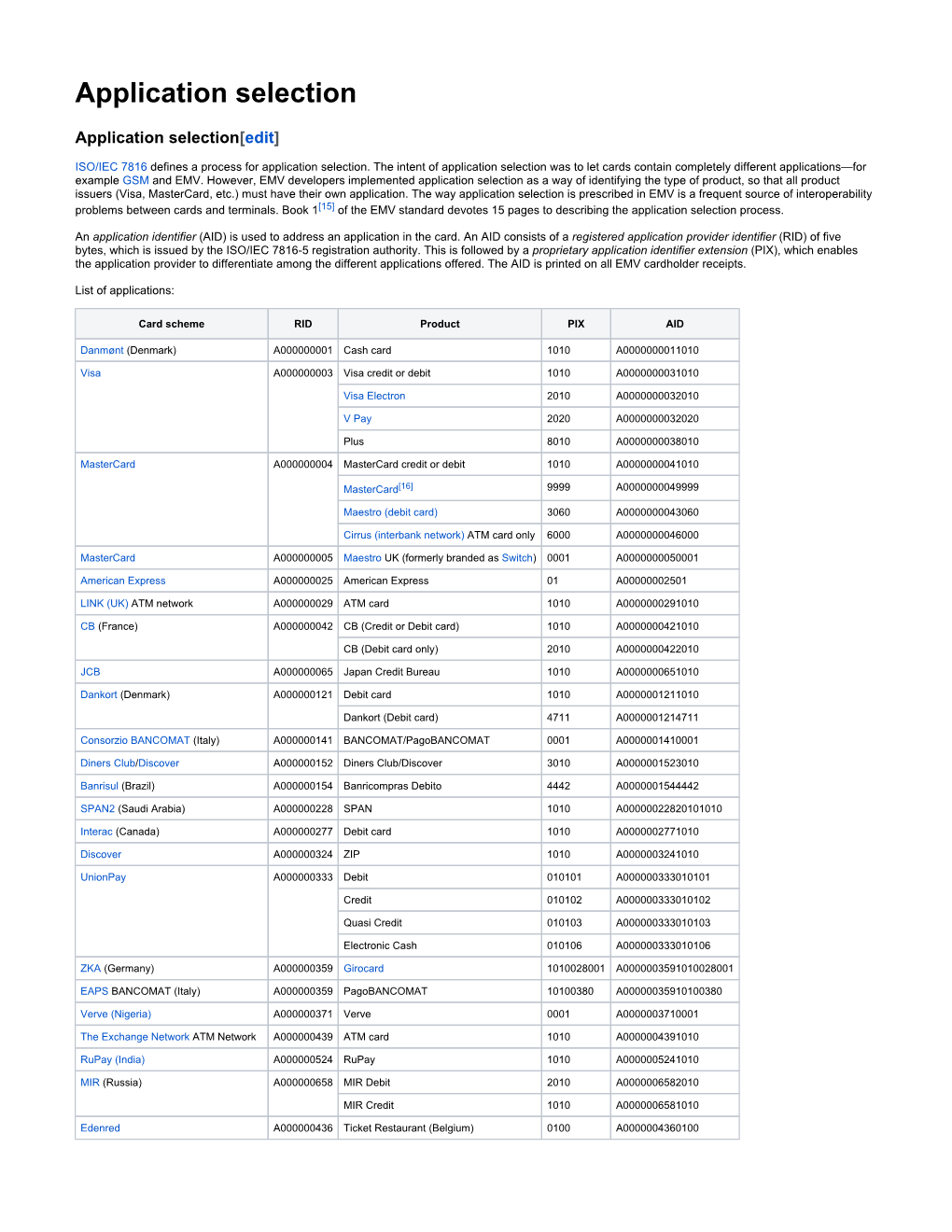

Application Selection

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Mobile Banking

Automated teller machine "Cash machine" Smaller indoor ATMs dispense money inside convenience stores and other busy areas, such as this off-premise Wincor Nixdorf mono-function ATM in Sweden. An automated teller machine (ATM) is a computerized telecommunications device that provides the customers of a financial institution with access to financial transactions in a public space without the need for a human clerk or bank teller. On most modern ATMs, the customer is identified by inserting a plastic ATM card with a magnetic stripe or a plastic smartcard with a chip, that contains a unique card number and some security information, such as an expiration date or CVVC (CVV). Security is provided by the customer entering a personal identification number (PIN). Using an ATM, customers can access their bank accounts in order to make cash withdrawals (or credit card cash advances) and check their account balances as well as purchasing mobile cell phone prepaid credit. ATMs are known by various other names including automated transaction machine,[1] automated banking machine, money machine, bank machine, cash machine, hole-in-the-wall, cashpoint, Bancomat (in various countries in Europe and Russia), Multibanco (after a registered trade mark, in Portugal), and Any Time Money (in India). Contents • 1 History • 2 Location • 3 Financial networks • 4 Global use • 5 Hardware • 6 Software • 7 Security o 7.1 Physical o 7.2 Transactional secrecy and integrity o 7.3 Customer identity integrity o 7.4 Device operation integrity o 7.5 Customer security o 7.6 Alternative uses • 8 Reliability • 9 Fraud 1 o 9.1 Card fraud • 10 Related devices • 11 See also • 12 References • 13 Books • 14 External links History An old Nixdorf ATM British actor Reg Varney using the world's first ATM in 1967, located at a branch of Barclays Bank, Enfield. -

Eftpos Payment Asustralia Limited Submission to Review of The

eftpos Payments Australia Limited Level 11 45 Clarence Street Sydney NSW 2000 GPO Box 126 Sydney NSW 2001 Telephone +61 2 8270 1800 Facsimile +61 2 9299 2885 eftposaustralia.com.au 22 January 2021 Secretariat Payments System Review The Treasury Langton Crescent PARKES ACT 2600 [email protected] Thank you for the opportunity to respond to the Treasury Department’s Payments System Review: Issues Paper dated November 2020 (Review). The Review is timely as Australia’s payments system is on the cusp of a fundamental transformation driven by a combination of digital technologies, nimble new fintech players and changes in consumer and merchant payment preferences accelerated by the COVID-19 pandemic. Additionally, the Reserve Bank of Australia (RBA) is conducting its Retail Payments Regulatory Review, which commenced in 2019 (RBA Review) but was postponed due to COVID-19 and there is a proposal to consolidate Australia’s domestic payments systems which has potential implications for competition within the Australian domestic schemes, as well as with existing and emerging competitors in the Australian payments market through all channels. Getting the regulatory architecture right will set Australia up for success in the digital economy for the short term and in years to come. However, a substandard regulatory architecture has the potential to stall technologically driven innovation and stymie future competition, efficiencies and enhanced end user outcomes. eftpos’ response comprises: Part A – eftpos’ position statement Part B – eftpos’ background Part C – responses to specific questions in the Review. We would be pleased to meet to discuss any aspects of this submission. Please contact Robyn Sanders on Yours sincerely Robyn Sanders General Counsel and Company Secretary eftpos Payments Australia Limited ABN 37 136 180 366 Public eftpos Payments Australia Limited Level 11 45 Clarence Street Sydney NSW 2000 GPO Box 126 Sydney NSW 2001 Telephone +61 2 8270 1800 Facsimile +61 2 9299 2885 eftposaustralia.com.au A. -

VX690 User Manual

Sivu 1(36) 28.9.2016 VX690 User Manual English Author: Verifone Finland Oy Date: 28.9.2016 Pages: 20 Sivu 2(36) 28.9.2016 INDEX: 1. BEFORE USE ............................................................................................................................... 5 1.1 Important ......................................................................................................................................... 5 1.2 Terminal Structure ......................................................................................................................... 6 1.3 Terminal start-up and shutdown .................................................................................................. 6 1.4 Technical data ................................................................................................................................ 7 1.5 Connecting cables ......................................................................................................................... 7 1.6 SIM-card.......................................................................................................................................... 8 1.7 Touchscreen ................................................................................................................................... 8 1.8 Using the menus ............................................................................................................................ 9 1.9 Letters and special characters.................................................................................................... -

Word Files Coverted

About MasterCard International: MasterCard International is a leading global payments solutions company that provides a broad variety of innovative services in support of their global members' credit, deposit access, electronic cash, business-to-business and related payment programs. MasterCard international manages a family of well-known, widely accepted payment cards brands including MasterCard®, Maestro®, and Cirrus® and serves financial institutions, consumers and businesses in over 210 countries and territories. What is a Debit Card: Maestro® is the Global Debit Card cum ATM Card product of MasterCard International. This card can be used to make on-line bill payments through 49,000 Point of Sale (POS) terminals in India and 70,00,000 merchant establishments worldwide exhibiting “MAESTRO” logo. In other words the Debit Card holder can pay their bills, at shops exhibiting “Maestro” Logo, using this card instead by cash or cheque. The card holder need not carry cash in future when all the shops provide this facility. SIB's Debit Card can also be used as an ATM card within the ATM network of the Bank. People around the world prefer debit card over credit card since the spending can be restricted to what they have in their account. Since payment is effected only if there is available balance in the customer's account, it is absolutely risk-free for the banks. SIB plans to issue debit cards liberally as an added convenience to its customers which in turn reduces the pressure on cash transactions at the counters. How is CIRRUS relevant to other bank's Maestro Card holders: SIB has acquired “CIRRUS”, the product of MasterCard International. -

NPCI Appoints FIME to Set up the Certification Body for India's

NPCI appoints FIME to set up the certification body for India’s Payment Scheme, RuPay FIME to define, manage and execute certification programme for RuPay 6 March 2014 – National Payments Corporation of India (NPCI), the umbrella organisation of all retail payment systems in the country, has appointed advanced secure-chip testing provider FIME to deliver its RuPay certification programme. NPCI will utilise FIME’s expertise in setting up EMV®-based certification board for its card payment scheme- RuPay. FIME will define the certification specification, laboratory setup, test plan specification, test tools and operate the certification board for RuPay. FIME will also be involved in setting up the certification process including the associated administrative and business operations. This certification board will be effective from March 2014. This will ensure all payment cards and point-of-sale terminals deployed under the brand align to the requirements of RuPay specifications. It will also ensure necessary infrastructural alignment of acquirers and issuers with the payment system. Prakash Sambandam, Director of FIME India says: “Many countries have, or are in the process of migrating to the EMV payment standard. Transitioning to a chip payment infrastructure will take time and require the implementation of new product development cycles. Adhering to RuPay, an EMV payment scheme will ensure that the products achieve the required functional and security standards and perform as intended, once live in the marketplace. This level of compliance is vital to ensure product interoperability and security optimisation”. In addition to enhanced security, the new payment platform presents opportunities to deliver advanced payment solutions – such as mobile and contactless payments – which are based on secure-chip technology. -

Authorisation Service Sales Sheet Download

Authorisation Service OmniPay is First Data’s™ cost effective, Supported business profiles industry-leading payment processing platform. In addition to card present POS processing, the OmniPay platform Authorisation Service also supports these transaction The OmniPay platform Authorisation Service gives you types and products: 24/7 secure authorisation switching for both domestic and international merchants on behalf of merchant acquirers. • Card Present EMV offline PIN • Card Present EMV online PIN Card brand support • Card Not Present – MOTO The Authorisation Service supports a wide range of payment products including: • Dynamic Currency Conversion • Visa • eCommerce • Mastercard • Secure eCommerce –MasterCard SecureCode, Verified by Visa and SecurePlus • Maestro • Purchase with Cashback • Union Pay • SecureCode for telephone orders • JCB • MasterCard Gaming (Payment of winnings) • Diners Card International • Address Verification Service • Discover • Recurring and Installment • BCMC • Hotel Gratuity • Unattended Petrol • Aggregator • Maestro Advanced Registration Program (MARP) Supported authorisation message protocols • OmniPay ISO8583 • APACS 70 Authorisation Service Connectivity to the Card Schemes OmniPay Authorisation Server Resilience Visa – Each Data Centre has either two or four Visa EAS servers and resilient connectivity to Visa Europe, Visa US, Visa Canada, Visa CEMEA and Visa AP. Mastercard – Each Data Centre has a dedicated Mastercard MIP and resilient connectivity to the Mastercard MIP in the other Data Centre. The OmniPay platform has connections to Banknet for both European and non-European authorisations. Diners/Discover – Each Data Centre has connectivity to Diners Club International which is also used to process Discover Card authorisations. JCB – Each Data Centre has connectivity to Japan Credit Bureau which is used to process JCB authorisations. UnionPay – Each Data Centre has connectivity to UnionPay International which is used to process UnionPay authorisations. -

(Automated Teller Machine) and Debit Cards Is Rising. ATM Cards Have A

Consumer Decision Making Contest 2001-2002 Study Guide ATM/Debit Cards The popularity of ATM (automated teller machine) and debit cards is rising. ATM cards have a longer history than debit cards, but the National Consumers League estimates that two-thirds of American households are likely to have debit cards by the end of 2000. It is expected that debit cards will rival cash and checks as a form of payment. In the future, “smart cards” with embedded computer chips may replace ATM, debit and credit cards. Single-purpose smart cards can be used for one purpose, like making a phone call, or riding mass transit. The smart card keeps track of how much value is left on your card. Other smart cards have multiple functions - serve as an ATM card, a debit card, a credit card and an electronic cash card. While this Study Guide will not discuss smart cards, they are on the horizon. Future consumers who understand how to select and use ATM and debit cards will know how to evaluate the features and costs of smart cards. ATM and Debit Cards and How They Work Electronic banking transactions are now a part of the American landscape. ATM cards and debit cards play a major role in these transactions. While ATM cards allow us to withdraw cash to meet our needs, debit cards allow us to by-pass the use of cash in point-of-sale (POS) purchases. Debit cards can also be used to withdraw cash from ATM machines. Both types of plastic cards are tied to a basic transaction account, either a checking account or a savings account. -

Location Optimization of ATM Networks

Location Optimization of ATM Networks Somnath Basu Roy Chowdhury Biswarup Bhaacharya Sumit Agarwal Indian Institute of Technology Indian Institute of Technology Indian Institute of Technology Kharagpur, West Bengal 721302 Kharagpur, West Bengal 721302 Kharagpur, West Bengal 721302 [email protected] [email protected] [email protected] ABSTRACT & infrastructure, potential criminal activity, maintenance & power ATMs enable the public to perform nancial transactions. Banks costs etc. e companies also consider the cost of seing up an ATM try to strategically position their ATMs in order to maximize trans- in such locations and the amount of return that can be estimated. actions and revenue. In this paper, we introduce a model which At last the companies can analyze whether the entire venture is provides a score to an ATM location, which serves as an indicator of successful. its relative likelihood of transactions. In order to eciently capture We dene a similar problem where we consider the ATM loca- the spatially dynamic features, we utilize two concurrent prediction tions of dierent banks in the state of California, USA. e location models: the local model which encodes the spatial variance by con- features like the population density, average income, living stan- sidering highly energetic features in a given location, and the global dard can be gathered from the given zipcodes. We try to form a model which enforces the dominant trends in the entire data and logical inference of the features at hand in order to assign accu- serves as a feedback to the local model to prevent overing. e rate priority to the appropriate features. -

B+S Card Service: Transaction Volume Grows – Newly Established Top Management

Press release B+S Card Service: Transaction Volume Grows – Newly Established Top Management Frankfurt/Main, January 28th 2013. Once again, in the just ended fiscal year 2012 (October 2011 thru September 2012), B+S Card Service was able to grow processing volume originating from the processing of card payment transactions. In whole, B+S, a partly owned subsidiary of Deutscher Sparkassenverlag, processed payments amounting to 23.1 billion Euros (2 per cent increase) – the B+S all-time corporate record since start up in 1989. At the end of the 2012 fiscal year, B+S had more than 227,000 customers in fourteen European countries. As one of the few companies not only offering one-stop network and POS but also comprehensive acquiring services, B+S currently operates approximately 167,000 payment terminals that processed roughly 553 Million transactions during the fiscal year. B+S Innovation in Contactless Payment In 2011/12, the focus in particular was on product development for contactless payments. B+S started the service of payment processing compliant to the new girogo payment process and as first service provider even introduced two further contactless-enabled payment terminals H5000 and VX820 to the German market. The product portfolio was honoured with numerous awards, most recently with an innovation prize sponsored by the Deutscher Sparkassen- und Giroverband (German Savings Banks Association, DSGV) contactless payments terminal competition.“. - 1 - „From a product perspective, contactless payment remains the central issue for our company“, B+S managing director Matthias Kaufmann explains. “Especially in Germany it accelerates the existing trend towards distinctly more cashless payments. -

Sonderbedingungen Für Die Girocard (Fassung

Girocard (Debit Card) The present translation is furnished for the customer’s convenience only. The original German text is binding in all respects. Special Terms and Conditions In the event of any divergence between the English and the German texts, A. Guaranteed Types of Payment constructions, meanings, or interpretations, the German text, construction, meaning B. Other Bank Services or interpretation shall govern exclusively. C. Additional Applications D. Amicable Dispute Resolution and Other Possibilities for Complaints A. Guaranteed Types of Payment I. Scope of Application Girocard is a debit card. Card Holder may use the Card for the below payment services if the Card and the terminals are equipped accordingly: 1 in connection with a personal identification number (PIN) with all German debit card systems: a) for withdrawing cash at cash machines belonging to the German cash machine system showing the girocard logo; b) for using it with retailers and services providers at automated tills belonging to the German girocard system showing the girocard logo (“Girocard Terminals”); c) for topping up prepaid mobile phone accounts at cash machines which a user has with a mobile phone operator if the cash machine operator offers such services and the mobile phone operator participates in the system. 2 in connection with a personal identification number (PIN) with third-party debit card systems: a) for withdrawing cash at cash machines belonging to third-party cash machine systems if the card is equipped accordingly; b) for using it with retailers and services providers at automated tills belonging to third-party systems if the card is equipped accordingly; c) for topping up prepaid mobile phone accounts at third-party cash machines which a user has with a mobile phone operator if the cash machine operator offers such services and the mobile phone operator participates in the system, whereby Card acceptance by third-party systems is subject to the third-party system acceptance logo. -

Online User Guide

Online User Guide Terms and conditions and fees apply to the use of your card. Minimum and maximum transfer amounts may apply. Refer to the PDS. Gobsmacked Loyalty Pty Ltd ABN 60 098 218 216 (AFSL 444609) is the issuer of the card. The PDS is available on the above link. You should consider the PDS in deciding whether or not to acquire or keep the card. Moorebank Sports Club Limited is responsible for the Infinity Plus Rewards program and promotions and the conversion of reward points to monetary value. Refer to the Moorebank Sports Club Limited reward promotions and program terms and conditions. Infinity Plus Prepaid eftpos Card So you’ve got your new Moorebank Sports Club Infinity Plus Prepaid eftpos Card. Now what do you do? This User Guide will explain how to start using your Infinity Plus Card for everyday purchases. If you have any enquiries at all whilst you are a Infinity Plus cardholder please visit Moorebank Sports Club and we will help you. Please refer to the Product Disclosure Statement (PDS) for the terms and conditions governing the use of the Infinity Plus Card. A copy of the PDS is also available online at www.moorebanksports.com.au Table of Contents WHAT IS THE INFINITY PLUS PREPAID eftpos CARD? GETTING STARTED Activate my Infinity Plus Card At the Club At home USING MY INFINITY PLUS CARD Card Loads How do I transfer my rewards onto my Infinity Plus Card? How do I load my card with extra funds so I can spend more? Making Purchases Where can I use my Infinity Plus Card? INFINITY PLUS CARDHOLDER ACCOUNT PAGE Features PIN -

Account Selection Made Easy Money Management Tools

ACCOUNT SELECTION MADE EASY MONEY MANAGEMENT TOOLS Recordkeeping As an online or mobile Banking Customer, you can view your account transactions whenever you wish. Banking, you can view, print and save copies of cheques that have cleard through your Canadian accounts service is free of charge. Automatic transfers Pre-authorized payments and direct deposits Overdraft protection6 FINDING THE PERFECT FIT FOR MANAGING YOUR MONEY Easy, exible banking, to suit all your needs Bank the way you want (ATMs) or in branch ® ATM cash withdrawals throughout Canada secure way to send, request and receive money directly from one bank account to another © ATMs cash withdrawals around the world EASY ACCESS ATMs, Mobile, Telephone and Online Banking. Your Online Banking Telephone Banking ATMs Interac® Debit Interac® e-Transfer Use Online Banking to send/request money to/from anyone with an email address or cellphone number and a bank account at a Canadian nancial institution. International ATM withdrawals Cirrus©2 ATM. First Nations Bank of Canada branch service The Exchange® Network Withdraw cash or make deposits at participating ATMs displaying e Exchange® Network symbol. Looking for a convenient way to needs? Our chequing accounts have what you need to take care of your bill payments, deposits, withdrawals and Value Account Transactions Included 12 included Additional Fees Interac® ATM withdrawal $1.50 each Cirrus©2 ATM (inside U.S. and Mexico) $3 each Cirrus©2 ATM (outside Canada, U.S. and Mexico) $5 each Interac® e-Transfers sent $1.50 each Receive a Fullled Interac® Money Request $1.50 Fulfill an Interac® e-Transfer Money Request free Recordkeeping Options Additional Features Monthly Fees and Rebates Value Plus Account Transactions Included Additional Fees Interac® ATM withdrawal $1.50 each Cirrus©2 ATM (inside U.S.