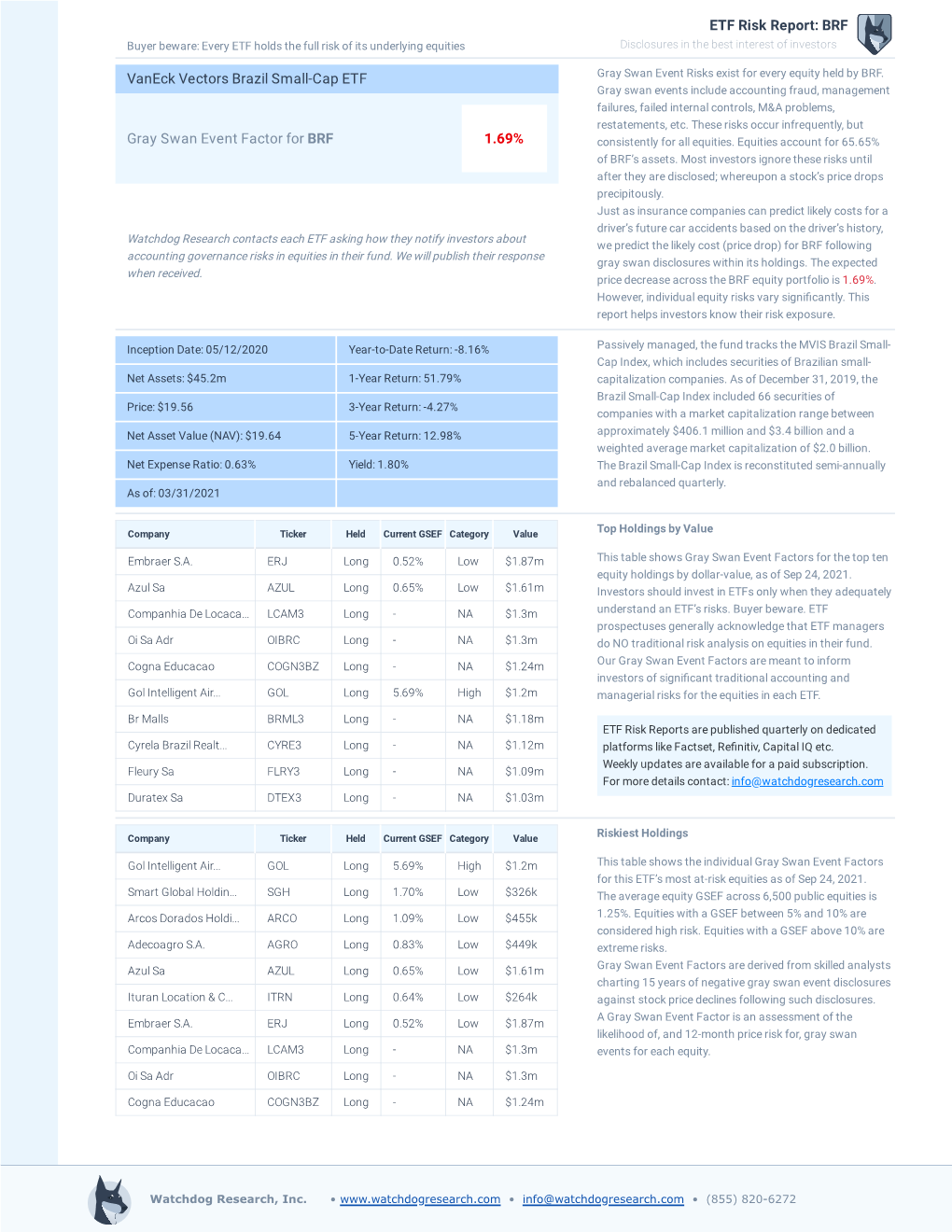

ETF Risk Report: BRF Vaneck Vectors Brazil Small-Cap ETF Gray Swan

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Templeton Latin America Fund - I LU0229944334 31 August 2021 (Acc) USD

Franklin Templeton Investment Funds Latin America Equity Templeton Latin America Fund - I LU0229944334 31 August 2021 (acc) USD Fund Fact Sheet For Professional Client Use Only. Not for distribution to Retail Clients. Fund Overview Performance Base Currency for Fund USD Performance over 5 Years in Share Class Currency (%) Templeton Latin America Fund I (acc) USD MSCI EM Latin America Index-NR Total Net Assets (USD) 733 million Fund Inception Date 28.02.1991 140 Number of Issuers 36 Benchmark MSCI EM Latin America 120 Index-NR Morningstar Category™ Latin America Equity 100 Summary of Investment Objective The Fund aims to achieve long-term capital appreciation by investing primarily in equity securities of issuers 80 incorporated or having their principal business activities in the Latin American region. 60 Fund Management 08/16 02/17 08/17 02/18 08/18 02/19 08/19 02/20 08/20 02/21 08/21 Gustavo Stenzel, CFA: Brazil Discrete Annual Performance in Share Class Currency (%) 08/20 08/19 08/18 08/17 08/16 Ratings - I (acc) USD 08/21 08/20 08/19 08/18 08/17 I (acc) USD 24.44 -20.38 15.27 -13.58 19.77 Overall Morningstar Rating™: Benchmark in USD 34.73 -23.59 8.86 -11.80 22.63 Asset Allocation Performance in Share Class Currency (%) Cumulative Annualised Since Since 1 Mth 3 Mths 6 Mths YTD 1 Yr 3 Yrs 5 Yrs Incept 3 Yrs 5 Yrs Incept I (acc) USD 0.24 -4.37 10.65 0.19 24.44 14.21 18.21 105.68 4.53 3.40 4.66 Benchmark in USD 0.84 -0.65 16.40 5.33 34.73 12.07 21.22 102.56 3.87 3.92 4.55 % Equity 99.03 Past performance is not an indicator or a guarantee of future performance. -

Latin American Fund QUARTERLY LETTER | THIRD QUARTER 2019

Latin American Fund QUARTERLY LETTER | THIRD QUARTER 2019 The Latin American Fund aims to achieve capital growth by investing in a concentrated portfolio of high-quality Latin American growth companies. The Fund seeks high absolute returns over the long term and minimises the level of long-term risk by choosing well- capitalised, high-quality investments at reasonable valuations. INTRODUCTION The fund returned -9.9% (net of fees) in the third quarter and -2.6% year-to-date. While we had a setback in Argentina during the quarter we believe the region is entering a multi-year economic upcycle. In particular, Brazil is passing a series of pro- productivity reforms just as it emerges from a bad recession, setting the scene PETER CAWSTON for a prolonged period of strong growth in this top-ten global economy. We think RUPERT BRANDT, CFA Portfolio Manager Portfolio Manager this is positive for the region as a whole and particularly positive for the private sector in Brazil, where the government will deliberately shrink the market share of state-owned companies, allowing the private sector to grow much faster than the economy without taking undue risk. Interest rates at all-time lows in Brazil will stimulate the economy and should drive a reallocation of local assets from fixed income into equities, potentially kicking off Brazil’s first domestically-driven bull market. We have both spent time in Brazil in the past couple of months and for the first time in years the mood on the ground is very positive. At the end of the quarter we had 64.1% invested in Brazil, 16.5% in Peru, 9.7% in Colombia, 4.8% in Chile, 2.7% in Argentina, and 0.8% in Mexico. -

Latin American Construction Companies' Woes May Not Be Over

EMERGING MARKETS RESTRUCTURING JOURNAL ISSUE NO. 3 — SPRING 2017 Latin American Construction Companies’ Woes May Not Be Over, Yet By BROCK EDGAR and DEVI RAJANI Can Latin American construction Many regional construction companies have experienced companies survive an expected plateau or will likely be going through restructurings. In Mexico, the three largest homebuilders went through restructurings in gross fixed capital formation in a region between 2014 and 2016 and one of Mexico’s largest engineering that so desperately needs infrastructure and construction companies, Empresas ICA, S.A.B. de C.V., investment? is currently being restructured. Similarly, in a process that has been ongoing since 2015, one of Brazil’s largest engineering and construction companies, OAS S.A. is also currently being In recent years, Latin American construction companies have restructured. Looking ahead, the fallout from Odebrecht’s faced deteriorating cash flows due to overexpansion at home admission of foreign bribery will likely affect its engineering or abroad, limited financing availability due to changing and construction business, as well as its consortium partners regulations and/or government investigations (i.e., “Lava throughout Latin America where projects are being cancelled, Jato” in Brazil, also known as the Car Wash Investigation), triggering sureties and bank guarantees. falling commodity prices (primarily oil) and cutbacks in government spending; all of which have led to over-levered Against this backdrop, the uncertainty with respect to -

Abc Brasil Daycoval Linx Sabesp Aes Tiete E Dimed

LISTA DAS EMPRESAS ELEGÍVEIS - CARTEIRA DO ISE 2017 PERÍODO BASE 2016 ABC BRASIL DAYCOVAL LINX SABESP AES TIETE E DIMED LOCALIZA SANEPAR ALFA INVEST DIRECIONAL LOCAMERICA SANTANDER BR ALIANSCE DURATEX LOG-IN SANTOS BRP ALPARGATAS ECORODOVIAS LOJAS AMERIC SAO CARLOS ALUPAR ELETROBRAS LOJAS MARISA SAO MARTINHO AMBEV S/A ELETROPAULO LOJAS RENNER SARAIVA LIVR ANIMA EMBRAER LOPES BRASIL SCHULZ AREZZO CO ENERGIAS BR M.DIASBRANCO SENIOR SOL ARTERIS EQUATORIAL MAGAZ LUIZA SER EDUCA B2W DIGITAL ESTACIO PART MAGNESITA SA SID NACIONAL BANCO PAN ETERNIT MARCOPOLO SIERRABRASIL BANRISUL EUCATEX MARFRIG SLC AGRICOLA BBSEGURIDADE EVEN METAL LEVE SMILES BMFBOVESPA EZTEC MILLS SOMOS EDUCA BR BROKERS FER HERINGER MINERVA SPRINGS BR INSURANCE FERBASA MRV SUL AMERICA BR MALLS PAR FIBRIA MULTIPLAN SUZANO PAPEL BR PHARMA FLEURY MULTIPLUS TAESA BR PROPERT FORJA TAURUS NATURA TARPON INV BRADESCO GAFISA ODONTOPREV TECHNOS BRADESPAR GENERALSHOPP OI TECNISA BRASIL GERDAU OUROFINO S/A TEGMA BRASILAGRO GERDAU MET P.ACUCAR-CBD TELEF BRASIL BRASKEM GOL PARANA TEMPO PART BRF SA GRAZZIOTIN PARANAPANEMA TEREOS CCR SA GRENDENE PARCORRETORA TIM PART S/A CCX CARVAO GUARARAPES PDG REALT TIME FOR FUN CELESC HELBOR PETROBRAS TOTVS CEMIG HYPERMARCAS PETRORIO TRACTEBEL CESP IDEIASNET PINE TRAN PAULIST CETIP IGUATEMI PLASCAR PART TRISUL CIA HERING IMC S/A PORTO SEGURO TRIUNFO PART CIELO INDS ROMI PORTOBELLO TUPY COELCE IOCHP-MAXION POSITIVO INF ULTRAPAR COMGAS ITAUSA PROFARMA UNICASA COPASA ITAUUNIBANCO PRUMO UNIPAR COPEL JBS QGEP PART USIMINAS COSAN JHSF PART QUALICORP V-AGRO COSAN LOG JSL RAIADROGASIL VALE CPFL ENERGIA KEPLER WEBER RANDON PART VALID CSU CARDSYST KLABIN S/A RENOVA VIAVAREJO CVC BRASIL KROTON RODOBENSIMOB WEG CYRELA REALT LE LIS BLANC ROSSI RESID WHIRLPOOL DASA LIGHT S/A RUMO LOG. -

Análise De Empresas 27/07/2018

Análise de Empresas 27/07/2018 EcoRodovias: Bom trimestre, apesar da greve dos ECOR3 caminhoneiros Recomendação: COMPRA Preço-alvo: 12,00 • Na noite de ontem (26), a EcoRodovias divulgou um bom resultado para o Upside: 45,8% 2T18, com o Ebitda ajustado de R$ 401 milhões ficando dentro da nossa 150 ECOR3 X IBOV estimativa; 140 130 • Os principais destaques no período foram: (i) o tráfego total de veículos, 120 110 que teve queda de 5% em base anual; (ii) os custos, que ficaram estáveis 100 em base anual; e (iii) o Ebitda ajustado, que sem os efeitos da greve dos 90 caminhoneiros, teria ficado 11% acima da nossa estimativa e 7% acima do 80 70 ECOR3 IBOV consenso das projeções de mercado; 60 jul-17 out-17 jan-18 abr-18 jul-18 • Seguimos com recomendação de Compra para ECOR3 e preço-alvo de R$ Fonte: Bradesco BBI e Bloomberg 12,00/ação para dezembro de 2019. A greve dos motoristas de caminhão reduziu as receitas no 2T18 em 7% Logística (cerca de R$ 47 milhões) frente ao 1T18. No trimestre, a Ecorodovias reportou Victor Mizusaki* receita líquida de R$ 584 milhões (-2% em base anual), Ebitda ajustado de R$ 401 Ricardo França milhões (-3%) e lucro líquido de R$ 80 milhões (+4% no período). A Ecorodovias +55 11 2178 4202 perdeu R$ 47 milhões de receitas de pedágio devido à greve dos caminhoneiros e [email protected] novas isenções de tarifa de pedágio para eixos traseiros suspensos de caminhões vazios. Por outro lado, os custos permaneceram estáveis e ficaram 3% abaixo das *Analista de valores mobiliários credenciado nossas estimativas, principalmente devido às renegociações de contratos na Ecopistas responsável pelas declarações nos termos do Art. -

BLACKROCK LATIN AMERICA FUND, INC. Form NPORT-P Filed 2021-03-31

SECURITIES AND EXCHANGE COMMISSION FORM NPORT-P Filing Date: 2021-03-31 | Period of Report: 2021-01-31 SEC Accession No. 0001752724-21-068746 (HTML Version on secdatabase.com) FILER BLACKROCK LATIN AMERICA FUND, INC. Mailing Address Business Address 100 BELLEVUE PARKWAY 100 BELLEVUE PARKWAY CIK:877151| IRS No.: 223122997 | State of Incorp.:MD | Fiscal Year End: 1130 WILMINGTON DE 19809 WILMINGTON DE 19809 Type: NPORT-P | Act: 40 | File No.: 811-06349 | Film No.: 21791675 800-441-7762 Copyright © 2021 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document Schedule of Investments (unaudited) BlackRock Latin America Fund, Inc. (Percentages shown are based on Net Assets) January 31, 2021 Par Security Shares Value Security (000) Value Common Stocks Corporate Bonds Argentina 1.7% Brazil 0.0% Globant SA(a) 7,432 $1,426,944 Klabin SA, 2.50%, 06/15/22 BRL 7 $35,211 Brazil 60.5% Lupatech SA, 6.50%, 04/15/21(a)(d)(e) 2,128 Afya Ltd., Class A(a) 51,837 1,150,781 Total Corporate Bonds 0.0% B3 SA - Brasil Bolsa Balcao 388,880 4,250,288 (Cost: $1,124,525) 35,211 Banco Bradesco SA, ADR 1,028,713 4,670,357 Banco BTG Pactual SA 85,786 1,490,288 Shares BB Seguridade Participacoes SA 294,609 1,489,360 Preferred Securities Cia de Locacao das Americas 227,156 1,086,084 Cyrela Brazil Realty SA Empreendimentos e Preferred Stocks 2.1% Participacoes 283,229 1,326,746 Brazil 2.1% Fleury SA 213,936 1,026,786 Gol Linhas Aereas Inteligentes SA, Preference Itau Unibanco Holding SA, ADR 724,629 3,782,563 Shares(a) . -

UEM Factsheet

EMERGING CITIES. EMERGING WEALTH. EMERGING OPPORTUNITIES. Offering long-term value in emerging markets investments MARCH 2020 KEY DATES PERFORMANCE UK closed-end investment trust focused 500 + on long-term total return Launch Date 20 July 2005 450 OBJECTIVE Year End 31 March Utilico Emerging Markets Trust plc (“UEM”) 400 seeks to provide long-term total return by AGM September 350 investing predominantly in infrastructure, Ex-Dividend Dates September, utility and related sectors mainly in December, 300 emerging markets. March & June 250 INVESTMENT APPROACH Dividend Paid Dates September, To seek to invest mainly in companies and December, 200 Mar Mar Mar Mar Mar sectors displaying the characteristics of March & June 16 17 18 19 20 essential services or monopolies such Share price total return* NAV total return* Continuation Vote To be proposed at as utilities, transportation infrastructure, MSCI Emerging Markets Indextotal return (GBP adjusted) the AGM in 2021 communications or companies with a unique product or market position. +Utilico Emerging Markets Limited – UEM’s predecessor Rebased to 100 as at 20 July 2005 PERFORMANCE (Total return*) 1 month 3 months 1 year 3 years Inception Share Price (19.9%) (31.0%) (23.2%) (13.3%) 184.8% Net Asset Value (22.3%) (29.2%) (24.9%) (17.1%) 215.5% MSCI Emerging Markets Index (GBP adjusted) (12.9%) (18.3%) (13.7%) (3.7%) 186.7% ROLLING 12 MONTH PERFORMANCE (Total return*) 12 Months to Mar 20 Mar 19 Mar 18 Mar 17 Mar 16 Share Price (23.2%) 5.4% 7.1% 24.9% (1.8%) Net Asset Value (24.9%) 3.5% 6.6% 26.2% 1.7% MSCI Emerging Markets Index (GBP adjusted) (13.7%) (0.0%) 11.7% 34.5% (9.3%) *Total return is calculated based on undiluted NAV/share price plus dividends reinvested and adjusted for the exercise of warrants and subscription shares FUND DETAILS ORDINARY SHARES Ticker: UEM.L CAPITAL STRUCTURE INVESTMENT MANAGEMENT FEE NAV at launch+ 98.36p Gross Assets less Current Liabilities £461.4m 0.65% of net assets plus Company NAV (cum income) 181.84p Bank Debt £(47.1)m Secretarial Fee. -

Disclosure Ranking of Environmental Impacts of Brazilian Companies: Analysis Using Methods Multicriteria

Disclosure Ranking of Environmental Impacts of Brazilian Companies: Analysis Using Methods Multicriteria Fabricia Silva da Rosa 1 Mara Vogt 2 Larissa Degnhart 2 Nelson Hein 2 Maria Margarete Brizzola 1 1 – Universidade Federal de Santa Catarina – Brazil 2 – Universidade Regional de Blumenau - Brazil Introduction The disclosure of social and environmental data by businesses is considered a dialogue between such businesses and their stakeholders, as the latter demonstrate interest in social and environmental activities developed by the former, which are evidence of businesses’ commitment to satisfying their corporate social responsibility (Lu & Abeysekera, 2014). Therefore, social and environmental disclosure by companies is expected to function as an effective management strategy for developing and maintaining good relations among stakeholders. Research question Objective Based on the use of the Analyzing the ranking of multi-criteria disclosure of methodologies T-ODA environmental impacts by and TOPSIS, what is the Brazilian companies ranking of disclosure of through the multi-criteria environmental impacts methodologies T-ODA and of Brazilian companies? TOPSIS. ENVIRONMENTAL DISCLOSURE The corporate The growing challenges environmental disclosure pertaining to environmental has considerable economic preservation have forced potential, given the scarcity businesses to change their of alternative sources of operational structures, thus information. However, the improving the disclosure of environmental disclosure by their policies, as well as companies is only partially their actions towards the regulated (Ane, 2012), and environment (Trierweiller, it tends to vary considerably Severo Peixe, Bornia & Campos, 2012). from company to company (Rosa et al, 2015). MATERIAL AND METHODS Population: companies belonging to the Brazilian Index 100 (IBr-X100) listed on the BM&FBovespa, constituting a total of 100 enterprises. -

John Hancock Emerging Markets Fund

John Hancock Emerging Markets Fund Quarterly portfolio holdings 5/31/2021 Fund’s investments As of 5-31-21 (unaudited) Shares Value Common stocks 98.2% $200,999,813 (Cost $136,665,998) Australia 0.0% 68,087 MMG, Ltd. (A) 112,000 68,087 Belgium 0.0% 39,744 Titan Cement International SA (A) 1,861 39,744 Brazil 4.2% 8,517,702 AES Brasil Energia SA 14,898 40,592 Aliansce Sonae Shopping Centers SA 3,800 21,896 Alliar Medicos A Frente SA (A) 3,900 8,553 Alupar Investimento SA 7,050 36,713 Ambev SA, ADR 62,009 214,551 Arezzo Industria e Comercio SA 1,094 18,688 Atacadao SA 7,500 31,530 B2W Cia Digital (A) 1,700 19,535 B3 SA - Brasil Bolsa Balcao 90,234 302,644 Banco Bradesco SA 18,310 80,311 Banco BTG Pactual SA 3,588 84,638 Banco do Brasil SA 15,837 101,919 Banco Inter SA 3,300 14,088 Banco Santander Brasil SA 3,800 29,748 BB Seguridade Participacoes SA 8,229 36,932 BR Malls Participacoes SA (A) 28,804 62,453 BR Properties SA 8,524 15,489 BrasilAgro - Company Brasileira de Propriedades Agricolas 2,247 13,581 Braskem SA, ADR (A) 4,563 90,667 BRF SA (A) 18,790 92,838 Camil Alimentos SA 11,340 21,541 CCR SA 34,669 92,199 Centrais Eletricas Brasileiras SA 5,600 46,343 Cia Brasileira de Distribuicao 8,517 63,718 Cia de Locacao das Americas 18,348 93,294 Cia de Saneamento Basico do Estado de Sao Paulo 8,299 63,631 Cia de Saneamento de Minas Gerais-COPASA 4,505 14,816 Cia de Saneamento do Parana 3,000 2,337 Cia de Saneamento do Parana, Unit 8,545 33,283 Cia Energetica de Minas Gerais 8,594 27,209 Cia Hering 4,235 27,141 Cia Paranaense de Energia 3,200 -

Templeton Latin America Fund LU0592650328 31 August 2021

Franklin Templeton Investment Funds Latin America Equity Templeton Latin America Fund LU0592650328 31 August 2021 Fund Fact Sheet For Professional Client Use Only. Not for distribution to Retail Clients. Fund Overview Performance Base Currency for Fund USD Performance over 5 Years in Share Class Currency (%) Templeton Latin America Fund A (acc) EUR MSCI EM Latin America Index-NR Total Net Assets (USD) 733 million Fund Inception Date 28.02.1991 140 Number of Issuers 36 Benchmark MSCI EM Latin America 120 Index-NR Morningstar Category™ Latin America Equity 100 Summary of Investment Objective The Fund aims to achieve long-term capital appreciation by investing primarily in equity securities of issuers 80 incorporated or having their principal business activities in the Latin American region. 60 Fund Management 08/16 02/17 08/17 02/18 08/18 02/19 08/19 02/20 08/20 02/21 08/21 Gustavo Stenzel, CFA: Brazil Discrete Annual Performance in Share Class Currency (%) 08/20 08/19 08/18 08/17 08/16 Ratings - A (acc) EUR 08/21 08/20 08/19 08/18 08/17 A (acc) EUR 24,49 -27,36 20,49 -12,26 11,11 Overall Morningstar Rating™: Benchmark in EUR 36,49 -29,64 15,01 -9,87 14,88 Asset Allocation Performance in Share Class Currency (%) Cumulative Annualised Since Since 1 Mth 3 Mths 6 Mths 1 Yr 3 Yrs 5 Yrs Incept 3 Yrs 5 Yrs Incept A (acc) EUR 0,63 -1,23 12,46 24,49 8,95 6,21 -19,70 2,90 1,21 -2,08 Benchmark in EUR 1,30 2,90 19,69 36,49 10,46 14,37 -6,45 3,37 2,72 -0,64 % Category Average -0,65 1,84 14,88 29,81 11,09 9,85 -7,68 3,57 1,90 -0,76 Equity 99,03 Cash & Cash Equivalents 0,97 Calendar Year Performance in Share Class Currency (%) 2020 2019 2018 2017 2016 2015 2014 2013 2012 A (acc) EUR -20,49 24,97 -3,68 7,95 27,75 -20,24 -7,03 -20,38 8,69 Benchmark in EUR -20,92 19,63 -1,86 8,69 34,96 -23,18 -0,13 -17,10 6,99 Past performance is not an indicator or a guarantee of future performance. -

ANNUAL REPORT 2015 Worldreginfo - 89A874dc-2Db7-4517-9E22-96F61e512268 TABLE of CONTENTS ABOUT THIS STRATEGY and 03 | REPORT 23 | INVESTMENTS 25 Intangible Assets

ANNUAL REPORT 2015 WorldReginfo - 89a874dc-2db7-4517-9e22-96f61e512268 TABLE OF CONTENTS ABOUT THIS STRATEGY AND 03 | REPORT 23 | INVESTMENTS 25 Intangible assets MESSAGE FROM THE ECONOMIC | CHAIRMAN OF THE BOARD 30 | PERFORMANCE 06 30 Market context 31 Results 37 Capital markets MESSAGE 08 | FROM THE CEO SOCIAL AND 41 | ENVIRONMENTAL PERFORMANCE 42 People 10 | ITAÚSA 44 Society 10 Profile 45 Environment 11 Subsidiaries 14 Itaúsa Presence 15 Ownership structure GRI G4 47 | SUMMARY INDEPENDENT CORPORATE AUDITORS’ LIMITED GOVERNANCE 60 | 17 | ASSURANCE REPORT 20 Risk management 21 Ethical behavior CORPORATE 63 | INFORMATION Annual Report 2015 WorldReginfo - 89a874dc-2db7-4517-9e22-96f61e512268 01 ABOUT THIS REPORT WorldReginfo - 89a874dc-2db7-4517-9e22-96f61e512268 REPORT PROFILE As a way of maintaining a transparent relationship with its stakeholders, Itaúsa – Investimentos Itaú S.A. (Itaúsa) presents its Annual Report 2015, which covers the period between January 1 and December 31, 2015. The report contains the initiatives and achievements for the year and includes information about the economic, social and environmental performance of the four major subsidiaries that make up the holding: Itaú Unibanco Holding S.A. (Itaú Unibanco), Duratex S.A. (Duratex), Elekeiroz S.A. (Elekeiroz) and Itautec S.A.– Itautec Group (Itautec), the results of which are reflected in Itaúsa’s Financial Statements. |GRI G4-28, G4-29, G4-30, G4-17| As from 2009, the report complies with the guidelines of the Global Reporting Initiative (GRI) and, for the third time, uses the G4 version, Comprehensive option, that includes the management approach related to the most relevant DETAILED INFORMATION IS aspects and with greater impact from the perspective of the Company and its stakeholders. -

Integrated Report 2018 Contents 06

INTEGRATED REPORT 2018 CONTENTS 06 42 Human capital 01 03 Message from 07 the Management 45 Reputational capital 02 08 06 Introduction 57 Intellectual capital 03 09 09 Itaúsa 64 Materiality 67 Summary of 04 GRI content 75 Independent 20 Value creation auditors' limited assurance report 05 77 Glossary 79 Corporate 27 Financial information capital MESSAGE 01 FROM THE MANAGEMENT We proceed in our pursuit of sustainable value creation to our stockholders and society, attentive to investment opportunities. 3 GRI Message from the Management As a holding company, our challenge is managing capital We have also strengthened the monitoring of the investees’ and investment portfolio efficiently, focused on the sus- performance and endeavored the best efforts so that com- tainable value creation to stakeholders. panies with a consolidated position in our portfolio are able to raise their profitability and efficiency levels and exert- in Due to its relevant weight in our results, Itaú Unibanco creasingly more discipline in the use of capital. remains our greatest asset – and will continue to do so. We are however attentive to other opportunities to Another concern of ours is ensuring that investees are increase our portfolio and bring attractive returns, and aligned with good practices in people management – and for exceeds Itaúsa’s cost of capital. We target well-established this reason we are part of the Personnel Committee, set up companies, with good cash generation, a consistent history at Itaú Unibanco and Duratex, and the People Committee, set of results, preferably that own recognized brands and up at Alpargatas. operate in sectors with low execution and regulatory risks.