Is High Inequality an Issue in Poland?

Total Page:16

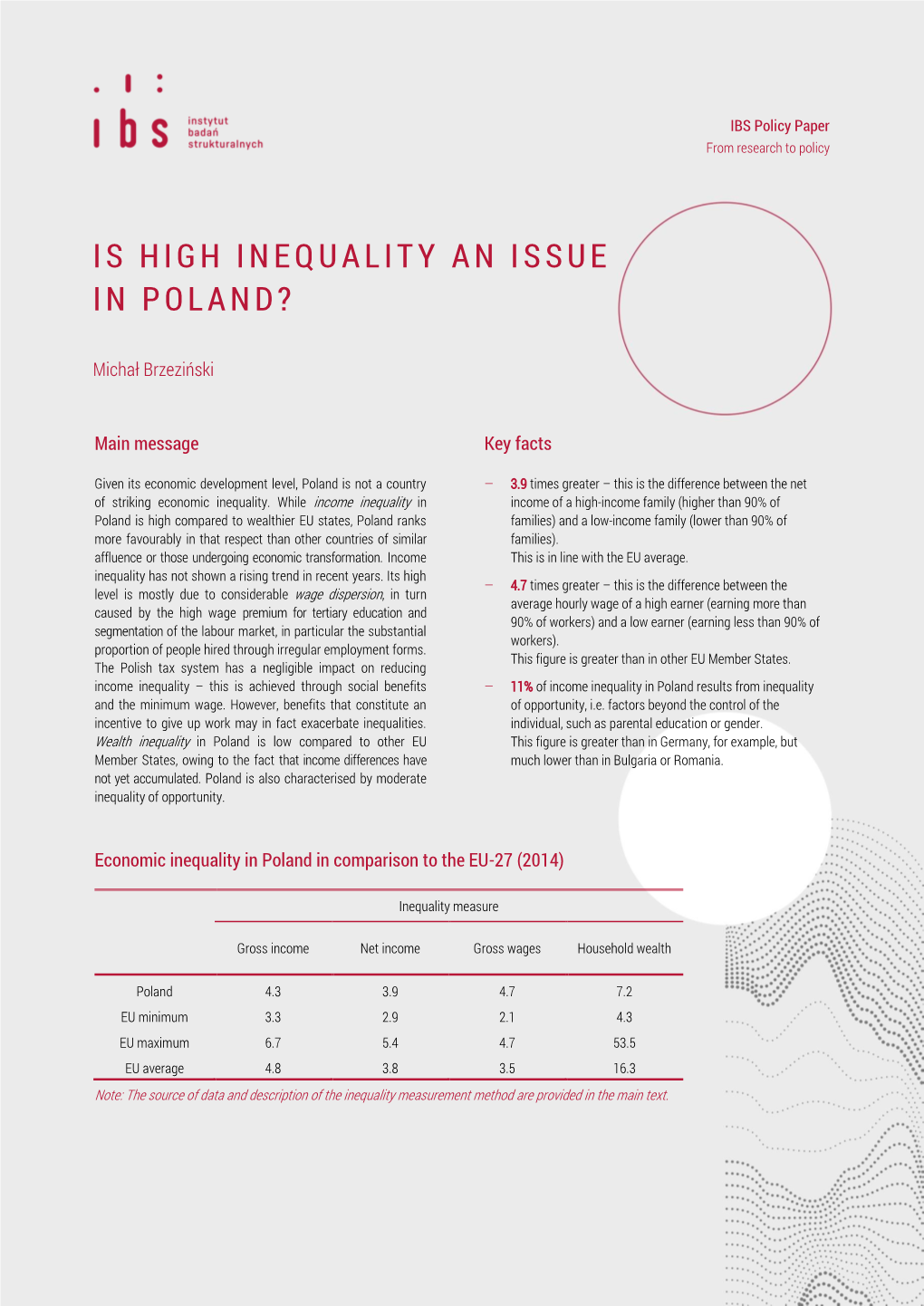

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Debt Crisis in Poland and Its Impact on Society

Gavin Rae ABSTRACT This paper considers the question of public debt and how it impacts upon other areas of socio-economic life in Poland, in the context of the recent global economic crisis. It begins by placing Poland’s public debt in its historical context that reaches back to the Communist period. One result of the large debt incurred during this time, was that Poland became indebted and dependent upon creditors in the West. This dependency helped to shape its neo-liberal economic policy from the late 1980s. This has resulted in a large deactivation of labour that has placed a huge burden on the country’s public finances. Furthermore, the creation of a compulsory private pension system at the end of the 1990s, sucked large amounts of money out of the government’s budget and swelled the country’s public debt. Since the outbreak of the economic crisis, Poland has avoided a recession through increasing public investment by utilising available EU funds. However, due to internal and external limits on the size of its public debt, the government is being pressured to reduce this spending that threatens to suppress growth and further increase unemployment. In order to create more fiscal room, the government has partly dismantled the compulsory private pension system, which has temporarily reduced public debt. Poland already has high levels of poverty and social exclusion, with large sections of society inadequately supported with social benefits and services. Any further reduction in public and social spending could have serious negative consequences for large sections of society. 2 Public Debt in Poland CONTENTS 1. -

Pinpointing Poverty in Poland

Country Policy Brief Poverty in Europe March 2016 Poverty and Equity Global Practice Pinpointing Poverty in Poland Rates of poverty and social exclusion vary program planning and the allocation of EU widely across European Union (EU) member funds. The EC and the World Bank, in cooper- states, and there is also a high degree of ation with individual EU member states, have variability in living standards within member developed a set of high-resolution poverty states.1 In its 2014–20 multiannual financial maps.3 The greater geographical disaggrega- framework, the EU budgeted €1 trillion to tion of the new poverty maps reveals which support growth and jobs and to reduce the parts of these larger regions have particularly number of people living at risk of poverty or high rates of poverty and require greater at- social exclusion by 20 million by the year 2020. tention in poverty reduction programs. To this end, the Government of Poland has The poverty maps confirm existing knowl- set a national goal of reducing the number of edge about poverty in Poland, but also reveal the poor and socially excluded by 1.5 million new insights. For example, previous surveys people.2 have shown the southeastern voivodships (in Success depends on developing the ap- particular Lubelskie and Swietokrzynskie) as propriate policies and programs and target- well as Lubuskie in the west to have higher ing them effectively. However, the EC has poverty rates (map 1, panel a). The more de- previously had to rely on sub-national data tailed poverty map shows that most of the at a relatively high level of aggregation for statistical subregions with the highest risk of Map 1 At-Risk-of-Poverty Rates, Poland a. -

Transitional Social Policy in the Czech Republic and Poland Orenstein, Mitchell

www.ssoar.info Transitional social policy in the Czech Republic and Poland Orenstein, Mitchell Veröffentlichungsversion / Published Version Zeitschriftenartikel / journal article Empfohlene Zitierung / Suggested Citation: Orenstein, M. (1995). Transitional social policy in the Czech Republic and Poland. Sociologický časopis / Czech Sociological Review, 3(2), 179-196. https://nbn-resolving.org/urn:nbn:de:0168-ssoar-53127 Nutzungsbedingungen: Terms of use: Dieser Text wird unter einer Deposit-Lizenz (Keine This document is made available under Deposit Licence (No Weiterverbreitung - keine Bearbeitung) zur Verfügung gestellt. Redistribution - no modifications). We grant a non-exclusive, non- Gewährt wird ein nicht exklusives, nicht übertragbares, transferable, individual and limited right to using this document. persönliches und beschränktes Recht auf Nutzung dieses This document is solely intended for your personal, non- Dokuments. Dieses Dokument ist ausschließlich für commercial use. All of the copies of this documents must retain den persönlichen, nicht-kommerziellen Gebrauch bestimmt. all copyright information and other information regarding legal Auf sämtlichen Kopien dieses Dokuments müssen alle protection. You are not allowed to alter this document in any Urheberrechtshinweise und sonstigen Hinweise auf gesetzlichen way, to copy it for public or commercial purposes, to exhibit the Schutz beibehalten werden. Sie dürfen dieses Dokument document in public, to perform, distribute or otherwise use the nicht in irgendeiner Weise abändern, -

Globalization and Poverty: an Introduction

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: Globalization and Poverty Volume Author/Editor: Ann Harrison, editor Volume Publisher: University of Chicago Press Volume ISBN: 0-226-31794-3 Volume URL: http://www.nber.org/books/harr06-1 Conference Date: September 10-12, 2004 Publication Date: March 2007 Title: Globalization and Poverty: An Introduction Author: Ann Harrison URL: http://www.nber.org/chapters/c10713 Globalization and Poverty An Introduction Ann Harrison 1 Overview More than one billion people live in extreme poverty, which is defined by the World Bank as subsisting on less than one dollar a day.1 In 2001, fully half of the developing world lived on less than two dollars a day. Yet poverty rates are much lower today than twenty years ago. In the last two decades, the per- centage of the developing world living in extreme poverty has been cut in half. While poverty rates were falling, developing countries became increasingly in- tegrated into the world trading system. Poor countries have slashed protective tariffs and increased their participation in world trade. If we use the share of exports in gross domestic product (GDP) as a measure of globalization, then developing countries are now more globalized than high-income countries.2 Does globalization reduce poverty? Will ongoing efforts to eliminate protection and increase world trade improve the lives of the world’s poor? There is surprisingly little evidence on this question.3 The comprehensive Ann Harrison is a professor of agricultural and resource economics at the University of California, Berkeley, and a research associate of the National Bureau of Economic Research. -

The Distributional Impact of Taxes and Transfers in Poland

WPS7787 Policy Research Working Paper 7787 Public Disclosure Authorized The Distributional Impact of Taxes and Transfers in Poland Public Disclosure Authorized Karolina Goraus Gabriela Inchauste Public Disclosure Authorized Public Disclosure Authorized Poverty and Equity Global Practice Group August 2016 Policy Research Working Paper 7787 Abstract This paper assesses the impact of fiscal policy on the Polish fiscal system in 2014 had the capacity to redistribute, incidence, depth, and severity of poverty, and examines it had a relatively weak capacity to reduce poverty given the whether there is room for an increased role for fiscal policy resources at its disposal, and this was especially true for fam- in improving the wellbeing of the poor. The results show ilies with children. Microsimulations of the introduction of that the combined effect of taxes and social spending helped the Family 500+ program in 2016 show the redistributive substantially to reduce poverty and inequality in Poland and poverty reduction impacts of the new program, even in 2014, in line with other European Union countries, after taking into account the potential increase in indirect with most of the reduction largely being achieved by pen- taxes. Finally, alternative reforms of the tax-free allowance sions. However, in cash terms, households beginning in the are considered, and estimates of their likely impact on pov- second decile were net payers to the treasury in 2014, as the erty, inequality, and the potential fiscal cost are presented. share of taxes paid exceeded the cash benefits received for all The simulations show that there are potential efficiency but the poorest 10 percent of the population. -

Poverty Dynamics in Poland Selected Quantitative Analyses

Poverty Dynamics in Poland Selected quantitative analyses Miriam Beblo Stanis³awa Golinowska Charlotte Lauer Katarzyna Piêtka Agnieszka Sowa CASE – Warsaw / ZEW – Mannheim This research was made possible thanks to the financial support of Volkswagen Foundation. Review by Irena Topiñska, Phd Key words: alcohol abuse, education, labour supply, poverty, social exclusion, social transfers, unemployment © CASE – Center for Social and Economic Research, Warsaw 2002 Graphic Design: Agnieszka Natalia Bury DTP: CeDeWu Sp. z o.o. ISSN 1506-1647, ISBN 83-7178-296-9 Publisher: CASE – Center for Social and Economic Research ul.Sienkiewicza 12,00-944 Warsaw,Poland tel.: (4822) 622 66 27, 828 61 33, fax (4822) 828 60 69 e-mail: [email protected] Poverty Dynamics in Poland Contents Contributors . 5 Abbreviations . 6 Introduction . 7 1. Poverty in Poland: Causes, Measures and Studies . 11 Stanis³awa Golinowska Introduction . 11 1.1. The Causes of Poverty . 11 1.1.1. The Communist Legacy . 12 1.1.2. Transition and Poverty. 14 1.1.3. Challenges of the New Economy Versus Poverty . 18 1.2. Defining and Measuring Poverty . 21 1.2.1. The Poverty Line Approach . 22 1.2.2. Measures of Poverty Applied in Poland . 23 1.2.3. Research into Poverty . 26 1.3. The Picture of Poverty in the 1990s . 30 1.3.1. Most Vulnerable Groups . 32 1.4. Concluding Remarks. 34 2. Labour Supply Effects of Social Security Transfers. 37 Katarzyna Piêtka Introduction . 37 2.1. Background . 38 2.1.1. Review of Social Policy in Poland During the Transition . 38 2.1.2. Social Expenditures. -

Reducing Poverty Sustaining Growth

Reducing Poverty Sustaining Growth Scaling Up Poverty Reduction A Global Learning Process and Conference in Shanghai, May 25–27, 2004 Case Study Summaries Acknowledgments The World Bank gratefully acknowledges the participation of, and contributions from, the Governments of Austria, Belgium, Canada, France, Germany, Italy, Spain, Sweden, and the United Kingdom, as well as the United Nations Development Programme. Many hundreds of people cooperated to bring these cases to you—too many to be acknowledged individually in the summaries. For the full text of any of the cases summarized here, as well as contact information for the authors and sponsors of the case, check after the conference at http://www.reducingpoverty.org. Except as otherwise noted in the summaries, the cases summarized here were commissioned by the World Bank Institute through the World Bank operational vice presidencies. This unedited collection of case studies was prepared for use at the Scaling Up Poverty Reduction conference in Shanghai, China, held in May 2004. A thorough synthesis of the findings of the conference will be published as a book by the World Bank late in 2004. © 2004 The International Bank for Reconstruction and Development/ The World Bank 1818 H Street, NW Washington, DC 20433 Telephone 202-473-1000 Internet www.worldbank.org E-mail [email protected] All rights reserved. The findings, interpretations, and conclusions expressed herein are those of the author(s) and do not necessarily reflect the views of the Board of Executive Directors of the World Bank or the governments they represent. The World Bank does not guarantee the accuracy of the data included in this work. -

Poland and the European Union

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Matkowski, Zbigniew; Rapacki, Ryszard; Prochniak, Mariusz Book Part — Published Version Comparative Economic Performance: Poland and the European Union Suggested Citation: Matkowski, Zbigniew; Rapacki, Ryszard; Prochniak, Mariusz (2016) : Comparative Economic Performance: Poland and the European Union, In: Weresa, Marzenna Anna (Ed.): Poland. Competitiveness Report 2016. The Role of Economic Policy and Institutions, SGH Warsaw School of Economics, Warsaw, pp. 11-35 This Version is available at: http://hdl.handle.net/10419/147256 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. may exercise further usage rights as specified in the indicated licence. www.econstor.eu POLAND POLAND COMPETITIVENESS REPORT 2016 Competitiveness is usually understood as a broad category embedded in the level of a nation’s prosperity, taking into account not only economic factors, but also so-called THE ROLE OF ECONOMIC POLICY AND INSTITUTIONS sustainable competitiveness based on social and environmental pillars. -

The Growth-Poverty Nexus: Evidence from Kazakhstan

ADB Institute Discussion Paper No. 51 The Growth-Poverty Nexus: Evidence from Kazakhstan Akram Esanov July 2006 Akram Esanov is Lecturer at Department of Economics, University of Toronto, Canada. This paper was written when he was a Visiting Researcher at Asian Development Bank Institute (ADBI). The views expressed in this paper are the views of the author and do not necessarily reflect the view or policies of ADBI nor Asian Development Bank. Names of countries or economies mentioned are chosen by the author/s, in the exercise of his/her/their academic freedom, and the Institute is in no way responsible for such usage. Abstract This paper examines the extent, dynamics and distribution of poverty in Kazakhstan during the period of 2001-2004. Furthermore, the study decomposes changes in poverty into growth and redistribution components. The analysis demonstrates that over the period of 2001-2004 both the incidence and the depth of poverty have significantly declined, improving the living standards of population. The decomposition of changes in poverty reveals that the fall in poverty was entirely driven by the improvements in the inequality, whereas the growth appears to be poverty enhancing. 2 1. Introduction A salient feature of the initial phase of transition from a planned economy to a market economy in post-soviet states has been a dramatic decline in living standards. Researchers attributed this phenomenon to a steep fall in aggregate output and sharp increases in income inequality. One of the understudied topics in this literature, however, is the analysis of the impact of substantial economic growth on poverty dynamics, which was characteristic of most transition economies in the second half of the 1990s. -

Income Inequality and Income Stratification in Poland

STATISTICS IN TRANSITION new series, Spring 2014 269 STATISTICS IN TRANSITION new series, Spring 2014 Vol. 15, No. 2, pp. 269–282 INCOME INEQUALITY AND INCOME STRATIFICATION IN POLAND Alina Jędrzejczak1 ABSTRACT Income inequality refers to the degree of income differences among various individuals or segments of a population. When the population has been partitioned into subgroups, according to some criterion, one common application of inequality measures is evaluation of the relationship between inequality in the whole population and inequality in its constituent subgroups in order to work out the within and the between subgroups contributions to the overall inequality. In the paper selected decomposition methods of the well-known Gini concentration ratio were discussed and applied to the analysis of income distribution in Poland. The aim of the analysis was to verify to what extent the inequality in different subpopulations contributes to the overall income inequality in Poland and to what extent their members form distinct segments or strata. To provide the decomposition of the Gini index the population of households was partitioned into several socio-economic groups on the basis of the exclusive or primary source of maintenance. Moreover, the households were divided by economic regions using the Eurostat classification units NUTS 1 as well as by family type defined by the number of children. Key words: income distribution, income inequality. 1. Introduction In the analysis of income inequality it may be relevant to assign inequality contributions to various income components (such as labor income or property income) or to various population subgroups associated with socio-economic characteristics of individuals (age, sex, occupation, composition of their household, ethnic groups, etc.). -

Poverty Watch 2020 POLAND

Contents Summary .......................................... 1 Poverty is more than low income and economic hardship .............................. 3 Situation on the labour market and in household budgets .............................. 4 ‘Europe 2020’ in Poland - a big overachievement of an unambitious target ....................................................... 6 Poverty and material and social deprivation in general, a continuous improvement, but high risk of social exclusion ........................................... 8 Poverty among children, seniors and POVERTY people with disabilities ..................... 10 Poverty in voivodeships.................... 13 In-Work Poverty ............................. 15 WATCH Experiencing multidimensional poverty .. 16 Impact of the COVID-19 epidemic on income and poverty ........................... 18 2020 EAPN Poland responds to the COVID-19 epidemic - examples ....................... 20 Policy against income poverty and its problems in 2019 and the first half of POLAND 2020 ............................................... 22 Policies against poverty and social monitoring poverty and social exclusion for the period 2021-2027 ...... 25 policy against poverty in Poland in About EAPN Poland ............................ 29 2019 and the first half of 2020 17 October 2020 International Day for the Eradication of Poverty EAPN Polska POVERTY WATCH 2020 Summary 1. SUCCESS IN EXCEEDING AN UNAMBITIOUS TARGET ▪ In 2011, as part of the implementation of the EU 2020 Strategy, the Polish Government assumed that by 2020, the number of Poles living in poverty would be 1.5 million fewer. In the EU as a whole, this was to be 20 million fewer people. As EAPN Poland, we have repeatedly pointed out that the target adopted by Poland is inadequate and lower than the possibilities. ▪ By 2019, not 1.5 million Poles had come out of poverty, but a total of 4.8 million, which was already a quarter of the EU target. -

Luxembourg Income Study Working Paper Series

Luxembourg Income Study Working Paper Series Working Paper No. 144 Income Inequality and Poverty of Economies in Transition Marina Popova August 1996 Luxembourg Income Study (LIS), asbl 1 INCOME INEQUALITY AND POVERTY OF ECONOMIES IN TRANSITION by Marina Popova Karelian Research Center Russian Academy of Sciences Petrozavodsk The main aim of this paper is to compare income inequality and poverty in former socialist countries with those in a market society, focusing on the ways in which social welfare systems operate in different states. Evidence of inequality and poverty is considered for three countries: Russia, Poland, and Finland. These issues in Russia are considered at the level of country as well as that of one of its regions - the Republic of Karelia. Another approach arisen here is devoted to sensitivity of the results to the techniques used to measure income inequality and poverty. INTRODUCTION The transition of Eastern European countries into market economies is accompanied by the transformation of all their social welfare systems. In efforts to create a new concept of social welfare, each country tries to learn through experience, to compare results, and to prevent further stresses. In relation to these efforts, the problem of poverty is nowadays a matter of constant concern and discussion. Poverty is not a new phenomenon in the life of former socialist countries, but its nature has changed. The stratification of society has made the problem of poverty much more apparent. In addressing the problem of poverty, it is important to answer the following questions: what are the differences between the poverty rate and the composition of poor in a market economy and in ____ Note: This paper summarizes two independent projects.