Comprehensive Annual Financial Report for the Fiscal Year Ended June 30, 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Illinois ... Football Guide

University of Illinois at Urbana-Champaign !~he Quad s the :enter of :ampus ife 3 . H«H» H 1 i % UI 6 U= tiii L L,._ L-'IA-OHAMPAIGK The 1990 Illinois Football Media Guide • The University of Illinois . • A 100-year Tradition, continued ~> The University at a Glance 118 Chronology 4 President Stanley Ikenberrv • The Athletes . 4 Chancellor Morton Weir 122 Consensus All-American/ 5 UI Board of Trustees All-Big Ten 6 Academics 124 Football Captains/ " Life on Campus Most Valuable Players • The Division of 125 All-Stars Intercollegiate Athletics 127 Academic All-Americans/ 10 A Brief History Academic All-Big Ten 11 Football Facilities 128 Hall of Fame Winners 12 John Mackovic 129 Silver Football Award 10 Assistant Coaches 130 Fighting Illini in the 20 D.I.A. Staff Heisman Voting • 1990 Outlook... 131 Bruce Capel Award 28 Alpha/Numerical Outlook 132 Illini in the NFL 30 1990 Outlook • Statistical Highlights 34 1990 Fighting Illini 134 V early Statistical Leaders • 1990 Opponents at a Glance 136 Individual Records-Offense 64 Opponent Previews 143 Individual Records-Defense All-Time Record vs. Opponents 41 NCAA Records 75 UNIVERSITY LIBRARY 78 UI Travel Plans/ 145 Freshman /Single-Play/ ILLINOIS AT URBANA-CHAMPAIGN Opponent Directory Regular Season UNIVERSITY OF responsible for its charging this material is • A Look back at the 1989 Season Team Records The person on or before theidue date. 146 Ail-Time Marks renewal or return to the library Sll 1989 Illinois Stats for is $125.00, $300.00 14, Top Performances minimum fee for a lost item 82 1989 Big Ten Stats The 149 Television Appearances journals. -

Chicago Southland Venue Guide

Chicago Southland SPORTS venue guide With reasonable prices, convenient transportation options, exciting extracurricular activities and a wide variety of easily accessible venues for over 45 sports, the Chicago Southland provides unlimited potential for your next sporting event Just Beyond the City Limits. The Chicago Southland, the 62 south and southwest suburbs of Chicago, is an ideal sporting event and tournament location, conveniently accessible via Interstates 55, 57, 80, 94, 294 and 355, minutes from downtown Chicago and Midway and O’Hare International Airports, making getting to and from your event a breeze. Area 1 Bridgeview, Burbank & Oak Lawn O’HARE AIRPORT MIDWAY Area 2 AIRPORT Chicago Southland . Convention & Visitors Alsip, Crestwood, Oak Forest, 95TH ST Bureau offices BRIDGEVIEW BURBANK OAK LAWN Orland Hills & Orland Park CALUMET PARK WORTH DOLTON CALUMET CITY PALOS ALSIP HILLS CRESTWOOD Area 3 SOUTH HOLLAND HARLEM AVE. Chicago Heights, East Hazel Crest, HARVEY LANSING HALSTED ST Harvey, Homewood & Markham OAK FOREST MARKHAM . EAST HAZEL CREST ORLAND PARK 159TH ST . TINLEY CICERO HOMEWOOD GLENWOOD PARK FLOSSMOOR LAGRANGE RD LINCOLN HWY. Area 4 ORLAND AVE. HILLS OLYMPIA Calumet City, Lansing & South Holland FIELDS CHICAGO WOLF RD. HEIGHTS . PARK HOMER GLEN FOREST Area 5 CRETE Matteson, Mokena & Monee MOKENA MATTESON UNIVERSITY PARK NEW LENOX FRANKFORT Area 6 MONEE BEECHER Tinley Park PEOTONE PlayChicagoSouthland.com 708-895-8200 • 888-895-3211 • Fax 708-895-8288 Joel Koester, Sports Sales Manager [email protected] 2304 173rd Street, Lansing, IL 60438 The information provided in this brochure was compiled by the Chicago Southland Convention & Visitors Bureau based on information materials submitted directly from the organization or business entity. -

Game Locations

WCKYA LEAGUE GAME LOCATIONS Chicago “Cardinals” Marist High School 4200 W 115th St Chicago IL 60655 Go North on Cicero Ave/IL Rte 50 Turn right onto 115th St (.08 miles) To site address 4200 W. 115th. Country Club Hills “Cougars” Country Club Hills Sports Complex 4200 W 175th St Country Club Hills, Illinois Governors Hwy to 175th St, left on 175th St to first parking lot on right. OR Cicero to 175th St, right onto 175th, proceed to third parking lot on left. Kankakee Riverside “Colts” Riverside Sports Complex 1640 Butterfield Trail Kankakee, Illinois Take I-57 south to exit 312. Exit to the right and proceed on Court St. Cross over the river to Wall St. Turn right on Wall St. Go under the viaduct to Butterfield Trail. Turn left on Butterfield Trail and proceed to Riverside Sports Complex (on the left). Markham “Patriots” Roesner Park 16053 Richmond Ave Markham, Illinois From Kedzie and Vollmer take Kedzie North to 163rd Street. Turn right onto 163rd Street, turn left onto Richmond Ave... End at Roesner Park. From Vollmer Rd..traveling north on Cicero or Crawford...travel north to 159th, turn right onto 159th, turn right onto Richmond Ave (Richmond is east of Kedzie)...end at Roesner Park From I-57..take I-57 towards Chicago, exit 159th st, go east on 159th, turn onto Richmond Ave (Richmond is east of Kedzie)...end at Roesner Park From Dixie Hwy and Vollmer Rd..take Dixie Hwy north to 159th St, turn left onto 159th St, turn left onto Richmond Ave (Richmond is west of I-294)...end at Roesner Park Matteson “Bears” Matteson Community Center 20642 Matteson Ave Matteson, Illinois From Allemong Park take Willow Road North to Vollmer Road. -

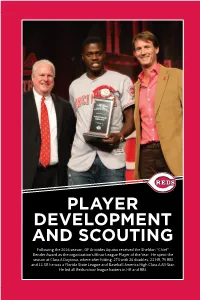

Player Development and Scouting

PLAYER DEVELOPMENT PLAYER DEVELOPMENT AND SCOUTING Following the 2016 season, OF Aristides Aquino received the Sheldon “Chief” Bender Award as the organization’s Minor League Player of the Year. He spent the season at Class A Daytona, where after hitting .273 with 26 doubles, 23 HR, 79 RBI and 11 SB he was a Florida State League and Baseball America High Class A All-Star. He led all Reds minor league batters in HR and RBI. CINCINNATI REDS MEDIA GUIDE 193 PLAYER DEVELOPMENT 2017 PLAYER DEVELOPMENT AND PLAYER SCOUTING PLAYER DEVELOPMENT SCOUTING SUPERVISORS Jeff Graupe ........................Senior Director, Player Development Charlie Aliano ..........................................................South Texas Melissa Hill ........................Coordinator, Baseball Administration Rich Bordi ........................................... Northern California, Reno Mark Heil ........................................Player Development Analyst Jeff Brookens ................................Delaware, Maryland, Virginia, Mike Saverino ................................Arizona Operations Manager Washington DC, Pennsylvania Branden Croteau .... Assistant to Arizona Operations Manager Sean Buckley ....................................................................Florida Charlie Rodriguez ......Assistant to Arizona Operations Manager John Ceprini ........Maine, NH, VT, RI, CT, MA, NYC/Long Island Jonathan Snyder ..................Minor League Equipment Manager Dan Cholowsky ...............Arizona, New Mexico, Utah, Colorado, John Bryk ............................ -

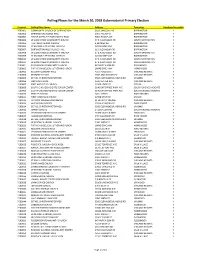

Polling Place List

Polling Places for the March 20, 2018 Gubernatorial Primary Election Precinct Polling Place Name Address Township Handicap Accessible 7000001 COMMUNITY CHURCH OF BARRINGTON 301 E LINCOLN AVE BARRINGTON Y 7000002 BARRINGTON VILLAGE HALL 200 S HOUGH ST BARRINGTON Y 7000003 GROVE AVENUE ELEMENTARY SCHOOL 900 S GROVE AVE BARRINGTON Y 7000004 WILLOW CREEK COMMUNITY CHURCH 67 E ALGONQUIN RD SOUTH BARRINGTON Y 7000005 THE PRESBYTERIAN CHURCH 6 BRINKER RD BARRINGTON Y 7000006 ST MICHAELS EPISCOPAL CHURCH 647 DUNDEE AVE BARRINGTON Y 7000007 BARRINGTON HILLS VILLAGE HALL 112 ALGONQUIN RD BARRINGTON Y 7000008 WILLOW CREEK COMMUNITY CHURCH 67 E ALGONQUIN RD SOUTH BARRINGTON Y 7000009 ST MICHAELS EPISCOPAL CHURCH 647 DUNDEE AVE BARRINGTON Y 7000010 WILLOW CREEK COMMUNITY CHURCH 67 E ALGONQUIN RD SOUTH BARRINGTON Y 7000011 WILLOW CREEK COMMUNITY CHURCH 67 E ALGONQUIN RD SOUTH BARRINGTON Y 7100001 FLOSSMOOR COMMUNITY CHURCH 847 HUTCHISON RD FLOSSMOOR Y 7100002 FAITH EVANGELICAL LUTHERAN CHURCH 18645 DIXIE HWY HOMEWOOD Y 7100003 BLOOM TOWNSHIP HALL 425 S HALSTED ST CHICAGO HEIGHTS Y 7100004 KENNEDY SCHOOL 10TH AND DIVISION ST CHICAGO HEIGHTS Y 7100005 BETHEL CHRISTIAN REFORMED 3500 GLENWOOD/LANSING RD LANSING Y 7100006 LINCOLN SCHOOL 1520 CENTER AVE CHICAGO HEIGHTS Y 7100007 FIRST APOSTOLIC CHURCH 22709 STATE ST STEGER Y 7100008 SOUTH CHICAGO HEIGHTS SENIOR CENTER 3140 ENTERPRISE PARK AVE SOUTH CHICAGO HEIGHTS Y 7100009 SOUTH CHICAGO HEIGHTS SENIOR CENTER 3140 ENTERPRISE PARK AVE SOUTH CHICAGO HEIGHTS Y 7100010 PHILLIPS SCHOOL 1401 13TH PL FORD HEIGHTS -

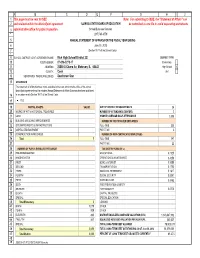

Copy of 227Asa12form (2) Revised Page 3 Page 3

AB CDEF G HIJ 1 This page must be sent to ISBE Note: For submitting to ISBE, the "Statement of Affairs" can 2 and retained within the district/joint agreementILLINOIS STATE BOARD OF EDUCATION be submitted as one file to avoid separating worksheets. 3 administrative office for public inspection. School Business Services 4 (217)785-8779 5 ANNUAL STATEMENT OF AFFAIRS FOR THE FISCAL YEAR ENDING 6 June 30, 2012 7 (Section 10-17 of the School Code) 8 9 SCHOOL DISTRICT/JOINT AGREEMENT NAME: Rich High School District 227 DISTRICT TYPE 10 RCDT NUMBER: 07-016-2270-17 Elementary 11 ADDRESS: 20550 S Cicero Av, Matteson, IL 60443 High School X 12 COUNTY: Cook Unit 1413 NEWSPAPER WHERE PUBLISHED: Southtown Star 15 ASSURANCE The statement of affairs has been made available in the main administrative office of the school district/joint agreement and the required Annual Statement of Affairs Summary has been published 16 in accordance with Section 10-17 of the School Code. YES 1817 19 CAPITAL ASSETS VALUE SIZE OF DISTRICT IN SQUARE MILES 34 20 WORKS OF ART & HISTORICAL TREASURES NUMBER OF ATTENDANCE CENTERS 3 21 LAND 9 MONTH AVERAGE DAILY ATTENDANCE 3,358 22 BUILDING & BUILDING IMPROVEMENTS NUMBER OF CERTIFICATED EMPLOYEES 23 SITE IMPROVMENTS & INFRASTRUCTURE FULL-TIME 335 24 CAPITALIZED EQUIPMENT PART-TIME 3 25 CONSTRUCTION IN PROGRESS NUMBER OF NON-CERTIFICATED EMPLOYEES 26 Total 0 FULL-TIME 247 27 PART-TIME 22 28 NUMBER OF PUPILS ENROLLED PER GRADE TAX RATE BY FUND (IN %) 29 PRE-KINDERGARTEN EDUCATIONAL 3.1820 30 KINDERGARTEN OPERATIONS & MAINTENANCE -

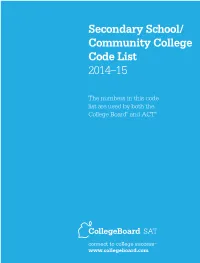

Secondary School/ Community College Code List 2014–15

Secondary School/ Community College Code List 2014–15 The numbers in this code list are used by both the College Board® and ACT® connect to college successTM www.collegeboard.com Alabama - United States Code School Name & Address Alabama 010000 ABBEVILLE HIGH SCHOOL, 411 GRABALL CUTOFF, ABBEVILLE AL 36310-2073 010001 ABBEVILLE CHRISTIAN ACADEMY, PO BOX 9, ABBEVILLE AL 36310-0009 010040 WOODLAND WEST CHRISTIAN SCHOOL, 3717 OLD JASPER HWY, PO BOX 190, ADAMSVILLE AL 35005 010375 MINOR HIGH SCHOOL, 2285 MINOR PKWY, ADAMSVILLE AL 35005-2532 010010 ADDISON HIGH SCHOOL, 151 SCHOOL DRIVE, PO BOX 240, ADDISON AL 35540 010017 AKRON COMMUNITY SCHOOL EAST, PO BOX 38, AKRON AL 35441-0038 010022 KINGWOOD CHRISTIAN SCHOOL, 1351 ROYALTY DR, ALABASTER AL 35007-3035 010026 EVANGEL CHRISTIAN SCHOOL, PO BOX 1670, ALABASTER AL 35007-2066 010028 EVANGEL CLASSICAL CHRISTIAN, 423 THOMPSON RD, ALABASTER AL 35007-2066 012485 THOMPSON HIGH SCHOOL, 100 WARRIOR DR, ALABASTER AL 35007-8700 010025 ALBERTVILLE HIGH SCHOOL, 402 EAST MCCORD AVE, ALBERTVILLE AL 35950 010027 ASBURY HIGH SCHOOL, 1990 ASBURY RD, ALBERTVILLE AL 35951-6040 010030 MARSHALL CHRISTIAN ACADEMY, 1631 BRASHERS CHAPEL RD, ALBERTVILLE AL 35951-3511 010035 BENJAMIN RUSSELL HIGH SCHOOL, 225 HEARD BLVD, ALEXANDER CITY AL 35011-2702 010047 LAUREL HIGH SCHOOL, LAUREL STREET, ALEXANDER CITY AL 35010 010051 VICTORY BAPTIST ACADEMY, 210 SOUTH ROAD, ALEXANDER CITY AL 35010 010055 ALEXANDRIA HIGH SCHOOL, PO BOX 180, ALEXANDRIA AL 36250-0180 010060 ALICEVILLE HIGH SCHOOL, 417 3RD STREET SE, ALICEVILLE AL 35442 -

Statewide Audit of Dual Credit Course Costs

Cost Information by Community College Community College High Schools Cost Per Course Cost Per Credit Responsible Party Additional Notes North Naperville Central High School Addison Trail High School Glenbard South High School Downers Grove North High School Downers Grove South High School Hinsdale South High School Lake Park High School Lyons Township High School-No Metea Valley High School Naperville North High School Neuqua Valley High School College of Technology Center of DuPage DuPage Waubonsie Valley High School $0 N/A N/A (2018-2019) West Chicago High School Wheaton North High School Wilco Area Career Center Willowbrook High School York High School Bolingbrook High School Hinsdale Central High School Islamic Foundation School Lisle High School Montini High School Morton East High School Westmont High School Andrew High School $0 $0 Argo High School Cost Per Course $0 for all but $0 - $145 $0 - $72.50 two math courses. Bremen High School $0 $0 Brother Rice High School $44 $14.67 - $44 Chicago Christian High School $44 $15 Delta High School $0 $0 Eisenhower High School $0 $0 Evergreen Park High School Course Fee is $0 for all but $0 - $145 $0 - $29 two math courses. Hillcrest High School $0 $0 Hinsdale South High School $0 $0 Hinsdale Central High School $0 $0 Lyons Township High School $145 $36.25 - $48.33 Marist High School $145 $36 Only offers a Math course. Morgan Park Academy $145 $29 Only offers a Math course. Moraine Valley Oak Lawn Community High School Information not provided Course Fee is $0 for all but (FY19) $0 - $145 $0 - $48.33 two English courses. -

Annual Report May 2016

IVS Now! Annual Report May 2016 Prepared by the Peoria County Regional Office of Education d/b/a Illinois Virtual School Peoria County Regional Office of Education d/b/a Illinois Virtual School Peoria County Regional Office of Education #48 Elizabeth A. Crider Derry, Regional Superintendent Cindy Dollman, Assistant Regional Superintendent Illinois Virtual School Staff Cindy Hamblin, Director Danielle Brush Lewis, Coordinator of Professional Development Services Edward Cook, Customer Service Lead Maria Gottschalk, Learning Management System Specialist Jennifer Kolar-Burden, Coordinator of Curriculum Liz Lappin, Instructional Media Developer Lara Zink Pritchard, Enrollment and Data Specialist Illinois Virtual School has institutional membership in the following organizations. • International Association for K-12 Online Learning (iNACOL) • Virtual School Leadership Alliance • Quality Matters • Consortium of School Networks (CoSN) Background and Purpose Illinois Virtual School (IVS) is the Illinois State Board of Education’s (ISBE) statewide virtual school. ISBE established IVS as a supplemental online program. The IVS program is designed to allow students who are enrolled in a public or private school to supplement their education by taking courses that are educationally appropriate. In addition, IVS works with homeschool students. Illinois State Board of Education (ISBE) GOAL 1: “Every child in each public school system in the state of Illinois deserves to attend a system wherein . Ninety percent or more students graduate from high school -

(Head Boys Cross Country Coach/Head Girls Track & Field

Mitch, Thank you so much for coming to visit our track and field practice a couple of weeks ago! Thank you also for the donated racing spikes! They will certainly be put to good use. Our girl’s track and field program has blossomed to over sixty student-athletes this current season. We are excited about the opportunity to have ALL of our student-athletes competing in the proper equipment. In fact, last week I gave a pair of new racing spikes that you delivered to a student -athlete that was working out in the same shoes that she had before last year's track and field season. She was thrilled and is wearing them proudly! Her personal best in the pole vault at Friday night's meet was probably aided by better footwear. Thank you again! If there is an opportunity to receive more donated racing spikes from your foundation, please let me know. It is great to know that there are former track and field stalwarts working to promote the sport of track and field. Lance Pacernick (Head Boys Cross Country Coach/Head Girls Track & Field Coach, Waukegan High School , Waukegan, IL) Mr. Johnston, "My son Johnny Dickson runs for Thornridge High. At his last track meet I climbed into the bleachers to find him lacing up new trainers and spikes! I was so moved by how elated he was to receive brand- named shoes right before a meet. High five to Mr. Johnston (who personally delivered them) and to the other charitable champions at Winged Foot Foundation. -

Assistant Coaches)

To: The Winged Foot Foundation, I think this foundation was a GOD send. We needed trainers and spikes for the girl’s teams (Thornridge Cross Country and Track and Field) and I was told about this foundation through a fellow track coach. I e-mailed Mr. Johnson and he quickly got back to me, a couple of days later I had shoes/spikes for my girls. I really feel this organization blesses the teams that are less fortunate and we really appreciate it. Thank you, Coach Catron (Head Coach, Thornridge High School) To: Winged Foot Foundation, We are so appreciative to benefit from the Winged Foot Foundation. I can’t tell you how many injuries my athletes suffer due to improper gear. They were all so grateful for this surprise. I know these trainers and spikes will enhance our performances. Thanks to your foundation, the running program at Rich South HS will be better than ever. Sincerely, Ron Lynch (Head Coach, Rich South Girls & Boys Cross Country) Marcyio Chachakis & Derrick Gordon (Assistant Coaches) Mitch, I just wanted to say thanks to you and the Winged Foot Foundation for your generous donation of the running shoes as well as the cool sheik Brooks Racing spikes. Without these donations, my student athletes would not have such a quality shoe to run or practice in. You should have seen their faces light up and smiles emerge when they saw the shoes. It was amazing! Most all of my student athletes come from families that are at or below the poverty level, struggling to make ends meet. -

Prairie State College in Its First Quarter Century, 1957-1982: a Community College History/By Richard G

DOCUMENT RESUME ED 377 906 JC 950 036 AUTHOR Sherman, Richard G. TITLE Prairie State College in Its First QuarterCentury, 1957-1982: A Community College History. INSTITUTION Prairie State Coll., Chicago Heights, Iii. PUB DATE 94 NOTE 399p.; Photographs may not reproduce well. PUB TYPE Historical Materials (060) EDRS PRICE MF01/PC16 Plus Postage. DESCRIPTORS *College Administration; *Community Colleges; *Educational History; *InstitutionalCharacteristics; *Organizational Change; Two Year Colleges IDENTIFIERS *Prairie State College IL ABSTRACT Written especially for students, staff,faculty, administrators, and trustees of the college,this history of Prairie State College in Illinois traces t.,he college'sdevelopment from its inception in 1957 through 1982. Thisbook contains the following chapters:(1) "A Community Emerges"; (2) "AnAmerican Educational Institution Emerges";(3) "Higher Educb.ion Under Siege";(4) "A Junior College Is Founded";(5) "A Junior College in Infancy"; (6) "Becoming a Community College";(7) "Breaking Away and Forginga Community";(8) "Looking towarda New Era";(9) "Hard Problems Thwart High Hopes"; (10) "Turmoil Strikes in.the Late Sixties"; (11) "Administration and Faculty Alienate";(12) "Alienation Increases and a President Is Terminated"; (13) "New Leadership andReappraisal"; (.14) "A Main Campus at Last"; (15)"Student Services and Activities";. (16) "Faculty and AdministrationStrains Continue But Improve";(17) "Carrying Out the Community College Mission";(18) "Getting Along with the System and Neighbors"; (19) "Another Era Begins";(20) "Adjusting to a New Campus anda New Administration"; (21) "Profile of a Community College Approaching Its FirstQuarter-of-a-Century"; (22) "Continuing the Task ofa Community College"; (23) "Providing More Community Services"; (24) "ProvidingMore Student Services"; (25) "Apogee and.Dismay"; and (26)"The College Reachesa Milestone.