 Employees and labor relations 342 Corporate governance 107 Dividend policy 342 Differences between Dutch and US company laws 112 The offer and listing 343 Code of ethics 113 Memorandum and Articles of Association 344 Controls and procedures 114 Material contracts 346 Exchange controls 346 Taxation 346 Consolidated financial statements Principal accountant fees and services 353 Exchange rates 120 Purchases of equity securities by the issuer Consolidated income statement of Aegon N.V. 122 and affiliated purchasers 354 Consolidated statement of comprehensive income Quarterly results – unaudited 355 of Aegon N.V. -

2014 Champions of Tennis

Customization Pioneer Youth Tennis STRING SELECTOR: The wit and Hit a winner Find the right string and warmth of with COACH for your customers VIC BRADEN YOUTH TENNIS JANUARY 2015 / VOLUME 43/ NUMBER 1 / $5.00 2014 Champions of Tennis CONGRATULATIONS TO: BAHRAM AKRADI ARMY NAVY COUNTRY CLUB Our annual awards honor DAVID YAMANE TRANS TEXAS TENNIS those who continue to make ALLAN IVERSON YOUR SERVE TENNIS this sport a winner. JOE & SHIMA GROVER ELLEN MILLER SIMON GALE INNERCITY TENNIS FOUNDATION INDIAN WELLS TENNIS GARDEN JACK NEWMAN MERCER COUNTY PARK T.C. LAURIE MARTIN WASH. DC DEPT. OF PARKS & REC PAUL WALKER SIGNATURE TENNIS THE TENNIS CONGRESS NIGEL PUGH RANDY MATTINGLEY USTA INTERMOUNTAIN pg. 45 Incorporating USPTA Te nnisIndustry www.tennisindustrymag.com JANUARY 2015 DEPARTMENTS 4 Our Serve 7 Industry News 15 TIA news 20 Youth Tennis: Coach Youth Tennis 22 Pioneers: Vic Braden 40 Ask the Experts 42 String Playtest: Babolat Origin 17 44 Your Serve, by Mark Rearden INDUSTRY NEWS 7 Asics debuts BZ100 Performance Racquet 7 World TeamTennis celebrates 40 years 7 Gerflor buys Connor Sport Court 8 MRT John Gugel honored by IART Symposium 8 NYJTL honored by Bronx Chamber of Commerce p.23 8 Tecnifibre partners with ProWorld Tennis FEATURES 8 Head introduces new Graphene XT Speed line 23 2014 Champions of Tennis 9 UST A’s Gordon Smith honored by University of Georgia Our annual awards honor the people, 9 UST A honors grassroots businesses and organizations that are making a tennis at Atlanta TDW 11 Mason promoted to president difference in the tennis industry. -

City of Indian Wells, California Comprehensive Annual Financial Report Fiscal Year Ended June 30, 2014

CITY OF INDIAN WELLS, CALIFORNIA COMPREHENSIVE ANNUAL FINANCIAL REPORT FISCAL YEAR ENDED JUNE 30, 2014 CITY OF INDIAN WELLS, CALIFORNIA COMPREHENSIVE ANNUAL FINANCIAL REPORT FISCAL YEAR ENDED JUNE 30, 2014 Prepared by the Finance Director Kevin McCarthy, Finance Director Susan Leong, Senior Accountant Norma Rojo, Accounting Technician III/Payroll Amy Dallosta, Accounting Technician II Daisy Amezcua, Accounting Technician I 44-950 Eldorado Drive, Indian Wells, California 92210-7497 Telephone: 760-346-2489 – Fax: 760-346-0407 www.cityofindianwells.org THIS PAGE INTENTIONALLY LEFT BLANK CITY OF INDIAN WELLS FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED JUNE 30, 2014 TABLE OF CONTENTS Page Number INTRODUCTORY SECTION Letter of Transmittal ............................................................................................................................ i GFOA Certificate of Achievement for Excellence in Financial Reporting........................................... xi Organization Chart ............................................................................................................................. xii List of Principal Officials ..................................................................................................................... xiii FINANCIAL SECTION Independent Auditors’ Report ................................................................................................................... 1 Management's Discussion and Analysis .................................................................................................. -

EMIRATES ATP RANKINGS FACTS and FIGURES Atpworldtour.Com 2015 Year-End Emirates Atp Rankings

EMIRATES ATP RANKINGS FACTS AND FIGURES ATPWorldTour.com 2015 year-end emirates atp rankings As of November 30, 2015 1 Djokovic,Novak/SRB 64 Andujar,Pablo/ESP 127 Youzhny,Mikhail/RUS 190 Lapentti,Giovanni/ECU 2 Murray,Andy/GBR 65 Kukushkin,Mikhail/KAZ 128 Fratangelo,Bjorn/USA 191 Samper-Montana,Jordi/ESP 3 Federer,Roger/SUI 66 Haase,Robin/NED 129 Smith,John-Patrick/AUS 192 Volandri,Filippo/ITA 4 Wawrinka,Stan/SUI 67 Carreño Busta,Pablo/ESP 130 Coppejans,Kimmer/BEL 193 Przysiezny,Michal/POL 5 Nadal,Rafael/ESP 68 Lorenzi,Paolo/ITA 131 Carballes Baena,Roberto/ESP 194 Gojowczyk,Peter/GER 6 Berdych,Tomas/CZE 69 Kudla,Denis/USA 132 Soeda,Go/JPN 195 Karatsev,Aslan/RUS 7 Ferrer,David/ESP 70 Giraldo,Santiago/COL 133 Elias,Gastao/POR 196 Lamasine,Tristan/FRA 8 Nishikori,Kei/JPN 71 Mahut,Nicolas/FRA 134 Novikov,Dennis/USA 197 Stepanek,Radek/CZE 9 Gasquet,Richard/FRA 72 Cervantes,Iñigo/ESP 135 Donaldson,Jared/USA 198 Sarkissian,Alexander/USA 10 Tsonga,Jo-Wilfried/FRA 73 Almagro,Nicolas/ESP 136 Basic,Mirza/BIH 199 Moriya,Hiroki/JPN 11 Isner,John/USA 74 Pella,Guido/ARG 137 Ymer,Elias/SWE 200 Laaksonen,Henri/SUI 12 Anderson,Kevin/RSA 75 Muñoz-De La Nava,Daniel/ESP 138 Arguello,Facundo/ARG 201 Mertens,Yannick/BEL 13 Cilic,Marin/CRO 76 Lajovic,Dusan/SRB 139 Gombos,Norbert/SVK 202 McGee,James/IRL 14 Raonic,Milos/CAN 77 Lu,Yen-Hsun/TPE 140 Kravchuk,Konstantin/RUS 203 Yang,Tsung-Hua/TPE 15 Simon,Gilles/FRA 78 Pouille,Lucas/FRA 141 Bagnis,Facundo/ARG 204 Halys,Quentin/FRA 16 Goffin,David/BEL 79 Kuznetsov,Andrey/RUS 142 Gonzalez,Alejandro/COL 205 Bourgue,Mathias/FRA -

Tharunka 2014

Week 2 - Week 3, Semester 1, 2014 Volume 60, No. 02 First Published 1953 University of NSW’s Independent Student Newspaper EDITORIAL 2 CALENDAR 2 AGONY IBIS 2 SHORTLIST 3 LETTERS 3 NEWS 4-7 Warrane Punished For Sexist 4 Conduct Nick Timms Do We Need A Voice For Men? 5 Crystal Moran Conservative Club Controversy 6 With Rival Liberal Factions Continues Ammy Singh Coalition To Propose Crack 7 Downs On Torrenting Matthew Bugden Christine Lagarde Discusses The 7 World Economy, Women’s Rights And Climate Change Action At Sydney’s Seymour Centre Matthew Baker COLUMNS 3, 10-11 Noodle House Yarns 3 David Bailey-Mckay The Hirst Report 10 Ned Hirst An Expert’s Guide To Life 10 Dylan Chalwell They Are Just Chilling, Stop The 11 Killing Connor Mulholland Being Political Without Being A 11 Wanker Jeremiasz Sieczko FEATURES 8-9 Redfern Creative Hub Gives Kids 8 A Different Kind Of Education Freya King Thailand Torn 9 Chiara Gargano COMICS & CREATIVE 12-14 LEFT VS. RIGHT 15 Sydney Lockout Laws Lauren Mccracken One-Punch Reform Fuelled By Emotion, Not Facts Nicholas Gerovasilis REVIEWS & SATIRE 16-18 SRC, PGC, SDC REPORTS 20 SPORT 22-24 Roosters Can Boast, They Are Best 22 Rugby League Club In The World Niko Pajarillo Say Sport? A Social And Political 23 Commentary In And Around The Playing Field Raylenne Galloway Serena Williams & Indian Wells 23 Lawrence Leung UNSW Sport Preview 24 Sam Davies Connect with Tharunka twitter.com/tharunka tharunka tharunka fb.me/ .tumblr.com 2 EDITORIAL VOLUME 60, ISSUE 2 Date Events Week 2 - Week 3 th Mar Tuesday, 11th – Saturday, 15th of March 11 A Creative Practice Lab Production: MONKEY Myers Studio, near Gate 2, Kensington Campus Welcome to the long-haul kiddies! It’s week 2 and here’s the second issue of Tharunka, our shining beacon th Mar of independent student journalism on campus. -

Memoir Given New Life

WEDNESDAY, MARCH 19, 2014 Volume 95, Issue 28 Raising interest in science, math 11th annual NSM- SYMPOSIUM ICC symposium will showcase research • Theme: “Explorations DENA HAMEDANI Daily Titan in Citizen Science” With the campus buzz- • 16 student oral ing in anticipation for scientist Bill Nye’s ap- presentations, 37 stu- pearance on campus dent research poster Thursday, the Natural Science and Mathematics presentations Interclub Council (NSM- ICC) hopes to take ad- • 5 faculty lectures vantage of the excite- ment with two days of science and research • Keynote by Bill Nye presentations. “The Science Guy” The NSM-ICC will pres- ent its 11th annual Sci- ence and Mathematics • Subjects include: Symposium, to be held - Mathematics Wednesday and Thurs- day in the Titan Student - Biology Union. Students and pro- - Chemistry fessors will present their research, encouraging all - Psychology attendees to rethink math - Physics MARIAH CARRILLO / Daily Titan and science. Ingrid Garner, 21, a senior theatre arts major, is transforming her grandmother’s non-fiction book about surviving Nazi Germany as a Each year, the sym- young American girl into a one-hour monoplay, which she will be taking to theater festivals overseas. posium provides stu- • Events start at noon dents who have received Wednesday and Thurs- funding to present their day in TSU research to the CSUF community. Students at- Memoir given new life tending conferences re- ceive funding through physics major and chair NSM-ICC by a majority of NSM-ICC, seeing the Student brings grandmother’s inspiring story to the stage vote. symposium come to life NSM-ICC also extends is sure to feel like a huge but she is also acting each an invitation to organi- accomplishment. -

Women's Tennis Association Media Guide

2017 Women’s Tennis Association Media Guide © Copyright WTA 2017 All Rights Reserved. No portion of this book may be reproduced —electronically, mechanically or by any other means, including photocopying— without the written permission of the Women’s Tennis Association (WTA). Printed in Canada Compiled by the Women’s Tennis Association (WTA) Communications Department WTA CEO & Chairman: Steve Simon Editors-in-Chief: Kevin Fischer & Adam Lincoln Assistant Editors: Amy Binder, Heather Bowler, Kate Goff, Estelle LaPorte, Alex Prior, Catherine Sneddon, Bryan Shapiro, Eloise Tyson, Jeff Watson, Yanyan Xu Cover Design: Jack Anton, Henrique Ruiz, Tim Smith Graphic Design: Provations Group, Nicholasville, KY, USA Contributors: Mike Anders, Crystal Christian, Sloan Floyd, Kelly Frey, Anne Hartman, Jill Hausler, Jamie Holley, Pete Holtermann, Kico Jiang, David Kane, Ashley Keber, Peachy Kellmeyer, Cindy Lupkey, Courtney McBride, Sean O’Malley, Joan Pennello, Neil Robinson, Kathleen Stroia, Chris Whitmore Photography: Getty Images (AFP, Bongarts), Action Images, GEPA Pictures, Ron Angle, Michael Baz, Matt May, Pascal Ratthe, Art Seitz, Chris Smith, Red Photographic, adidas, WTA www.wtatennis.com (English) facebook.com/WTA www.wta.cn (Chinese) twitter.com/WTA www.es.wtatennis.com (Spanish) youtube.com/WTA Snapchat.com/WTA Instagram.com/WTA WTA WTA WTA WTA Corporate European Asia-Pacific Finals Headquarters Headquarters Headquarters Headquarters 100 Second Avenue South, Palliser House, Palliser Road Vantone Center Tower C, Suite 601 6 Stadium Walk Suite 1100-S London W14 9EB, England 6A Chaowai Avenue #01-05 Sports Information & St Petersburg, Florida 33701 USA Tel: +44.20.7386.4100 Chaoyang District, Resource Centrer Tel: +1.727.895.5000 Beijing 100020, China Singapore, 397698 Tel: +86.10.5910.2700 Tel: +65.6653.9450 2 Table of Contents GENERAL INFORMATION Women’s Tennis Association (WTA) Story. -

The Fight to Save Professional Tennis in Indian Wells

David versus Goliath: The Fight to Save Professional Tennis in Indian Wells In late 2004, the Pacific Life Open was in danger of being sold to a group from Shanghai, China. The tournament, one of the premier stops on both the women’s and men’s professional tennis tours, had been played in the Coachella Valley since 1974 and at the Indian Wells Tennis Garden since 2000. Were its days on American soil numbered? In late 2004, Charlie Pasarell and Raymond Moore were well as the bankruptcy of their only media partner, sitting in the Indian Wells Tennis Garden offices when International Sports and Leisure (ISL). they received a fax from International Management Group (IMG) chairman and CEO, Teddy Forstmann. The offer from Shanghai was significant – $44 million IMG was an ownership partner with Moore and Pasarell for the tournament sanction – but it had never been (PM Sports Management) for the Pacific Life Open, about the money for PM Sports. During lean years in one of the premier events on the professional tennis the early 2000s, they fought tooth and nail to ensure circuit. The Open was played annually at the Indian that the tournament still delivered a world-class Wells Tennis Garden, situated in the beautiful Coachella experience to both players and spectators. As the Valley in Southern California. Moore and Pasarell stared partnership with IMG was an equal 50/50 split, each blankly at the fax, which contained a term sheet signed partner had to agree to all contractual terms for any by Forstmann and a group from Shanghai, China. -

2014 Wta Official Rulebook Official Wta 2014

2014 WTA OFFICIAL RULEBOOK 2014 WTA OFFICIAL RULEBOOK 2014 WTA WTA - Women’s Tennis Association 100 Second Avenue South, Suite 1100-S St. Petersburg, Florida, USA 33701 TEL: +1.727.895.5000 FAX: +1.727.894.1982 www.wtatennis.com Printed in the United States of America 1-122-Intro-Players (vNov2013):Layout 1 11/19/2013 9:53 AM Page 1 2014 Official Rulebook Copyright 2014 WTA Tour, Inc. All Rights Reserved WTA and WTA Tour are registered trademarks of WTA Tour, Inc. Printed in the United States of America 1-122-Intro-Players (vNov2013):Layout 1 11/19/2013 9:53 AM Page 2 . 1-122-Intro-Players (vNov2013):Layout 1 11/19/2013 9:53 AM Page 1 TABLE OF CONTENTS THE WTA I. INTRODUCTION 7 A. DESCRIPTION 7 B. ADMINISTRATION 7 C. RULES 7 D. TOURNAMENT ACCEPTANCES 8 E. TOUR YEARS 8 F. WORLD CHAMPION 8 G. WTA BOARD OF DIRECTORS 9 II. TOP 10 PLAYER LIST 11 A. COMPOSITION AND ORDER 11 B. MINIMUM COMMITMENT REQUIREMENTS 12 C. COMPENSATION 13 D. COMMITMENT DEADLINES AND RULES 13 E. INCENTIVE PAYMENTS 15 F. SUSPENSION RULE 16 G. CALCULATION AND PAYMENT 20 H. ADDITIONAL RULES FOR TOP 10 PLAYERS 20 I. YEARS OF SERVICE 21 J. FUNDING OF BONUS POOL 21 III. ENTRIES/WITHDRAWALS/DRAWS/SCHEDULING 23 A. ENTRIES AND ACCEPTANCES 23 B. WITHDRAWING FROM A TOURNAMENT 34 C. DRAWS 45 D. SCHEDULING 81 IV. PLAYER RESPONSIBILITIES/ON-COURT RULES AND PROCEDURES 89 A. DIAMOND ACES POLICY 89 B. MEDIA/SPONSOR/PUBLIC RELATIONS RESPONSIBILITIES 98 C. CLOTHING AND EQUIPMENT 111 D. -

Colo May June 06

February March 2014 Departments Contents Dinah Shore Tournament Course Hole 14 ON PAR GAME PLAY PUBLISHER’S NOTES 2014 KRAFT NABISCO CHAMPIONSHIP .......................................................8 Who will leap into Poppie’s Pond this year? .........36 ON COVER TEN YEARS AND COUNTING Michelle Wie and Paula Creamer, seasoned 2014 BNP PARIBAS OPEN veterans on the LPGA Tour .......................................39 It sets records, it sets precedents, it’s all about must-see tennis in a superb venue ..........................12 ROCKIN’ THE FAIRWAYS WITH PATRICK WARBURTON The 4th annual Patrick Warburton Celebrity PLAY WORTHY Golf Tournament is a must-do event .......................46 INDIAN WELLS TENNIS GARDEN Where beauty, technology and extraordinary SPOTLIGHT talent come together .................................................16 THE GOLF ART JOURNEY OF GRAEME BAXTER His gift is in finding the heart of each course TOP GOLF & TENNIS RESORTS OF THE SOUTHWEST and capturing it on canvas ......................................40 Find your ideal for challenging play and luxury digs .....................................................................22 COURSE DESIGN MISSION HILLS COUNTRY CLUB THE COMPLEX WORLD OF GOLF COURSE DESIGN When it comes to tennis, Mission Hills has What are architects thinking when they design exemplary credentials ................................................28 a course? It may surprise you .................................42 DESERT DUNES GOLF CLUB REDEFINES ITS FUTURE New development at the resort creates -

Colo May June 06

73520 EL PASEO SUITE E PALM DESERT 760-773-1040 ELPASEOJEWELERS.COM EL PASEO JEWELERS CONTENTS F EBRUARY M ARCH 2017 9 Publisher’s Notes 16 The 2017 BNP Paribas Open In preparation for future tournaments, Indian Wells Tennis Garden’s Stadium 1 has been renovated. 20 PGA Tour Superstores Offer a Comprehensive Experience No mere retail outlet, this store is a golf and tennis enthusiast’s one-stop shop 22 Tennis with the Stars The popular event returns to Omni Rancho Las Palmas for 2017. 24 ANA Inspiration 2017 Golf’s first major of the year seeks to enhance the first-class experience. 26 Hassle-Free Home Ownership at The Residence Club at PGA West A PGA West Premier Sports Membership is 12 just one of the benefits. ROGER FEDERER’S LEGACY 30 IS ASSURED—ON AND OFF 2017 Warburton Celebrity Golf Music Run It’s golf and a whole lot more—for a worthy THE COURT cause. The tennis great deserves to celebrate good times 32 What You Need to Know About Pickleball To start, it’s one of the fastest growing sports in the nation and it’s for everyone 34 GOLFER’S PLAYBOOK Intertwining Club Fitting and Instruction for Better Results Photo by Nikko Milkovic Desert Golf &tennis • february March 2017 5 CONTENTS F EBRUARY M ARCH 2017 41 36 Experience Italy as a Local in a GOLF AND TENNIS Private Villa COMMUNITIES ARE NOT Villas and castles offer an appealing ONE-SIZE-FITS-ALL alternative to hotels How to choose the golf or tennis community that’s right for you 42 Romancing the Palate February is the month of love, but romance reigns at these restaurants all year