Private Equity & Venture Capital

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report

Building Long-term Wealth by Investing in Private Companies Annual Report and Accounts 12 Months to 31 January 2021 Our Purpose HarbourVest Global Private Equity (“HVPE” or the “Company”) exists to provide easy access to a diversified global portfolio of high-quality private companies by investing in HarbourVest-managed funds, through which we help support innovation and growth in a responsible manner, creating value for all our stakeholders. Investment Objective The Company’s investment objective is to generate superior shareholder returns through long-term capital appreciation by investing primarily in a diversified portfolio of private markets investments. Our Purpose in Detail Focus and Approach Investment Manager Investment into private companies requires Our Investment Manager, HarbourVest Partners,1 experience, skill, and expertise. Our focus is on is an experienced and trusted global private building a comprehensive global portfolio of the markets asset manager. HVPE, through its highest-quality investments, in a proactive yet investments in HarbourVest funds, helps to measured way, with the strength of our balance support innovation and growth in the global sheet underpinning everything we do. economy whilst seeking to promote improvement in environmental, social, Our multi-layered investment approach creates and governance (“ESG”) standards. diversification, helping to spread risk, and is fundamental to our aim of creating a portfolio that no individual investor can replicate. The Result Company Overview We connect the everyday investor with a broad HarbourVest Global Private Equity is a Guernsey base of private markets experts. The result is incorporated, London listed, FTSE 250 Investment a distinct single access point to HarbourVest Company with assets of $2.9 billion and a market Partners, and a prudently managed global private capitalisation of £1.5 billion as at 31 January 2021 companies portfolio designed to navigate (tickers: HVPE (£)/HVPD ($)). -

2014 10 October__Calabasas Capital Market Update & Industry

7/9/2015 2014_10_October__Calabasas Capital Market Update & Industry Spotlight.htm From: Calabasas Capital <[email protected]> on behalf of Calabasas Capital <[email protected]> Sent: Thursday, October 30, 2014 10:06 AM To: David Bonrouhi Subject: Calabasas Capital Market Update & Industry Spotlight Hi, just a reminder that you're receiving this email because you have expressed an interest in Calabasas Capital. Don't forget to add [email protected] to your address book so we'll be sure to land in your inbox! You may unsubscribe if you no longer wish to receive our emails. 3rd Quarter 2014 Market Update & Industry Spotlight June 2014 Dear David, We hope you find our latest market update insightful. We have included a spotlight on a few of the key industries we have been tracking closely, including Business Services, Nutritional Supplements, Restaurants & Retail and ECommerce and would you like to invite you to a great event next week. U.S. Middle Market M&A* file:///Users/qiuhuang1/Dropbox/Calabasas%20Capital/html/2014_10_October__Calabasas%20Capital%20Market%20Update%20&%20Industry%20Spotlight.htm 1/9 7/9/2015 2014_10_October__Calabasas Capital Market Update & Industry Spotlight.htm The first three quarters of 2014 delivered the highest middlemarket deal value for the period in five years. Dealmakers have been predicting that 2014 would be a great year for M&A, and, so far, they're right. The first nine months of the year yielded 1,721 completed middlemarket transactions, the secondhighest deal volume for the JanuarythroughSeptember period in five years. Total deal value was $230.3 billion, the highest for the period in five years * Sources: Mergers & Acquisitions. -

Structured Finance

Financial Institutions U.S.A. Investcorp Bank B.S.C. Full Rating Report Ratings Key Rating Drivers Investcorp Bank B.S.C. Strong Gulf Franchise: The ratings of Investcorp B.S.C. (Investcorp, or the company) reflect Long-Term IDR BB Short-Term IDR B the company’s strong client franchise in the Gulf, established track record in private equity (PE) Viability Rating bb and commercial real estate investment, strong capital levels and solid funding profile. Rating constraints include sizable balance sheet co-investments and potential earnings volatility and Investcorp S.A. Investcorp Capital Ltd. placement risks presented by the business model, which could pressure interest coverage. Long-Term IDR BB Short-Term IDR B Gulf Institutional Owners Positive: The Positive Rating Outlook reflects franchise and Senior Unsecured Debt BB earnings benefits that may accrue to Investcorp from the 20% strategic equity stake sale to Support Rating Floor NF Mubadala Development Co. (Mubadala) in March 2017, a sovereign wealth fund of Abu Dhabi. This follows a 9.99% equity stake sale to another Gulf-based institution in 2015. Fitch Ratings Rating Outlook Positive views these transactions favorably, as the relationships may give Investcorp expanded access to potential new investors as well as a more stable equity base. 3i Business Diversifies AUM: The cash-funded acquisition of 3i Debt Management (3iDM) in March 2017 added $10.8 billion in AUM and is expected to be accretive for Investcorp, adding Financial Data stable management fee income. However, the acquired co-investment assets and ongoing risk Investcorp Bank B.S.C. retention requirements do increase Investcorp’s balance sheet risk exposure. -

Dear Fellow Shareholders

Dear Fellow Shareholders: At Evercore, we aspire to be the most respected independent investment banking advi- sory firm globally. Our overarching objective is to help a growing base of clients achieve superior results through trusted independent and innovative advice, provided by excep- tional professionals who bring to our clients diverse perspectives and experiences. Our clients include multinational corporations, financial sponsors, institutional investors, sov- ereign wealth funds, and wealthy individuals and family offices. Achieving this objective requires that we steadily build our team by recruiting the best, from those beginning their professional careers to veterans with decades of experience. We are deliberate in selecting and developing the members of our team, seeking to attract individuals who share our Core Values: Client Focus, Integrity, Excellence, Respect, Investment in People and Partnership. Our values are the defining elements of our culture, telling our clients and current and future generations of partners and employees what they can expect from our firm. Realizing our aspiration also requires that we deliver attractive financial results over time. Strong financial results create the opportunity to invest and grow, enabling us to serve more clients and enhance the range of services we offer. The environment for our business was generally favorable in 2017, providing both good opportunities and a few challenges: • Advisory Services: Demand for strategic corporate and capital markets advisory services remains strong. The appeal of purely independent, unconflicted advice continues to grow and the opportunities and challenges facing our clients are broad, as economic conditions, globalization, technology and regulation drive strategic change. We believe that we are well positioned here. -

Sovereign Wealth Funds As Sustainability Instruments? Disclosure of Sustainability Criteria in Worldwide Comparison

sustainability Article Sovereign Wealth Funds as Sustainability Instruments? Disclosure of Sustainability Criteria in Worldwide Comparison Stefan Wurster * and Steffen Johannes Schlosser TUM School of Governance, Technical University Munich, 80333 Munich, Germany * Correspondence: [email protected] Abstract: Sovereign wealth funds (SWFs) are state-owned investment vehicles intended to pursue national objectives. Their nature as long-term investors combined with their political mandate could make SWFs an instrument suited to promote sustainability. As an essential precondition, it is important for SWFs to commit to sustainability criteria as part of an overarching strategy. In the article, we present the sustainability disclosure index (SDI), an original new dataset for a selection of over 50 SWFs to investigate whether SWFs disclose sustainability criteria covering environmental, social, economic, and governance aspects into their mandate. In addition to an empirical measurement of the disclosure rate, we conduct multiple regressions to analyze what factors help to explain the variance between SWFs. We see that a majority of SWFs disclose at least some of the sustainability criteria. However, until today, only a small minority address a broad selection as a possible basis for a comprehensive sustainability strategy. While a high-state capacity and a young population in a country as well as a commitment to the international Santiago Principles are positively associated with a higher disclosure rate, we find no evidence for strong effects of the economic development level, the resource abundance, and the degree of democratization of a country or of the specific size and structure of a fund. Identifying favorable conditions for a higher commitment of SWFs could Citation: Wurster, S.; Schlosser, S.J. -

Sovereign Wealth Funds": Regulatory Issues, Financial Stability and Prudential Supervision

EUROPEAN ECONOMY Economic Papers 378| April 2009 The so-called "Sovereign Wealth Funds": regulatory issues, financial stability and prudential supervision Simone Mezzacapo EUROPEAN COMMISSION Economic Papers are written by the Staff of the Directorate-General for Economic and Financial Affairs, or by experts working in association with them. The Papers are intended to increase awareness of the technical work being done by staff and to seek comments and suggestions for further analysis. The views expressed are the author’s alone and do not necessarily correspond to those of the European Commission. Comments and enquiries should be addressed to: European Commission Directorate-General for Economic and Financial Affairs Publications B-1049 Brussels Belgium E-mail: [email protected] This paper exists in English only and can be downloaded from the website http://ec.europa.eu/economy_finance/publications A great deal of additional information is available on the Internet. It can be accessed through the Europa server (http://europa.eu ) KC-AI-09-378-EN-N ISSN 1725-3187 ISBN 978-92-79-11189-1 DOI 10.2765/36156 © European Communities, 2009 THE SO-CALLED "SOVEREIGN WEALTH FUNDS": REGULATORY ISSUES, FINANCIAL STABILITY, AND PRUDENTIAL SUPERVISION By Simone Mezzacapo* University of Perugia Abstract This paper aims to contribute to the debate on the regulatory and economic issues raised by the recent gain in prominence of the so-called “Sovereign Wealth Funds” (SWFs), by first trying to better identify the actual legal and economic nature of such “special purpose” government investment vehicles. SWFs are generally deemed to bring significant benefits to global capital markets. -

Alternative Perspectives on Challenges and Opportunities of Financing Development

FINANCING FOR DEVELOPMENT Alternative Perspectives on Challenges and Opportunities of Financing Development ORGANISATION OF ISLAMIC COOPERATION STATISTICAL, ECONOMIC AND SOCIAL RESEARCH AND TRAINING CENTRE FOR ISLAMIC COUNTRIES Financing for Development Alternative Perspectives on Challenges and Opportunities of Financing Development Editors: Kenan Bağcı and Erhan Türbedar ORGANIZATION OF ISLAMIC COOPERATION THE STATISTICAL, ECONOMIC AND SOCIAL RESEARCH AND TRAINING CENTRE FOR ISLAMIC COUNTRIES (SESRIC) © May 2019 | Statistical, Economic and Social Research and Training Centre for Islamic Countries (SESRIC) Editors: Kenan Bağcı and Erhan Türbedar Kudüs Cad. No: 9, Diplomatik Site, 06450 Oran, Ankara –Turkey Telephone +90–312–468 6172 Internet www.sesric.org E-mail [email protected] The material presented in this publication is copyrighted. The authors give the permission to view, copy, download, and print the material presented provided that these materials are not going to be reused, on whatsoever condition, for commercial purposes. For permission to reproduce or reprint any part of this publication, please send a request with complete information to the Publication Department of SESRIC. All queries on rights and licenses should be addressed to the Publication Department, SESRIC, at the aforementioned address. The responsibility for the content, the views, interpretations and conditions expressed herein rests solely with the authors and can in no way be taken to reflect the views of the SESRIC or its Member States, partners, or of the OIC. The boundaries, colours and other information shown on any map in this work do not imply any judgment on the part of the SESRIC concerning the legal status of any territory or the endorsement of such boundaries. -

PEI 300 Guess Who’S Back on Top?

Issue 165 | May 2018 | privateequityinternational.com PEI 300 Guess who’s back on top? THE ORACLE SPEAKS David Rubenstein on the future of private capital SECONDARIES ROUNDTABLE Keeping LPs front and centre WHY PRIVATE EQUITY? The asset allocation special PLUS: the PEI Q1 Fundraising Report; IRRs vs money multiples; introducing the CEPRES model portfolio; Texas TRS goes Canadian; inside the PE retail blowouts; and much more… Equistone announced the successful final We are one of close of Fund VI at its €2.8bn hard cap in March 2018. Europe’s most Equistone has made three investments for Fund VI and will continue to source deals active mid-market and build value with management teams across our target markets. investors. www.equistonepe.com Evercore acted as the exclusive global placement agent for Equistone Partners Europe Fund VI. © EQUISTONE PARTNERS EUROPE LIMITED Authorised and regulated by The Financial Conduct Authority. PE International Ad May 2018.indd 1 18/04/2018 15:18 Riding high historically it’s been successful, but it needs to ISOBEL ISSN 1474–8800 | ISSUE 165 | MARKHAM work hard to avoid becoming a victim of that MAY 2018 EDITOR'S success. The signs are already there that this LETTER is starting to happen. Senior Editor, Private Equity Toby Mitchenall Tel: +44 207 566 5447 Sandra Robertson, chief investment officer [email protected] and chief executive of the UK’s £3 billion ($4.3 Americas Editor, Private Equity Marine Cole billion; €3.4 billion) Oxford University Endow- Tel: +1 212 633 1455 [email protected] ment -

Sovereign Wealth Funds 2019 Managing Continuity, Embracing Change

SOVEREIGN WEALTH FUNDS 2019 MANAGING CONTINUITY, EMBRACING CHANGE SOVEREIGN WEALTH FUNDS 2019 Editor: Javier Capapé, PhD Director, Sovereign Wealth Research, IE Center for the Governance of Change Adjunct Professor, IE University 6 SOVEREIGN WEALTH FUNDS 2019. PREFACE Index 11 Executive Summary. Sovereign Wealth Funds 2019 23 Managing Continuity...Embracing Change: Sovereign Wealth Fund Direct Investments in 2018-2019 37 Technology, Venture Capital and SWFs: The Role of the Government Forging Innovation and Change 55 SWFs in a Bad Year: Challenges, Reporting, and Responses to a Low Return Environment 65 The Sustainable Development Goals and the Market for Sustainable Sovereign Investments 83 SWFs In-Depth. Mubadala: The 360-degree Sovereign Wealth Fund 97 Annex 1. Sovereign Wealth Research Ranking 2019 103 Annex 2. Sovereign Wealth Funds in Spain PREFACE 8 SOVEREIGN WEALTH FUNDS 2019. PREFACE Preface In 2019, the growth of the world economy slowed by very little margin for stimulating the economy to 2.9%, the lowest annual rate recorded since the through the fiscal and monetary policy strategies. subprime crisis. This was a year in which the ele- In any case, the developed world is undergoing its ments of uncertainty that had previously threate- tenth consecutive year of expansion, and the risks ned the stability of the cycle began to have a more of relapsing into a recessive cycle appear to have serious effect on economic expansion. Among these been allayed in view of the fact that, in spite of re- elements, there are essentially two – both of a poli- cord low interest rates, inflation and debt remain at tical nature – that stand out from the rest. -

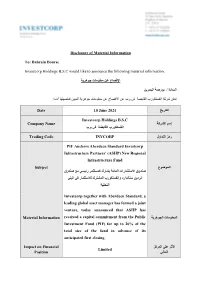

Disclosure of Material Information To: Bahrain Bourse Investcorp Holdings B.S.C Would Like to Announce the Following Material In

Disclosure of Material Information To: Bahrain Bourse Investcorp Holdings B.S.C would like to announce the following material information: اﻹفصاح عن معلومات جوهرية السادة / بورصة البحرين تعلن شركة إنفستكورب القابضة ش.م.ب عن اﻹفصاح عن معلومات جوهرية المبين تفاصيلها أدناه: التاريخ Date 10 June 2021 Investcorp Holdings B.S.C إسم الشركة Company Name إنفستكورب القابضة ش.م.ب رمز التداول Trading Code INVCORP PIF Anchors Aberdeen Standard Investcorp Infrastructure Partners’ (ASIIP) New Regional Infrastructure Fund الموضوع Subject صندوق اﻻستثمارات العامة يشارك كمستثمر رئيسي مع صندوق أبردين ستاندارد وإنفستكورب المشترك لﻻستثمار في البنى التحتية Investcorp together with Aberdeen Standard, a leading global asset manager has formed a joint venture, today announced that ASIIP has المعلومات الجوهرية Material Information received a capital commitment from the Public Investment Fund (PIF) for up to 20% of the total size of the fund in advance of its anticipated first closing. اﻷثر على المركز Impact on Financial Limited المالي Position إفصاحات سابقة ذات Previous relevant صلة )إن ُوجدت( (disclosures (if any ا ﻹسم Name Hazem Ben-Gacem المسمى الوظيفي Title Co-Chief Executive Officer of Investcorp التوقيع Signature ختم الشركة Company Seal PIF Anchors Aberdeen Standard Investcorp Infrastructure Partners’ (ASIIP) New Regional Infrastructure Fund Bahrain, 10th June 2021 – Investcorp together with Aberdeen Standard Investments, a leading global asset manager has formed a joint venture, today announced that ASIIP has received a capital commitment from the Public Investment Fund (PIF) for up to 20% of the total size of the fund in advance of its anticipated first closing. The fund has also received board approval from the Asian Infrastructure Investment Bank (AIIB) to commit US $90 million. -

Private Equity Performance Investment Horizon Performance Through March 31, 2006

LOS ANGELES CITY EMPLOYEES' RETIREMENT SYSTEM JUNE 30, 2006 ALTERNATIVE INVESTMENT REVIEW GSB BUILDING ONE BELMONT AVENUE, 9TH FLOOR BALA CYNWYD, PA 19004 TELEPHONE: (610) 934-2222 FAX: (610) 617-9855 WWW.HAMILTONLANE.COM TABLE OF CONTENTS SECTION 1: PORTFOLIO UPDATE SECTION 2: PORTFOLIO ASSESSMENT Performance Summary By Investment......................................................................................... 2-1-2-3 Performance Summary By Category............................................................................................ 2-4 Private Equity Benchmarks.......................................................................................................... 2-5-2-6 SECTION 3: PORTFOLIO ANALYTICS Commitments By Vintage Year.................................................................................................... 3-1 Portfolio Strategic Diversification as Measured by Reported Market Value................................. 3-2 Portfolio Strategic Diversification as Measured by Total Exposure.............................................. 3-3 Underlying Investment Diversification By Industry Classification................................................. 3-4 Cost and Fair Market Value (Exposed Market Value) of Portfolio Holdings................................. 3-5 Underlying Investment Diversification By Geographic Location................................................... 3-6 Public vs. Private Holdings.......................................................................................................... -

Environmental Services Insider Mergers & Acquisitions Overall M&A Activity

Environmental Services Services Insider Insider Volume II, No II July 2011 Highlights The BGL Environmental Services M&A Activity Insider is published by Inside: Brown Gibbons Lang & Company, a leading independent investment bank • Th e middle market is active, with M&A volume in the fi rst half BGL Spotlight: serving middle market companies and of 2011 up 33 percent over the same period a year ago. Q2 ’11 their owners throughout the U.S. and deal fl ow was up 34 percent over the prior quarter and 41 percent internationally. over the comparable period last year. Valuations remain strong in a Private Equity Roundtable Page 6 competitive deal market, with the median strategic buyer multiple Private equity fi rms discuss sector exceeding a healthy 8x EBITDA. Th e median fi nancial buyer opportunities, M&A, and the state of the Brown Gibbons multiple also remains healthy, equaling 7.4x EBITDA for middle fi nancing markets. market transaction values below $500 million (Page 2). Lang & Oil Collections & Re-Refi ning Page 18 • M&A activity in environmental services is following the same Company positive trend, with deal fl ow in the fi rst half up 31 percent from Market Update the year ago period. Sectors leading transaction activity are Solid The industry continues to undergo change as Cleveland Waste, up nearly two-fold and Metals Recycling & E-Waste, competition for the waste material heats up, 1111 Superior Avenue doubling over the same period. Q2 ’11 deal fl ow slowed from the and participants are encouraged by Valvoline’s Suite 900 prior quarter with Solid Waste and Metals Recycling & E-Waste entry into the market.