2014-2015 Audited Financial Statements

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ms Amy Spina Supervior of Special Education Antietam

MS AMY SPINA MR MATTHEW LINK SUPERVIOR OF SPECIAL EDUCATION DIRECTOR OF SPECIAL ED ANTIETAM SCHOOL DISTRICT KUTZTOWN SCHOOL DISTRICT 201 N. 25TH STREET 50 TREXLER AVENUE READING, PA 19606 KUTZTOWN, PA 19530 610-370-2898 610-683-3261 MS KALYN BARTMAN MS BEVERLY GALLAGHER DIRECTOR SPECIAL EDUCATION SUPERVISOR OF SPECIAL ED BOYERTOWN SCHOOL DISTRICT MUHLENBERG SCHOOL DISTRICT 120 N. MONROE STREET 827 BELLEVUE AVENUE BOYERTOWN, PA 19512 LAURELDALE, PA 19605 610-473-3613 610-921-8000 MS MARY DARRACH MS DAWN CAMBRIA DIRECTOR OF SPECIAL ED DIRECTOR OF STUDENT SVCS BRANDYWINE HEIGHTS AREA S.D. OLEY VALLEY SCHOOL DIST 200 WEST WEIS STREET ADMINISTRATION BUILDING TOPTON, PA 19562 17 JEFFERSON STREET 610-682-5182 OLEY, PA 19547 610-987-4100 MR EDWARD J SKOCZEN, JR MS JACKIE DUDASH DIRECTOR SPECIAL EDUCATION DIRECTOR SPECIAL EDUCATION CONRAD WEISER AREA SCHOOL DISTRICT READING SCHOOL DISTRICT 200 LINCOLN DRIVE 800 WASHINGTON STREET WERNERSVILLE, PA 19565 READING, PA 19601 610-678-9236 484-258-7171 MS SHELLY MIECZKOWSKI MS LACIE CUFFIUFFO DIRECTOR OF SPECIAL EDUCATION ELEMENTARY SCHOOL PRINCIPAL DANIEL BOONE AREA SCHOOL DIST SCHUYLKILL VALLEY SCHOOL DIST MATTHEW BROOKE BUILDING SUITE 200 62 ASHLEY WAY 321 N FURNACE ST PO BOX 490 LEESPORT, PA 19533 BIRDSBORO, PA 19508 610-926-4165 610-582-6167 DR. SUZANNE MILLER MS LISA KISS SUPERVISOR OF SPECIAL EDUCATION DIRECTOR/INSTR SUP SVCS EXETER AREA SCHOOL DISTRICT TULPEHOCKEN SCHOOL DIST 4355 DUNHAM DRIVE 27 REHRERSBURG ROAD READING, PA 19606 BETHEL, PA 19507 610-779-7102 717-933-4611 MS GWYNN BOLLINGER DR MARK SAKOIAN DIRECTOR OF STUDENT SVCS DIRECTOR OF PUPIL SERVICES FLEETWOOD MIDDLE SCHOOL TWIN VALLEY SCHOOL DISTRICT 801 N. -

Country State Business

Spotted Lanternfly Permit Participants These Participants have been trained on and found to be compliant with standards listed in the Order of Quarantine and Treatment regarding Spotted Lanternfly for operating in the quarantine area. The companies listed here have agreed to participate in and comply with the terms and conditions of the Order of Quarantine and Treatment which is designed to stop the movement of Spotted Lanternfly within or out of the current quarantine zone. Country State Business Canada AB 1763579 ON INC Canada AB 624889 BC LTD Canada AB 9958169 CANADA INC/LOHGARH TRANSPORT Canada AB ADMIRAL MERCHANTS MOTOR FREIGHT Canada AB BCD AB TRANSPORT LTD Canada AB CANEDA TRANSPORT LTD Canada AB CARAVAN AB INC Canada AB CBS TRUCKING INC Canada AB CERTARUS LTD Canada AB CODE LOGISTICS LTD Canada AB DAY AND ROSS INC Canada AB GILBERT TRUCKING LTD Canada AB JJ TRANSPORT INC Canada AB LANDSTAR Canada AB LOADSAFE CROSSBORDER FREIGHT INC Canada AB LOADSAFE/SL TRANSPORT LTD Canada AB MULLEN TRUCKING CORP Canada AB NORD-DECK TRANSPORT INC Canada AB SNOWY OWL TRANSPORTATION Canada BC 1063282 BC LTD Canada BC BERRY AND SMITH TRUCKING LTD Canada BC I-5 LOGISTICS SERVICES LTD Canada BC INTERNATIONAL MACHINE TRANSPORT INC Canada BC KDMS HOLDINGS INC Canada BC LODEXO LOGISTICS INC Canada BC MAVEN TRANSPORT LTD Canada BC PISTON TRANSPORT LTD Canada BC POWERLANE LOGISTICS INC Canada BC SKY BLUE TRANSPORT Canada BC SRT LOGISTICS Canada BC SYER TRANSPORTATION SERVICES LTD Canada BC TEN FOUR TRUCKING Canada BC THE DAY & ROSS TRANSPORTATION GROUP -

Bus Scholarship Program Eligibility List Eligible Districts/Schools

Bus Scholarship Program Eligibility List *Please note: this list will periodically will be updated and is not a complete list. If you do not know if your school is eligible, indicate this in the application form. Free Lunch Programs: For school districts that are not included in the list below, visit the Pennsylvania Department of Education for a detailed list of schools participating in the National School Lunch Program. The Michener Art Museum will accept applications for school districts/schools with 28% or more on the program. Title I Status: For schools that are not included in the list below, visit the Pennsylvania Department of Education for a detailed list of Title I schools. The Michener Art Museum will accept applications to all schools with Title I status. Eligible Districts/Schools: *PLEASE NOTE: some schools located within eligible school districts may not be qualified to participate in the Bus Transportation Scholarship Program. These are listed with an asterisk*. Pennsylvania Bucks County Bensalem School District Bristol Borough School District Bristol Township School District* Centennial School District* Morrisville School District Quakertown School District* Central Bucks School District* Neshaminy School District* Pennridge School District* Pennsbury School District* Bucks County Technical High School Upper Bucks County Technical High School Berks County Antietam School District Reading School District Boyertown Area School District* James A. Michener Art Museum, April 2018 Brandywine Heights Area School District* Conrad -

Intermediate Unit Reporting

Pennsylvania Department of Education INTERMEDIATE UNIT REPORTING IU14 INTERMEDIATE UNIT NAME Berks County INTERMEDIATE UNIT ADDRESS 1111 Commons Blvd., Reading, PA 19605 INTERMEDIATE UNIT WEBSITE www.berksiu. -

Local Right to Education Task Force

Member School Districts MEMBERSHIP Parents of special education students are the main- BERKS COUNTY of Berks County stay of the Local Task Force, which is required to Intermediate Unit 14 have a 51 percent parent-consumer membership. Also serving on the Local Right to Education Task Local Force are concerned citizens and representatives from: Antietam School District Right To Berks County Intermediate Unit #14 Boyertown Area School District Local school districts Education Brandywine Heights Area School District ARC Advocacy Services Conrad Weiser Area School District Local and regional special education service Task Force Daniel Boone Area School District Exeter Township School District CHILDREN ARE OUR INSPIRATION Fleetwood Area School District It is not enough to have a vision - We must embrace it Governor Mifflin School District The Right to Education Consent Agreement of and act upon it 1972 provided for the establishment of a Local Hamburg Area School District Together Task Force in each of the 29 Intermediate Units Kutztown Area School District to insure that the intent and spirit of the Berks County Muhlenberg School District Agreement is carried out throughout the Local Right to Education Commonwealth. Task Force Oley Valley School District Reading School District Schuylkill Valley School District Tulpehocken Area School District Twin Valley School District BERKS COUNTY Wilson School District Local Right To Education Task Force Wyomissing Area School District 1111 Commons Blvd PO Box 16050 Reading, PA 19612-6050 610-987-8511 Duties of the Resources Meetings Local Task Force 1. Assist families and professionals of school- Arc Advocacy Services Berks County Dates: Tues, Oct 5, 2010 age students with special education needs 610-603-0227 www.marcpa.org/ Tues, Dec 7, 2010 by providing educational and networking Tues, Feb 1, 2011 opportunities so that they are better able Autism Society of Berks County Tues, Apr 5, 2011 to make informed decisions to meet the 610-736-3739 www.autismsocietyofberks.org Agenda: 11:30 a.m.-noon Lunch needs of their student (s). -

Updated ESTIMATED Distribution for Pennsylvania Leas from Winter 2020 Federal Relief ESSER Fund

Updated ESTIMATED Distribution for Pennsylvania LEAs from Winter 2020 Federal Relief ESSER Fund These figures are estimates. The Pennsylvania Department of Education will release actual allocations. For Calculation: ESTIMATED Share of Local Education Agency (LEA) Federal Stimulus Preliminary 2020- school districts listed alphabetically followed by charter schools Winter 2020 21 Title I ($2.002 billion) Allotment ABINGTON HEIGHTS SCHOOL DISTRICT 0.0584% $1,169,220 ABINGTON SCHOOL DISTRICT 0.1113% $2,229,531 ALBERT GALLATIN AREA SCHOOL DISTRICT 0.2529% $5,064,973 ALIQUIPPA SCHOOL DISTRICT 0.1816% $3,637,331 ALLEGHENY VALLEY SCHOOL DISTRICT 0.0361% $723,112 ALLEGHENY-CLARION VALLEY SCHOOL DISTRICT 0.0349% $698,343 ALLENTOWN CITY SCHOOL DISTRICT 1.9803% $39,655,376 ALTOONA AREA SCHOOL DISTRICT 0.5385% $10,783,896 AMBRIDGE AREA SCHOOL DISTRICT 0.1058% $2,119,335 ANNVILLE-CLEONA SCHOOL DISTRICT 0.0365% $731,295 ANTIETAM SCHOOL DISTRICT 0.0527% $1,056,017 APOLLO-RIDGE SCHOOL DISTRICT 0.0473% $946,482 ARMSTRONG SCHOOL DISTRICT 0.2644% $5,293,971 ATHENS AREA SCHOOL DISTRICT 0.0961% $1,923,714 AUSTIN AREA SCHOOL DISTRICT 0.0074% $147,859 AVELLA AREA SCHOOL DISTRICT 0.0138% $275,929 AVON GROVE SCHOOL DISTRICT 0.0789% $1,580,587 AVONWORTH SCHOOL DISTRICT 0.0104% $207,859 BALD EAGLE AREA SCHOOL DISTRICT 0.0522% $1,045,169 BALDWIN-WHITEHALL SCHOOL DISTRICT 0.1143% $2,288,966 BANGOR AREA SCHOOL DISTRICT 0.0846% $1,694,729 BEAVER AREA SCHOOL DISTRICT 0.0368% $736,541 BEDFORD AREA SCHOOL DISTRICT 0.0756% $1,514,649 BELLE VERNON AREA SCHOOL DISTRICT 0.0781% -

TRANSPORTATION CONTACTS Cocalico School District

TRANSPORTATION CONTACTS Cocalico School District Fleetwood School District Transportation Dept./David Lutz Shirley Moll Sue Knauer/Admin Ass’t. Transportation 820 South 4th St. 801 N. Richmond Street PO Box 800 Fleetwood, PA 19522 Denver, PA 17517 610-944-8111 x3 Phone: (717) 336-1574 610-944-6842 FAX (717- 336-1576 FAX [email protected] [email protected] [email protected] Governor Mifflin School District Conrad Weiser School District Transportation Department Maggie Schearer Joanne Witmoyer 44 Big Spring Road 10 S. Waverly Street Robesonia, PA 19551 Shillington, PA 19607 610-693-8561 610-775-1464 x5510 610-693-8586 FAX 610-603-2290 FAX [email protected] [email protected] Daniel Boone School District Muhlenberg School District Ron Smith Denise Rapp 1816 Weavertown Road 801 Bellevue Avenue Douglassville, PA 19518 Laureldale, PA 19605 610-689-4850 610-921-8000 x 1240 610-689-5247 FAX 610-921-8076 FAX [email protected] [email protected] ELANCO (East’n. Lanc Cty.) Oley School District Charlie Kantner or Janet Bergstresser Barry Christman 154 Eastern School Road Stacy Skokowski New Holland, PA 17557 17 Jefferson Street 717-354-1523 Oley, PA 19547 Fax: 717-354-1512 FAX 610-987-4100 x6063 or 6062 [email protected] 610-987-4202 FAX [email protected] [email protected] [email protected] ELCO (East’n. Lebanon Cty) Transportation Office - Rod Sams Reading School District ELCO Intermediate School Barbara Kilpatrick 100 Evergreen Drive 800 Washington Street Myerstown, PA 17067 Reading, PA 19601 [email protected] 610-371-5824 610-371-5872 FAX Exeter School District [email protected] Todd Hurchalla or Richard Wegman 200 Elm Street Reading, PA 19606 Schuylkill Valley School District 610-779-0410 Tara Jacoby 610-406-0376 FAX 929 Lakeshore Drive [email protected] Leesport, PA 19533 610-916-5447 610-926-3960 FAX [email protected] Tulpehocken Area School District Wendy A. -

School Districts in Berks County

School Districts in Berks County Listed below are all the school districts located in Berks County. For more information about the school district, click the website link. Antietam School District 100 Antietam Road Reading, PA 19606 610-779-0554 610-779-4424 (fax) www.antietamsd.org Boyertown Area School District 911 Montgomery Avenue Boyertown, PA 19512 610-367-6031 610-369-7620 (fax) www.boyertownasd.org Brandywine Heights Area 200 W. Weis Street Topton, PA 19562 610-682-5100 610-682-5136 (fax) www.bhasd.k12.pa.us Conrad Weiser Area School District 44 Big Spring Road Robesonia, PA 19551 610-693-8545 610-693-8586 (fax) www.conradweiser.org Daniel Boone Area School District Matthew Brooke Building, Suite 200 321 N. Furnace Street P.O. Box 490 Birdsboro, PA 19508 610-582-6140 610-582-0059 (fax) www.dboone.k12.pa.us Exeter Township School District 3650 Perkiomen Avenue Reading, PA 19606 610-779-0700 610-779-7104 (fax) www.exeter.k12.pa.us Fleetwood Area School District 801 N. Richmond Street Fleetwood, PA 19522 610-944-8111 610-944-9408 (fax) http://www.fleetwoodasd.k12.pa.us/ Governor Mifflin School District 10 S. Waverly Street Shillington, PA 19607 610-775-1461 610-775-6586 (fax) www.governormifflinsd.org Hamburg Area School District Windsor Street Hamburg, PA 19526-0401 610-562-2241 610-562-2634 (fax) www.hasdhawks.org Kutztown Area School District 50 Trexler Avenue Kutztown, PA 19530 610-683-7361 610-683-7230 (fax) www.kasd.org Muhlenberg School District 801 Bellevue Avenue Laureldale, PA 19605-1799 610-921-8000 610-921-8076 (fax) www.muhlsdk12.org Oley Valley School District 17 Jefferson Street Oley, PA 19547 610-987-4100 www.oleyvalleysd.org Reading School District 800 Washington Street Reading, PA 19601-3691 610-371-5611 610-371-5971 (fax) www.readingsd.org Schuylkill Valley School District 929 Lakeshore Drive Leesport, PA 19533-8631 610-916-0957 610-926-3960 (fax) www.schuylkillvalley.org Tulpehocken Area School District 27 Rehrersburg Road Bethel, PA 19507 717-933-4611 717-933-9724 (fax) www.tulpehocken.org Twin Valley School District 4851 N. -

Schools and Libraries 2Q2014 Funding Year 2013 Commitments - 4Q2013 Page 1 of 129

Universal Service Administrative Company Appendix SL38 Schools and Libraries 2Q2014 Funding Year 2013 Commitments - 4Q2013 Page 1 of 129 Applicant Name City State Committed AB GRAHAM ACADEMY ST PARIS OH 11,527.44 ABILENE UNIF SCH DISTRICT 435 ABILENE KS 61,096.09 ACADEMIA DISCIPULOS DE CRISTO MANATI PR 31,203.90 ACADEMIA MENONITA BETANIA AIBONITO PR 23,772.64 ACADEMIA MODERNA WALNUT PARK CA 152,154.72 ACADEMIA NUESTRA SENORA DE FATIMA BARCELONETA PR 15,373.37 ACADEMIA PRESBITERIANA CAROLINA CAROLINA PR 33,167.91 ACADEMIC PERFORMANCE EXCELLENCE ACADEMY LOS ANGELES CA 27,904.58 ACADEMY FOR URBAN LEADERSHIP PERTH AMBOY NJ 16,826.16 ACADEMY ST BENEDICT-STEWART CHICAGO IL 7,952.90 ADDISON COMM SCHOOL DISTRICT ADDISON MI 1,690.75 ADRIAN SCHOOL DISTRICT ADRIAN MI 56,364.00 AF-BROWNSVILLE CHARTER SCHOOL BROOKLYN NY 18,043.78 AF-PROVIDENCE MAYORAL ACADEMY PROVIDENCE RI 21,394.15 AFYA PUBLIC CHARTER MIDDLE BALTIMORE MD 15,317.28 ALABASTER CITY SCHOOL DISTRICT ALABASTER AL 16,433.28 ALACHUA COUNTY SCHOOL DISTRICT GAINESVILLE FL 381,738.99 ALBANY CITY SCHOOL DISTRICT ALBANY NY 548,158.56 ALBANY SCHOOL DISTRICT R 3 ALBANY MO 28,093.47 ALBUQUERQUE CHRISTIAN SCHOOL ALBUQUERQUE NM 2,573.33 ALBUQUERQUE SIGN LANGUAGE ACADEMY ALBUQUERQUE NM 4,232.25 ALCOA CITY SCHOOL DISTRICT ALCOA TN 134,230.08 ALEXANDER CITY SCHOOL DISTRICT ALEXANDER CITY AL 25,967.17 ALEXANDER LOCAL SCHOOL DIST ALBANY OH 47,851.83 ALGIERS CHARTER SCHOOLS ASSOCIATION NEW ORLEANS LA 218,620.40 ALL SAINTS CATHOLIC SCHOOL CINCINNATI OH 6,332.59 ALL SAINTS CATHOLIC SCHOOLS DAVENPORT IA 4,334.40 -

Berks County Anti-Racism and Equity Statement

Exhibit G-1 8/12/2020 Berks County Anti-Racism and Equity Statement Recent events, protests, and discussions around racial injustice throughout our country have sparked increased and urgent dialogue among community leaders to fight racism and address pressing issues of social injustices. The education community is no different. The 18 Berks County school districts, the two career and technology centers, and the Berks County Intermediate Unit are committed to providing safe and inclusive learning and working environments where racism is not tolerated and equity is the standard for the more than 70,000 students here in Berks County, their families, and our teachers and staff. Collectively, we share concern over how systemic racism and social injustices are impacting our Berks County schools and the community. As education leaders, we are obligated to have productive conversations around these inequities and the work that needs to be done to address them. Furthermore, we are committed to deep, sometimes difficult reflection on our routine practices and assumptions that might otherwise go unexamined. Over the years, measures have been taken to increase diversity, equity, and inclusion in our schools — and yet, we still have so much work to do. We believe that education will ultimately create the equitable society all students deserve. Schools can provide every student with opportunities for success and advocate for social justice by ensuring equity and access to a high-quality education, by providing safe and supportive learning environments, and by recognizing the intrinsic value of every individual, regardless of race, culture, sexual identity, disability, or economic status. We must take responsibility for transforming the knowledge, beliefs, and practices that act as obstacles to student learning and staff development, and we must be vigilant in finding solutions and creating action for substantive change in the areas that we as education leaders can control. -

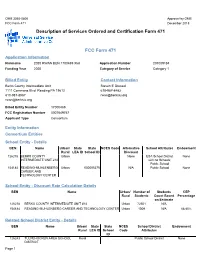

Description of Services Ordered and Certification Form 471 FCC Form

OMB 3060-0806 Approval by OMB FCC Form 471 December 2018 Description of Services Ordered and Certification Form 471 FCC Form 471 Application Information Nickname 2020 RWAN BEN 1700469 Xtel Application Number 201009184 Funding Year 2020 Category of Service Category 1 Billed Entity Contact Information Berks County Intermediate Unit Steven E Dressel 1111 Commons Blvd Reading PA 19612 610-987-8482 610-987-8567 [email protected] [email protected] Billed Entity Number 17000469 FCC Registration Number 0007649767 Applicant Type Consortium Entity Information Consortium Entities School Entity - Details BEN Name Urban/ State State NCES Code Alternative School Attributes Endowment Rural LEA ID School ID Discount 126278 BERKS COUNTY Urban None ESA School District None INTERMEDIATE UNIT #14 with no Schools; Public School 154184 READING-MUHLENBERG Urban 000005275 N/A Public School None CAREER AND TECHNOLOGY CENTER School Entity - Discount Rate Calculation Details BEN Name Urban/ Number of Students CEP Rural Students Count Based Percentage on Estimate 126278 BERKS COUNTY INTERMEDIATE UNIT #14 Urban 72501 N/A 154184 READING-MUHLENBERG CAREER AND TECHNOLOGY CENTER Urban 1009 N/A 68.80% Related School District Entity - Details BEN Name Urban/ State State NCES School District Endowment Rural LEA ID School Code Attributes ID 126243 TULPEHOCKEN AREA SCHOOL Rural Public School District None DISTRICT Page 1 BEN Name Urban/ State State NCES School District Endowment Rural LEA ID School Code Attributes ID 126246 BOYERTOWN AREA SCHOOL Urban Public School District -

School Board Minutes

UPPER ST CLAIR SCHOOL DISTRICT BOARD OF SCHOOL DIRECTORS Mr. Patrick A. Hewitt, President • Mr. Phillip J. Elias, Vice President • Mrs. Amy L Billerbeck Mrs. Barbara L. Bolas • Mrs. Jennifer L. Bowen • Dr. Daphna Gans • Mr. Louis P. Mafrice, Jr. Mrs. Angela B. Petersen • Mrs. Jennifer A. Schnore Dr. John T. Rozzo, Superintendent • Mrs. Jocelyn P. Kramer, Solicitor SCHOOL BOARD MEETING MINUTES Monday, January 25, 2021 @ 7:00pm Executive Session @ 6:00pm (Personnel and Legal Matters) District Administration Building Board Room Notice having been advertised and posted and members duly notified, a Board Meeting of the Board of School Directors was held on January 25, 2021 in the District Administration Room. School Board Members in Attendance: Mr. Phillip J. Elias, Vice President (in-person) Mrs. Amy Billerbeck (virtual) Mrs. Barbara L. Bolas (in-person) Mrs. Jennifer L. Bowen (virtual) Dr. Daphna Gans (virtual) Mr. Louis P. Mafrice Jr. (virtual) Mrs. Angela Petersen (in-person) Mrs. Jennifer Schnore (virtual) School Personnel in Attendance: Dr. John T. Rozzo, Superintendent (in-person) Dr. Sharon K. Suritsky, Assistant/Deputy Superintendent (virtual) Mrs. Amy Pfender, Assistant to the Superintendent (in-person) Mr. Ray Carson, Senior Director of Operations & Administrative Services (in-person) Mr. Scott Burchill, Director of Business & Finance (in-person) Dr. Lou Angelo, Director of Facilities and Operations (virtual) Mr. Raymond Berrott, Director of Technology (in-person) Dr. Judith Bulazo, Director of Curriculum and Development (virtual) Mrs. Cassandra Doggrell, Director of Student Support Services (virtual) Mrs. Lauren Madia, Assistant Director of Student Support Services (in-person) Mr. Bradley Wilson, Director of Strategic Initiatives (virtual) Mrs.