Market Analysis Report WFP VAM | Food Security Analysis

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

General License No. 8A

DEPARTMENT OF THE TREASURY WASHINGTON, D.C. 20220 Office of Foreign Assets Control Libyan Sanctions Regulations 31 C.F.R. Part 570 Executive Order 13566 of February 25, 2011 Blocking Property and Prohibiting Certain Transactions Related to Libya GENERAL LICENSE NO. SA General License with Respect to the Government of Libya, its Agencies, Instrumentalities, and Controlled Entities, and the Central Bank of Libya (a) General License No.8, dated Septernber 19,2011, is replaced and superseded in its entirety by this General License No. 8A. (b) Effective September 19,2011, all transactions involving the Government ofLibya, its agencies, instrumentalities, and controlled entities, and the Central Bank of Libya are authorized, subject to the following limitations: (1) All funds, including cash, securities, bank accounts, and investment accounts, and precious metals blocked pursuant to Executive Order 13566 of February 25, 2011, or the Libyan Sanctions Regulations, 31 C.F .R. part 570, as of September 19, 2011, remain blocked, except as provided in General License No.7A; and (2) The transactions do not involve any persons listed on the Annex to this general license. (c) Effective September 19,2011, the authorization in paragraph (b) ofthis general license supersedes General License No. 1B. Note to General License No. SA: Subject to the limitations set forth in subparagraphs (1) and (2), paragraph (b) ofthis general license authorizes any transaction involving contracts that have been blocked pursuant to Executive Order 13566 because ofan interest by the Government of Libya. Director Office of Foreign Assets Control Annex to General License No. 8A 1. AL BAGHDADI, Ali AI-Mahmoudi (a.k.a. -

The Synergies of Hedge Funds and Reinsurance

The Synergies of Hedge Funds and Reinsurance Eric Andersen May 13th, 2013 Advisor: Dwight Jaffee Department of Economics University of California, Berkeley Acknowledgements I would like to convey my sincerest gratitude to Dr. Dwight Jaffee, my advisor, whose support and assistance were crucial to this project’s development and execution. I also want to thank Angus Hildreth for providing critical feedback and insightful input on my statistical methods and analyses. Credit goes to my Deutsche Bank colleagues for introducing me to and stoking my curiosity in a truly fascinating, but infrequently studied, field. Lastly, I am thankful to the UC Berkeley Department of Economics for providing me the opportunity to engage this project. i Abstract Bermuda-based alternative asset focused reinsurance has grown in popularity over the last decade as a joint venture for hedge funds and insurers to pursue superior returns coupled with insignificant increases in systematic risk. Seeking to provide permanent capital to hedge funds and superlative investment returns to insurers, alternative asset focused reinsurers claim to outpace traditional reinsurers by providing exceptional yields with little to no correlation risk. Data examining stock price and asset returns of 33 reinsurers from 2000 through 2012 lends little credence to support such claims. Rather, analyses show that, despite a positive relationship between firms’ gross returns and alternative asset management domiciled in Bermuda, exposure to alternative investments not only fails to mitigate market risk, but also may actually eliminate any exceptional returns asset managers would have otherwise produced by maintaining a traditional investment strategy. ii Table of Contents Acknowledgements .......................................................................................................................... i Abstract .......................................................................................................................................... -

07319-9781452746784.Pdf

© 2007 International Monetary Fund May 2007 IMF Country Report No. 07/148 The Socialist People's Libyan Arab Jamahiriya: Statistical Appendix This Statistical Appendix for the The Socialist People’s Libyan Arab Jamahiriya was prepared by a staff team of the International Monetary Fund as background documentation for the periodic consultation with the member country. It is based on the information available at the time it was completed on April 5, 2007. The views expressed in this document are those of the staff team and do not necessarily reflect the views of the government of The Socialist People’s Libyan Arab Jamahiriya or the Executive Board of the IMF. The policy of publication of staff reports and other documents by the IMF allows for the deletion of market-sensitive information. To assist the IMF in evaluating the publication policy, reader comments are invited and may be sent by e-mail to [email protected]. Copies of this report are available to the public from International Monetary Fund ● Publication Services 700 19th Street, N.W. ● Washington, D.C. 20431 Telephone: (202) 623 7430 ● Telefax: (202) 623 7201 E-mail: [email protected] ● Internet: http://www.imf.org Price: $18.00 a copy International Monetary Fund Washington, D.C. ©International Monetary Fund. Not for Redistribution This page intentionally left blank ©International Monetary Fund. Not for Redistribution INTERNATIONAL MONETARY FUND THE SOCIALIST PEOPLE’S LIBYAN ARAB JAMAHIRIYA Statistical Appendix Prepared by a staff team comprising M. Elhage (head), R. Abdoun, I. Al-Ghelaiqah, and S. Hussein (all MCD) Approved by the Middle East and Central Asia Department April 5, 2007 Contents Page 1. -

List of Certain Foreign Institutions Classified As Official for Purposes of Reporting on the Treasury International Capital (TIC) Forms

NOT FOR PUBLICATION DEPARTMENT OF THE TREASURY JANUARY 2001 Revised Aug. 2002, May 2004, May 2005, May/July 2006, June 2007 List of Certain Foreign Institutions classified as Official for Purposes of Reporting on the Treasury International Capital (TIC) Forms The attached list of foreign institutions, which conform to the definition of foreign official institutions on the Treasury International Capital (TIC) Forms, supersedes all previous lists. The definition of foreign official institutions is: "FOREIGN OFFICIAL INSTITUTIONS (FOI) include the following: 1. Treasuries, including ministries of finance, or corresponding departments of national governments; central banks, including all departments thereof; stabilization funds, including official exchange control offices or other government exchange authorities; and diplomatic and consular establishments and other departments and agencies of national governments. 2. International and regional organizations. 3. Banks, corporations, or other agencies (including development banks and other institutions that are majority-owned by central governments) that are fiscal agents of national governments and perform activities similar to those of a treasury, central bank, stabilization fund, or exchange control authority." Although the attached list includes the major foreign official institutions which have come to the attention of the Federal Reserve Banks and the Department of the Treasury, it does not purport to be exhaustive. Whenever a question arises whether or not an institution should, in accordance with the instructions on the TIC forms, be classified as official, the Federal Reserve Bank with which you file reports should be consulted. It should be noted that the list does not in every case include all alternative names applying to the same institution. -

Tax Relief Country: Italy Security: Intesa Sanpaolo S.P.A

Important Notice The Depository Trust Company B #: 15497-21 Date: August 24, 2021 To: All Participants Category: Tax Relief, Distributions From: International Services Attention: Operations, Reorg & Dividend Managers, Partners & Cashiers Tax Relief Country: Italy Security: Intesa Sanpaolo S.p.A. CUSIPs: 46115HAU1 Subject: Record Date: 9/2/2021 Payable Date: 9/17/2021 CA Web Instruction Deadline: 9/16/2021 8:00 PM (E.T.) Participants can use DTC’s Corporate Actions Web (CA Web) service to certify all or a portion of their position entitled to the applicable withholding tax rate. Participants are urged to consult TaxInfo before certifying their instructions over CA Web. Important: Prior to certifying tax withholding instructions, participants are urged to read, understand and comply with the information in the Legal Conditions category found on TaxInfo over the CA Web. ***Please read this Important Notice fully to ensure that the self-certification document is sent to the agent by the indicated deadline*** Questions regarding this Important Notice may be directed to Acupay at +1 212-422-1222. Important Legal Information: The Depository Trust Company (“DTC”) does not represent or warrant the accuracy, adequacy, timeliness, completeness or fitness for any particular purpose of the information contained in this communication, which is based in part on information obtained from third parties and not independently verified by DTC and which is provided as is. The information contained in this communication is not intended to be a substitute for obtaining tax advice from an appropriate professional advisor. In providing this communication, DTC shall not be liable for (1) any loss resulting directly or indirectly from mistakes, errors, omissions, interruptions, delays or defects in such communication, unless caused directly by gross negligence or willful misconduct on the part of DTC, and (2) any special, consequential, exemplary, incidental or punitive damages. -

The Association of Exchange Rates and Stock Returns. (Linear Regression Analysis)

March 2007 U.S.B.E- Umeå School of Business Masters Program: Accounting and Finance Masters Thesis- Spring Semester 2007 Author : Akumbu Martin Nshom Supervisor : Stefan Sundgren Thesis seminar : 7 th May 2007 The Association of Exchange rates and Stock returns. (Linear regression Analysis) Acknowledgement I will start by thanking God Almighty for giving me the intellect to complete this project. A big thanks goes to my supervisor Stefan Sundgren for giving me guidance and all the help I needed to complete this thesis To my family for their continuous help and support to see that I under take my studies here especially my Mother Lydia Botame. Finally to all my friends and well wishers who supported me in one way or an other through out my stay here in Umeå, may God bless you all! ABSTRACT The association of exchange rates with stock returns and performance in major trading markets is widely accepted. The world’s economy has seen unprecedented growth of interdependent; as such the magnitude of the effect of exchange rates on returns will be even stronger. Since the author perceives the importance of exchange rates on stock returns, the author found it interesting to study the effect of exchange rates on some stocks traded on the Stock exchange. There has been a renewed interest to investigate the relationship between returns and exchange rates as such; the author has chosen to investigate the present study to focus in the United Kingdom with data from the London Stock exchange .The author carried out his research on 18 companies traded on the London Stock Exchange in the process, using linear regression analysis. -

Countries Codes and Currencies 2020.Xlsx

World Bank Country Code Country Name WHO Region Currency Name Currency Code Income Group (2018) AFG Afghanistan EMR Low Afghanistan Afghani AFN ALB Albania EUR Upper‐middle Albanian Lek ALL DZA Algeria AFR Upper‐middle Algerian Dinar DZD AND Andorra EUR High Euro EUR AGO Angola AFR Lower‐middle Angolan Kwanza AON ATG Antigua and Barbuda AMR High Eastern Caribbean Dollar XCD ARG Argentina AMR Upper‐middle Argentine Peso ARS ARM Armenia EUR Upper‐middle Dram AMD AUS Australia WPR High Australian Dollar AUD AUT Austria EUR High Euro EUR AZE Azerbaijan EUR Upper‐middle Manat AZN BHS Bahamas AMR High Bahamian Dollar BSD BHR Bahrain EMR High Baharaini Dinar BHD BGD Bangladesh SEAR Lower‐middle Taka BDT BRB Barbados AMR High Barbados Dollar BBD BLR Belarus EUR Upper‐middle Belarusian Ruble BYN BEL Belgium EUR High Euro EUR BLZ Belize AMR Upper‐middle Belize Dollar BZD BEN Benin AFR Low CFA Franc XOF BTN Bhutan SEAR Lower‐middle Ngultrum BTN BOL Bolivia Plurinational States of AMR Lower‐middle Boliviano BOB BIH Bosnia and Herzegovina EUR Upper‐middle Convertible Mark BAM BWA Botswana AFR Upper‐middle Botswana Pula BWP BRA Brazil AMR Upper‐middle Brazilian Real BRL BRN Brunei Darussalam WPR High Brunei Dollar BND BGR Bulgaria EUR Upper‐middle Bulgarian Lev BGL BFA Burkina Faso AFR Low CFA Franc XOF BDI Burundi AFR Low Burundi Franc BIF CPV Cabo Verde Republic of AFR Lower‐middle Cape Verde Escudo CVE KHM Cambodia WPR Lower‐middle Riel KHR CMR Cameroon AFR Lower‐middle CFA Franc XAF CAN Canada AMR High Canadian Dollar CAD CAF Central African Republic -

Unit 1: Investments

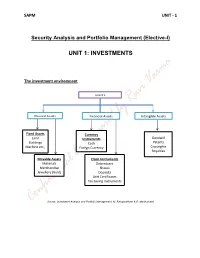

SAPM UNIT - 1 Security Analysis and Portfolio Management (Elective-I) UNIT 1: INVESTMENTS The investment environment ASSETS Physical Assets Financial Assets Intangible Assets Fixed Assets Currency Goodwill Land Instruments Patents Buildings Cash Machine etc., Copyrights Foregn Currency Royalties Movable Assets Claim Instruments Materials Debentures Merchandise Shares Jewellery (Gold) Deposits Unit Certificates Tax Saving Instruments Source: Investment Analysis and Portfolio Management, M. Ranganatham & R. Madhumathi SAPM UNIT - 1 Classification of Financial Markets: Financial Markets Securities Market Currency Market/ Forex market National Market International Market Domestic Segment Foreign Segment Capital Market Money Market Equity Market Debt Market Primary Market Secondary Market Spot Market Derivative Market Source: Investment Analysis and Portfolio Management, M. Ranganatham & R. Madhumathi SAPM UNIT - 1 SAPM UNIT - 1 Investment Meaning & Definition: investment is an activity that is engaged in by people who have savings i.e. investments are made from savings. Investment may be defined as a “commitment of funds made in the expectations of some positive rate of return.” Characteristics of Investment: Return Risk Safety Liquidity Objectives of Investment: Maximisation of Return Minimization of Risk Hedge against Inflation Investment Vs Speculation: Traditionally investment is distinguished from speculation with respect to four factors. These are: Risk Capital Gain Time Period Leverage Financial instruments (Investment Avenues available in India): Corporate Securities Deposits in banks and non-banking companies UTI and other mutual fund schemes SAPM UNIT - 1 Post office deposits and certificates Life insurance policies Provident fund schemes Government and semi government securities Regulatory Environment: In India the ministry of finance, the reserve bank of india, the securities and exchange board of India etc. -

Libya Joint Market Monitoring Initiative (JMMI) Libya Cash Working Group 2 - 10 April 2020

Libya Joint Market Monitoring Initiative (JMMI) Libya Cash Working Group 2 - 10 April 2020 INTRODUCTION METHODOLOGY KEY FINDINGS JMMI KEY FIGURES In an effort to inform cash-based interventions and better • Field staff familiar with the local market conditions • The most notable increases in the cost of the MEB Data collection from 2 - 10 April 2020 understand market dynamics in Libya, the Joint Market identified shops representative of the general were; Nalut (+50.4%), Ashshgega (+50%), Sabratha 3 participating agencies Monitoring Initiative (JMMI) was created by the Libya Cash price level in their respective locations. (+49.1%), Ghadamis (48.7%) and Algatroun (+44.5%). (DRC, REACH, WFP) Working Group (CWG) in June 2017. The initiative is guided • At least three prices per assessed item were The following factors are likely to have contributed to 34 assessed cities by the CWG Markets Taskforce, led by REACH and supported collected within each location. In line with the the increase in the cost of living in the last month: 1. 31 assessed items by the CWG members. It is funded by Office for Foreign purpose of the JMMI, only the price of the Stockpiling of essential goods due COVID-19, 2. 26% 417 assessed shops Disaster Assistance (OFDA) and the United Nations High cheapest available brand was recorded for each increase in the parallel market USD/LYD exchange Commissioner for Refugees (UNHCR). item. rate from December 2019 - April 2020, 3. the Central Bank of Libya halted foreign currency transactions EXCHANGE RATES6 April JMMI price data largely confirms preliminary price • Enumerators were trained on methodology and during the month of March, stemming the flow of goods changes outlined by key informants in the Rapid Market tools by REACH. -

OECD International Network on Financial Education

OECD International Network on Financial Education Membership lists as at May 2020 Full members ........................................................................................................................ 1 Regular members ................................................................................................................. 3 Associate (full) member ....................................................................................................... 6 Associate (regular) members ............................................................................................... 6 Affiliate members ................................................................................................................. 6 More information about the OECD/INFE is available online at: www.oecd.org/finance/financial-education.htm │ 1 Full members Angola Capital Market Commission Armenia Office of the Financial System Mediator Central Bank Australia Australian Securities and Investments Commission Austria Central Bank of Austria (OeNB) Bangladesh Microcredit Regulatory Authority, Ministry of Finance Belgium Financial Services and Markets Authority Brazil Central Bank of Brazil Securities and Exchange Commission (CVM) Brunei Darussalam Autoriti Monetari Brunei Darussalam Bulgaria Ministry of Finance Canada Financial Consumer Agency of Canada Chile Comisión para el Mercado Financiero China (People’s Republic of) China Banking and Insurance Regulatory Commission Czech Republic Ministry of Finance Estonia Ministry of Finance Finland Bank -

Fiscal Year 2009

Statement by the Chairperson of the METAC Steering Committee t was a pleasure for me to chair the Steering Committee of the IMF Middle East Regional Technical Assistance Center (METAC) for the first time this year. The meeting, which was held in Beirut on May 6, I 2009, provided a good opportunity for member countries and donors to gauge the important results and progress achieved in Fiscal Year (FY) 2009, widely recognized by beneficiary member governments, to review the priorities and work plan for FY 2010, and to look forward to the next medium-term phase. The present Annual Report for FY 2009 reviews and addresses these subjects in some detail. As Chairperson, I seized the opportunity to highlight the important role of the Steering Committee in promoting and guiding the work of METAC, and to review ways and means to enhance the role of the Committee with a view to make it more dynamic and effective, including through increased networking and monitoring. I emphasized the important role of METAC in the cross-border fertilization of knowledge and stressed the need for increasing knowledge-sharing and learning as an integral part of METAC’s work. Being located in Beirut, close to the countries it serves, METAC provides several important benefits, including decentralized delivery of technical assistance, which allows for greater flexibility in responding to changing or emerging needs, close coordination with regional technical assistance providers, enhanced country ownership and accountability, and more focused and subject-specific training for local officials. The location of this important center reaffirms the traditional role of Beirut as a regional center of excellence and reflects recognition of Lebanon’s wealth in qualified human resources. -

Origins of the Libyan Conflict and Options for Its Resolution

ORIGINS OF THE LIBYAN CONFLICT AND OPTIONS FOR ITS RESOLUTION JONATHAN M. WINER MAY 2019 POLICY PAPER 2019-12 CONTENTS * 1 INTRODUCTION * 4 HISTORICAL FACTORS * 7 PRIMARY DOMESTIC ACTORS * 10 PRIMARY FOREIGN ACTORS * 11 UNDERLYING CONDITIONS FUELING CONFLICT * 12 PRECIPITATING EVENTS LEADING TO OPEN CONFLICT * 12 MITIGATING FACTORS * 14 THE SKHIRAT PROCESS LEADING TO THE LPA * 15 POST-SKHIRAT BALANCE OF POWER * 18 MOVING BEYOND SKHIRAT: POLITICAL AGREEMENT OR STALLING FOR TIME? * 20 THE CURRENT CONFLICT * 22 PATHWAYS TO END CONFLICT SUMMARY After 42 years during which Muammar Gaddafi controlled all power in Libya, since the 2011 uprising, Libyans, fragmented by geography, tribe, ideology, and history, have resisted having anyone, foreigner or Libyan, telling them what to do. In the process, they have frustrated the efforts of outsiders to help them rebuild institutions at the national level, preferring instead to maintain control locally when they have it, often supported by foreign backers. Despite General Khalifa Hifter’s ongoing attempt in 2019 to conquer Tripoli by military force, Libya’s best chance for progress remains a unified international approach built on near complete alignment among international actors, supporting Libyans convening as a whole to address political, security, and economic issues at the same time. While the tracks can be separate, progress is required on all three for any of them to work in the long run. But first the country will need to find a way to pull back from the confrontation created by General Hifter. © The Middle East Institute The Middle East Institute 1319 18th Street NW Washington, D.C.