Statement of Accounts 2015/2016 Audited Version September 2016

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Engagement and Involvement of Children and Young People with Special Educational Needs and Disabilities (SEND)

Meeting: Corporate Parenting Panel Date: 1 December 2014 Subject: Engagement and Involvement of Children and Young People with Special Educational Needs and Disabilities (SEND) Report of: Sue Harrison, Director of Children’s Services Summary: The report set out how Children’s Services are responding to the requirements of the Children and Families Act 2014, to include children and young people with SEND in the development of the Local Offer. Local authorities must publish a Local Offer, setting out in one place information about provision they expect to be available across education, health and social care for children and young people in their area in their area who have Special Educational Needs or are disabled. Contact Officer: Ken Harvey, Head of Service, Children with Disabilities. Public/Exempt: Public Wards Affected: All Function of: Council CORPORATE IMPLICATIONS Council Priorities: Central Bedfordshire Council’s Strategic Plan 2012-16 Priority 3 – Promote health and wellbeing and protecting the vulnerable The Children and Young People’s Plan 2011-2014 Priority 2 – Protecting children and keeping them safe. Financial: 1. The work has been commissioned and monitored by the Head of Service, Children with Disabilities and funded from core budget. The work is monitored through the Support and Aspiration Board (Work stream 2 :The Engagement and Involvement of Children and Young People with SEND) 2. Further funding will be required to continue the development work and a bid will be made to the Support and Aspiration Board, against the SEND transformation grant, to support the children and young people’s contribution to the Local Offer and for ensuring that a forum to support development through the SEND reforms is established. -

Annual Reports

Annual Report 2016-17 Gathering on the Green - July 2016 Community Litter Pick – March 2017 Brickhill – Annual Parish Meeting St Marks Church and Community Centre, Calder Rise, Brickhill, Thursday 16th March 2017 Annual Overview by Cllr Mark Fitzpatrick, Chairman of Brickhill Parish Council Introduction Welcome to St Mark’s for the 13th Annual Parish Meeting for Brickhill. The Annual Parish Meeting is not a council meeting. It is intended to enable parish electors and local organisations, including the parish council, to meet and discuss items of interest or concern. We can share news of what has happened over the past year and what is planned for the future, as well as allowing residents to ask questions. Work of the Parish Council 2016/2017 Over the past year, the parish council met 10 times. There have also been meetings of its Planning Committee, Allotments and Open Spaces Committee and other groups. The agendas and minutes of these meetings are available on the parish website. Residents are welcome to all meetings of the council and its committees. During the past year there have been three parish councillor vacancies. Nick Carter had been co-opted in early 2016 and sadly died in December 2016. He had made a strong contribution to the council during his short time with us. His fellow councillors made a donation to the PEPS team at St John’s, Moggerhanger, in his memory. The vacancy will be filled by Lynne Seymour. Alex Chrusiack resigned when he moved out of the area, with James Cross elected in October 2016 to replace him. -

NQT Enrichment Programme 2016-17

NQT enrichment programme 2016-17 In addition to their in-school training and support, all NQTs registered with Central Bedfordshire Council are entitled to attend after-school enrichment events which run throughout the county. These events are run by very experienced practitioners and are designed to share best practice, provide new ideas and a space for reflection, networking and exchanging experiences. Events start at 4.00 pm and end by 5.45pm. Booking is essential and can be done via CPD Online: www.centralbedscpd.co.uk. Cross-phase events – open to all NQTs Inspiring teaching and learning for all This cross-phase event will provide a chance to try out innovative approaches and creative ideas for engaging all learners. We will explore the qualities of inspirational teachers and how to develop the confidence to take a risk. The course will be facilitated by one primary and one secondary practitioner. Who is it Focus on Teachers’ Where will it run? When? for? Standards Vandyke Upper School, Vandyke Road, Wednesday 12 Leighton Buzzard, LU7 3DY October NQTs Greenfield C of E School, Pulloxhill Road, Wednesday 23 working in 1,2,3,4 Greenfield, Bedford, MK45 5ES November all phases Stratton Upper School, Eagle Farm Road, Tuesday 10 Biggleswade, SG18 8JB January Supporting the progress of pupils with SEND This is a cross-phase event which will help NQTs explore planning for the effective use of support staff, understand four broad areas of need and make referrals for more support. Who is it Focus on Teachers’ Where will it run? When? for? Standards Samuel Whitbread Academy, Shefford Wednesday 22 NQTs Road, Clifton, Shefford,, SG17 5QS February 2017 working in 5 Vandyke Upper School, Vandyke Road, all phases TBC March 2017 Leighton Buzzard, LU7 3DY Working with more able pupils Why we must provide for more able pupils, how to identify them and effective ways of differentiating. -

BCL July 15 Newsletter.Indd

Bedfordshire Cricket Ltd driving and inspiring cricket JULY 2015 Bedfordshire young talent ECB U15 National Club Luton T20 Lord’s Taverners City County Under 14s captain and Bedford Cricket Club Championship County winners Cup Competition opening batsman Rahul Sheemar has been awarded a two-year place on Essex County Cricket Club’s academy programme. Essex academy director John Childs has been impressed with Rahul’s ability and attitude during this winter’s Emerging Player Programme (EPP), which has been run in conjunction with Cambs, Hunts and Su olk and supported by Essex CCC. Childs drew comparisons to a young Alistair Cook who, like Sheemar, attended Bedford school, captained and is a left handed opener. Cook also went through the Essex Academy. Sheemar’s success doesn’t stop there: he has been selected to represent London and East at the prestigious U15 The Under 15 County Final was recently contested between Bunbury Festival despite still being under 14. The Festival, which brings together Pictured: Competition organiser Brad Matthews with man of the Match Sharks’ Yasin Khan Bedford Cricket Club and Luton Town & Indians Cricket Club with the best talent in country, has been running for 29 years and has seen 62 players The competition got underway in June with players from throughout Bedfordshire go on and play for England and 702 play fi rst-class cricket. The Festival runs Bedford winning by 8 wickets. Bedford now go through to the National Knock-Out Competition. They have a bye in the fi rst round taking part in four teams – Luton Lions, Pumas, Sharks and Tigers. -

07 Appendix C Review of Polling Districts and Places V2

APPENDIX C CURRENT AND PROJECTED DATA, RESPONSES TO STAKEHOLDER COMMENTS AND ARO’s RECOMMENDATIONS Ampthill Ward Polling PD Polling Electorate Polling Station Recommendation Place Ref. District 2013 2018 The Firs Lower School, Station Road, To create a more even number of electors at each AMP1-4 AMP1 Ampthill (part) 2,131 2,510 Ampthill MK45 2QR polling station and to accommodate the projected Ampthill Baptist Church, Dunstable growth in the number of electors, the ARO AMP1-4 AMP2 Ampthill (part) 1,543 1,553 Street, Ampthill MK45 2JS RECOMMENDS that the polling district Russell Lower School, Queens Road boundaries in Ampthill be redrawn to create an AMP1-4 AMP3 Ampthill (part) (access via Saunders Piece entrance), 1,398 1,777 additional polling district (AMP5) and that two new Ampthill MK45 2TD polling stations be used – Ampthill Library and The Wingfield Club – which will be more convenient for electors in the new polling districts. This would necessitate discontinuing the use of Ampthill Baptist Church. The ARO was asked to consider using the Town Ampthill Methodist Church Room, Council Chamber, 66 Dunstable Street, Ampthill AMP1-4 AMP4 Ampthill (part) 887 896 Chandos Road, Ampthill MK45 2JS as a polling station but the Methodist Church Room is more convenient for voters and has parking advantages. The current polling districts AMP5 to AMP7 will be re-indexed. The streets and polling stations in the new Ampthill polling districts are set out below. Clophill Methodist Church, High Street, AMP5 AMP5 Clophill 1,409 1,460 No changes other -

Bedford Borough Schools 2018

Establishment Guide A list of Bedford Borough Schools contact details September 2018 Children’s Services Establishment Guide - September 2018 Contents Nursery Schools 3 Lower Schools 4 Primary Schools 5 Middle Schools 14 Secondary Schools 15 Upper School 17 Special Schools 17 PRU 17 2 Establishment Guide - September 2018 Nursery Schools Cherry Trees Nursery School School Phase Category Hawkins Road, Bedford, MK42 9LS Age Range Head: Mrs I Davis Nursery Community Tel: (01234) 354788 Up to 5 years e-mail: [email protected] website: www.cherrytreesnurseryschool.com Peter Pan Nursery School School Phase Category Edward Road, Bedford, MK429DR Age Range Head: Mrs I Davis Nursery Community Tel: (01234) 350864 Up to 5 years e-mail: [email protected] website: www.peterpannurseryschool.com 3 Establishment Guide - September 2018 Lower Schools Broadmead Lower School School Phase Category Park Crescent, Stewartby, Bedford, MK43 9NN Age Range Head: Mrs K Hewlett Lower Community Tel: (01234) 768318 Fax: (01234) 768800 Up to 9 years e-mail: [email protected] website: www.broadmeadlower.beds.sch.uk Wootton Lower School (Dual Site) School Phase Category Bedford Road, Wootton, Bedford, MK43 9JT Age Range Harris Way, Wootton, Bedford, MK43 9FZ Head: Mr C Tavener Lower Community Tel: (01234) 768239 Up to 9 years e-mail: [email protected] website: www.woottonlowerschool.org 4 Establishment Guide - September 2018 Primary Schools Balliol Primary School School Phase Category Balliol Road, Kempston, -

Gardening Club Plant Sale Aley Green Pepperstock Slip End Woodside PARISH NEWS July 2017

Aley Green Pepperstock Slip End Woodside PARISH NEWS July 2017 Gardening Club Plant Sale and our much-loved village is preserved Editors’ Notes just the way it is for generations to come. If you want a reminder of what it is that Make no mistake, the future of our village makes Slip End so special, you only have hangs on a thread. to pop along to the Village Day in a Plans by Central Bedfordshire Council, week’s time, a perfect showcase for and private firm Legal and General, could everything great about where we live. both transform Slip End forever. Reminder: There is no Parish News in The intimate community we know and August so the next issue will be love faces becoming a suburb of Luton, September. Please have any items to the or even the development of its Editor for that issue (Alison) by 15th surrounding Green Belt fields, under August. proposals mooted by both of these organisations. It’s easy to sit back and think that nothing will come of either suggestion, but apathy (The cover photos show some of the is never the answer. Gardening Club Committee and the Plant Instead, get involved and speak out now Sale set up ready to go. Pictured below is to ensure the status quo is maintained the GNS stall at last year’s Village Day.) 2 Make sure you have Village Day in your diary. We look forward to seeing everyone on Saturday 8th July from 11 until 4 at the Playing Fields in Church Road. This year we have a good selection of stalls, BBQ and bar, teas, coffee and cakes and the ice cream van, and our Grand Raffle with many great prizes. -

Sharnbrook Academy Federation Consultation on Proposed Changes to Age-Ranges, Structures and Admissions

Dear Parents and Carers, Sharnbrook Academy Federation Consultation on proposed changes to age-ranges, structures and admissions Our last update on the structure of the Sharnbrook Academy Federation’s schools was in July. At that time we were looking to consult on change in the summer of 2015. Since then we have continued to work up the detail of these changes. We have also maintained a dialogue with Bedford Borough Council, our feeder lower schools and the St Albans Church of England Diocese. From all that we have heard, we have decided to bring our consultation forward, to shorten the period of uncertainty for parents and staff. We are now therefore publishing our Consultation document today and this can be accessed via the following link http://www.sharnbrook.beds.sch.uk/saf-governance/13589.html. Our proposal is as follows: That Harrold Priory Middle, Margaret Beaufort Middle and Sharnbrook Upper Schools should become a single school, based on the three existing sites, offering provision from age 9 (Year 5) to age 18/19 (Year 13) and that Lincroft School should extend its age-range to become an all-through secondary school offering provision from age 9 (Year 5) to age 16 (Year 11). The consultation will run until 12pm on 27 February 2015. You will have several opportunities in January to meet with us to hear more about our proposal for change. The consultation document is detailed but in summary: The proposal does not affect any lower schools and has the support of Bedford Borough Council Strong Key Stage 2 provision in Years 5 and 6 will continue By bringing Harrold Priory, Margaret Beaufort and Sharnbrook Upper School together and extending the age range at Lincroft, we can deliver a high quality Key Stage 3 curriculum and have Key Stage 3 and Key Stage 4 in one school. -

This Meeting May Be Filmed.*

Central Bedfordshire This meeting may Council Priory House be filmed.* Monks Walk Chicksands, Shefford SG17 5TQ please ask for Martha Clampitt direct line 0300 300 4032 date 16 January 2015 NOTICE OF MEETING SCHOOLS FORUM Date & Time Monday, 26 January 2015 at 9.00 a.m. Venue at Committee Room 2, Watling House, High Street North, Dunstable Richard Carr Chief Executive To: The Chairman and Members of the SCHOOLS FORUM: David Brandon-Bravo, Headteacher, Parkfields Middle School Paul Burrett, Headteacher, Studham CofE Lower School and Pre-School Shirley-Anne Crosbie OBE, Headteacher, The Chiltern School James Davis, Governor, Leighton Middle School Angie Hardy, Headteacher, Clipstone Brook Lower School School Richard Holland, Governor, Harlington Upper School Members: Sue Howley MBE, Governor, Greenleas Lower School Sharon Ingham, Headteacher, Hadrian Academy Jim Parker, Headteacher, Manshead Upper School John Street, Academy Middle School Representative Stephen Tiktin, Governor, Beaudesert Lower School Rob Watson, Headteacher Stratton Upper School Mr M Foster, Trade Union representative Non School Mrs M Morris, Catholic Diocese Representative Members Mrs S Mortimer, Post-16 Education Representative Sarah Stevens, Church of England Diocese Representative Observer: Cllr MAG Versallion, Executive Member for Children’s Services Please note that there will be a pre-meeting starting half an hour before the Forum meeting to enable technical aspects of the reports to be discussed with officers before the Forum meeting begins. *Please note that phones and other equipment may be used to film, audio record, tweet or blog from this meeting. No part of the meeting room is exempt from public filming. The use of arising images or recordings is not under the Council’s control. -

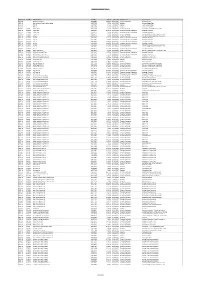

Payments Over £250 Report

BEDFORD BOROUGH COUNCIL Directorate Supplier Supplier Name TransNo Amount Trans.date Expense Area Expense Type ADCHILD Chiltern Properties 10626882 1,823.09 18/07/2017 Transfer Payments Accommodation ADCHILD County Court Money Claims Centre 10627370 255.00 20/07/2017 Supplies Court and Legal Fees ADCHILD HMCTS 10627365 400.00 19/07/2017 Supplies Court and Legal Fees ADCHILD HMCTS 10627366 400.00 20/07/2017 Supplies Court and Legal Fees ADCHILD LILL98 Lillibet House 20172764 7,735.00 12/07/2017 Transfer Payments Residential Care Home Placements ADCHILD 3STA99 3 Star Cars 10625491 12,554.00 06/07/2017 Transport Related Expenditure Passenger Transport ADCHILD 3STA99 3 Star Cars 10626154 606.00 06/07/2017 Transport Related Expenditure Passenger Transport ADCHILD 3STA99 3 Star Cars 10626191 280.00 06/07/2017 Transfer Payments Transport & Meals (Social Services Care) ADCHILD A1CA01 A1 Cars 10623770 434.60 05/04/2017 Transfer Payments Transport & Meals (Social Services Care) ADCHILD A1CA01 A1 Cars 10624950 6,211.60 30/06/2017 Transport Related Expenditure Passenger Transport ADCHILD A1CA01 A1 Cars 10625901 5,468.00 05/07/2017 Transport Related Expenditure Passenger Transport ADCHILD A1CA01 A1 Cars 10626188 2,086.00 06/07/2017 Transport Related Expenditure Passenger Transport ADCHILD A1CA01 A1 Cars 10626190 1,444.00 05/07/2017 Transport Related Expenditure Passenger Transport ADCHILD A1CA01 A1 Cars 10626190 2,478.00 05/07/2017 Transfer Payments Transport & Meals (Social Services Care) ADCHILD A1CA01 A1 Cars 10626193 2,214.00 06/07/2017 Transfer -

Area D Assessments

Central Bedfordshire Council www.centralbedfordshire.gov.uk Appendix D: Area D Assessments Central Bedfordshire Council Local Plan Initial Settlements Capacity Study CENTRAL BEDFORDSHIRE COUNCIL LOCAL PLAN: INITIAL SETTLEMENTS CAPACITY STUDY Appendix IID: Area D Initial Settlement Capacity Assessment Contents Table BLUNHAM .................................................................................................................. 1 CAMPTON ................................................................................................................. 6 CLIFTON ................................................................................................................... 10 CLOPHILL ................................................................................................................. 15 EVERTON .................................................................................................................. 20 FLITTON & GREENFIELD ............................................................................................ 24 UPPER GRAVENHURST ............................................................................................. 29 HAYNES ................................................................................................................... 33 LOWER STONDON ................................................................................................... 38 MAULDEN ................................................................................................................ 42 MEPPERSHALL ......................................................................................................... -

Luton SUE Site Size (Ha): 283.81

Site: NLP426 - North Luton SUE Site size (ha): 283.81 Parcel: NLP426f Parcel area (ha): 89.74 Stage 1 assessment Stage 2 assessment Parcel: L2 Parcel: n/a Highest contribution: Purpose 3 - Strong Contribution: contribution Contribution to Green Belt purposes Purpose Comments Purpose 1: Checking The parcel is located adjacent to the large built up area and development here would relate the unrestricted to the expansion of Luton. The parcel is only separated from the settlement edge to the sprawl of large, built- south by occasional hedgerow trees. However, the low hedgerows, and intermittent up areas hedgerow trees along the remaining boundaries provide little separation between the parcel and the rolling farmland beyond the parcel to the north, west and east, so that despite its proximity to Luton, the parcel relates more strongly to the wider countryside and its release would constitute significant sprawl into the countryside. Purpose 2: The development of the parcel would result in little perception of the narrowing of the gap Preventing the between neighbouring towns because the larger towns to the north of Luton, including merger of Flitwick, are separated by the chalk escarpment running east-west which would limit the neighbouring towns impact. Purpose 3: The proximity of the adjacent residential settlement edge has some urbanising influence on Safeguarding the the parcel particularly as the occasional hedgerow trees on the boundary offer little countryside from separation. However, there is no urban development within the parcel itself and openness encroachment and undulating topography of the parcel give it a stronger relationship with the wider downland countryside.