HASH# Cannabis Sector.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

11-05-18 DRAFT 4:41 PM UTAH MEDICAL CANNABIS ACT 1 2018 THIRD SPECIAL SESSION 2 STATE of UTAH 3 4 LONG TITLE 5 General Descript

11-05-18 DRAFT 4:41 PM 1 UTAH MEDICAL CANNABIS ACT 2 2018 THIRD SPECIAL SESSION 3 STATE OF UTAH 4 5 LONG TITLE 6 General Description: 7 This bill provides for the cultivation, processing, medical recommendation, and patient use of 8 medical cannabis. 9 Highlighted Provisions: 10 This bill: 11 ▸ defines terms; 12 ▸ provides for licensing and regulation of a cannabis cultivation facility, a 13 cannabis processing facility, an independent cannabis testing laboratory, and a 14 medical cannabis pharmacy; 15 ▸ provides for security and tracking of medical cannabis and a medical cannabis 16 product from cultivation to consumptionuse to ensure safety and chemical content; 17 ▸ requires certain labeling and childproof packaging of medical cannabis and a 18 medical cannabis product; 19 ▸ requires the Department of Agriculture and Food, the Department of Health, the 20 Department of Public Safety, and the Department of Technology Services to create 21 an electronic verification system to facilitate recommendation, dispensing, and 22 record-keeping for medical cannabis transactions; 23 ▸ allows an individual with a qualifying condition to obtain a medical cannabis 24 patient card on the recommendation of a certain medical professional to gain access 25 to medical cannabis; 26 ▸ allows a patient to designate a caregiver to assist with accessing medical 27 cannabis; 28 ▸ provides thatfor a parent or legal guardian isto obtain a medical cannabis 29 guardian card for an eligible minor patient and for the designated caregiver for a 30 minorminor patient -

Personal Use Cannabis Rules Special Adopted New Rules: N.J.A.C

NEW JERSEY CANNABIS REGULATORY COMMISSION Personal Use Cannabis Rules Special Adopted New Rules: N.J.A.C. 17:30 Adopted: August 19, 2021 by New Jersey Cannabis Regulatory Commission, Dianna Houenou, Chair. Filed: August 19, 2021 Authority: N.J.S.A. 24:6I-31 et seq. Effective Date: August 19, 2021 Expiration Date: August 19, 2022 This rule may be viewed or downloaded from the Commission’s website at nj.gov/cannabis. These rules are adopted pursuant to N.J.S.A. 24:6I-34(d)1a of the New Jersey Cannabis Regulatory, Enforcement Assistance, and Marketplace Modernization Act, N.J.S.A. 24:6I- 31 et seq., and became effective upon acceptance for filing by the Office of Administrative Law. The specially adopted new rules shall be effective for a period not to exceed one year from the date of filing of the new rules, that is, until August 19, 2022. The Commission has provided this special adoption to the Attorney General, State Treasurer, Commissioner of Health, and Commissioner of Banking and Insurance for a consultation period, after which the Commission anticipates filing a proposal to readopt these rules with amendments reflecting the results of that consultation. In accordance with N.J.S.A. 24:6I-34(d)1b the rules, as readopted, will become effective upon acceptance for filing by the Office of Administrative Law if filed on or before the expiration date of the rules published herein. The adopted amendments will be effective upon publication in the New Jersey Register. Federal Standards Analysis The Cannabis Regulatory, Enforcement Assistance, and Marketplace Modernization Act obliges the Cannabis Regulatory Commission to promulgate rules necessary or proper to enable it to carry out the Commission’s duties, functions, and powers with respect to overseeing the development, regulation, and enforcement of activities associated with the personal use of cannabis pursuant to P.L.2021, c.16. -

Effective 12/3/2018 Superseded 3/26/2019 4-41A-701 Cannabis and Cannabis Product Testing. (1) a Medical Cannabis Pharmacy and Th

Utah Code Effective 12/3/2018 Superseded 3/26/2019 4-41a-701 Cannabis and cannabis product testing. (1) A medical cannabis pharmacy and the state central fill medical cannabis pharmacy may not offer any cannabis or cannabis product for sale unless an independent cannabis testing laboratory has tested a representative sample of the cannabis or cannabis product to determine: (a) (i) the amount of total composite tetrahydrocannabinol and cannabidiol in the cannabis or cannabis product; and (ii) the amount of any other cannabinoid in the cannabis or cannabis product that the label claims the cannabis or cannabis product contains; (b) that the presence of contaminants, including mold, fungus, pesticides, microbial contaminants, heavy metals, or foreign material, does not exceed an amount that is safe for human consumption; and (c) for a cannabis product that is manufactured using a process that involves extraction using hydrocarbons, that the cannabis product does not contain a level of a residual solvent that is not safe for human consumption. (2) By rule, in accordance with Title 63G, Chapter 3, Utah Administrative Rulemaking Act, the department: (a) may determine the amount of any substance described in Subsections (1)(b) and (c) that is safe for human consumption; and (b) shall establish protocols for a recall of cannabis or a cannabis product by a cannabis production establishment. (3) The department may require testing for a toxin if: (a) the department receives information indicating the potential presence of a toxin; or (b) the department's inspector has reason to believe a toxin may be present based on the inspection of a facility. -

FDA Office of Women's Health US Food and Drug Administration

FDA OFFICE OF WOMEN’S HEALTH SCIENTIFIC CONFERENCE CBD & Other Cannabinoids Sex and Gender Differences in Use and Responses Thursday, November 19, 2020 | 9:00 AM–4:00 PM EST Virtual Meeting CBD and Other Cannabinoids: Sex and Gender Differences in Use and Responses | 1 !/"'""'', 11 U.S. FOOD & DRUG •J ADMINISTRATION Dear Colleagues, On behalf of the U.S. Food and Drug Administration's (FDA) Office of Women's Health (OWH), I am pleased to welcome you to today's conference, "CBD and Other Cannabinoids: Sex and Gender Differences in Use and Responses." The mission of FDA is to protect and promote public health. A top priority for OWH is to identify and monitor emerging areas of interest and potential concern for the health of women. Cannabidiol (CBD) products are appearing everywhere - from medical cannabis dispensaries, to pharmacies, to gas stations. Many of these products are illegally marketed and purport to target a myriad of health concerns, including conditions more commonly experienced by women than men, such as chronic pain, sleep disturbances, anxiety and depression. Given that little is known about how and if many cannabis derived products work, how and why women are using them, and their potential associated risks, there is a mounting need to consolidate and communicate what we know about these products and to identify knowledge gaps. Further, the use of these products during pregnancy and lactation raises additional questions and concerns. The purpose of today's meeting is to highlight the needed and existing research to address the many "who", "what", and "why" questions surrounding products containing CBD and other cannabinoids. -

Overview of the WSLCB Rule Development Process Sara Cooley Broschart

Overview of the WSLCB Rule Development Process Kathy Hoffman, MPA, MALC Policy and Rules Manager Washington State Liquor and Cannabis Board Prevention Summit November 4, 2020 Presentation Outline Today’s Presentation • WSLCB rule development process, including: • What does the WSLCB do? • Rule development process • From concept to completion • How to get involved • Statutory and regulatory authority • The most effective ways to provide input and comment • Current Rule Projects and Future Rule Projects Presentation Outline Who is WSLCB and what does WSLCB do? • Three-person Board • License liquor, cannabis, vapor and tobacco product production, processing and product sale. Presentation Outline Rule Development Process Basic Rule Making Process The standard rule making process is described in chapter 34.05 RCW, the Administrative Procedures Act, and divided into three stages: • Stage 1: Pre-proposal Statement of Inquiry (CR-101) – RCW 34.05.310 • Stage 2: Proposed Rule Making (CR-102) - RCW 34.05.320 • State 3: Rule-making Order (CR-103) - RCW 34.05.360 Each stage consists of specific tasks and processes. Start CR-101 Pre-proposal . Statement of Inquiry CR-102 Proposal Public Hearing: Oral Testimony Written Testimony Stakeholder Engagement: Listen and Learn Forums Draft Conceptual Rule Workshops DeliBerative Dialogue Sessions CR-103 Final Agency Responds Adoption to Comments Rule development, drafting, Finish and analysis Standard Rule Making – Stage 1 Pre-Proposal Statement of Inquiry (CR-101) – RCW 34.05.310 Purpose: Describes the issue(s) being considered for rule development • The CR-101 identifies the purpose and scope of rulemaking. • The scope of the rules created through this process is controlled by statutory authority and must be compatible with existing requirements. -

What Is in the Law Public Health and Safety

What is in the Law Public Health and Safety Overview On March 31, 2021, New York State legalized adult-use cannabis (also known as marijuana, or recreational marijuana) by passing the Marijuana Regulation & Taxation Act (MRTA). The legislation creates a new Office of Cannabis Management (OCM) governed by a Cannabis Control Board to oversee and implement the law (collectively referred to as the “OCM”). The OCM will issue licenses and develop regulations outlining how and when business can participate in the new industry. The OCM will also oversee the State’s existing Medical Marijuana and Cannabinoid Hemp Programs. The information below is a collection of key provisions from the MRTA that are intended to help protect the public health and safety of New Yorkers. For additional information, or to contact the Office of Cannabis Management (OCM), please visit our website at: www.cannabis.ny.gov or e-mail us at: [email protected]. Benefits of Regulation One of the main benefits of legalizing adult-use cannabis is that cannabis products will be regulated under a framework that protects consumer health and safety, similar to many other products humans consume. The OCM will be implementing quality assurance regulations, governing the manufacturing, packaging, labeling, advertising, and testing of cannabis products. The OCM will also be conducting a robust public health and education campaign, to monitor and track the impact of adult-use cannabis legalization on public health and safety indicators and to implement regulations that protect vulnerable populations and prohibit the marketing and advertising of cannabis to youth. In addition, 20% of all adult-use cannabis tax revenue is dedicated to public health education and substance-use prevention programs. -

Understanding Cannabinoid Analytics

A Primer on the Process of Cannabinoids Derived Through Biosynthesis Understanding Cannabinoid Analytics New York, Toronto | LAVVAN.com | 1-888-528-8261 The United States Food and Drug Administration currently prohibits the addition of CBD to food and dietary supplement product This is a confidential document. Do not distribute. Table of Contents Introduction ....................................................................................................................... 3 The Current State of Cannabinoid Product Testing ........................................................ 3 Analytical Targets in Cannabis Products ......................................................................... 5 Cannabinoids ............................................................................................................................. 5 Water Content ............................................................................................................................ 6 Terpenes .................................................................................................................................... 6 Microbial Contamination ............................................................................................................ 6 Endogenous Contaminants: Residual Solvents, Heavy Metals, and Pesticides ...................... 7 Defining the Analytical Testing Process .......................................................................... 7 Sampling of the Product Material.............................................................................................. -

A Baseline Review and Assessment of the Massachusetts Adult-Use Cannabis Industry: Market Data and Industry Participation

A Baseline Review and Assessment of the Massachusetts Adult-Use Cannabis Industry: Market Data and Industry Participation February 2020 Massachusetts Cannabis Control Commission: Steven J. Hoffman, Chairman Kay Doyle, Commissioner Jennifer Flanagan, Commissioner Britte McBride, Commissioner Shaleen Title, Commissioner Shawn Collins, Executive Director Prepared by the Massachusetts Cannabis Control Commission Research and Information Technology Departments: Samantha M. Doonan, BA, Research Analyst David McKenna, PhD, Chief Technology Officer Julie K. Johnson, PhD, Director of Research Acknowledgements External Collaborators Alexandra F. Kritikos, MA, Brandeis University Cannabis Control Commission Communications Cedric Sinclair, Director of Communications Maryalice Gill, Press Secretary Kirsten Swenson, Communications Specialist Management Alisa Stack, Chief Operating Officer Erika Scibelli, Chief of Staff Legal Christine Baily, General Counsel Allie DeAngelis, Associate General Counsel Enforcement and Licensing Yaw Gyebi, Chief of Enforcement Paul Payer, Enforcement Counsel Kyle Potvin, Director of Licensing Patrick Beyea, Director of Investigations Derek Chamberlin, Licensing Analyst Anne DiMare, Licensing Specialist Government Affairs David Lakeman, Director of Government Affairs 2 Suggested bibliographic reference format: Doonan SM., McKenna, D., Johnson JK., (2020, February). A Baseline Review and Assessment of the Massachusetts Adult-Use Cannabis Industry— A Report to the Massachusetts Legislature. Boston, MA: Massachusetts Cannabis -

CV Sciences and Alkemist Labs Form Partnership to Support the National Institute of Standards and Technology's Cannabis Qualit

April 13, 2021 CV Sciences and Alkemist Labs Form Partnership to Support the National Institute of Standards and Technology’s Cannabis Quality Assurance Program SAN DIEGO, April 13, 2021 (GLOBE NEWSWIRE) -- CV Sciences, Inc. (OTCQB:CVSI) (the “Company”, “CV Sciences”, “our”, “us” or “we”), a preeminent leader in hemp derived cannabidiol (CBD) products, today announced an ongoing partnership with Alkemist Labs, an established leader in botanical plant testing, to collaborate with the National Institute of Standards and Technology (“NIST”) on efforts to help cannabis testing labs demonstrate and improve measurement capabilities and comparability. The tools developed by this NIST cannabis program will support measurements establishing legal, commerce, and safety claims through the development of fit-for-purpose analytical methodologies, production of Reference Materials, and implementation of NIST’s Cannabis Quality Assurance Program (“CannaQAP”). As part of this collaboration, CV Sciences will prepare and provide hemp oil samples that NIST will distribute to laboratories that participate in CannaQAP. In addition, Alkemist Labs will provide initial measurements of cannabinoid levels in those samples. Currently, marijuana and THC remain on the controlled substances list, although medical marijuana is legal in 33 states and recreational marijuana is legal in 11 states as well as the District of Columbia. The 2018 Farm Bill defined hemp as cannabis containing not more than 0.3% THC and removed hemp from the controlled substances list. These legal changes have required laboratories throughout the United States to implement quantitative analytical methods to distinguish cannabis raw material and finished products as marijuana or hemp. “As one of the first accredited cannabis testing labs in California, Alkemist Labs has a long history as a strong advocate for rigorous laboratory standards for cannabis products,” said Alkemist Labs CEO Elan Sudberg. -

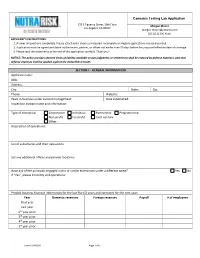

Cannabis Testing Lab Application SECTION I

Cannabis Testing Lab Application 725 S Figueroa Street, 19th Floor Morgan Moore Los Angeles, CA 90017 [email protected] (D) (213) 236-4566 APPLICANT’S INSTRUCTIONS: 1. Answer all questions completely. Please attach extra sheets as required. Incomplete or illegible applications may be discarded. 2. Application must be signed and dated by the owner, partner, or officer not earlier than 90 days before the proposed effective date of coverage. 3. Please read the statements at the end of this application carefully. Thank you! NOTICE: The policy provides that the limits of liability available to pay judgments or settlements shall be reduced by defense expenses, and that defense expenses shall be applied against the deductible amount. SECTION I – GENERAL INFORMATION Applicant name: DBA: Address: City: State: Zip: Phone: Website: Years in business under current management: Date established: Inspection contact name and information: Type of enterprise: Corporation Individual Partnership Proprietorship Non‐profit For profit Joint venture Other: Description of operations: List of subsidiaries and their operations: List any additional offices and provide locations: Have any of the principals engaged in this or similar enterprises under a different name? Yes No If “Yes”, please list entity and operations: Provide business financial information for the last five (5) years and estimates for the next year: Year Domestic revenues Foreign revenues Payroll # of employees Next year Last year 2nd year prior 3rd year prior 4th year prior 5th year prior Form JRAP0200 Page 1 of 5 SECTION II – QUESTIONS 1. Description of products tested (check all that apply): Medical Marijuana Recreational Marijuana Hemp/CBD Non‐cannabis Products. -

REGULAR MEETING Monday, March 27, 2017, at 7:00 Pm 7217 - 4Th Street, City Hall Council Chambers

THE CORPORATION OF THE CITY OF GRAND FORKS AGENDA – REGULAR MEETING Monday, March 27, 2017, at 7:00 pm 7217 - 4th Street, City Hall Council Chambers ITEM SUBJECT MATTER RECOMMENDATION 1. CALL TO ORDER 2. ADOPTION OF AGENDA a) Adopt agenda March 27, 2017, Regular THAT Council adopts the Meeting agenda March 27, 2017, Regular Meeting agenda as presented. 3. MINUTES a) Adopt minutes March 9, 2017, Special THAT Council adopts the March-9-2017-Special-to-go-In- Meeting to go In-Camera March 9, 2017, Special Camera-Meeting-Minutes-Not Yet minutes Meeting to go In-Camera Adopted minutes as presented. b) Adopt minutes March 13, 2017, Committee THAT Council adopts the March-13-2017-Committee-of-the- of the Whole Meeting minutes March 13, 2017, Committee Whole-Meeting-Minutes-Not Yet of the Whole Meeting minutes Adopted as presented. c) Adopt minutes March 13, 2017, Regular THAT Council adopts the March-13-2017-Regular-Meeting- Meeting minutes March 13, 2017, Regular Minutes-Not Yet Adopted Meeting minutes as presented. 4. REGISTERED PETITIONS AND DELEGATIONS 5. UNFINISHED BUSINESS 6. REPORTS, QUESTIONS AND INQUIRIES FROM MEMBERS OF COUNCIL a) Corporate Officer's Report Written reports of Council THAT all written reports of RFD - Proc. Bylaw-CAO - Rpts., Council submitted to the Questions, & Inquiries from Council March 27, 2017, Regular Councillor Thompson's Report Meeting be received. Councillor Tripp's Report Councillor Butler's Report 7. REPORT FROM COUNCIL'S REPRESENTATIVE TO THE REGIONAL DISTRICT OF KOOTENAY BOUNDARY Page 1 of 133 a) Corporate Officer's Report Verbal report from Council's THAT Mayor Konrad's report RFD - Proc. -

Annual Report 2020

ANNUAL REPORT 2020 ANNUAL ANNUAL REPORT REPORT 2020 2020 CONTENTS FINANCIAL HIGHLIGHTS Financial Operating + 1 Highlights 14 Financial Review Financial Financial 1 Highlights 30 Report 2019 Chairman’s Financial 4 Letter 30 Report 2020 Chairman’s Independent 4 Letter 77 Auditor’s Report Managing Independent 8 Director’s 85 Auditor’s Letter Report Managing Director’s Shareholders 6 Letter 81 Information Shareholders’ Revenue US independent pharmacies 90 Information up 519% from $5.7m to up 510% from 525 to Operating + Corporate 10 Financial Review 85 Directory Corporate $35.6m 3,200 93 Directory About Ecofibre NPAT Channel mix Ecofibre is a provider of hemp products in the United up 170% from $8.6m loss to Branded channel sales States and Australia. In the United States, the Ananda Health business is the #1 + $6.0m 84% provider of hemp-derived CBD for retail pharmacies. The Company produces nutraceutical products for human and pet consumption, as well as topical creams and salves. See www.anandahemp.com and www.anandaprofessional.com. The Company also supplies its leading Ananda Hemp CBD Fully diluted EPS Gross Margin products to Australians via the SAS B program. up 158% from 3.7 cps loss to for H2 FY2019 In Australia, the Company produces 100% Australian grown and processed hemp food products including protein 2.2 CPS 77% powders, de-hulled hemp seed and hemp oil. See + www.anandafood.com. The Company is also developing innovative hemp-based products in textiles and composite materials in the United Net Assets EBITDA margin States. See www.hempblack.com. up from $1.6m to for H2 FY2019 The Company owns or controls key parts of the value chain in each business, from breeding, growing and production to $ sales and marketing.