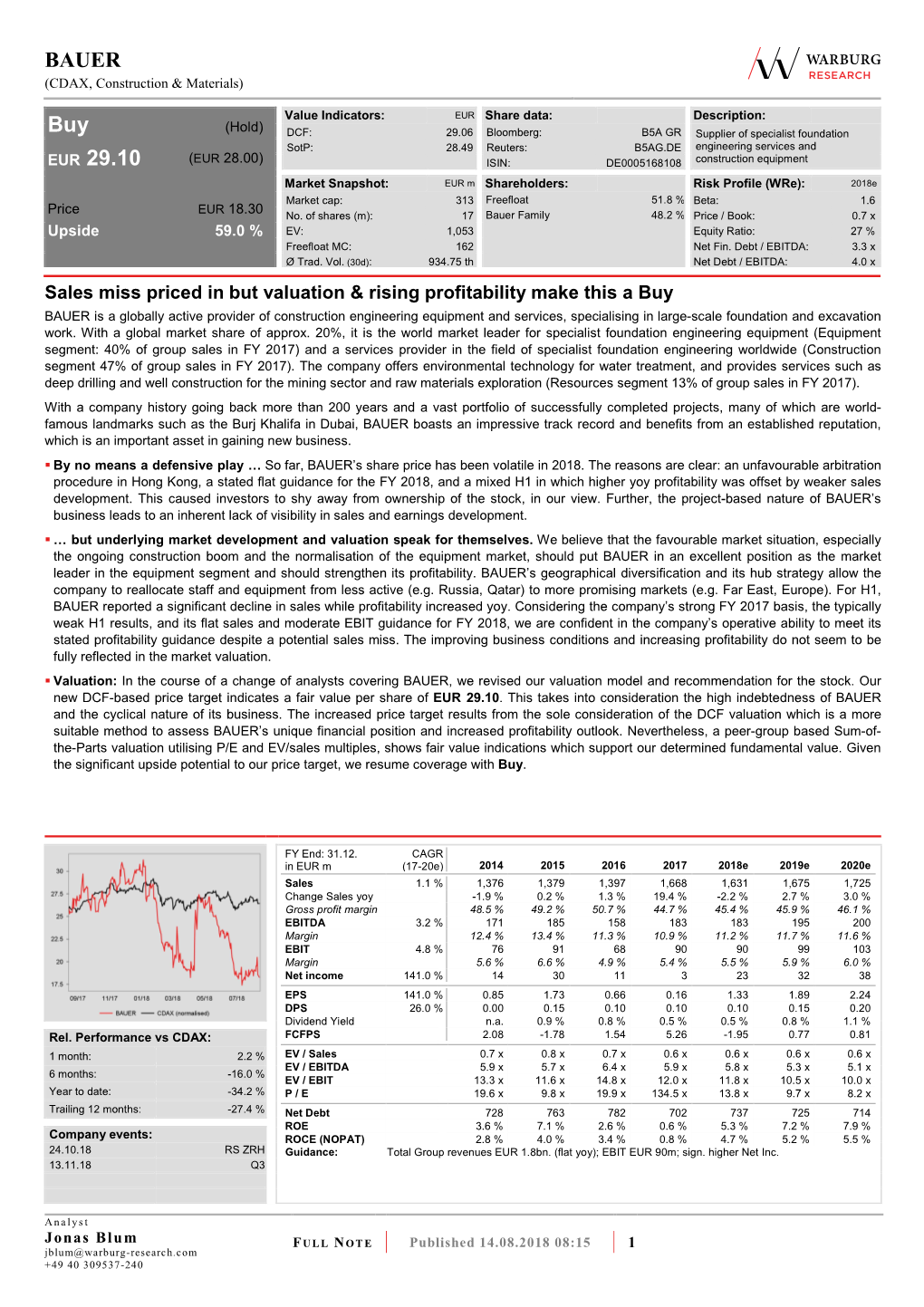

BAUER Buy EUR 29.10

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report 2010 the BAUER Group Is an International Construction and Machinery Manufacturing Concern Based in Schrobenhausen, Bavaria

Annual Report 2010 The BAUER Group is an international construction and machinery manufacturing concern based in Schrobenhausen, Bavaria. The stock market-listed holding company BAUER Aktiengesellschaft is the parent of more than 110 subsidiary businesses across its Construction, Equipment and Resources segments. Bauer is a leader in the execution of complex excavation pits, foundations and vertical seals, as well as in the development and manufacture of related machinery for this dynamic market. The Group also deploys its expertise in the exploration, mining and safeguarding of valuable natural resources. In 2010 the companies of the BAUER Group employed some 9,100 people in around 70 countries and achieved total Group revenues of EUR 1.3 billion. Passion for progress The origins of Bauer date back as far as 1790, and still today the company's success is founded on highly flexible application of the specialist know-how it has built up over those many years. As an innovator and technology leader, Bauer has played a major role in the advancement of the international specialist foundation engineering industry and related business fields. Indeed, today Bauer is also the world market leader in manufacture of the relevant machinery. It is with just such innovative strength and a keen focus on the challenges of the future, that the Group is also developing its recently established Resources segment. The Group at a glance GROUP KEY FIGURES 2007-2010 Change: IFRS in EUR million 2007 2008 2009 2010 2009/2010 Total Group revenues * 1,208.1 1,527.2 -

Our Company Sustainability Report 2014 Our Company

Sustainability Report 2014 Our Company in the Community The Group at a glance Group key figures 2011 – 2014 IFRS in EUR million 2011 2012 2013 2014 Change (adjusted) (adjusted) 2013/2014 Total group revenues 1,371.8 1,435.8 1,504.2 1,560.2 3.7 % of which Germany 370.3 378.6 410.4 440.2 7.3 % International 1,001.5 1,057.2 1,093.8 1,120.0 2.4 % of which Construction 606.6 655.2 741.7 725.6 -2.2 % Equipment 636.5 589.1 628.6 639.2 1.7 % Resources 211.5 262.8 188.9 252.8 33.9 % Sales revenues 1,219.6 1,344.4 1,402.2 1,375.7 -1.9 % Cost of materials 672.8 686.8 755.9 749.2 -0.9 % Staff costs 298.8 325.0 342.8 355.3 3.6 % EBIT 82.3 72.0 30.1 76.4 n/a Net profit or loss 34.1 25.8 -19.4 15.7 n/a Employees (on average over the year) 9,646 10,253 10,264 10,405 1.4 % of which Germany 4,065 4,090 4,144 4,158 0.3 % International 5,581 6,163 6,120 6,247 2.1 % Consolidated balance sheet ASSETS in EUR '000 Dec. 31, 2013 Dec. 31,2014 EQUITY AND LIABILITIES in EUR '000 Dec. 31, 2013 Dec. 31, 2014 NON-CURRENT ASSETS SHAREHOLDERS' EQUITY Intangible assets 35,388 34,440 Equity of BAUER AG shareholders 397,006 399,308 Property, plant and equipment and Non-controlling interests 22,809 19,617 investment property 459,537 446,909 419,815 418,925 Investments accounted for using the equity method 13,249 42,906 NON-CURRENT LIABILITIES Participations 3,613 3,613 Defined benefit plans 81,637 116,358 Deferred tax assets 26,299 30,973 Financial liabilities 279,437 387,816 Receivables from concession arrangements 36,762 0 Other liabilities 6,483 5,959 Other non-current -

225 Years of Bauer: Proud of What We Have Achieved Together

225 years of Bauer: Proud of what we have achieved together Bauer foundation piles support Karl Bauer (1894 – 1956), who required new well and water Dr. Karlheinz Bauer – were car- the glass dome of the Reichstag took over the business after World pipelines. The work was diffi cult; ried out under the management of building in Berlin, Germany; the War I. An important step was the the biggest and most important Karl Bauer. 828-meter-tall Burj Khalifa in construction of the central water tool was the tripod. With Dr. Dubai stands on Bauer founda- supply system for Schrobenhau- Karlheinz Bauer, born in 1928, In the 1950s, Bauer turned more tion piles – Bauer has infl uenced sen in 1928. Eventually, the water the next generation of the family and more towards specialist specialist foundation engineering supply and well drilling business entered the business during this foundation engineering. A major since the mid 20th century. The expanded all across Bavaria. reconstruction phase. He was al- development was the invention equipment segment was also World War II badly affected the ready well established in the busi- of the grout injection anchor in growing, and soon new solutions company, as an increasing num- ness when his father, Dipl.-Ing. 1958. The company was contract- were being found for numerous ber of employees were drafted Karl Bauer, died unexpectedly ed to construct a large, exposed problems in the construction into the army. in 1956. The fi rst projects in the excavation pit with anchored pile segment. What once started in a fi eld of foundation engineering walls for Bavarian Broadcasting small town in Upper Bavaria has Just a few months after the war – subsequently termed ‘special- Corporation center in Munich. -

Paving the Road to Recovery As Global Construction Rebounds, Contractors Eye Infrastructure Spending As a Chance to Grow Revenue

Overview p. 48 // International Market Analysis p. 48 // International Region Analysis p. 49 // 2020 Revenue Breakdown p. 49 2020 New Contracts p. 49 // Domestic Staff Hiring p. 49 // International Staff Hiring p. 49 // Top 10 by Region p. 50 Top 10 by Market p. 51 // Top 20 Non-U.S. International Construction/Program Managers p. 52 // Top 20 Non-U.S. Global Construction/Program Managers p. 52 // Profit-Lossp. 53 // Total Backlog p. 53 // Past Decade’s International Contractor Revenue p. 53 // How Contractors Shared the 2020 Market p. 54 // How To Read the Tables p. 55 // Hochtief's Highway Expansion p. 55 // Top 250 International Contractors List p. 57 // International Contractors Index p. 62 // Top 250 Global Contractors List p. 63 // Global Contractors Index p. 68 NUMBER 170 NUMBER TUNNEL VISION ICM SpA is contractor for the A26 Linzer Autobahn project in Austria, which includes construction of junction tunnels and a cable-stayed bridge. PHOTO COURTESY OF ICM SPA PHOTO COURTESY International Contractors Paving the Road to Recovery As global construction rebounds, contractors eye infrastructure spending as a chance to grow revenue. By Emell Adolphus, Peter Reina and Jonathan Keller enr.com August 16/23, 2021 ENR 47 0823_Top250_Intro.indd 47 8/17/21 6:34 PM nternational contractors on the long road to rebounding from the COVID-19 pandemic might find a shortcut to recovery in infrastructure projects, as countries ramp up spending to help build economies back to normal. While the global construction market is red hot for some firms, it is Istone cold for others as contractors deal with unpredictable project risks while readying for new growth opportunities. -

For Employees and Friends of the Bauer Group Companies

BAUER REVIEW FOR EMPLOYEES AND FRIENDS OF THE BAUER GROUP COMPANIES 2009 39 Contents Status report 3 Bauer on the American continent 4 Official opening of BAUER-Strasse 1 18 Building in Germany 22 In-house exhibition 2009 30 Equipment in customer projects 32 Deep-level drilling rig 33 Employees from far and wide 34 Bauer projects worldwide 36 News in brief 43 In the late summer of 2009 work began on the tunnel beneath Munich’s Central Ring Road (Mittlerer Ring) in the south-west of the city. Bauer is constructing piled walls by the top-down method as well as installing other retaining structures. 3 Status report s it entered 2009, the BAUER Group was emerging from a segment is facing the toughest conditions. Our customers are re- record previous year, yet facing up to the challenges posed by sponding to the crisis like virtually all others. The first thing they did Athe most severe economic crisis of the post-war era. As always was to drastically cut their capital investment. This has led to a dra- at this late stage of the year, we are taking the opportunity to review matic decline in machinery orders. The collapse is most severe in rela- the progress we have made thus far. tion to the smaller equipment forming part of the standard inventory Business in 2008 was outstanding; it was a year of superlatives all- of all specialist foundation engineering companies. By contrast, there round. We increased our total Group revenues by 26.4 percent to are some good prospects for sales of large-size machinery purchased EUR 1,527 million and after-tax profit improved by 44.5 percent to for specific projects. -

Standard Presentation –

Investor Relations Group Presentation Q1 2021 BAUER AG May 12, 2021 1 Overview ▪ BAUER Group ▪ Highlights Q1 2021 2 BAUER Group Three closely interlinked segments – a business model with a future Mission The BAUER Group is a leading provider of services, equipment & products dealing with ground and groundwater. Construction Equipment Resources Global provider for One of the technical leading manufacturer Products and services for the water, specialist foundation engineering services of specialist foundation equipment mining and environmental industries ▪ For private and public clients ▪ Equipment for all specialist foundation ▪ Drilling services and well construction, ▪ Broad portfolio of specialist foundation engineering methods environmental technology, constructed techniques and many years of know-how ▪ Innovative and digital assistance systems wetlands, mining and remediation ▪ Focus on complex projects in the world ▪ Specialized machines for mining, deep ▪ Waste disposal and brownfield services drilling and offshore drilling often in combination with specialist ▪ Own equipment in use foundation engineering 3 Highlights Q1 2021 – Further increase of order backlog Total Group revenues EBIT* Earnings after tax Order intake Order backlog EUR 356.6 million EUR 1.8 million EUR -5.1 million EUR 516.1 million EUR 1,322 million (-8.6%) (EUR 8.5 million) (EUR -5.0 million) (+13.4%) (+21.0%) Significant financial developments Significant operational developments ▪ Decline in total Group revenues – Q1 2020 without nearly no ▪ Good start on construction sites worldwide COVID 19 pandemic impact ▪ Improved demand situation in the Equipment segment; no ▪ EBIT decreased because of the lower revenue volume significant improvement expected before H2 2021 ▪ Earnings after taxes stable – improvement of financial result ▪ Resources with good start into 2021 ▪ Order intake show a further increase ▪ Order backlog at new record-level * Previous year adjusted; see p. -

Specialist Foundation Projects on All Continents

44 Contents Status report 5 Special task 6 Schwarzkopf Tunnel 16 Peter Teschemacher 18 Standard projects 20 Towers on Bauer piles 24 New machinery innovation 28 Equipment in customer use 30 Construction engineering all over the world 32 The Resources Group 40 Health, Safety & Environment 43 In-house news he tallest buildings in the world are also deliberated – thoughts that were standing on Bauer piles. Burj Khalifa presented by Thomas Bauer, Chairman T in Dubai holds the current record, of the Management Board, in a speech. but Bauer Spezialtiefbau has already completed the foundation of the King- dom Tower in Jeddah, Saudi-Arabia, the second-tallest tower, and structural en- gineering work is underway. This issue contains a whole section just on this foundation and the large towers. But not all things reach for the sky. Bauer engineers have an ideal and effi cient so- lution for every problems, no matter how small, in specialist foundation engineer- ing. These “standard projects” are also presented in a separate section. The headline feature of this issue show- cases the varied tasks that have come our way in recent years in special foun- dation engineering and in all things re- lated to Bauer techniques. It describes projects in extreme situations and unu- sual technical challenges such as a drill- ing rig for research work on the sea bed. A BG 25 was used for 219 piles supporting the walls of a 44 m Technical innovations play an important long connecting tunnel between the underground car park and and integral part in the life of Bauer en- Souq Waqif in Doha, Qatar. -

Annual Report 2019 the BAUER Group Is a Leading Provider of Services, Equipment and Products Related to Ground and Groundwater

Annual Report 2019 The BAUER Group is a leading provider of services, equipment and products related to ground and groundwater. With over 110 subsidiaries, Bauer operates a worldwide network on all continents. The operations of the Group are divided into three future-oriented segments with high synergy potential: Construction, Equipment and Resources. The Construction segment offers new and innovative specialist foundation engineering services alongside the established ones, and carries out foundation and excavation work, cut-off walls and ground improvements worldwide. Bauer is a world market leader in the Equipment segment and provides a full range of equipment for specialist foundation engineering as well as for the exploration, mining and extraction of natural resources. In the Resources segment, Bauer focuses on highly innovative products and services in the areas of water, environment and natural resources. Bauer profits greatly from the collaboration between its three separate segments, enabling the Group to position itself as an innovative, highly specialized provider of products and services for demanding projects in specialist foundation enginee- ring and related markets. Bauer therefore offers suitable solutions to the greatest problems in the world, such as urbanization, the growing infrastructure needs, the environment and water, oil and gas. The BAUER Group was founded in 1790 and is based in Schrobenhausen, Bavaria. In 2019, it employed some 12,000 people in around 70 countries and achieved total Group revenues of EUR 1.6 -

Annual Report 2014 the BAUER Group Is an International Construction and Machinery Manufacturing Concern Based in Schrobenhausen, Bavaria

Annual Report 2014 The BAUER Group is an international construction and machinery manufacturing concern based in Schrobenhausen, Bavaria. The stock market-listed holding company BAUER Aktiengesellschaft is the parent of more than 110 subsidiary businesses across its Construction, Equipment and Resources segments. Bauer is a leader in the execution of complex excavation pits, foundation and vertical seals, as well as in the development and manufacture of related machinery for this dynamic market. The Group also deploys its expertise in the exploration, mining and safeguarding of valuable natural resources. In 2014 the companies of the BAUER Group employed some 10,400 people in around 70 countries and achieved total Group revenues of EUR 1.56 billion. Passion for progress – The origins of Bauer date back as far as 1790, and still today the company's success is founded on highly flexible application of the specialist know-how it has built up over those many years. As an innovator and technology leader, Bauer has played a major role in the advancement of the international specialist foundation engineering industry and related busniess fields. Indeed, today Bauer is also the world market leader in the manufacture of the relevant machinery. It is with just such innovative strength and a keen focus on the challenges of the future that the Group is also developing its recently established Resources segment. The Group at a glance GROUP KEY FIGURES 2011 – 2014 IFRS in EUR million 2011 2012 2013 ** 2014 Change 2013/2014 Total Group revenues 1,371.8 -

Standard Presentation –

BAUER AG Group Presentation 6M/Q2 2020 Investor Relations August 13, 2020 Highlights 6M 2020 Total Group revenues Sales revenues EBITDA EBIT Earnings after tax EUR 725 million EUR 649 million EUR 58.0 million EUR 6.5 million EUR -16.0 million (-12.8%) (-13.0%) (-29.7%) (-81.5%) (6M 20: EUR -0.4 million) Order intake Order backlog Total assets Net debt Equity ratio EUR 973 million EUR 1,276 million EUR 1,656 million EUR 613 million 22.2% (+16.2%) (+25.1%) (-4.5%) (-5.3%) (6M 20: 24.3%) . Total Group revenues decreased significantly by 12.8%, from EUR 831.6 million to EUR 725.0 million. EBIT fell significantly from EUR 35.3 million in the previous year to EUR 6.5 million. Earnings after tax amounted to EUR -16.0 million (previous year: EUR -0.4 million). In addition to the losses in the Construction and Equipment segments, interest rate hedging transactions had a significant negative impact. The Construction segment and, in particular, the Equipment segment fell significantly short of the original expectations, which can primarily be attributed to the effects of the coronavirus pandemic. The Resources segment remained nearly unaffected and demonstrates a better development than the previous year in operational terms. The order backlog increased very significantly by 25.1% to EUR 1,275.7. This was primarily attributable to Construction, where very large order volumes were commissioned, including in Europe. The impact of the pandemic on further construction activities around the world and on customer demand for equipment, and thus ultimately on the revenue and earnings development, still cannot be predicted reliably. -

Group Presentation 6M/Q2 2021

Investor Relations Group Presentation 6M/Q2 2021 BAUER AG August 12, 2021 1 Overview ▪ BAUER Group ▪ Highlights 6M/Q2 2021 2 BAUER Group Three closely interlinked segments – a business model with a future Mission The BAUER Group is a leading provider of services, equipment & products dealing with ground and groundwater Construction Equipment Resources Global provider for One of the technical leading manufacturer Products and services for the water, specialist foundation engineering services of specialist foundation equipment mining and environmental industries ▪ For private and public clients ▪ Equipment for all specialist foundation ▪ Drilling services and well construction, ▪ Broad portfolio of specialist foundation engineering methods environmental technology, constructed techniques and many years of know-how ▪ Innovative and digital assistance systems wetlands, mining and remediation ▪ Focus on complex projects in the world ▪ Specialized machines for mining, deep ▪ Waste disposal and brownfield services drilling and offshore drilling often in combination with specialist ▪ Own equipment in use foundation engineering 3 Highlights 6M 2021 – Increase of revenues and earnings in still difficult environment Total Group revenues EBIT* Earnings after tax Order backlog Equity EUR 767.4 million EUR 15.3 million EUR -5.6 million EUR 1,279 million EUR 450.4 million (+5.8%) (EUR 11.0 million) (EUR -16.0 million) (+0.3%) (+22.8%) Significant financial developments Significant operational developments ▪ Increase of total Group revenues in a still difficult market ▪ Construction markets are still significantly influenced by COVID-19 environment pandemic, especially in the Far East ▪ EBIT increased in all business segments ▪ Improved demand situation in the Equipment segment, but no significant improvement in key figures. -

Annual Report 2020 the BAUER Group Is a Leading Provider of Services, Equipment and Products Related to Ground and Groundwater

Annual Report 2020 The BAUER Group is a leading provider of services, equipment and products related to ground and groundwater. With over 110 subsidiaries, Bauer operates a worldwide network on all continents. The operations of the Group are divided into three future-oriented segments with high synergy potential: Construction, Equipment and Resources. The Construction segment offers new and innovative specialist foundation engineering services alongside the established ones, and carries out foundation and excavation work, cut-off walls and ground improvements worldwide. Bauer is a world market leader in the Equipment segment and provides a full range of equipment for specialist foundation engineering as well as for the exploration, mining and extraction of natural resources. In the Resources segment, Bauer focuses on innovative pro- ducts and services in the fields of drilling services and water wells, environmental services, constructed wetlands, mining and remediation. Bauer profits greatly from the collaboration between its three separate segments, enabling the Group to position itself as an innovative, highly specialized provider of products and services for demanding projects in specialist foundation enginee- ring and related markets. Bauer therefore offers suitable solutions to the greatest problems in the world, such as urbanization, the growing infrastructure needs, the environment and water, oil and gas. The BAUER Group was founded in 1790 and is based in Schrobenhausen, Bavaria. In 2020, it employed some 11,000 people in around