Fsimultiform 1..115

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Pn1701 2013 年第 28 期憲報第 6 號副刊 S. No. 6 to Gazette No. 28

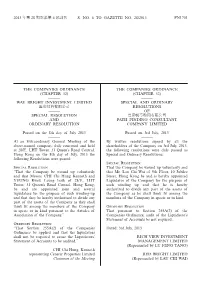

2013 年第 28 期憲報第 6 號副刊 S. NO. 6 TO GAZETTE NO. 28/2013 PN1701 THE COMPANIES ORDINANCE THE COMPANIES ORDINANCE (CHAPTER 32) (CHAPTER 32) ——— ——— WAY BRIGHT INVESTMENT LIMITED SPECIAL AND ORDINARY 匯亮投資有限公司 RESOLUTIONS ——— OF SPECIAL RESOLUTION 巴富帆亭顧問有限公司 AND PATH FINDING CONSULTANT ORDINARY RESOLUTION COMPANY LIMITED ——— ——— Passed on the 8th day of July 2013 Passed on 3rd July, 2013 ——— ——— At an Extraordinary General Meeting of the By written resolutions signed by all the above-named company, duly convened and held shareholders of the Company on 3rd July, 2013, at 28/F., LHT Tower, 31 Queen’s Road Central, the following resolutions were duly passed as Hong Kong on the 8th day of July, 2013 the Special and Ordinary Resolutions:— following Resolutions were passed:— Special Resolution Special Resolution That the Company be wound up voluntarily and “That the Company be wound up voluntarily that Mr. Lau Chi Wai of 9th Floor, 10 Jubilee and that Messrs. CHI Chi Hung Kenneth and Street, Hong Kong be and is hereby appointed YEUNG Kwok Leung both of 28/F., LHT Liquidator of the Company for the purpose of Tower, 31 Queen’s Road Central, Hong Kong, such winding up and that he is hereby be and are appointed joint and several authorized to divide any part of the assets of liquidators for the purpose of such winding-up the Company as he shall think fit among the and that they be hereby authorised to divide any members of the Company in specie or in kind. part of the assets of the Company as they shall think fit among the members of the Company Ordinary Resolution in specie or in kind pursuant to the Articles of That pursuant to Section 255A(2) of the Association of the Company.” Companies Ordinance, audit of the Liquidator’s Statement of Accounts be not required. -

Hong Kong Island Asking Rates / Oct 2017

Hong Kong Island LKF 29 (Onfem Tower) $46 Sunlight Tower $38 - $43 Lucky Building $34 - $38 Sunshine Plaza Full Lyndhurst Tower $45 Tai Tung Building $45 Asking Rates / Oct 2017 Man Yee Building $83 - $88 Tai Yau Building $40 - $45 New Henry House Full Tai Yip Building $32 - $34 New World Tower 1 & 2 $75 - $78 Tesbury Centre Full Nexxus Building $78 The Hennessy $33 Sheung Wan / Central West One / Two Exchange Square $165 The Phoenix $38 Three Exchange Square Full The Sun’s Group Centre $38 - $40 69 Jervois Street $30 - $32 One / Two IFC $170+ Times Media Centre $33 135 Bonham Strand Trade Centre $27 - $29 On Hing Building Full Trust Tower $26 - $28 181 Queens Road Central $50 - $55 Pacific House Full Tung Wai Commercial Building $30 235 Wing Lok Street Trade Centre Full Pacific Place One & Two $145 W Square $38 238 Des Voeux Road Central Full Parker House Full Wu Chung House Full 299 Queen’s Road Central $28.60 Prince’s Building $135 Yam Tze Commercial Building $25 - $28 Bangkok Bank Building $28 Printing House $70 - $73 Beautiful Group Tower $56 Prosperity Tower Full Causeway Bay BOC Group Life Assurance Building $40 Prosperous Building $40 - $46 Bonham Circus $45 - $55 Regent Centre Full 68 Yee Wo Street $45 Bonham Trade Centre $29 - $34 Ruttonjee Centre / Dina House $50 - $83 Bartlock Centre Full Central 88 $57 Shanghai Commercial Bank Tower Full Causeway Bay Plaza 1 & 2 $41 - $44 Centre Mark II $32 Silver Fortune Plaza Full China Taiping Tower 1 & 2 Full Chao’s Building $28 Somptueux Central $48 Chinachem Leighton Plaza Full China -

Directors and Parties Involved in the Placing

DIRECTORS AND PARTIES INVOLVED IN THE PLACING DIRECTORS Name Residential address Nationality Executive Directors Mr. Tam Wing Ki (談永基) G/F, 99 Fourth Street Chinese (Chairman and chief executive Section L officer) Fairview Park New Territories Hong Kong Mr. Hsu Wing Sang (許永生) Flat 1218, 12/F, Shing Ka House Chinese Kwai Shing East Estate Kwai Chung New Territories Hong Kong Mr. Tao Hong Ming (陶康明) Flat A, 31/F, Block 12 Chinese Discovery Park Tsuen Wan New Territories Hong Kong Non-executive Director Mr. Chau Wai Hung, Andy Room 1905, Shek Cheung House Chinese (周煒雄) Shek Lei Estate Kwai Chung New Territories Hong Kong –56– DIRECTORS AND PARTIES INVOLVED IN THE PLACING Name Residential address Nationality Independent non-executive Directors Mr. Cheng Yuk Kin (鄭煜健) Flat 1809, Tower 2 Chinese Harbourview Horizon 12 Hung Lok Road Hung Hom Bay, Kowloon Hong Kong Mr. Fan Chun Wah, Andrew Room E, 22/F, Block 38 Chinese (范駿華) Laguna City 11 South Laguna Street Kwun Tong, Kowloon Hong Kong Ms. Reina Lim Yan Xin Flat 3011, Block R Singaporean (林延芯) Kornhill Quarry Bay Hong Kong See “Directors and Senior Management” for further details of our Directors and senior management. –57– DIRECTORS AND PARTIES INVOLVED IN THE PLACING PARTIES INVOLVED IN THE PLACING Sponsor Quam Capital Limited 18/F-19/F, China Building 29 Queen’s Road Central Hong Kong Joint Lead Managers Quam Securities Company Limited 18/F-19/F, China Building 29 Queen’s Road Central Hong Kong Pacific Foundation Securities Limited 11/F, New World Tower II 16-18 Queen’s Road Central Hong Kong Sole Bookrunner Pacific Foundation Securities Limited 11/F, New World Tower II 16-18 Queen’s Road Central Hong Kong Legal advisers to our Company As to Hong Kong law Tung & Co. -

Participating Restaurants 參與餐廳

Participating Restaurants 參與餐廳 11/6/2021 - 19/12/2021 Restaurant 餐廳 Address 地址 1441 FOURTEEN FORTYONE Ground floor, 41 Peel Street, Central 中環卑利街41號地下 404plant G/F, 109 Jervois Street, Sheung Wan 上環蘇杭街109號地下 Base8 - Coffee.Dining.Salon 1/F 8 Cleveland Street. Causeway Bay. Base8 - 咖啡.餐廳.沙龍 銅鑼灣加寧街8號1樓 Burgeroom Shop D, G/F, 50-56 Paterson Street, Fashion Walk, Causeway Bay, Hk 銅鑼灣百德新街50-56號地下D鋪 Café Circles 9/F Nina Hotel Tsuen Wan West, 8 Yeung Uk Road, Tsuen Wan, Hong Kong 荃灣楊屋道8號荃灣西如心酒店 9樓 canton pot 2/F, Lodgewood by Nina Hospitality | Mong Kok, 1131 Canton Road, Mong Kok 旺角廣東道1131號旺角薈賢居2樓 DALLOYAU 1. Shop 325B, L3, Pacific Place, Admiralty 金鐘太古廣場L3層325B號舖 2. Shop C, G/F, Entertainment Building, 30 Queen’s Road Central 中環皇后大道中30號娛樂行地面C舖 Dynasty Garden Level 1, Goldin Financial Global Centre, 17 Kai Cheung Road, Kowloon Bay, 皇御園 Hong Kong 九龍灣啓祥道17號高銀金融國際中心1樓 forte 2/F, Nina Hotel Kowloon East, 38 Chong Yip Street, Kwun Tong 觀塘創業街38號九龍東如心酒店2樓 LE PAN Ground Floor, Goldin Financial Global Centre, 17 Kai Cheung Road, Kowloon Bay, Hong Kong 九龍灣啟祥道17號高銀金融國際中心地下 Matsunichi Level 2, Goldin Financial Global Centre, 17 Kai Cheung Road, Kowloon Bay, 大松日 Hong Kong 九龍灣啓祥道17號高銀金融國際中心2樓 Megan's Kitchen 5/F Lucky Centre, 165-171 Wan Chai Road, Wan Chai 美味廚 香港灣仔道165-171樂基中心5樓 Nice Yakiniku & Fine Wine 7/F, Aura on Pennington, 66 Jardine's Bazaar, Causeway Bay 佳牛美酒 香港銅鑼灣渣甸街66號Aura on Pennington 7樓 Ru 7/F Nina Hotel Tsuen Wan West, 8 Yeung Uk Road, Tsuen Wan, Hong Kong 如 香港荃灣楊屋道8號荃灣西如心酒店 7樓 16/9/2021 AXP Internal 1 Sen88 Japanese Restaurant G/F & 1/F, -

Name of Buildings Awarded the Quality Water Supply Scheme for Buildings – Fresh Water (Plus) Certificate (As at 8 February 2018)

Name of Buildings awarded the Quality Water Supply Scheme for Buildings – Fresh Water (Plus) Certificate (as at 8 February 2018) Name of Building Type of Building District @Convoy Commercial/Industrial/Public Utilities Eastern 1 & 3 Ede Road Private/HOS Residential Kowloon City 1 Duddell Street Commercial/Industrial/Public Utilities Central & Western 100 QRC Commercial/Industrial/Public Utilities Central & Western 102 Austin Road Commercial/Industrial/Public Utilities Yau Tsim Mong 1063 King's Road Private/HOS Residential Eastern 11 MacDonnell Road Private/HOS Residential Central & Western 111 Lee Nam Road Commercial/Industrial/Public Utilities Southern 12 Shouson Hill Road Private/HOS Residential Central & Western 127 Repulse Bay Road Private/HOS Residential Southern 12W Commercial/Industrial/Public Utilities Tai Po 15 Homantin Hill Private/HOS Residential Yau Tsim Mong 15W Commercial/Industrial/Public Utilities Tai Po 168 Queen's Road Central Commercial/Industrial/Public Utilities Central & Western 16W Commercial/Industrial/Public Utilities Tai Po 17-19 Ashley Road Commercial/Industrial/Public Utilities Yau Tsim Mong 18 Farm Road (Shopping Arcade) Commercial/Industrial/Public Utilities Kowloon City 18 Upper East Private/HOS Residential Eastern 1881 Heritage Commercial/Industrial/Public Utilities Yau Tsim Mong 211 Johnston Road Commercial/Industrial/Public Utilities Wan Chai 225 Nathan Road Commercial/Industrial/Public Utilities Yau Tsim Mong Name of Buildings awarded the Quality Water Supply Scheme for Buildings – Fresh Water (Plus) -

Retail Leasing Savills Research

Hong Kong – January 2021 MARKET IN MINUTES Retail Leasing Savills Research Savills team Please contact us for further information RETAIL Nick Bradstreet Managing Director Head of Leasing +852 2842 4255 [email protected] Barrie Chan Deputy Senior Director +852 2842 4527 A grim 2020 draws to a close [email protected] A raft of poor economic data alongside travel restrictions meant a muted end RESEARCH to the year and a much more pragmatic attitude from landlords. Simon Smith Senior Director • The rate of decline in retail sales slowed further in October Asia Pacifi c during the fourth wave of COVID-19. “ While rents may continue +852 2842 4573 [email protected] • F&B continues to take up space as landlords are keen to to slip over the fi rst half of Kathy Lee sign up crowd-pulling concepts to support footfall in major this year, we can see some Director Retail Consultancy malls. Beyond F&B, market activity remains very low. activity returning after +852 2842 4591 [email protected] • Shopping centre landlords are now reconciled to market Chinese New Year with a Savills plc conditions and becoming more fl exible in both asking rents Savills is a leading global real and lease terms. estate service provider listed on market turnaround likely in the London Stock Exchange. The company established in 1855, has 2022.” a rich heritage with unrivalled • Amidst a sluggish leasing market, both prime street shop growth. It is a company that leads rather than follows, and now has rents and base rents of major shopping centres fell by -5.9% SIMON SMITH, SAVILLS RESEARCH over 600 offi ces and associates throughout the Americas, Europe, QoQ in Q4/2020. -

HONG KONG OTHER RECOMMENDED HOTELS 3 2 1 the Peninsula 5 2 Sheraton 4 3 3 Intercontinental 4 Metropark Hotel

7 LEGEND Nathan Road TSIM 6 SHA TSUI 3 MAYER BROWN JSM OFFICES China Ferry 1 Prince’s Building Terminal Canton Road Cameron Road 2 Infinitus Plaza HOTELS WITH SPECIAL RATES* 4 2 1 Hotel LKF (Central) Mody Road 2 Landmark Mandarin Oriental (Central) Chatham Road 3 Mandarin Oriental Hotel (Central) 1 Tsim Sha Tsui 4 Upper House (Admiralty) Station Salisbury Road INTA 2014 5 J.W. Marriott Hotel (Admiralty) 2 Ocean 1 1 6 Conrad Hotel (Admiralty) Terminal MAP OF HONG KONG OTHER RECOMMENDED HOTELS 3 2 1 The Peninsula 5 2 Sheraton 4 3 3 InterContinental 4 Metropark Hotel Star Ferry Pier 5 Grand Hyatt 6 Renaissance Harbour View Hotel 7 Novotel Century Hotel KEY TOURIST ATTRACTIONS Macau Ferry Terminal 1 1881 Heritage 2 Clock Tower 3 Hong Kong Space Museum 4 Hong Kong Museum of Art Central Government Pier Victoria Harbour 5 Avenue of Stars SHEUNG Pier 2 6 Hong Kong Museum of History Pier 3 Ferries to 6 Discovery Bay Pier 4 Ferries to 7 Hong Kong Science Museum WAN Lamma Island Pier 5 Ferries to 2 Cheung Chau 8 Dr Sun Yat-sen Museum C Central Ferry Piers Pier 6 9 Man Mo Temple Exit E5 onn a Ferries to ug Lantau & Peng Chau 10 The Peak - Sky Terrace 428 h Pier 7 t R Star Ferry Pier D o Pier 8 11 Zoological & Botanical Gardens e ad Sheung Wan s V C Airport Express/ 12 Government House o e Pier 9 Station e n 13 Court of Final Appeal ux t Hong Kong Station Causeway 5 R ra (The Former French Mission Building) oa l 8 Pier 10 Bay 7 d 14 Peak Tram C Typhoon 9 e 15 Hong Kong Park n Bus 17 Shelter H tr 16 High Court ollyw a Terminal o l 17 Golden Bauhinia -

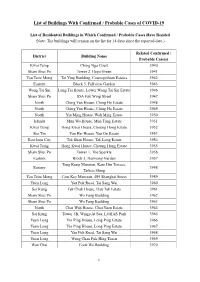

List of Buildings with Confirmed / Probable Cases of COVID-19

List of Buildings With Confirmed / Probable Cases of COVID-19 List of Residential Buildings in Which Confirmed / Probable Cases Have Resided (Note: The buildings will remain on the list for 14 days since the reported date.) Related Confirmed / District Building Name Probable Case(s) Yuen Long Hop Wo Yu Tong, Mai Po 3671 Yuen Long Hop Wo Yu Tong, Mai Po 3672 Yuen Long Ma Tin Tsuen 3673 Renaissance Hong Kong Harbour View Wan Chai 3676 Hotel Wan Chai Hennessy Apartments 3678 Kowloon City Tower 9, Mantin Heights 3679 Yau Tsim Mong Dorsett Mongkok, Hong Kong 3680 Sai Kung Block 6, Metro Town 3681 Tuen Mun Block 6, Bauhinia Garden 3682 Sha Tin Shek Kwu Lung Village 3684 Tsuen Wan Nanking House, Tsuen Wan Centre 3685 Eastern Tower 3, Fleur Pavilia 3686 Kwai Tsing Block 1, Kwai Shing West Estate 3687 Sham Shui Po 12 Wing Lung Street 3688 Yuen Long Yuen Kong Tsuen 3689 Tuen Mun On Hei House, Siu Hei Court 3690 Tuen Mun Block 4, Lung Mun Oasis 3691 Eastern Block C, Sun Sing Centre 3692 Kowloon City Tower 1, Grand Waterfront 3693 Kwun Tong Yuk Mei House, Yau Chui Court 3694 Wong Tai Sin Chui Yuen House, Chuk Yuen South Estate 3695 Wong Tai Sin Chui Yuen House, Chuk Yuen South Estate 3696 Southern Tower 8, Marinella 3697 Block 3, Bamboo Mansions, Whampoa Kowloon City 3698 Garden Block 3, Bamboo Mansions, Whampoa Kowloon City 3699 Garden Kwun Tong Lei Yan House, Lei On Court 3700 Kwun Tong Kai Ning House, Kai Yip Estate 3701 Yau Tsim Mong Rear Block, Man Ying Building 3702 1 Related Confirmed / District Building Name Probable Case(s) Kwai Tsing On -

List of Licensed Banks Which Are Not Currently Issuing and Facilitating the Issue Of

List of licensed banks which are not currently issuing and facilitating the issue of SVF Licence Effective Date Name of Licenced Bank (in alphabetical order) Address of the Principal Place of Business in Hong Kong Number (dd/mm/yyyy) ABN AMRO BANK N.V. UNITS 7001-06 & 7008B, LEVEL 70, INTERNATIONAL COMMERCE CENTRE, 1 AUSTIN ROAD WEST, KOWLOON, HONG KONG. SVFB299 13/11/2016 AGRICULTURAL BANK OF CHINA LIMITED 25/F, AGRICULTURAL BANK OF CHINA TOWER, 50 CONNAUGHT ROAD CENTRAL, HONG KONG. SVFB235 13/11/2016 AIRSTAR BANK LIMITED SUITES 3201-07, TOWER 5, THE GATEWAY, HARBOUR CITY, TSIM SHA TSUI, KOWLOON SVFB329 09/05/2019 ANT BANK (HONG KONG) LIMITED SUITES 2312-13, 23/F, TOWER ONE, TIMES SQUARE, 1 MATHESON STREET, CAUSEWAY BAY, HONG KONG SVFB331 09/05/2019 AUSTRALIA AND NEW ZEALAND BANKING GROUP LIMITED 22/F, THREE EXCHANGE SQUARE, 8 CONNAUGHT PLACE, CENTRAL, HONG KONG. SVFB164 13/11/2016 AXIS BANK LIMITED SUITE 1707-1708, CENTRAL PLAZA, 18 HARBOUR ROAD, WANCHAI, HONG KONG SVFB281 13/11/2016 BANCO BILBAO VIZCAYA ARGENTARIA S.A. UNIT 9507, LEVEL 95, INTERNATIONAL COMMERCE CENTRE, 1 AUSTIN ROAD WEST, KOWLOON. SVFB157 13/11/2016 BANCO SANTANDER, S.A. 10/F, TWO INTERNATIONAL FINANCE CENTRE, 8 FINANCE STREET, CENTRAL, HONG KONG. SVFB289 13/11/2016 BANGKOK BANK PUBLIC COMPANY LIMITED BANGKOK BANK BUILDING, 28 DES VOEUX ROAD, CENTRAL, HONG KONG. SVFB036 13/11/2016 BANK J. SAFRA SARASIN AG 40/F, EDINBURGH TOWER, THE LANDMARK, 15 QUEEN'S ROAD CENTRAL, HONG KONG. SVFB297 13/11/2016 BANK JULIUS BAER & CO. LTD. 39/F, ONE INTERNATIONAL FINANCE CENTRE, 1 HARBOUR VIEW STREET, CENTRAL, HONG KONG. -

List of Buildings with Confirmed / Probable Cases of COVID-19

List of Buildings With Confirmed / Probable Cases of COVID-19 List of Residential Buildings in Which Confirmed / Probable Cases Have Resided (Note: The buildings will remain on the list for 14 days since the reported date.) Related Confirmed / District Building Name Probable Case(s) Kwai Tsing Ching Nga Court 3940 Sham Shui Po Tower 2, Heya Green 3941 Yau Tsim Mong Tai Ying Building, Cosmopolitan Estates 3942 Eastern Block 3, Fullview Garden 3943 Wong Tai Sin Lung Tai House, Lower Wong Tai Sin Estate 3946 Sham Shui Po 85A Fuk Wing Street 3947 North Ching Yun House, Ching Ho Estate 3948 North Ching Yun House, Ching Ho Estate 3949 North Yiu Ming House, Wah Ming Estate 3950 Islands Mun Wo House, Mun Tung Estate 3951 Kwai Tsing Hong Kwai House, Cheung Hong Estate 3952 Sha Tin Yan Hei House, Yan On Estate 3953 Kowloon City Tak Shan House, Tak Long Estate 3954 Kwai Tsing Hong Kwai House, Cheung Hong Estate 3955 Sham Shui Po Tower 1, The Sparkle 3956 Eastern Block 3, Harmony Garden 3957 Tang Kung Mansion, Kam Din Terrace, Eastern 3958 Taikoo Shing Yau Tsim Mong Cam Key Mansion, 489 Shanghai Street 3959 Yuen Long Yau Pok Road, Tai Sang Wai 3960 Sai Kung Tak Chak House, Hau Tak Estate 3961 Sham Shui Po Wo Fung Building 3962 Sham Shui Po Wo Fung Building 3963 North Choi Wah House, Choi Yuen Estate 3964 Sai Kung Tower 5B, Wings At Sea, LOHAS Park 3965 Yuen Long Yin Ping House, Long Ping Estate 3966 Yuen Long Yin Ping House, Long Ping Estate 3967 Yuen Long Yau Pok Road, Tai Sang Wai 3968 Yuen Long Wang Chau Fuk Hing Tsuen 3969 Wan Chai Fook Wo Building -

Hk-New-Retail-Beauty.Pdf

The hyperlinks of merchant websites will bring to you to another website on the Internet, which is published and operated by a third party. Such links are only provided on our website for the convenience of the Client and Standard Chartered Bank does not control or endorse such websites, and is not responsible for their contents. The use of such websites is also subject to the terms of use and other terms and guidelines, if any, contained within each such website. In the event that any of the terms contained herein conflict with the terms of use or other terms and guidelines contained within any such websites, then the terms of use and other terms and guidelines for such website shall prevail. Offers are applicable for Standard Chartered Visa Credit Card Offers are applicable for Standard Chartered Mastercard Offers are applicable for Standard Chartered UnionPay Dual Currency Platinum Credit Card Offers are applicable for Standard Chartered WorldMiles Card Merchants Offers Details and Merchant's Additional Terms and Conditions Contact Details ℃ (852) 2831 4886 32 15/F, SOGO Club, East Point Centre New Wing, 555 Hennessy 10% off on regular-priced items Road, Causeway Bay, Hong Kong Special price of HK$280 on the first trial of Contour Tightening Mask Treatment (valued at HK$980) Promotion period is from 1 Jan to 31 Dec 2017. Offers of treatment are only applicable to new customers. Offers cannot be used in conjunction with any other promotional offers, discounts and cash coupons. Treatment offer can only be enjoyed once per customer. Prior reservation is required and booking of treatment cannot be changed. -

List of Licensed Banks Which Are Not Currently Issuing and Facilitating The

List of licensed banks which are not currently issuing and facilitating the issue of SVF Licence Effective Date Name of Licenced Bank (in alphabetical order) Address of the Principal Place of Business in Hong Kong Number (dd/mm/yyyy) ABN AMRO BANK N.V. LEVEL 70, INTERNATIONAL COMMERCE CENTRE, 1 AUSTIN ROAD WEST, KOWLOON, HONG KONG. SVFB299 13/11/2016 AGRICULTURAL BANK OF CHINA LIMITED 25/F, AGRICULTURAL BANK OF CHINA TOWER, 50 CONNAUGHT ROAD CENTRAL, HONG KONG. SVFB235 13/11/2016 ALLAHABAD BANK 1908-09, TOWER ONE, LIPPO CENTRE, 89 QUEENSWAY, ADMIRALTY, HONG KONG. SVFB275 13/11/2016 AUSTRALIA AND NEW ZEALAND BANKING GROUP LIMITED 22/F, THREE EXCHANGE SQUARE, 8 CONNAUGHT PLACE, CENTRAL, HONG KONG. SVFB164 13/11/2016 AXIS BANK LIMITED SUITE 1707-1708, CENTRAL PLAZA, 18 HARBOUR ROAD, WANCHAI, HONG KONG SVFB281 13/11/2016 BANCA MONTE DEI PASCHI DI SIENA S.P.A. 2305-13, 23RD FLOOR, CITIC TOWER, 1 TIM MEI AVENUE, CENTRAL, HONG KONG. SVFB246 13/11/2016 BANCO BILBAO VIZCAYA ARGENTARIA S.A. UNIT 9507, LEVEL 95, INTERNATIONAL COMMERCE CENTRE, 1 AUSTIN ROAD WEST, KOWLOON. SVFB157 13/11/2016 BANCO SANTANDER, S.A. 10/F, TWO INTERNATIONAL FINANCE CENTRE, 8 FINANCE STREET, CENTRAL, HONG KONG. SVFB289 13/11/2016 BANGKOK BANK PUBLIC COMPANY LIMITED BANGKOK BANK BUILDING, 28 DES VOEUX ROAD, CENTRAL, HONG KONG. SVFB036 13/11/2016 BANK J. SAFRA SARASIN AG 40/F, EDINBURGH TOWER, THE LANDMARK, 15 QUEEN'S ROAD CENTRAL, HONG KONG. SVFB297 13/11/2016 BANK JULIUS BAER & CO. LTD. 39/F, ONE INTERNATIONAL FINANCE CENTRE, 1 HARBOUR VIEW STREET, CENTRAL, HONG KONG.