Stockholm, Sweden Market Snapshot

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

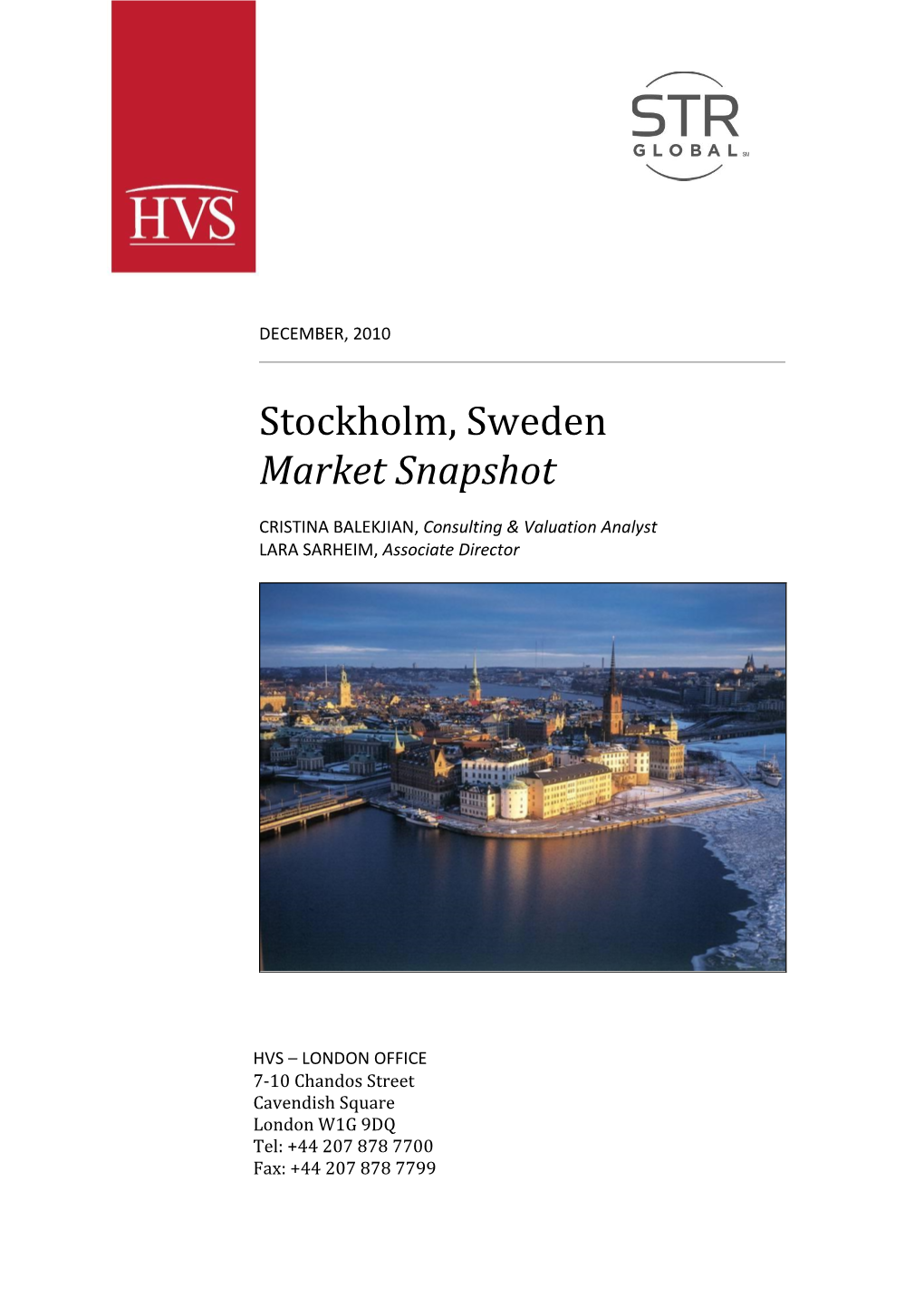

Stockholm, Sweden

U.S. Embassy Stockholm, Sweden Please follow the steps below before your immigrant visa interview at the U.S. Embassy Contact information in Stockholm, Sweden. Please note that interviews for applicants residing in Sweden, Denmark and Norway are conducted in Stockholm. U.S. Embassy Dag Hammarskjölds Väg 31 115 89 Stockholm Step 1: Register your appointment online Sweden If you are a resident of Sweden, you need to register your address online. Registering Email: your address provides us with the information we need to return your passport to [email protected] you after your interview. Registration is free. Click the “Register” button below to Website: register. Please make sure to register your delivery location before your interview in se.usembassy.gov order to avoid delay in the return of the immigrant visa. Residents of Denmark and Norway should not register their address online. The address registration will be Cancel and Reschedule: handled at the time of the interview. [email protected] Map: If you want to cancel or reschedule your appointment, you will be able to do so after you register your appointment. Register Step 2: Get a medical exam in Sweden, Denmark or Norway As soon as you receive your appointment date, you must schedule a medical exam in Sweden, Denmark or Norway. Click the “Medical Exam Instructions” button below for a list of designated doctors’ offices in Sweden, Denmark or Norway. Please schedule and attend a medical exam with one of these doctors before your interview. Other links Diversity visa instructions Medical Exam Instructions After your interview Frequently asked questions Step 3: Complete your pre-interview checklist Where to find civil documents It is important that you bring all required original documents to your interview. -

PARADE Study Guide Written by Talia Rockland Edited by Yuko Kurahashi

Study Guide, Parade PARADE Study Guide Written by Talia Rockland Edited by Yuko Kurahashi TABLE OF CONTENTS ABOUT THE PLAY ................................................................. 2 GLOSSARY ............................................................................. 3 CONTEXT ............................................................................... 6 MARY PHAGAN MURDER AND LEO FRANK TRIAL TIMELINE ............................................................................... 9 HISOTRICAL INFLUENCES ON THE EVENTS OF PARADE11 TRIAL OUTCOMES .............................................................. 11 SOURCES .............................................................................. 12 1 Study Guide, Parade ABOUT THE PLAY Parade was written by Alfred Uhry and lyrically and musically composed by Jason Robert Brown in 1998. The show opened at the Lincoln Center Theatre on December 17th, 1998 and closed February 28th, 1999 with a total of 39 previews and 85 performances. It won the Tony Award for Best Book of a Musical and Best Original Score and the New York Drama Critics Circle for Best Musical. It also won Drama Desk awards for Outstanding Musical, Outstanding Actor (Brent Carver), Outstanding Actress (Carolee Carmelo), Outstanding Book of a Musical, Outstanding Orchestrations (Don Sebesky), and Outstanding Score of a Musical. Alfred Uhry is a playwright, lyricist and screenwriter. Born in Atlanta, Georgia from German- Jewish descendants, Uhry graduated Brown University in 1958 with a degree in English and Drama. Uhry relocated to New York City where he taught English and wrote plays. His first success was the musical adaption of The Robber Bridegroom. He received a Tony Award nomination for Best Book of a Musical. His other successful works include Driving Miss Daisy, Last Night of Ballyhoo, and LoveMusik. Jason Robert Brown is a composer, lyricist, conductor, arranger, orchestrator, director and performer. He was born in Ossining, New York and was raised Jewish. He attended the Eastman School of Music in Rochester, New York. -

Breast Cancer Patients and Survivors in the Eu Workforce Finland: Supporting Return to Work

A report by The Economist Intelligence Unit THE ROAD TO A BETTER NORMAL: Breast cancer patients and survivors in the EU workforce BREAST CANCER PATIENTS AND SURVIVORS IN THE EU WORKFORCE FINLAND: SUPPORTING RETURN TO WORK Sponsored by: This report is part of a series of profiles focusing on the main employment-related issues affecting female breast 1 Although male breast 1 cancer does occur, it is cancer patients and survivors in selected EU countries. very rare, with an age- adjusted incidence of less Key data than 1 per 100,000 in most Crude breast cancer incidence rate per 100,000: 162.9 (2012, IARC) of Europe and no clear sign of increase or decrease Breast cancer prevalence (five-year) per 100,000: 809.2 (2012, IARC) (Diana Ly et al., “An Labour force participation rate—general: 75.9% (2015, OECD) International Comparison Labour force participation rate—women aged 40-64: 79.8% (2015, EIU calculations from OECD data) of Male and Female Breast Unemployment rate—general: 9.5% (2015, OECD) Cancer Incidence Rates”, International Journal of Unemployment rate—women aged 40-64: 6.6% (2015, EIU calculations from OECD data) Cancer, 2012). This study Breast cancer is a substantial health challenge for Finland. In 2012 the country had Europe’s, and therefore deals exclusively the world’s, seventh-highest crude incidence rate at 162.9 per 100,000 women.2 While this is less with female breast cancer. than Denmark’s burden (185.4 per 100,000), it is well ahead of the rates recorded in its Nordic 2 Unless otherwise stated, neighbours: the average for northern Europe as a whole is 153.6 per 100,000 women. -

Book, Music and Lyrics by Jason Robert Brown the Last Five Years Is Presented Through Special Arrangement with Music Theater International (MTI)

The Last Five Years Book, Music and Lyrics by Jason Robert Brown The Last Five Years is presented through special arrangement with Music Theater International (MTI). All authorized performance materials are also supplied by MTI. 421 West 54th Street, New York, NY 10019, www.MTIShows.com Book, Music and Lyrics by JASON ROBERT BROWN Director’s Note They say, “there are two sides to every story” and in the case of The Last Five Years, “they” couldn’t be more right! We all have our own story, our own goals, our own experiences, that we carry with us throughout our lives. When two lives come together in a relationship, often with different societal parameters of what love is, how relationships should be, and countless other expectations, the relationship is no longer living in each moment, but rather moving from one expectation to the next. The characters of Jamie and Cathy continually remind us of the dangers that expectation can have on, not just romantic, but all variations of human relationships. I chose to produce The Last Five Years because this musical so brilliantly portrays the intimate and often hidden moments that make up a relationship; making it unmistakably familiar to audiences who have experienced the trials of love and loss. Vulnerably told through Jason Robert Brown’s soaring melodies and tight, witty lyrics, The Last Five Years tells the very human story of the struggles we face when we commit ourselves to blind love. Brown wrote this piece after concluding his own five-year marriage, influencing him to create a unique and dynamic form of storytelling; having the show begin at the end of the relationship for Cathy and the beginning for Jamie. -

YMTC "Parade" Press Release

Youth Musical Theater Company FOR IMMEDIATE RELEASE Press Inquiries: Laura Soble/YMTC Phone 510-595-5514 Email: [email protected] Website: www.ymtcbayarea.org PARADE COMING TO EL CERRITO, JULY 20–29. Berkeley, California, June 11, 2019—Youth Musical Theater Company (YMTC) concludes its 13th season with the award-winning musical Parade. It will run July 20–29 at El Cerrito High School Performing Arts Theater. Set in 1913, Parade tells the true story of Leo Frank, a Brooklyn-raised Jew living in Georgia. Frank is put on trial for the murder of thirteen-year-old Mary Phagan, a factory worker he employed. Already deemed guilty in the eyes of everyone around him, Frank suffered the added consequences of sensationalist news stories and a janitor's false testimony. His only defenders were a governor with a conscience and, eventually, his assimilated Southern wife, who finds the strength and love to become his greatest champion. “Parade is a story about one of the most glaring miscarriages of justice in recent American history,” says Director Jennifer Boesing. “It’s also a cautionary tale, a warning against scapegoating, racism, xenophobia, and sensationalism in the media—all issues that we can see playing out in American politics today.” Boesing adds, “Underneath these issues, Parade reveals a deeply human lesson about how love and human connection can be forged, even in a climate of intolerance—a story that needs to be told now more than ever. Theater has the power to change hearts and minds, and the young artists at the heart of YMTC take their role as storytellers very seriously.” The book was written by Alfred Uhry (Driving Miss Daisy), and the music and lyrics by Jason Robert Brown (The Last Five Years, The Bridges of Madison County). -

Denmark Ranked 1 out of 128 Countries on Rule of Law

UNDER EMBARGO – DO NOT PUBLISH UNTIL: 11 March 2020 (3:00 AM Washington DC / Eastern Standard Time) DENMARK RANKED 1 OUT OF 128 COUNTRIES ON RULE OF LAW 2020 WJP Rule of Law Index Shows Sustained Negative Slide Toward Weaker Rule of Law Around the World Denmark Placed 1st out of 24 in the European Union, European Free Trade Association, and North America Region WASHINGTON, DC (11 March 2020) – The World Justice Project (WJP) today released the WJP Rule of Law Index® 2020, an annual report based on national surveys of more than 130,000 households and 4,000 legal practitioners and experts around the world. The WJP Rule of Law Index measures rule of law performance in 128 countries and jurisdictions across eight primary factors: Constraints on Government Powers, Absence of Corruption, Open Government, Fundamental Rights, Order and Security, Regulatory Enforcement, Civil Justice, and Criminal Justice. The Index is the world’s leading source for original, independent data on the rule of law. Denmark’s overall rule of law score remained the same in this year’s Index. At 1st place out of 128 countries and jurisdictions worldwide, Denmark remained in the same position in global rank. Denmark’s score places it at 1 out of 24 countries in the European Union, European Free Trade Association, and North America region* and 1 out of 37 among high income** countries. Denmark, Norway, and Finland topped the WJP Rule of Law Index rankings in 2020. Venezuela, RB; Cambodia; and Democratic Republic of the Congo had the lowest overall rule of law scores—the same as in 2019. -

NOVEMBER 2020 the Economic Impact of Huawei in Poland

THE ECONOMIC IMPACT OF HUAWEI IN POLAND NOVEMBER 2020 The economic impact of Huawei in Poland POLAND Direct Indirect HUAWEI’S ECONOMIC IMPACT IN 2019 Induced Total Totals may not sum due to rounding. SPENDING WITH POLISH SUPPLIERS: €116 million CONTRIBUTION TO GDP EMPLOYMENT €95 800 million jobs €125 4,300 million jobs €126 4,600 million jobs €347 million 9,700 jobs 0.1% of Poland’s total GDP 0.1% of Poland’s total employment TAX REVENUES €175 million 0.1% of Poland’s total tax revenue HUAWEI’S ECONOMIC IMPACT BETWEEN 2015 AND 2019 All figures are annual averages (monetary values in 2019 prices) Spend with Polish suppliers: Contribution to GDP: €74 million €263 million Employment: 7, 200 jobs Tax revenues: Real growth in tax revenues 2015-2019: 135% €119 million 2 The economic impact of Huawei in Poland THE ECONOMIC IMPACT OF HUAWEI IN POLAND Huawei expanded its HUAWEI’S ECONOMIC CONTRIBUTION operations to Poland in 2017, with its representative office Huawei’s contribution to the • In addition, Huawei and the based in Warsaw. Huawei’s Polish economy is captured firms in its supply chain products and services reach through three channels: pay their staff wages. millions of local people, These wage payments Huawei’s direct contribution working alongside providers • are spent on goods and is generated through its own including P4, Orange, T-Mobile services at retail, leisure and operations in Poland, as well and Polkomtel. Huawei has other outlets, stimulating as the direct hiring of Polish made a sizeable contribution additional gross value staff and direct tax payments to the Polish economy over added (GVA), employment to the Polish government. -

The Polish Paradox: from a Fight for Democracy to the Political Radicalization and Social Exclusion

social sciences $€ £ ¥ Article The Polish Paradox: From a Fight for Democracy to the Political Radicalization and Social Exclusion Zofia Kinowska-Mazaraki Department of Studies of Elites and Political Institutions, Institute of Political Studies of the Polish Academy of Sciences, Polna 18/20, 00-625 Warsaw, Poland; [email protected] Abstract: Poland has gone through a series of remarkable political transformations over the last 30 years. It has changed from a communist state in the Soviet sphere of influence to an autonomic prosperous democracy and proud member of the EU. Paradoxically, since 2015, Poland seems to be heading rapidly in the opposite direction. It was the Polish Solidarity movement that started the peaceful revolution that subsequently triggered important democratic changes on a worldwide scale, including the demolition of the Berlin Wall, the collapse of Communism and the end of Cold War. Fighting for freedom and independence is an important part of Polish national identity, sealed with the blood of generations dying in numerous uprisings. However, participation in the democratic process is curiously limited in Poland. The right-wing, populist Law and Justice Party (PiS) won elections in Poland in 2015. Since then, Poles have given up more and more freedoms in exchange for promises of protection from different imaginary enemies, including Muslim refugees and the gay and lesbian community. More and more social groups are being marginalized and deprived of their civil rights. The COVID-19 pandemic has given the ruling party a reason to further limit the right of assembly and protest. Polish society is sinking into deeper and deeper divisions. -

U^T X^Y. Y*Z,. >/; the MUSEUM of MODERN

<^^r B \L~.i >u^t X^y. y*Z,. >/; THE MUSEUM OF MODERN ART 11 WEST 53 STREET. NEW YORK 19. N. Y. No. 85 TIUPHONl! CIICLI MM For Release: Wednesday, July 20, i960 Press Preview: Tuesday, July 19, i960 11 a.m. - k p.m. I MpV Spanish Painting and Sculpture, an exhibition of fifty-four works by sixteen Iaftis^3 who have come into prominence during the past decade, will be on view at the I Museum of Modern Art, 11 West 53 Street, New York City, from July 20 through September 125. Following the New York showing the exhibition will be sent to museums throughout I the country, the first survey of avant-garde Spanish art to tour the United States. As Frank O'Hara, director of the exhibition, points out in the catalog/* the I selection is intended to indicate the diversity of styles and preoccupations by which I some of the leading figures are developing their individual idioms. The artists in- I eluded are the painters Rafael Canogar, Modest Cuixart, Francisco Farreras, Luis IFeito, Manolo Millares, Lucio (Munoz), Manuel Rivera, Antoni Saura, Antonio Suarez, I Antoni Tapies, Joan Josep Tharrats, and Manuel Viola; and sculptors Eduardo Chillida, Martin Chirino, Oteiza (Jorge de Oteiza Embil) and Pablo Serrano. Each is represented by two to four works installed by Wilder Green, Assistant Director of the Department of Architecture and Design. Fifteen private collectors and galleries here and abroad as well as the artists • themselves have lent works to the exhibition. Many have never been shown in this country. -

The Last Five Years Press Release

I N T E R N A T I O N A L C I T Y TH E A T R E NEWS RELEASE FOR IMMEDIATE RELEASE Contact (for media only): Lucy Pollak [email protected] (818) 887-1499 ICT to stream emotional, powerful musical ‘The Last Five Years’ by Jason Robert Brown LONG BEACH, Calif. (May 5, 2021) — International City Theatre virtually presents The Last Five Years, an intimate, emotionally powerful musical by Tony Award-winning composer and lyricist Jason Robert Brown. Directed by Jamie Torcellini, with musical direction by Graham Sobelman, and starring John Battagliese and Gabriela Carrillo (recently seen together in Love Actually, Live! at the Wallis), The Last Five Years will stream June 3 through June 20 on Thursdays, Fridays, Saturdays and Sundays (dark Mondays, Tuesdays, Wednesdays) at www.InternationalCityTheatre.org. Funny and uplifting, The Last Five Years captures some of the most heartbreaking and universally felt moments of modern romance, ingeniously deconstructing a five-year love affair — from meeting to break-up and from break-up to meeting. Jamie, a young up-and-coming novelist, falls in love with Cathy, a struggling actress. Their story is told almost entirely through song, using an intercutting time line device: Jamie's songs start as they first get to know each other and move forward to the end of their marriage, while Cathy's songs begin as the marriage dissolves, moving backwards in time to the beginning of their love. The Last Five Years premiered at Chicago's Northlight Theatre, going on to an off-Broadway production at the Minetta Lane Theatre in New York City. -

Live Music and Translation: the Case of Performances Involving Singing 1

The Journal of Specialised Translation Issue 35 – January 2021 Live music and translation: The case of performances involving singing Lucile Desblache, University of Roehampton ABSTRACT This article explores the multicultural and multilingual context of live music today in relation to translation, focusing primarily on a European context. A first section examines the complex relationship of music and translation, arguing that in many respects, music is a form of translation. The article then focuses on the case of vocal music and/in translation, before considering accessibility in relation to music and how it is understood in this article. Past and current traditions and expectations of translation in live music are discussed in the next section. Two more sections explore respectively contemporary audiences’ preferences, and artists’ engagement with their public, as well as the solutions they find to communicate with their audiences and convey the verbal content of their songs. The conclusion draws on the findings of these sections to emphasise the importance of lyrics translation in the live music scene. It also outlines the key role that music can play in translation, particularly in the cosmopolitan context of live musical events. KEYWORDS Vocal music, popular music, live music, song translation, lyrics translation. 1. Introduction The ways in which music has been produced, disseminated and consumed in the last fifty years have been evolving constantly and rapidly, particularly in the popular arena. The industry focus has been on prioritising portability, so that listeners could access and interact with music individually and ubiquitously. One of the characteristics of popular music is that, with the exception of some electronic dance music (EDM), nearly all its mainstream genres, including pop/rock and rap, are vocal (Every Noise at Once no date). -

About the Author Jason Robert Brown

BRAZOSPORT COLLEGE THEATRE DEPARTMENT PROUDLY PRESENTS Originally Produced for the New York stage by Arielle Tepper and Marty Bell Orginally Produced by Northlight Theatre Chicago, IL Costume Design Lighting Design Shannon Averett Byron Gernand Musical Director Director Clayton Roberts Michael McIntosh Featuring Samantha Blackmar MaKayla Dunn Mason Rod Tomás Whitmarsh April 15-19, 2021 Shakespeare in the Glen Theatre Brazosport College Theatre Department Brazosport College | Lake Jackson TX Shakespeare in at Brazosport College Cast Samantha Blackmar .............................................Cathy MaKayla Dunn .......................................................Cathy Mason Rod .................................................................Jamie Tomás Whitmarsh ..................................................Jamie Songs Still Hurting Shiksa Goddess See, I’m Smiling Moving Too Fast I’m a Part of That The Schmuel Song A Summer in Ohio The Next Ten Minutes A Miracle Would Happen Climbing Uphill If I Didn’t Believe in You I Can Do Better Than That Nobody Needs to Know Goodbye Until Tomorrow/ I Could Never Rescue You Pianist Clayton Roberts THE LAST FIVE YEARS will be performed without an intermission. STREAMING IS PRESENTED BY SPECIAL ARRAGEMENT OF MUSIC THEATRE INTERNATIONAL (MTI) NEW YORK, NY. All authorized performance materials are also supplied by MTI. mtishows.com. Any video and/or audio recording of this production is strictly prohibited. Staff for The Last Five Years Video Streaming Specialist .............Kyle Parrinello Stage