Including Management Board Report on Performance of Mbank SA

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Financial Statements of Asseco Poland S.A

Asseco Poland S.A. Annual Report Annual Report for the year ended 31 December 2017 Financial Statements of Asseco Poland S.A. for the year ended 31 December 2017 FINANCIAL STATEMENTS OF ASSECO POLAND S.A. for the year ended 31 December 2017 FINANCIAL HIGHLIGHTS OF ASSECO POLAND S.A. ............................................................................................ 5 INCOME STATEMENT OF ASSECO POLAND S.A. ................................................................................................ 8 STATEMENT OF COMPREHENSIVE INCOME OF ASSECO POLAND S.A. .............................................................. 9 STATEMENT OF FINANCIAL POSITION OF ASSECO POLAND S.A. ..................................................................... 10 STATEMENT OF CHANGES IN EQUITY OF ASSECO POLAND S.A. ...................................................................... 12 STATEMENT OF CASH FLOWS OF ASSECO POLAND S.A................................................................................... 13 SUPPLEMENTARY INFORMATION TO THE FINANCIAL STATEMENTS ............................................................... 14 I. GENERAL INFORMATION............................................................................................................................... 14 II. BASIS FOR THE PREPARATION OF FINANCIAL STATEMENTS ......................................................................... 15 1. Basis for preparation ........................................................................................................................... -

Winter in Prague Tuesday 5 December to Friday 8 December 2017

emerging europe conference Winter in Prague Tuesday 5 December to Friday 8 December 2017 Our 2017 event held over 4 informative and jam-packed days, will continue the success of the previous five years and host almost 3,000 investor meetings, with over 160 companies representing 17 countries, covering multiple sectors. For more information please contact your WOOD sales representative: WOOD & Company Save Warsaw +48 222 22 1530 the Date! Prague +420 222 096 452 conferences 2017 London +44 20 3530 0611 [email protected] Participating companies in 2016 - by country Participating companies in 2016 - by sector Austria Hungary Romania Turkey Consumer Financials Healthcare TMT Atrium ANY Banca Transilvania Anadolu Efes Aegean Airlines Alior Bank Georgia Healthcare Group Asseco Poland AT&S Budapest Stock Exchange Bucharest Stock Exchange Arcelik AmRest Alpha Bank Krka AT&S CA Immobilien Magyar Telekom Conpet Bizim Toptan Anadolu Efes Athex Group (Hellenic Exchanges) Lokman Hekim CME Conwert MOL Group Electrica Cimsa Arcelik Banca Transilvania Cyfrowy Polsat S.A. Erste Bank OTP Bank Fondul Proprietatea Coca-Cola Icecek Astarta Bank Millennium Industrials Luxoft Immofinanz Wizz Air Hidroelectrica Dogan Holding Atlantic Grupa BGEO Aeroflot Magyar Telekom PORR Nuclearelectrica Dogus Otomotiv Bizim Toptan Bank Zachodni WBK Cimsa O2 Czech Republic RHI Kazakhstan OMV Petrom Ford Otosan CCC Bucharest Stock Exchange Ciech Orange Polska Uniqa Insurance Group Steppe Cement Romgaz Garanti Coca-Cola Icecek Budapest Stock Exchange Dogus Otomotiv OTE Vienna -

Annual Report Pgnig 2013

Annual Report PGNiG 2013 Annual Report PGNiG 2013 The following abbreviations and acronyms are used in this Report: • PGNiG – the parent company of the PGNiG Group, i.e. Polskie Górnictwo Naftowe i Gazownictwo SA (Polish Oil and Gas Company) • PGNiG Group – the PGNiG group of companies Contents 6 14 20 Mission Letter from the President Supervisory Board of the Management Board 8 15 24 PGNiG in Numbers Management Board PGNiG on the Stock Market 10 18 28 Key Events Letter from the Chairman Strategy for the of the Supervisory Board PGNiG Group 4 PGNiG 34 58 70 90 Exploration and Heat and electricity Employees Consolidated Financial Production generation Statements for the Year 2013 44 63 76 108 Trade and Storage Corporate Governance Environmental Protection Contact 54 66 82 Distribution Risks The PGNiG Group Annual Report 2013 5 Mission statement 6 PGNiG Our mission is to provide secure and reliable supplies of clean and environmentally friendly energy using competitive and innovative solutions. We are true and faithful to our traditions and to the trust our customers place in us, but also remain open to new challenges and changes. Acting in the best interests of our shareholders, customers and employees, we strive to be a reliable and trustworthy partner, pursuing business growth and value creation in accordance with the principles of sustainable development. Annual Report 2013 7 Letter from the President of the Letter from the Management Management Chairman of the Supervisory PGNiG on the Stock Strategy for the Exploration and Mission PGNiG in Numbers Key Events Board Board Supervisory Board Board Exchange PGNiG Group Production PGNiG in Numbers The PGNiG Group is the leader in the Polish natural gas market. -

W Warszawie Sa Wprowadzenie Indeksu Wig30

GIEŁDA PAPIERÓW WARTOŚCIOWYCH W WARSZAWIE S.A. WPROWADZENIE INDEKSU WIG30 SIERPIEŃ 2013 Zmiany na warszawskiej giełdzie Nowe indeksy na GPW Zmiany na GPW Nowy mnożnik w Nowe kontrakty kontraktach terminowych terminowe w ofercie GPW na WIG20 -2- Rozwój GPW od wprowadzenia indeksu WIG20 Indeks WIG20 publikowany jest od ponad 19 lat. W tym czasie: Liczba spółek notowanych na Głównym Rynku GPW wzrosła z 24 do 443 (w tym 45 spółek zagranicznych z ponad 20 krajów) Kapitalizacja spółek krajowych wzrosła z ponad 8 mld zł do blisko 540 mld zł Wartość obrotów ogółem na rynku akcji wzrosła z 11 710 mln zł do 264 312* mln zł Liczba Członków Giełdy wzrosła z 23 do 58 (w tym 25 zagranicznych podmiotów) * Zannualizowane dane za okres styczeń – czerwiec 2013 r. -3- Rozwój rynków i oferty produktowej GPW 1994 2013 Rynek kasowy Rynek Rynek Rynek kasowy akcji Rynek produktów Treasury Główny Rynek GPW NewConnect instrumentów Catalyst towarowy obligacji strukturyzowanych Bondspot pochodnych Akcje Obligacje Prawa do akcji skarbowe Akcje Rynek akcji dla Kontrakty Certyfikaty KNOCK- Obligacje Hurtowy rynek Rynek energii spółek terminowe OUT korporacyjne obligacji spot Prawa do akcji wzrostowych indeksowe, skarbowych (PDA) akcyjne, Waranty Obligacje Rynek energii Akcje komunalne forward Prawa poboru walutowe Trackery Prawa do akcji Opcje indeksowe Obligacje Rynek gazu spot (PDA) Obligacje spółdzielcze strukturyzowane Rynek gazu Kontrakty Prawa poboru walutowe Obligacje forward Certyfikaty FAKTOR skarbowe Rynek praw Jednostki Certyfikaty TURBO indeksowe Listy zastawne majątkowych Certyfikaty W przygotowa- Planowane ekspresowe, uruchomienie niu obsługa bonusowe, rynku OTC w 2013 r: dyskontowe Opcje na akcje ETF-y spółek Certyfikaty Kontrakty na Odwrotnie Zamienne stopy procentowe W 1994 r. -

Pgnig, PKN Orlen, Altus TFI, Atlanta

Dziennik 07 grudnia 2018 r. Najważniejsze informacje: Indeksy GPW zmiana WIG otw. 59 113,7 0,6% Indeksy - Trakcja wejdzie do indeksu mWIG40, opuści go Netia WIG zam. 58 409,1 -2,2% PGNiG - PGNiG rozpoczyna poszukiwania węglowodorów w Zjednoczonych Emiratach obrót (mln PLN) 832,5 0,6% Arabskich WIG 20 otw. 2 335,3 0,7% PKN Orlen - PKN Orlen podpisał porozumienie ze związkami dot. zmiany ZUZP i podwyżki WIG 20 zam. 2 294,3 -2,6% wynagrodzeń w '19 FW20 otw. 2 330,0 high Sektor bankowy - Zysk netto sektora bankowego w I-X '18 wyniósł 12,7 mld PLN, w X 1,06 mld FW20 zam. 2 301,0 -2,5% PLN - NBP mWIG40 otw. 4 039,7 0,6% mWIG40 zam. 3 997,3 -1,4% Sektor energetyczny - Minister energii wystąpi do szefów RN spółek energetycznych o zbadanie poziomu kosztów Największe wzrosty kurs zmiana Sektor energetyczny - ME zakłada, że wolumen na aukcjach OZE w '19 wyniesie nie mniej niż Budimex 125,80 4,8% 2,5 tys. MW - Tchórzewski AmRest 40,10 1,8% Altus TFI - KNF wszczęła postępowanie administracyjne ws. nałożenia kary na Altus TFI BGŻ BNP Paribas 46,50 1,3% Atlanta - Atlanta Poland i Rockfield ogłosili wezwanie na 2.468.957 akcji spółki, po 4,2 PLN za Neuca 260,00 0,8% akcję AB 17,20 0,6% Biomed-Lublin - Lek ONKO BCG Biomedu-Lublin nie spełnił warunków jakościowych Największe spadki kurs zmiana Biomed-Lublin - Biomed-Lublin zdecydował o emisji obligacji zamiennych na akcje KAZ Minerals 5,32 -6,0% ERG - ERG zakończył przegląd opcji strategicznych; nie wybrał żadnej z rozważanych opcji Raiffeisen 23,79 -5,6% ERG - Robert Groborz zrezygnował z funkcji prezesa -

OA S.A. Fee Regulations

Fee Regulations of the Online Arbitration S.A. 0 Fee Regulations (Appendix No. 1 to the Terms and Conditions for Provision of Electronic Services by Online Arbitration S.A. and Appendix No. 1 to the Terms and Conditions for Arbitrators of the Online Arbitration Court) § 1 List of Fees 1. The Administrator will collect the following fees: a) registration fee for opening User account in the Application, b) fee for proceedings before the Court, consisting of: administrative fee and arbitration fee in a 1:3 proportion, c) fee for the set-off claim, d) fee for issuing an additional copy of the ruling, e) fee for access to archived minutes from a closed case, f) fee for expert opinion. 2. The fees are to be paid to Administrator’s bank account, by bank transfer or through the online payment system in the Application. The payment system is provided by eCard S.A. § 2 Amounts of Fees for Proceedings before the Court and of the Fee for the Set-off Claim. 1. The base rate of the fee for proceedings before the Court will be calculated accordingly to the value of the dispute, i.e.: a) up to 2 200 EUR: 276 EUR, b) from 2 201 EUR to 4 500 EUR: 133 EUR and 6,5% of the value of the dispute (not less than 143 EUR), c) from 4 501 EUR to 11 500 EUR: 430 EUR and 4,0% of the amount over 4 500 EUR, d) from 11 501 EUR to 23 200 EUR: 444 EUR and 3,8% of the amount over 4 500 EUR, e) from 23 201 EUR to 232 500 EUR: 1155 EUR and 2% of the amount over 23 200 EUR, f) from 232 501 EUR to 2 325 600 EUR: 5341 EUR and 0,27% of the amount over 232 1 500 EUR, g) from 2 325 601 EUR: 10 922 EUR and 0,3% of the amount over 2 325 600 EUR. -

Towards Sustainability in E-Banking Website Assessment Methods

sustainability Article Towards Sustainability in E-Banking Website Assessment Methods Witold Chmielarz and Marek Zborowski * Faculty of Management, University of Warsaw, Krakowskie Przedmie´scie26/28, 00-927 Warsaw, Poland; [email protected] * Correspondence: [email protected] Received: 23 June 2020; Accepted: 24 August 2020; Published: 27 August 2020 Abstract: Nowadays, banking services have evolved from offline financial services to online platforms available in the form of websites and mobile applications. While multiple methods exist for evaluation of generic-purpose websites, the appraisal of banking services requires a more sophisticated approach. Multiple factors need to be taken into consideration, revolving not only around technical and usability aspects of the sites, but also considering the economic and anti-crisis factors. Moreover, due to the fact that one of the groups of people interested in banking services assessment are potential clients, which might or might not be technically and theoretically literate, a sustainable approach to banking services evaluation is needed. The main contribution of this paper is a sustainable approach balancing the evaluation accuracy with usage simplicity and computational complexity of evaluation methods. Also, a reference model for banking services evaluation is provided. In practical terms, a set of all significant commercial banking services in Poland is assessed. Last, but not least, a preliminary study of practical applicability of various evaluation methods amongst computer-literate banking clients is performed. Keywords: internet banking; website evaluations; multi-criteria evaluation methods 1. Introduction One of the most important problems associated with bank management at present is how to maintain the existing clients and how to acquire new ones. -

WOOD's Winter in Prague

emerging europe conference WOOD’s Winter in Prague Tuesday 5 December to Friday 8 December 2017 Please join us for our flagship event - now in its6th year - spanning 4 jam-packed days. We expect to host over 180 companies representing more than 15 countries. NEW: attending company (not covered) snapshotsattached! Click here ! For more information please contact your WOOD sales representative: Tuesday: Energy, Industrials and Materials Registration closes Warsaw +48 222 22 1530 Wednesday: TMT and Utilities on 10 November! Prague +420 222 096 453 Thursday: Consumer, Healthcare and Real Estate London +44 20 3530 7685 Friday: Diversified and Financials [email protected] Invited Companies by country Bolded confirmed Austria MOL Group PGNiG Sistema Ukraine AT & S OTP Bank PKN Orlen Tinkoff Bank Astarta Atrium Waberer’s International PKO BP TMK Industrial Milk Erste Group Bank Wizz Air PKP Cargo TransContainer Company Immofinanz PZU VTB Ferrexpo PORR Iraq Tauron X5 Kernel Raiffeisen International Genel Energy Warsaw Stock MHP Strabag Exchange Serbia Telekom Austria Kazakhstan Wirtualna Polska Belgrade Stock United Kingdom Uniqa Insurance Group Nostrum Oil & Gas Work Service Exchange Kaz Minerals Vienna Insurance Steppe Cement NIS Stock Spirits Group Romania Croatia Lithuania Banca Transilvania Slovenia Podravka Siauliu Bankas Bucharest Stock Gorenje Exchange Krka Conpet Czech Republic Poland Petrol SPEAKERS DIGI CEZ Agora Sava Re Ms. Charlotte Ruhe Electrica MD for Central Europe CME Alior Bank Zavarovalnica Triglav Fondul Proprietatea & the Baltics, EBRD CSOB AmRest Medlife Mr. Leszek Balcerowicz Kofola Asseco Poland Sweden Professor, Warsaw Nuclearelectrica Medicover Komercni Banka Bank Millennium School of Economics OMV Petrom Moneta Money Bank Bank Pekao Vostok Emerging and Chairman of FOR Sphera Finance O2 Czech Republic Budimex Mr. -

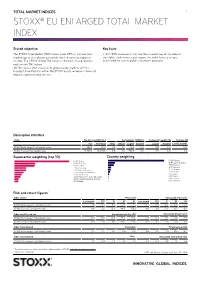

Stoxx® Eu Enlarged Total Market Index

TOTAL MARKET INDICES 1 STOXX® EU ENLARGED TOTAL MARKET INDEX Stated objective Key facts The STOXX Total Market (TMI) Indices cover 95% of the free-float » With 95% coverage of the free-float market cap of the relevant market cap of the relevant investable stock universe by region or investable stock universe per region, the index forms a unique country. The STOXX Global TMI serves as the basis for all regional benchmark for a truly global investment approach and country TMI indices. All TMI indices offer exposure to global equity markets with the broadest diversification within the STOXX equity universe in terms of regions, currencies and sectors. Descriptive statistics Index Market cap (USD bn.) Components (USD bn.) Component weight (%) Turnover (%) Full Free-float Mean Median Largest Smallest Largest Smallest Last 12 months STOXX EU Enlarged Total Market Index 266.7 121.0 0.6 0.1 10.3 0.0 8.5 0.0 N/A STOXX Europe Total Market Index 12,763.5 10,020.5 9.5 2.6 250.9 0.0 2.5 0.0 3.0 Supersector weighting (top 10) Country weighting Risk and return figures1 Index returns Return (%) Annualized return (%) Last month YTD 1Y 3Y 5Y Last month YTD 1Y 3Y 5Y STOXX EU Enlarged Total Market Index 1.2 -3.4 6.4 0.1 1.7 14.7 -4.9 6.3 0.0 0.3 STOXX Europe Total Market Index 0.4 2.0 18.3 44.5 55.2 4.8 2.9 17.9 12.7 8.9 Index volatility and risk Annualized volatility (%) Annualized Sharpe ratio2 STOXX EU Enlarged Total Market Index 15.1 15.0 16.3 23.2 25.3 -0.1 -0.4 0.4 0.0 -0.0 STOXX Europe Total Market Index 11.0 11.1 11.5 20.0 21.6 -0.9 0.3 1.3 0.6 0.4 Index to benchmark Correlation Tracking error (%) STOXX EU Enlarged Total Market Index 0.7 0.7 0.7 0.8 0.9 10.3 10.7 11.9 12.3 12.7 Index to benchmark Beta Annualized information ratio STOXX EU Enlarged Total Market Index 1.0 0.9 1.0 1.0 1.0 0.8 -0.8 -0.8 -1.0 -0.6 1 For information on data calculation, please refer to STOXX calculation reference guide. -

Downgrades Cyfrowy Polsat to NEUTRAL from BUY (FV PLN 28.9), Keeps Play Communications BUY (FV PLN 36.4) and Keeps Orange Polska NEUTRAL (FV PLN 6.4)

Warsaw, June 25, 2020 Konrad Księżopolski, Head of Research, Haitong Bank Haitong Bank in a report from June 24 (08:00) downgrades Cyfrowy Polsat to NEUTRAL from BUY (FV PLN 28.9), keeps Play Communications BUY (FV PLN 36.4) and keeps Orange Polska NEUTRAL (FV PLN 6.4). Valuation Methodology • Cyfrowy Polsat We value Cyfrowy Polsat using a DCF and peer multiples. Using a DCF we arrive at PLN 25.3/sh while our peer valuation yields PLN 32.6/sh. Our final fair value is PLN 28.9/sh, implying 4% potential upside. • Play Communications We value Play using a DCF, DDM and peer multiples. Using a DCF, we derive a fair value of PLN 35.1; using DDM we arrive at PLN 34.9 and peers of PLN 39.2. Applying an equal weighting to each valuation method we obtain a fair value of PLN 36.4, implying 26% upside potential to the current share price. • Orange Polska We value Orange Polska using a DCF and peer multiples where DCF and peers have a 50% weight each. As Orange Polska does not pay dividends, we stopped valuing the stock using the DDM method. Using a DCF, we derive a fair value of PLN 7.0 and using peers of PLN 5.8. Our fair value is PLN 6.4, implying 0% upside potential to the current share price. Risks to Fair Value • Cyfrowy Polsat 1. Weaker than expected delivery on capex and EBITDA synergies on Netia acquisition. 2. Weaker than expected monetization of UEFA TV content. 3. -

WOOD's Winter in Prague

emerging europe conference WOOD’s Winter in Prague Tuesday 5 December to Friday 8 December 2017 Please join us for our flagship event - now in its6th year - spanning 4 jam-packed days. We expect to host over 160 companies representing more than 15 countries. Click here ! For more information please contact Registration closes your WOOD sales representative: Tuesday: Energy, Industrials and Materials Warsaw +48 222 22 1530 Wednesday: TMT and Utilities on 10 November! Prague +420 222 096 453 Thursday: Consumer, Healthcare and Real Estate London +44 20 3530 7685 Friday: Diversified and Financials [email protected] Invited Companies by country Bolded confirmed Austria Iraq PGE PIK Lokman Hekim AT & S DNO PGNiG Polymetal International Migros Ticaret Atrium Genel Energy PKN Orlen Polyus Otokar BUWOG Kazakhstan PKO BP Raven Russia Pegasus Airlines DO&CO KMG EP PKP Cargo Rosneft Petkim Erste Group Bank Nostrum Oil & Gas Prime Car Management Rostelecom Reysas REIT Immofinanz Steppe Cement PZU Rusal Sabanci Holding OMV Lithuania Synthos Severstal Sisecam PORR Siauliu Bankas Tauron Sistema Tat Gida Raiffeisen International Poland Warsaw Stock Exchange Surgutneftegas TAV Strabag Agora Wirtualna Polska Tatneft Tekfen Holding Telekom Austria Alior Bank Work Service Tinkoff Bank Teknosa Uniqa Insurance Group Amica Romania TMK Torunlar REIC Vienna Insurance AmRest Banca Transilvania TransContainer Tofas Warimpex Asseco Poland Bucharest Stock Exchange VTB TSKB Croatia Bank Millennium Conpet X5 Tumosan Podravka Bank Pekao DIGI Yandex Turcas Petrol Czech -

Annual Report 2018 Pgnig - Polish Oil and Gas Company ANNUAL REPORT

Annual Report ANNUAL REPORT 2018 PR Department E-mail: [email protected] 2018 PGNiG - Polish Oil and Gas Company Marketing Department Phone: +48 22 106 45 92 Investor Relations Division Phone: +48 22 106 43 22 Phone: +48 22 106 48 46 Phone: +48 22 106 47 97 E-mail: [email protected] View the Annual Report online Website: ri.pgnig.pl Visit www.en.pgnig.pl PGNiG - Polish Oil and Gas Company to view the Annual Report in interactive format or download it as a PDF file Head Ofice 25 M. Kasprzaka, 01-224 Warsaw Phone: +48 22 106 45 55 Legend Website: pgnig.pl Notes in the margins refer to information highlighted in the Report. key to acronyms and abbreviations used in the Report websites containing additional information aupplementary information, definiotions and comments 07.12.2018 OPEC’s decision 19.12.2018 to reduce oil Contents 12.11.2018 production by LNG supply Calendar of events in 2018 US dollar exchange rate 1.2m barrels per contract with against the zloty at annual day from January Port Arthur LNG, 25.01.2018 highs (PLN 3.84). to June 2019. LLC. PLN President of URE’s decision to reduce the prices and rates of network fees under the PSG Distribution Tariff by 7.37%. 02.10.2018 08.11.2018 29.01.2018 PAO Gazprom and OOO Gazprom Export file LNG supply Agreement with Energinet for the provision of gas 26.06.2018 a complaint to reverse the partial award issued contract with 8 Letter from the Chairman transmission services, as part of the 2017 Open Agreements with Port by the Arbitration Institute.