Mtf Var Margin Requirement for the Month of September

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

India Capital Markets Experience

Dorsey’s Indian Capital Markets Capabilities March 2020 OVERVIEW Dorsey’s capital markets team has the practical wisdom and depth of experience necessary to help you succeed, even in the most challenging markets. Founded in 1912, Dorsey is an international firm with over 600 lawyers in 19 offices worldwide. Our involvement in Asia began in 1995. We now cover Asia from our offices in Hong Kong, Shanghai and Beijing. We collaborate across practice areas and across our international and U.S. offices to assemble the best team for our clients. Dorsey offers a full service capital markets practice in key domestic and international financial centers. Companies turn to Dorsey for all types of equity offerings, including IPOs, secondary offerings (including QIPs and OFSs) and debt offerings, including investment grade, high-yield and MTN programs. Our capital markets clients globally range from emerging companies, Fortune 500 seasoned issuers, and venture capital and private equity sponsors to the underwriting and advisory teams of investment banks. India has emerged as one of Dorsey’s most important international practice areas and we view India as a significant market for our clients, both in and outside of India. Dorsey has become a key player in the Indian market, working with major global and local investment banks and Indian companies on a range of international securities offerings. Dorsey is recognized for having a market-leading India capital markets practice, as well as ample international M&A and capital markets experience in the United States, Asia and Europe. Dorsey’s experience in Indian capital markets is deep and spans more than 15 years. -

AAVAS Financiers

31 July 2021 1QFY22 Results Update | Sector: Financials AAVAS Financiers Estimate change CMP: INR2,530 TP: INR2,820 (+12%) Neutral TP change Ability to recover and bounce back will be put to test Rating change Increase in 1+dpd transitory in our view Motilal Oswal values your support in the Asiamoney Brokers Poll 2021 for PAT grew 20% YoY, but fell 32% QoQ, to INR599m (in line) in 1QFY22. NII India Research, Sales, Corporate rose 14% QoQ and 29% YoY, while operating profit fell 10% QoQ (7% beat). Access and Trading team. However, higher-than-expected credit cost of INR170m (est. INR110m) led We request your ballot. to the in line PAT. Sharp deterioration in 1+dpd to 12.7% (up 620bp QoQ), relative to some of its other peers who have reported their 1QFY22 numbers, could be indicative of the stress that was seen at the time of demonetization and Bloomberg AAVAS IN higher proportion of self-employed customers in the mix. Equity Shares (m) 78 M.Cap.(INRb)/(USDb) 198.1 / 2.7 Given the strength of this franchise, we remain convinced that it can script 52-Week Range (INR) 3068 / 1285 a gradual improvement in its 1+dpd and GS3 once collections further 1, 6, 12 Rel. Per (%) -6/26/54 improve, led by a recovery in economic activity. Our estimates are largely 12M Avg Val (INR M) 246 unchanged and we are building in ~50bp/35bp of credit costs in FY22E/FY23E. We maintain our Neutral rating with a TP of INR2,820/share, Financials & Valuations (INR b) given that the stock trades at rich valuations of 6.3x FY23E P/BV. -

Management Discussion and Analysis

Corporate Overview Statutory Reports Financial Statements Management Discussion and Analysis Management Discussion and Analysis 1. INFRASTRUCTURE INDUSTRY OVERVIEW & create investor-friendly highway development initiatives OUTLOOK have already started the process of recouping the deficit In FY 2016-17, India’s infrastructure industry, including of last few years. The next fiscal year is likely to show an the road sector, continued on its path of recovery. The increase in BOT (Toll) bids with the Government aiming to Government has been undertaking initiatives to revive build 41 kms per day of roads. entrepreneurs’ interests in the road sector through innovative models like Hybrid Annuity. As a result, 3. COMPANY AND BUSINESS OVERVIEW around 4,337 kms ([approx. 422 km of Build-Operate- A. Company Overview Transfer(BOT) projects, 2,434 km of Hyrbid Annuity IRB Infrastructure Developers Ltd. (IRB), incorporated in projects, 1,481 km of Engineering-Procurement- 1998, has strong in-house integrated project execution Construction (EPC) projects]) of National Highways capabilities in both its business verticals viz. Construction improvement work were awarded by the National and Operation & Maintenance of Highways. It is the first Highways Authority of India (NHAI) in FY 2016-17. Most mover and pioneer in the road BOT business and is one of of the bids for the road projects saw good participation India’s largest road BOT operators with a rich portfolio of than the earlier years. NHAI has been focusing on 22 Road BOT projects. It also has approximately 18.79% addressing land acquisition and environmental clearances share of the Golden Quadrilateral Highway Network for its upcoming projects. -

Indian Energy Exchange Ltd. August 13, 2018

Indian Energy Exchange Ltd. August 13, 2018 Analyst: Abhilasha Satale (022) 67141435 Q1FY19 Result Update@ Dalal&Broacha BUY Q1FY19 performance in-line with estimates Current Price 1640 - Target Price 2025 Sales improved 22.4%yoy to Rs670mn. Total volume increased by 22%yoy to 14.43BU. This was driven by increase in procurement by distribution companies. DAM volumes Upside 23% increased 19% yoy, TAM volumes increased 214% yoy. 52 Week Range 1405/1689 - Contribution from Discoms to total volumes increased from 60% to 83% and the same from open access has gone down from 40% to 17%. Increase in MCP by 50% yoy to Key Share Data Rs4.13 p.u. and increase in cross subsidy charge has deterred open access volumes. REC volumes increased by 341% yoy to 20.1lacs. Market Cap (Rs.bn) 49.74 -Subscription revenue has gone down during the quarter as 400 clients deactivated from the exchange platform. Management expects subscription revenue to increase when Market Cap (US$ bn) 0.76 MCP on exchange falls. No of o/s shares (mn) 30.3 - EBITDA increased 25% yoy. On account of higher trade volume and reduction in Face Value 10 technology cost due to acquisition of trading software technology. EBITDA margin at 83% Monthly Avg. vs 77%. - Depreciation increased by 76% yoy. On account of capital expenditures incurred during Vol(BSE+NSE) Nos FY 2017-18, mainly, on acquisition of 63Moons trading software technology. (‘000) -Tax rate has gone down from 35% to 29% yoy improving PAT by 34% yoy. BSE Code 2130 NSE Code IEX Other highlights Bloomberg IEX IN Short term market remained 10%, while exchanges gained market share: Short term transactions increased 1.5% yoy. -

A. Semi-Annual Review

Date: February 22, 2016 PRESS RELEASE Semi-annual Review of Indices Mumbai: The Index Maintenance Sub-Committee has decided to make the following replacement of stocks in various indices as part of its periodic review. These changes shall become effective from April 1, 2016 (close of March 31, 2016). A. Semi-Annual Review: 1) Nifty 50 Index The following scrips are being excluded: Sr. No. Scrip Name Symbol 1 Cairn India Ltd. CAIRN 2 Punjab National Bank PNB 3 Vedanta Ltd. VEDL The following scrips are being included: Sr. No. Scrip Name Symbol 1 Aurobindo Pharma Ltd. AUROPHARMA 2 Bharti Infratel Ltd. INFRATEL 3 Eicher Motors Ltd. EICHERMOT 4 Tata Motors Ltd. (DVR) * TATAMTRDVR * As per the decision of the Index Policy Committee, equity shares with differential voting rights shall be eligible to be included in the indices as an additional security subject to the fulfilment of eligibility criteria. On account of inclusion of Tata Motors Ltd. (DVR), the Nifty 50 index shall have 51 securities. 2) Nifty100 Liquid 15 Index The following scrips are being excluded: Sr. No. Scrip Name Symbol 1 Hero MotoCorp Ltd. HEROMOTOCO 2 Tech Mahindra Ltd. TECHM The following scrips are being included: Sr. No. Scrip Name Symbol 1 Aurobindo Pharma Ltd. AUROPHARMA 2 LIC Housing Finance Ltd. LICHSGFIN 1 3) Nifty Midcap Liquid 15 Index ** The following scrips are being excluded: Sr. No. Scrip Name Symbol 1 Bharat Electronics Ltd. BEL 2 Glenmark Pharmaceuticals Ltd. GLENMARK 3 Hindustan Petroleum Corporation Ltd. HINDPETRO 4 Power Finance Corporation Ltd. PFC 5 Rural Electrification Corporation Ltd. RECLTD 6 Tata Global Beverages Ltd. -

Portfolio Holdings Listing Fidelity Emerging Asia Fund As of June 30

Portfolio Holdings Listing Fidelity Emerging Asia Fund DUMMY as of July 30, 2021 The portfolio holdings listing (listing) provides information on a fund’s investments as of the date indicated. Top 10 holdings information (top 10 holdings) is also provided for certain equity and high income funds. The listing and top 10 holdings are not part of a fund’s annual/semiannual report or Form N-Q and have not been audited. The information provided in this listing and top 10 holdings may differ from a fund’s holdings disclosed in its annual/semiannual report and Form N-Q as follows, where applicable: With certain exceptions, the listing and top 10 holdings provide information on the direct holdings of a fund as well as a fund’s pro rata share of any securities and other investments held indirectly through investment in underlying non- money market Fidelity Central Funds. A fund’s pro rata share of the underlying holdings of any investment in high income and floating rate central funds is provided at a fund’s fiscal quarter end. For certain funds, direct holdings in high income or convertible securities are presented at a fund’s fiscal quarter end and are presented collectively for other periods. For the annual/semiannual report, a fund’s investments include trades executed through the end of the last business day of the period. This listing and the top 10 holdings include trades executed through the end of the prior business day. The listing includes any investment in derivative instruments, and excludes the value of any cash collateral held for securities on loan and a fund’s net other assets. -

Aavas Financiers Ltd

Name of the issue: Aavas Financiers Limited Updated: April 2021 1 Type of issue (IPO/ FPO) IPO 2 Issue size (Rs. in Cr) 1,640.32 3 Grade of issue alongwith name of the rating agency Not Applicable (excl. Anchor 4 Subscription Level (Number of times) 0.9112* Investor) Source: Minutes for basis of allotment dated Oct 3, 2018 * Figure is after technical rejections 5 QIB holding (as a %age of total outstanding capital) as disclosed to stock exchanges Particulars % (i) On Allotment 23.09% (ii) at the end of the 1st Quarter immediately aftof the issue (Dec 31, 2018) 31.24% (iii) at the end of 1st FY (March 31, 2019) 31.84% (iv) at the end of 2nd FY (March 31, 2020) 37.10% (v) at the end of 3rd FY (March 31, 2021) 40.35% Source: SE website 6 Financials of the issuer (Consolidated in Rs Cr) Particulars 31-Mar-19 31-Mar-20 31-Mar-21 Net Sales/ Income from operations 710.17 902.55 Not Available Net Profit after Minority Interest 176.03 249.04 Not Available Equity Capital 78.11 78.32 Not Available Reserves excluding revaluation reserves 1,758.91 2,019.59 Not Available Note: Financial for the year ended March 31, 2021 shall be updated in due course 7 Trading status in the scrip of the issuer Company's Equity Shares are listed on both the BSE Limited ("BSE") and the National Stock Exchange of India Limited ("NSE") Particulars Status (i) at the end of 1st FY (March 31, 2019) Frequently Traded (ii) at the end of 2nd FY (March 31, 2020) Frequently Traded (iii) at the end of 3rd FY (March 31, 2021) Frequently Traded Source: SE website 8 Change, if any, -

Factsheet Jan 2014.Indd

Factsheet January 2014 Strengthen your portfolio with Religare Invesco. Equity Funds Debt Funds Religare Invesco Tax Plan Religare Invesco Liquid Fund Religare Invesco PSU Equity Fund Religare Invesco Ultra Short Term Fund Religare Invesco Contra Fund Religare Invesco Short Term Fund Religare Invesco Mid Cap Fund Religare Invesco Credit Opportunities Fund Religare Invesco Arbitrage Fund Religare Invesco Medium Term Bond Fund Religare Invesco Growth Fund Religare Invesco Active Income Fund Religare Invesco Equity Fund Religare Invesco Bank Debt Fund Religare Invesco Overnight Fund Religare Invesco Banking Fund Religare Invesco Gilt Fund Religare Invesco Business Leaders Fund Religare Invesco Infrastructure Fund Fund of Funds Religare Invesco Mid N Small Cap Fund Religare Invesco Gold Fund Hybrid Funds Exchange Traded Funds Religare Invesco Monthly Income Plan (MIP) Plus Religare Invesco Gold Exchange Traded Fund Religare Invesco Monthly Income Plan Religare Invesco Nifty Exchange Traded Fund Average Assets Under Management for the quarter ending December 2013: `13,706.16 Crores 1 Performance of Schemes Scheme / Benchmark NAV as on Dec. 31, 2012 - Dec. 30, 2011 - Dec. 31, 2010 - Since Inception Dec. 31, 2013 Dec. 31, 2013 Dec. 31, 2012 Dec. 30, 2011 (CAGR ) Current Value (`) (Absolute ) (Absolute ) (Absolute ) of `10,000 Fund Manager : Sujoy Das Religare Invesco Short Term Fund 1663.5623 6.57% 10.76% 9.60% 7.79% 16,636 Religare Invesco Short Term Fund - Plan B 1657.2822 6.22% 10.13% 9.13% 7.73% 16,573 CRISIL Short Term Bond Fund Index - -

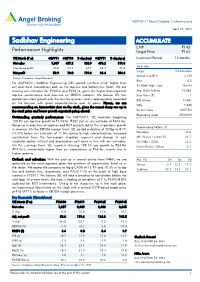

Sadbhav Engineering a CCUMULATE CMP `143 Performance Highlights Target Price `161

4QFY2011 Result Update | Infrastructure April 23, 2011 Sadbhav Engineering A CCUMULATE CMP `143 Performance Highlights Target Price `161 Y/E March (` cr) 4QFY11 4QFY10 % chg (yoy) 3QFY11 % chg (qoq) Investment Period 12 Months Net sales 1,047 457.2 128.9 476.2 119.8 Stock Info Operating profit 90.8 54.4 67.1 52.9 71.8 Sector Infrastructure Net profit 53.9 18.0 199.3 26.4 104.4 Market Cap (` cr) 2,140 Source: Company, Angel Research Beta 0.5 For 4QFY2011, Sadbhav Engineering (SEL) posted numbers much higher than our and street expectations both on the top-line and bottom-line fronts. We are 52 Week High / Low 164/94 revising our estimates for FY2012 and FY2013, given the higher-than-expected Avg. Daily Volume 19,468 top-line performance and pressure on EBITDA margins. We believe SEL has Face Value (` ) 1 posted consistent growth over the last few quarters and is appropriately rewarded BSE Sensex 19,602 on the bourses with great outperformance over its peers. Hence, we are Nifty 5,885 recommending an Accumulate view on the stock, given the recent sharp run up in the stock price and lower growth expected going ahead. Reuters Code SADE.BO Bloomberg Code SADE@IN Outstanding quarterly performance: For 4QFY2011, SEL reported staggering 128.9% yoy top-line growth to `1,047cr (`457.2cr) vs. our estimate of `603.6cr. Ramp-up in execution of captive road BOT projects led to this stupendous growth Shareholding Pattern (%) in revenue. On the EBITDA margin front, SEL posted a decline of 320bp to 8.7% (11.9%) below our estimates of 11.5%, owing to high subcontracting, increased Promoters 47.6 contribution from the low-margin irrigation segment and change in cost MF / Banks / Indian Fls 26.7 escalation policy. -

IRB Toll Road Portfolio IRB’S Portfolio of Road 18 Assets Amount in Rs Mn Adaptability to Changing Market Portfolio Highlights Competitive Advantage Conditions

Investor Presentation March 2020 Safe Harbour 2 This presentation has been prepared by IRB Infrastructure Developers Limited (the “Company”) solely for your information and for your use and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person (whether within or outside your organization or firm) or published in whole or in part, for any purpose. By attending or receiving this presentation, you are agreeing to be bound by the restrictions set forth herein regarding the information disclosed in these materials. The information contained in this presentation does not constitute or form any part of any offer, sale invitation or recommendation to purchase or subscribe for any securities or units in any jurisdiction, and neither the issue of the information nor anything contained herein shall form the basis of, or be relied upon in connection with, any contract or commitment on the part of any person to proceed with any transaction. The information contained in these materials has not been independently verified. No representation or warranty, express or implied, is made and no reliance should be placed on the accuracy, fairness or completeness of the information presented or contained in these materials. Any forward-looking statements in this presentation are subject to risks and uncertainties that could cause actual results to differ materially from those that may be inferred to being expressed in, or implied by, such statements. Such forward-looking statements are not indicative or guarantees of future performance. Any forward-looking statements, projections and industry data included in this presentation are for information only and the Company is not responsible for such statements and projections or for any updates thereto. -

Grant Thornton India LLP

Dealtracker Providing M&A and Private Equity Deal Insights 8th Annual Edition 2012 © Grant Thornton India LLP. All rights reserved. This document captures the list of deals announced based on information available in the public domain and based on public announcements. Grant Thornton India LLP does not take any responsibility for the information, any errors or any decision by the reader based on this information. This document should not be relied upon as a substitute for detailed advise and hence, we do not accept responsibility for any loss as a result of relying on the material contained herein. Further, our analysis of the deal values are based on publicly available information and based on appropriate assumptions (wherever necessary). Hence, if different assumptions were to be applied, the outcomes and results would be different. © Grant Thornton India LLP. All rights reserved. 2 Contents From the 4 - Foreword Editor's Desk 6 - Year Round Up 2012: 10 – M&A Round Up Mergers & 15 – Domestic Acquisitions 17 – Cross border 1001 25 – PE Round Up Private 27 – Top Deals Equity 29 – PE – Sector Highlight 31 – PE – City Break up deals Other 33 – IPO & QIP Features 35 – Deal List $49bn © Grant Thornton India LLP. All rights reserved. 3 Foreword The on-going Eurozone worries, weakening rupee and Contrary to expectations, inbound deal activity reverted a uncertain Indian economy with a slowdown in the to the single-digit levels seen in 2010, notching up US$ reform process, impacted M&A deal activity in certain 7 bn in deal value, after putting in a robust performance periods of 2012. -

Morning Note Market Snapshot

Morning Note Market Snapshot February 26, 2021 Market Snapshot (Updated at 8AM) Key Contents Indian Indices Close Net Chng. Chng. (%) Market Outlook/Recommendation Sensex 51039.31 257.62 0.51 Today’s Highlights Nifty 15097.35 115.35 0.77 Global News, Views and Updates Global Indices Close Net Chng. Chng. (%) Links to important News highlight DOW JONES 31402.01 559.85 1.75 Top News for Today NASDAQ COM. 13119.43 478.54 3.52 FTSE 100 6651.96 7.01 0.11 HCL Technologies: HCL America Inc., a wholly-owned step-down subsidiary of the company has approved the proposal for issuance of U.S. Dollar denominated CAC 40 5783.89 14.09 0.24 unsecured notes aggregating to an amount not exceeding $500 million. The DAX 13879.33 96.67 0.69 Notes are backed by a corporate guarantee of the company. The guarantee is NIKKEI 225 29408.38 762.98 2.53 subject to the aggregate liability of the company not exceeding $525 million, (105 % of the principal amount of the notes). SHANGHAI 3511.69 64.50 1.80 Infosys: Has announced its commitment to add 300 American workers in HANG SENG 29228.64 823.18 2.74 Pennsylvania in continuation of its overall hiring plan in the U.S. The company will recruit for a range of opportunities across technology and digital services, Currency Close Net Chng. Chng. (%) client administration, and operations as it expands its new Retirement Services Center of Excellence. USD / INR 72.43 0.08 0.12 Bank of Baroda: The Board of Directors has approved raising of funds not USD / EUR 1.22 0.00 0.40 exceeding Rs 4,500 crore through issue of equity shares through qualified USD / GBP 1.40 0.01 0.48 institutional placement subject to the approval of the regulatory and statutory USD / JPY 106.16 0.16 0.15 authorities.