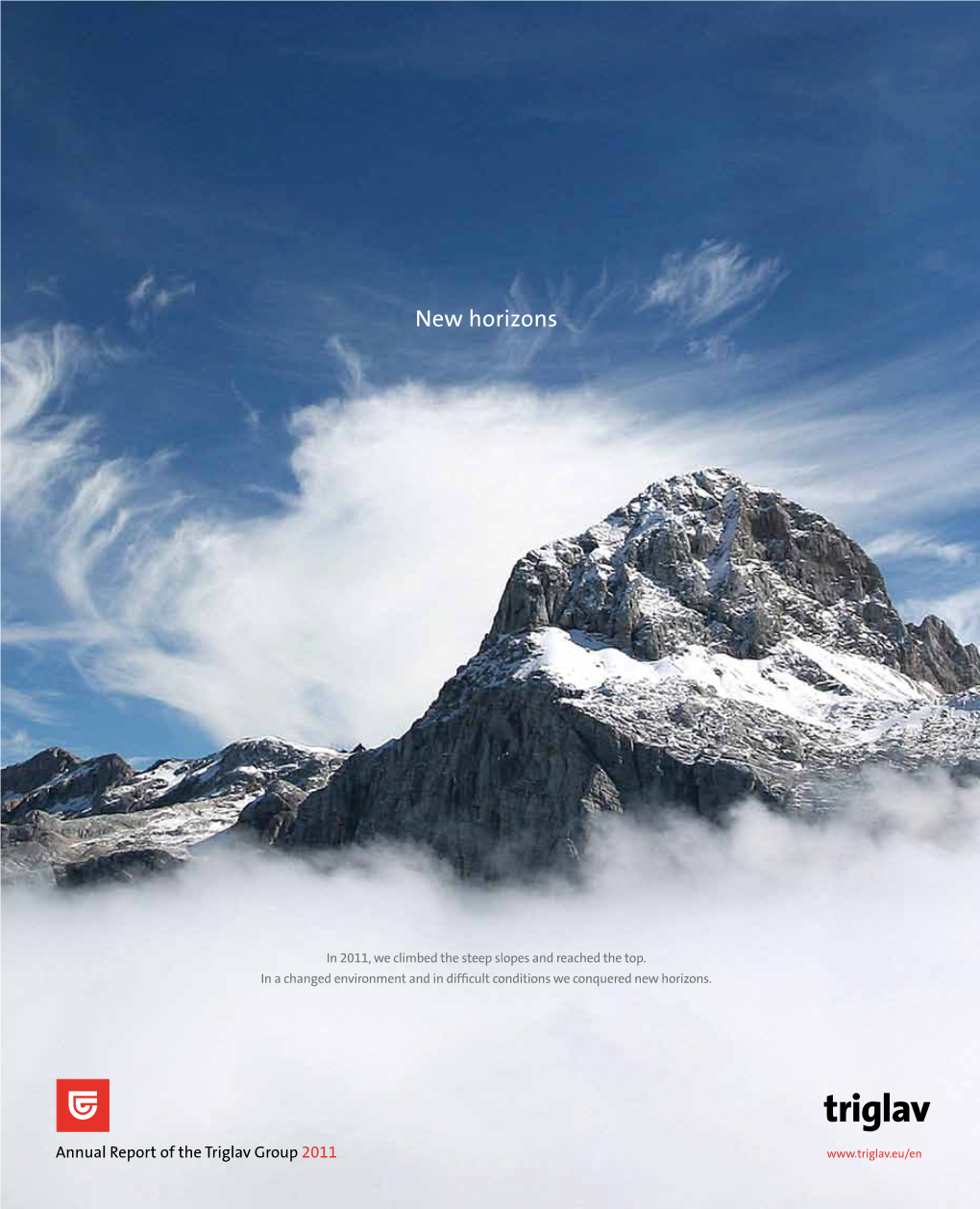

New Horizons

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Unaudited Interim Report of the Triglav Group and Zavarovalnica Triglav D.D. for the Period from 1 January 2020 to 30 June 2020

Unaudited Interim Report of the Triglav Group and Zavarovalnica Triglav d.d. for the period from 1 January 2020 to 30 June 2020 MANAGEMENT BOARD: President: Andrej Slapar Members: Uroš Ivanc Tadej Čoroli Barbara Smolnikar David Benedek Marica Makoter Ljubljana, August 2020 Credit rating Gross written premium for insurance, co-insurance and reinsurance contracts in EUR million Triglav Group Zavarovalnica Triglav "A" 673.4 of the Triglav Group 630.2 with a stable medium-term outlook 385.3 399.9 H1 2019 H1 2020 Net profit before tax in EUR million Triglav Group Zavarovalnica Triglav 41.7 40.6 33.0 31.6 H1 2019 H1 2020 Combined ratio of the Triglav Group Loss ratio Expense ratio 93.2% 92.4% 28.1% 28.2% 65.1% 64.3% H1 2019 H1 2020 Dear shareholders, business partner and colleagues, In the first half of 2020, we operated in the challenging conditions caused by the COVID-19 pandemic at a global level. The Triglav Group gave priority to protecting the health of its employees, clients, partners and other stakeholders, which remains our concern in the future. In these difficult times, we have continued to pursue our sustainability goals and integration into the environment in which we operate, which we have expressed also through donations to healthcare professionals and other service providers in the field during the pandemic. When the epidemic was declared in our markets, we successfully activated the Group’s business continuity plan. We are pleased with how quickly and efficiently we have been able to adapt to change. We provided our services to clients using already developed strategic solutions (for example, an omni-channel sales approach, digital and other solutions for remote business), which was received very well. -

Annual Report of the Triglav Group 2008

SAFETY. ASSISTANCE. RESPONSIBILITY. annual report of the triglav group 2008 WorldReginfo - 2adfe117-307a-408f-90c7-0539eb75de50 WorldReginfo - 2adfe117-307a-408f-90c7-0539eb75de50 annual report of the triglav group 22008008 WorldReginfo - 2adfe117-307a-408f-90c7-0539eb75de50 WorldReginfo - 2adfe117-307a-408f-90c7-0539eb75de50 content 3 business overview 8 1. FINANCIAL HIGHLIGHTS OF THE TRIGLAV GROUP IN 2008 54 9. PERFORMANCE OF THE TRIGLAV GROUP IN 2008 8 1.1 Zavarovalnica Triglav d.d. - Company Profi le 54 9.1 Gross written premium for insurance and co-insurance 8 1.2 Financial highlights of the Triglav Group contracts in 2008 9 1.3 Performance of Zavarovalnica Triglav d.d. 57 9.2 Gross claims paid in 2008 9 1.4 Triglav Group 60 9.3 Gross operating costs in 2008 10 1.5 Activities of the Triglav Group 61 9.4 Risk equalisation in 2008 11 2. ADDRESS BY THE PRESIDENT OF THE MANAGEMENT BOARD 62 10. FINANCIAL RESULT OF THE TRIGLAV GROUP IN 2008 15 3. REPORT OF THE SUPERVISORY BOARD 68 11. FINANCIAL STANDING OF THE TRIGLAV GROUP IN 2008 26 4. VALUES, MISSION AND VISION OF THE TRIGLAV GROUP 71 12. RISK MANAGEMENT 26 4.1 Values 71 12.1 Measures for insurance risk management 26 4.2 Mission 73 12.2 Measures for fi nancial risk management 26 4.3 Vision 75 12.3 Operational risk management measures 75 12.4 Internal audit 27 5. TRIGLAV GROUP STRATEGY 2009 - 2011 27 5.1 The Triglav Group in the 2009 - 2011 period 77 13. DEVELOPMENT AND MARKETING ACTIVITIES 27 5.2 Strategic platform IN THE TRIGLAV GROUP 27 5.3 Strategic objectives for three major regions 77 13.1 Marketing and sales activities 28 5.4 Strategic measures 79 13.2 Development activities 81 13.3 Investments in property and equipment in 2008 30 6. -

Triglav Group

Triglav Group Audited consolidated annual report for the year ended at December MANAGEMENT BOARD: President: Members: Ljubljana, "# March "&' WorldReginfo - 8fab634d-bd99-4b97-a352-e98eb0bd996d ZAVAROVALNICA TRIGLAV D.D. HEADQUARTERS MIKLOŠIČEVA CESTA , LJUBLJANA MANAGEMENT REPORT OF THE TRIGLAV GOUP FOR Ljubljana, . March # WorldReginfo - 8fab634d-bd99-4b97-a352-e98eb0bd996d MANAGEMENT REPORT OF THE TRIGLAV GROUP FOR CONTENTS: . THE TRIGLAV GROUP IN ...................................................................................................................... # . STRATEGY AND PLANES OF THE TRIGLAV GROUP ................................................................................... #. CORPORATE GOVERNANCE STATEMENT .................................................................................................. ' (. SHARE CAPITAL AND SHAREHOLDERS OF ZAVAROVALNICA TRIGLAV .................................................. ). DEVELOPMENT AND SALES ACTIVITIES ..................................................................................................... #' '. PERFORMANCE OF THE TRIGLAV GROUP ................................................................................................. (' *. FINANCIAL RESULT OF THE TRIGLAV GROUP IN ............................................................................. '' +. FINANCIAL STANDING OF THE TRIGLAV GROUP IN ........................................................................ ' . CASH FLOW STATEMENT ........................................................................................................................... -

Triglav Group Xxxx Presentation

Triglav Group Investor Presentation 3 April 2020 Current Coronavirus situation Triglav is the highest mountain in Slovenia and the highest peak of the Julian Alps (2,864 meters/9,396 ft). Current Coronavirus situation In coronavirus situation Triglav activated its business continuity plan¹: Protection of employees and clients: All appropriate measures have been taken to protect our employees (e.g. remote work), clients and ensure business continuation. Triglav is continuously adjusting these measures as the situation changes. Client Services Continuity: Insurance and AM services are adapted to the situation on individual #stayhome markets, e.g. in Slovenia exclusively through electronic and telecommunication channels (no physical Zavarovalnica contacts with clients in sales, claim settlement and other client solutions). Triglav is still available to you Efficient risk management: In the current conditions, Triglav comprehensively manages increased [email protected] 080 555 555 risks associated with the current situation. Due to the many unknowns, it is not yet possible to fully assess the effects of the pandemic. Nevertheless, Triglav assesses that its insurance and investment portfolios are sufficiently resilient and that the capital position is appropriate to cope with the increased risks arising from the COVID-19 pandemic situation and the financial markets. Due to uncertainty and increased volatility in the environment, it is currently not possible to reliably assess the impact of these conditions on the Group’s business performance. This impact will depend on the duration of the crises, among other things. Our regular information will be published in accordance with our financial calendar (page 13), in case of a material change in the circumstances or performance estimates of Triglav Group in relation to forecasts, we will transparently inform the public. -

Triglav Group Xxxx Presentation

Triglav Group Investor Presentation 2020 Unaudited Results March 2021 Disclaimer The information, statements or data contained herein has been prepared by Triglav Corporate officers. Zavarovalnica Triglav, d.d., or any member of Triglav Group, or any Zavarovalnica Triglav employee or representative accepts no responsibility for the information, statements or data contained herein or omitted here from, and will not be liable to any third party for any reason whatsoever relating to the information, statements or data contained herein or omitted here from. Such information, statements or data may not be prepared according to the same standards and requirements than the information, statements or data included in Triglav’s own reports and press releases are prepared to, and accordingly the level of information and materiality and nature of the disclosures may be different. Undue reliance should not be placed on the information, statements or data contained herein because they are subject to known and unknown risks and uncertainties and can be affected by other factors that could cause actual results to differ materially from those expressed or implied in such information, statements or data. Moreover, the information, statements and data contained herein have not been, and will not be, updated or supplemented with new or additional information, statements or data. 2 2020 2020 2021 Appendix Highlights Unaudited Outlook Results Financials & Investments 2020 HIGHLIGHTS Our mission is to build a safer future. 4 2020 Key Financials During COVID-19 -

Unaudited Interim Report of the Triglav Group and Zavarovalnica Triglav D.D

Unaudited Interim Report of the Triglav Group and Zavarovalnica Triglav d.d. for the period from 1 January 2020 to 31 March 2020 MANAGEMENT BOARD: President: Andrej Slapar Members: Uroš Ivanc Tadej Čoroli Barbara Smolnikar David Benedek Marica Makoter Ljubljana, May 2020 Credit rating Gross written premium for insurance, co-insurance and reinsurance contracts in EUR million "A" Triglav Group Zavarovalnica Triglav of the Triglav Group 348.9 with a stable 317.2 medium-term outlook 211.4 198.5 Q1 2019 Q1 2020 Net profit before tax in EUR million Triglav Group Zavarovalnica Triglav 29.9 26.4 22.9 19.9 Q1 2019 Q1 2020 Combined ratio of the Triglav Group Loss ratio Expense ratio 91.6% 93.9% 26.8% 27.1% 64.8% 66.9% Q1 2019 Q1 2020 Dear shareholders, business partner and colleagues, The first quarter of 2020 was marked by the COVID-19 pandemic and the Triglav Group quickly and effectively adapted to this changed situation. Priority was given to protecting the health of all stakeholders and to maintaining business continuity in all markets. In doing so, we used strategic solutions that we had systematically developed over the years, such as the omni- channel sales approach and digital and other remote business solutions. We are pleased to say that our clients received this way of doing business very well. The Triglav Group generated a consolidated profit of EUR 26.4 million before tax in the first three months of 2020. Its 12% decrease primarily resulted from the deteriorated situation in the financial markets and major CAT events, while the impact of premium income on profit was positive. -

Triglav Group Xxxx Presentation

Triglav Group Investor Presentation Triglav Group Investor Presentation December 2018 Table of Contents General information ………………………………………………. 3 - 12 Strategy ………………………………………………. 6 -7 Capital management policy ………………………………………………. 14 Dividend policy ………………………………………………. 16 Triglav Group in 9M 2018 ………………………………………………. 17 - 28 Triglav Group’s Markets ………………………………………………. 29 - 37 Appendix ………………………………………………. 38 - 41 Triglav Group Investor Presentation 2 Equity Story Modern, innovative and dynamic insurance- financial group, firmly remaining the leader both in Slovenia and Adria region 2017-2020 Focus on profitability and selective expansion Fast growth in the markets 2010 outside Slovenia 2008 Listing on the Ljubljana SE 2000 Leading position in Slovenia, expansion started (by 2007 presence in all existent markets) Transformation into a public limited company. Established in Austro-Hungarian Empire as Expansion of business. the first Slovenian insurance company 1990 3 founded with domestic capital. 1900 Triglav Group ▪ 38 companies Triglav Group: ▪ Over 5.100 employees ▪ Parent company Zavarovalnica Triglav founded in 1900. Two-tier board system. ▪ Insurance Core business: ▪ Asset management ▪ BUILDING A SAFER FUTURE for all our stakeholders, while being committed to responsible and Triglav mission: sustainable development. ▪ In 6 countries in Adria region, international through inward reinsurance Market position: ▪ Leading insurance - financial group in Adria region and in Slovenia Ratings: ▪ A / stable outlook ▪ Listed on Ljubljana Stock -

Slovenia Croatia Bosnia and Herzegovina Montenegro North Macedonia Serbia

<< >> Triglav Group and Zavarovalnica Triglav in 2019 Business Report Risk Management Accounting Report Table of Contents The Triglav Group and Zavarovalnica 14 Triglav d.d. Annual Report 2019 2.6 Activities, markets and position of the Triglav Group5 Slovenia The Triglav Group is the leading insurance/finan- st cial group in Slovenia and the Adria region as well 1 rank, 35.5% market share as one of the leading groups in South-East Europe. +10% written premium*** The Group operates on seven markets in six coun- tries. Furthermore, it operates in the wider interna- tional environment through partnerships with for- Croatia eign insurance brokerage and agency companies. th 8 rank, 4.6% market share +14% written premium*** Serbia th 5 rank, 6.4% market share* +19% written premium*** Montenegro st 1 rank, 38.7% market share +11% written premium*** Bosnia and Herzegovina th 6 rank, 7.7% market share** +9% written premium*** North Macedonia * Q1-3 2019 data ** H1 2019 data st *** The data show the growth 1 rank, 13.8% market share of the Triglav Group’s gross written premium by an indi- +1% written premium*** vidual market. 5 GRI GS 102-2, GS 102-4, GS 102-6 << >> Triglav Group and Zavarovalnica Triglav in 2019 Business Report Risk Management Accounting Report Table of Contents The Triglav Group and Zavarovalnica 15 Triglav d.d. Annual Report 2019 Strategic activities Insurance Asset management Non-life Own insurance portfolio (asset backing liabilities and Life backing funds) Pensions Mutual funds and individual asset management Health Reinsurance Pension funds << >> Triglav Group and Zavarovalnica Triglav in 2019 Business Report Risk Management Accounting Report Table of Contents The Triglav Group and Zavarovalnica 16 Triglav d.d. -

TRIGLAV GROUP WE ARE BUILDING a SAFER FUTURE TRIGLAV GROUP Key Features

TRIGLAV GROUP WE ARE BUILDING A SAFER FUTURE TRIGLAV GROUP Key Features Core business – 3 pillars Insurance Third-party asset management Banking Triglav Group Parent company Zavarovalnica Triglav, d.d. 31 subsidiaries and 12 associated companies Market presence in 8 countries S&P rating A/stable Key figures H1 2011 GPW: 549.9 mio EUR (-1%) Net profit: 34.1 mio EUR Combined ratio: 89.0% (-9 p.p.) Equity: 514 mio EUR (+3 %) TRIGLAV GROUP The core business is insurance Insurance Profit by business in 2010 Non-life 40 Life 27,8 Supplementary pensions 30 Health 20 Asset management 5,8 Mutual funds In EUR million 10 0,4 Investment companies -7,4 Investment holdings 0 Real Estate -10 Banking NON-LIFE LIFE HEALTH OTHER Significant interest in Abanka Vipa, d.d. 3 TRIGLAV GROUP Market presence with non-insurance businesses according to local opportunities/needs Banking Other Insurance Asset management (presence only trough (Supporting bussines) significant interest) Slovenia Zavarovalnica Triglav, d.d. Triglav DZU, d.o.o. Abanka Vipa, d.d. Triglav INT, d.d. Pozavarovalnica Triglav Re, d.d. Triglav Naložbe, d.d. TRI-PRO, d.o.o. Triglav, Zdravstvena zavarovalnica, d.d. Triglav nepremi čnine, d.d. AS Triglav, d.o.o. Triglavko, d.o.o. Skupna pokojninska družba, d.d. Croatia Triglav Osiguranje, d.d. Bosnia in Triglav BH Osiguranje, d.d. Polara Invest, d.d. Autocentar BH, d.o.o. Herzegovina Triglav Krajina Kopaonik, a.d. PROF-IN, d.o.o. TRI-PRO BH, d.o.o. Unis automobili i dijelovi, d.o.o. -

Triglav Group Xxxx Presentation

Triglav Group Investor Presentation 2017 Results March 2018 Table of Contents About Triglav Group and Financial Highlights General information ……………………………………………………………………………….………………………………………....................................... 5 Core Business …………………………………………………………………………….………………………………………………….…....................................... 6 Capital Management Policy …………………………………………………...................................................................................................... 9 Capital Adequacy, Risk Profile ………………………………………………………………………………................................................................... 10 Dividend Policy……………………………………………………………………….………….......................................................................................... 11 Equity Story ……………………………………………………………………………...................................................................................................... 12 Shareholders, ZVTG Share ……………………………………………………………………………….......................................................................... 13-14 Management Board ..…....................................................................................................................................................................... 15 Financial Reporting Triglav Group in 2017 ……………………………………………………………………………….................................................................................. 17-18 Structure of Profit before Tax of Triglav Group ……………………………………………………………………………………………….………………. 19-20 Equity, ROE and Gross Technical Provisions ……………………………………………………………………………………………………….…………… -

Belgrade, Serbia, November 7 2017, Hotel Hyatt Regency Belgrade

Belgrade, Serbia, November 7 2017, Hotel Hyatt Regency Belgrade Belgrade Stock Exchange and WOOD & Company 2017 Investor Conference will be organized during the 16th Belgrade SE International Conference, on November 7, in Belgrade Hyatt Regency Hotel. Companies from Serbia and other CEE countries will meet with investors for scheduled 1-on-1 meetings, lasting up to 45 minutes. In order to apply for the Investor Conference, please submit completed Investor Registration Form and send it by e-mail to Ms. Karolina Drach-Kowalczyk, [email protected]. For more info, please contact us by phone number: +48 22 222 15 52. Location Hyatt Regency Belgrade Milentija Popovica 5 11070 Belgrade Serbia Tel: +381 11 3011234 Fax: +381 11 3112234 Email: [email protected] Accommodation For the Conference participants accommodation is provided at discounted prices in Hyatt Regency Belgrade Hotel: standard single room at the rate of 135 € daily per room, and double use of 150 € daily per room (rates are per night and include breakfast and internet. Rates do not include VAT 8% and tourist tax EUR 1,5 p.p.). If you choose to stay in this Hotel, please download Hotel Reservation Form or contact us, to get further details. The accommodation and travel expenses are covered by participants. Scheduling Meetings will be scheduled according to the investors’ requests and the availability of free slots for each company at the moment of application. Preliminary schedule will be supplied to each participant by October 20. After that, further changes, will be distributed on an “as needs” basis. Belgrade Stock Exchange International Conference UPGRADE IN BELGRADE More details about the Belgrade Stock Exchange 16th International Conference UPGRADE IN BELGRADE 2016 may be found at the Conference website. -

Business Report for 2018

Pozavarovalnica Triglav Re, d.d. SUMMARY OF THE ANNUAL REPORT 2018 TRIGLAV RE / Business Report 2018 TABLE OF CONTENTS STATEMENT OF MANAGEMENT’S RESPONSIBILITIES 5 1. OPERATING PERFORMANCE AND EVENTS IN 2018 8 1.1. FINANCIAL HIGHLIGHTS OF TRIGLAV RE, D.D. 8 1.2. SIGNIFICANT EVENTS IN 2018 8 1.3. SIGNIFICANT EVENTS AFTER THE END OF 2018 9 1.4. ADDRESS BY THE PRESIDENT OF THE MANAGEMENT BOARD 10 2. REPORT OF THE SUPERVISORY BOARD 13 3. GENERAL INFORMATION ON TRIGLAV RE, D.D. 20 3.1. COMPANY PROFILE 20 3 3.2. BASIC DATA ON TRIGLAV RE, D.D. 20 3.3. TRIGLAV GROUP 22 3.4. SHAREHOLDERS’ EQUITY AND SHAREHOLDERS OF TRIGLAV RE, D.D. 23 3.5. CREDIT RATING OF TRIGLAV RE, D.D. 23 4. DECLARATION OF THE COMPANY MANAGEMENT 25 4.1. GOVERNANCE POLICY 25 4.2. STATEMENT OF COMPLIANCE WITH THE CORPORATE GOVERNANCE 25 CODE OF THE COMPANIES WITH THE STATE CAPITAL INVESTMENT AND COMMITMENT TO THE OTHER CODES 5. GENERAL ECONOMIC ENVIRONMENT IN 2018 28 5.1. ECONOMIC ENVIRONMENT 28 5.2. CAPITAL MARKETS 30 5.3.. INSURANCE MARKET 31 5.4. INSURANCE MARKET IN SLOVENIA 32 6. RISK MANAGEMENT 35 6.1. RISK MANAGEMENT SYSTEM 36 6.2. PROCESS OF RISK MANAGEMENT 39 6.3. OWN RISK AND SOLVENCY ASSESSMENT (ORSA) 40 6.4. CAPITAL MANAGEMENT 41 6.5. TYPES OF RISKS AND THEIR MANAGEMENT SYSTEM 42 6.6. FUTURE CHALLENGES IN RISK MANAGEMENT 59 TRIGLAV RE / Business Report 2018 7. FINANCIAL RESULTS 61 7.1. REINSURANCE PREMIUMS 61 7.2.