Canada Biomass-Bioenergy Report.(Pdf)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Bio-Oil Commercialization Plan

BIO-OIL COMMERCIALIZATION PLAN Bio-Oil Commercialization Plan Prepared for the NH Office of Energy and Planning by Cole Hill Associates 32 Dyke Road PO Box 523 Sugar Hill, NH 03585-5000 (603) 823-5109 July 2004 This material was prepared with financial support from the New Hampshire Governor’s Office of Energy and Community Services (ECS) and the New Hampshire Department of Resources and Economic Development (DRED). However, any opinions, findings, conclusions, or recommendations expressed are those of Cole Hill Associates and do not necessarily reflect the views of ECS (now the NH Office of Energy and Planning) or DRED and do not constitute an endorsement of products or services mentioned. Since this Plan was produced, Cole Hill Associates has relocated: Gerald W. Stewart Cole Hill Associates 4 St. Andrews Lane Bluffton, SC 29909 Telephone/Fax (843) 705-5924 Cell Phone (843) 368-5661 Cole Hill Associates Page 56 July 2004 BIO-OIL COMMERCIALIZATION PLAN Introduction I. Commercialization Plan Summary† A. There is a need for an expanded use of low-grade wood chips in the North Country of New Hampshire.1a,1b,2 B. One alternative is the conversion of wood chips into bio-oil, an environmentally friendly, renewable energy source. C. The objective of this study is to evaluate the economic viability of locating a bio-oil facility in New Hampshire as an alternative use of wood chips, and to inform interested parties as to the current state of bio-oil technology. Contractual requirements for developing this commercialization plan specifically forbid the selection of and /or bias towards any one producer or process. -

For Immediate Release Via the Canadian Custom Disclosure Network Magellan Aerospace Announces Report on Voting Results for Dire

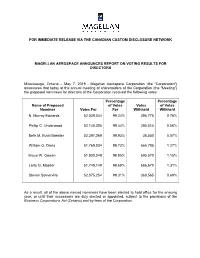

FOR IMMEDIATE RELEASE VIA THE CANADIAN CUSTOM DISCLOSURE NETWORK MAGELLAN AEROSPACE ANNOUNCES REPORT ON VOTING RESULTS FOR DIRECTORS Mississauga, Ontario – May 7, 2019 - Magellan Aerospace Corporation (the "Corporation") announces that today at the annual meeting of shareholders of the Corporation (the “Meeting”) the proposed nominees for directors of the Corporation received the following votes: Percentage Percentage Name of Proposed of Votes Votes of Votes Nominee Votes For For Withheld Withheld N. Murray Edwards 52,039,044 99.24% 396,775 0.76% Phillip C. Underwood 52,140,305 99.44% 295,514 0.56% Beth M. Budd Bandler 52,397,269 99.93% 38,550 0.07% William G. Davis 51,769,034 98.73% 666,785 1.27% Bruce W. Gowan 51,830,249 98.85% 605,570 1.15% Larry G. Moeller 51,749,149 98.69% 686,670 1.31% Steven Somerville 52,075,254 99.31% 360,565 0.69% As a result, all of the above named nominees have been elected to hold office for the ensuing year, or until their successors are duly elected or appointed, subject to the provisions of the Business Corporations Act (Ontario) and by-laws of the Corporation. About Magellan Aerospace: Magellan Aerospace is one of the world's most integrated aerospace industry suppliers. Magellan designs, engineers, and manufactures aeroengine and aerostructure assemblies and components for aerospace markets, advanced products for military and space markets, and complementary specialty products. Magellan is a public company whose shares trade on the Toronto Stock Exchange (TSX: MAL), with operating units throughout Canada, the United States, the United Kingdom, India, Northern Ireland, and Poland. -

Sustainable Growth Strategies in the Canadian Space Sector

Sustainable Growth Strategies in the Canadian Space Sector Sustainable Growth Strategies in the Canadian Space Sector Submitted by: Ian Christison Applied Project (APRJ-699) Word Count 20,187 Academic Coach: Conor VibertCarroll Submission Date: March 31, 2008 Assignment Number: 3 Sustainable Growth Strategies in the Canadian Space Sector 2 Table of Contents 1 Introduction....................................................................................................4 1.1 Defining the Problem ..............................................................................7 1.2 Problem Issues.......................................................................................7 1.3 Topic Definition.......................................................................................8 1.4 Project Definition Literature Search ........................................................8 1.5 Research Effective Reading Method and Literature Review...................8 1.6 Project Challenges and Focus Strategy..................................................9 2 Literature Review.........................................................................................10 2.1 Research Questions .............................................................................10 2.2 Research Boundaries ...........................................................................10 2.3 Alternative Courses of Action to be Evaluated......................................10 2.4 Research users ....................................................................................11 -

2021 First Quarter Report

QUARTERLY REPORT MARCH 31, 2021 This Management’s Discussion and Analysis (“MD&A”) of the financial condition and results of operations of Magellan Aerospace Corporation (“Magellan” or the “Corporation”) should be read in conjunction with the unaudited condensed consolidated interim financial statements and the notes thereto for the three month period ended March 31, 2021, and the audited annual consolidated financial statements for the year ended December 31, 2020 (available on SEDAR at www.sedar.com). Unless otherwise noted, all financial information has been prepared in accordance with Canadian Generally Accepted Accounting Principles (“GAAP”), specifically International Accounting Standard (“IAS”) 34, Interim Financial Reporting as issued by the International Accounting Standards Board (“IASB”), which is within the framework of International Financial Reporting Standards (“IFRS”). This MD&A provides a review of the significant developments that have impacted the Corporation’s performance during the three month period ended March 31, 2021 relative to the three month period ended March 31, 2020. The information contained in this report is as at May 4, 2021. All financial references are in Canadian dollars unless otherwise noted. The MD&A contains forward-looking information that represents the Corporation’s internal projections, expectations, estimates or beliefs concerning, among other things, future operating results and various components thereof or the Corporation’s future economic performance. These statements relate to future events or future performance. In particular and without limitation there are forward looking statements under the heading “Overview”, “Results of Operations”, “Liquidity and Capital Resources”, “Risk Factors”, “Future Changes in Accounting Policies” and “Outlook”. In some cases, forward-looking statements can be identified by terminology such as “may”, “will”, “should”, “expects”, “projects”, “plans”, “anticipates”, and similar expressions. -

110307 Nr Wsps

FOR IMMEDIATE RELEASE VIA THE CANADIAN CUSTOM DISCLOSURE NETWORK AND THE TOP US FINANCIAL MARKETS NEWS RELEASE New Bell Helicopter Wire Strike Protection System Development Winnipeg, Manitoba – March 8, 2011 – Magellan Aerospace announced today a new agreement with Bell Helicopter for a Wire Strike Protection System (WSPS®) kit development. The helicopter to be fitted with WSPS will be the Bell UH-1Y. The design and production of the WSPS will be carried out at Magellan’s Bristol Aerospace operating division in Winnipeg, Manitoba, for delivery of the prototype kits in 2011. Bristol is the global expert for this unique system, offering a proven design and acknowledged technological expertise. In January of this year, the company also announced a new agreement with Hindustan Aeronautics Limited (HAL), headquartered in Bangalore, India for the design and development of a new WSPS kit for the HAL Advanced Light Helicopter (ALH). Bell Helicopters is a long time customer and supporter of WSPS. Bristol's initial WSPS development and testing was for the Bell CH-136 Kiowa in 1977. Bristol has previously adapted the design to several variants of Bell's UH-1 helicopters. Mr. Don Boitson, Vice President and General Manger, Bristol Aerospace, commented, “Our WSPS continues to lead the way with helicopter OEMs, and we are proud of our long-lasting and ongoing relationship with Bell Helicopter.” In 1977 Bristol, with the Canadian Forces, designed the WSPS to provide a measure of protection for helicopters to the potentially devastating consequences of inadvertent encounters with horizontally strung wires and cables. In 2009, Bristol reached the milestone of delivering its 20,000 th WSPS kit. -

Exploration, Imagination, Innovation: a New

EXPLORATION IMAGINATION INNOVATION A New Space Strategy for Canada EXPLORATION IMAGINATION INNOVATION A New Space Strategy for Canada Contents Message from the Minister The Case for Space CANADA’S LEGACY IN SPACE 5 THE ROLE OF SPACE IN CANADIAN SCIENCE EXCELLENCE THE SOCIO-ECONOMIC BENEFITS OF SPACE Canada’s Vision for Space Delivering the Vision – Canada’s Space Strategy 1. ENSURE CANADA REMAINS A LEADING SPACEFARING NATION BY JOINING THE LUNAR GATEWAY MISSION 1 2. INSPIRE THE NEXT GENERATION OF CANADIANS TO REACH FOR THE STARS 12 3. HARNESS SPACE TO SOLVE EVERYDAY CHALLENGES FOR CANADIANS 14 4. POSITION CANADA’S COMMERCIAL SPACE SECTOR TO HELP GROW THE ECONOMY AND CREATE THE JOBS OF THE FUTURE 1 5. ENSURE CANADA’S LEADERSHIP IN ACQUIRING AND USING SPACE-BASED DATA TO SUPPORT SCIENCE EXCELLENCE, INNOVATION AND ECONOMIC GROWTH 1 Moving Forward Message from the Minister As the Minister of Innovation, Science and Economic Development Canada, I am pleased to present Canada’s Space Strategy. Canada has a long and proud history of leadership in space science and technology. We were among the fi rst to enter the space age and have maintained a global reputation for scientifi c and technological excellence and ingenuity. Nearly every aspect of our daily lives is touched and made better by space innovation. Canadian scientists and fi rms are reshaping the way space is being explored and utilized. It has been estimated that the global space economy will triple in size over the next 20 years. This growth will be driven by a radical shift in the sector, whereby commercial fi rms are investing heavily in and benefi tting signifi cantly from their own space activities. -

For Immediate Release Via the Canadian Custom Disclosure Network

FOR IMMEDIATE RELEASE VIA THE CANADIAN CUSTOM DISCLOSURE NETWORK MAGELLAN AEROSPACE DELIVERS THE STRUCTURE FOR THE FIRST TWO PAYLOAD MODULES FOR RADARSAT CONSTELLATION MISSION Toronto, ON – September 15, 2015 – Magellan Aerospace (“Magellan”) is pleased to report the progress on a previously announced contract with MacDonald, Dettwiler and Associates Ltd. (“MDA”), a prime contractor for Canada’s RADARSAT Constellation Mission (“RCM”). Magellan has achieved key milestones in the contract with the delivery of the structure for the first two payload modules to MDA. The payload modules are major structural assemblies that will house the electronics for the radar payload being developed by MDA, and are key delivery milestones in Magellan’s contract with MDA. The payload module structures were designed and built at Magellan Aerospace, Winnipeg, the company’s centre of excellence for space systems. “The RCM contract has a challenging schedule,” said Mr. Phil Underwood, President and CEO, Magellan Aerospace, “Magellan’s ability to deliver the payload module structures on-time, and to our customer’s specifications is crucial to the success of this important Canadian satellite mission. The spacecraft buses that Magellan is manufacturing for RCM are significantly larger than the buses that have been provided for previous Canadian space missions,” he continued, “and Magellan has invested in a new Advanced Satellite Integration Facility in Winnipeg that will be large enough to accommodate the simultaneous build of three satellite buses. This investment demonstrates Magellan’s commitment to the RCM program and the global satellite market”. The first payload module structure for RCM was delivered to MDA in fall of 2014, and the second payload module structure was delivered in late spring of 2015. -

Magellan Aerospace Breaks Ground for JSF Advanced Composite Manufacturing Facility

For Immediate Release Magellan Aerospace Breaks Ground for JSF Advanced Composite Manufacturing Facility TORONTO, October 8/CNW/ - Magellan Aerospace was honoured to host a visit from The Right Honourable Stephen Harper, Prime Minister of Canada, at its Bristol Aerospace division in Winnipeg yesterday. The Prime Minister joined Magellan in welcoming a group of international and Canadian dignitaries to celebrate the initiation of the new Advanced Composite Manufacturing Facility being constructed in Winnipeg in support of the Joint Strike Fighter (JSF) program. At the event, Magellan Aerospace Chairman of the Board, Mr. Murray Edwards, gave special thanks and recognition for the support of the Federal Government, the other major funding partners, customers, and stakeholders in this major new undertaking. The launch customer for the new Center is BAE Systems in the United Kingdom, who awarded Magellan a contract to produce the JSF F-35 Lightning II horizontal tail components. The $22 million dollar, 13,000 square meter facility will be equipped with advanced technology for the manufacture of complex fabrications and assemblies. Mr. Edwards said, “We are delighted to have this opportunity today to recognize the federal government’s contribution to this program, whose actions have helped ensure Canadian companies are confident and competitive leaders in the global aerospace market. The government’s investment and commitment to the program since it began in 1997 is truly commendable.” Since that initial participation in the Concept Demonstration Phase until today, Canada has garnered unprecedented opportunities in this strategic long-term program to build the F-35 Lightning II aircraft for Canada and eight other partner nations. -

Haley Industries, Haley, on Aug 2009 Haley Industries Limited, Owned by Magellan Aerospace

AIME Success Story: Haley Industries, Haley, ON Aug 2009 Haley Industries Limited, owned by Magellan Aerospace Company Profile Manufacturer of aluminum and magnesium sand castings for the international aerospace industry . Country of Ownership: Canada . Year Established: 1952 (Owned by Magellan Aerospace since 2002) . Exporting: Yes . Quality Certification: ISO 9001 . Primary Industry (NAICS): 331529 - Non-Ferrous Foundries (except Die-Casting) . Primary Business Activity: Manufacturer / Processor / Producer . Total Sales ($CDN): $50,000,000 + . Export Sales ($CDN): $10,000,000 to $24,999,999 . Number of Employees: 526 . Clients: Pratt & Whitney Canada, Fiat Avio, Rolls-Royce, General Electric, Sikorsky Aircraft, Pratt & Whitney, TRW Lucas, GKN Westland, Agusta, Hamilton Sundstrand . Geographic Markets: Export Experience: Algeria, France, Germany, India, Italy, Japan, United Kingdom, United States Actively Pursuing: China, Russian Federation Background Haley Industries is in the highly competitive business of manufacturing complex components for the aerospace industry. The company’s products serve a global niche market and their sand castings are some of the most difficult in the world to manufacture. Staying competitive in this business requires ongoing training of uniquely skilled engineers and technicians. Haley’s customers have come to depend on them for the supply of components for the 747, 767 and 777 aircraft, F15 and F16 fighter jets, and for airbuses and helicopters. Haley Industries was founded in 1952 and was a prime contributor to the Avro Arrow aircraft program. Today Haley is one of the few manufacturers left in the Ottawa Valley. The company has been in the midst of a significant period of growth, with sales increasing rapidly from 2004 to 2008. -

C3670 R F BC-Magellan-New-Contract 04-12 0264 News Release Via Canada Newswire, Toronto 416-863-9350

c3670 r f BC-Magellan-new-contract 04-12 0264 News release via Canada NewsWire, Toronto 416-863-9350 Attention Business Editors: Magellan Aerospace Announces New Aeroengine Manufacturing Contract TORONTO, April 12 /CNW/ - Magellan Aerospace Corporation announced today that it has won a multi-million dollar contract for the manufacture of CF34 engine fan frames for General Electric Aircraft Engines. The fan frames are for the new 8D/E variant engine that has forecasted deliveries through 2010. The estimated value of the new contract is $(Cdn) 49 million dollars with all options exercised. Magellan's Bristol Aerospace operating division will perform the work, with deliveries commencing later this year. Bristol Aerospace is currently under contract for the manufacture of the CF34 fan frames for the current CF34-8/C variant engine. The popular CF34 engines helped launch today's fast-growing regional jet market. They are the engines of choice for virtually every aircraft in their thrust classes, including the Bombardier CRJ200 and CRJ700 regional jets, and Bombardier Challenger business jets. The new CF34-8D/E engine will power the Embraer ERJ170 regional jet and other aircraft, with a forecasted requirement for 1000 engines through 2010. Magellan Aerospace Corporation is one of the world's most integrated and comprehensive aerospace industry suppliers. Magellan designs, engineers, and manufactures aeroengine and aerostructure components for aerospace markets, advanced products for military and space markets, and complementary specialty products. Magellan is a public company whose shares trade on the Toronto Stock Exchange (MAL), with operating units throughout the United States and Canada. %SEDAR: 00002367E -0- 04/12/2002 /For further information: William A. -

FOR IMMEDIATE RELEASE VIA the CANADIAN CUSTOM DISCLOSURE NETWORK Magellan Aerospace Announces Contracts to Produce Aircraft Il

FOR IMMEDIATE RELEASE VIA THE CANADIAN CUSTOM DISCLOSURE NETWORK Magellan Aerospace Announces Contracts to Produce Aircraft Illumination Flares Toronto, Ontario – 15 March 2019 -- Magellan Aerospace Corporation (“Magellan”) announced today, agreements valued at CDN $48 million, with the Canadian government to perform the licensed manufacture of LUU-2 illumination flares for the Royal Canadian Air Force (RCAF). Magellan-produced LUU-2 illumination flares will be delivered from the Winnipeg facility’s propellant plant in Manitoba, Canada. The term of the contracts is five years. The LUU-2 is an air-deployed high-intensity illumination flare. The RCAF utilizes the LUU-2 to support night time search and rescue operations with illumination. The flares produce about 1.8 million candlepower of visual illumination for five minutes. “Magellan remains committed to continuing our 60-year legacy in supporting the Canadian Armed Forces and the RCAF with the delivery of critical mission support equipment and services’”, said Mr. Haydn Martin, Vice President, Business Development, Marketing and Contracts, Magellan Aerospace. About Magellan Aerospace Corporation Magellan Aerospace Corporation is a global aerospace company that provides complex assemblies and systems solutions to aircraft and engine manufacturers, and defense and space agencies worldwide. Magellan designs and manufactures aeroengine and aerostructure assemblies and components for aerospace markets, advanced proprietary products for military and space markets, and provides engine and component repair and overhaul services worldwide. Magellan is a public company whose shares trade on the Toronto Stock Exchange (TSX: MAL), with operating units throughout North America, Europe, and India. Forward Looking Statements Some of the statements in this press release may be forward-looking statements or statements of future expectations based on currently available information. -

Notice of Annual Meeting of Shareholders to Be Held on May 4, 2021

Notice of Annual Meeting of Shareholders To be held on May 4, 2021 MAGELLAN AEROSPACE CORPORATION NOTICE OF ANNUAL MEETING OF SHAREHOLDERS NOTICE IS HEREBY GIVEN that an annual meeting (the "Meeting") of the holders of common shares of MAGELLAN AEROSPACE CORPORATION (the "Corporation"), which, due to the continuing concerns of the coronavirus (“COVID-19”) pandemic, and due to the sensitivity to the public health and travel concerns of its shareholders, directors, employees, communities and other stakeholders, will be held in a virtual format to provide a consistent experience to all shareholders regardless of location on Tuesday, the 4thth of May, 2021, at 2:00 p.m. (Eastern Time) for the following purposes: 1. to receive the consolidated financial statements of the Corporation for its financial year ended December 31, 2020, together with the report of the auditors thereon; 2. to elect seven (7) directors of the Corporation for the ensuing year; 3. to appoint Ernst & Young LLP as the auditors of the Corporation with remuneration to be fixed by the directors; and 4. to transact such further or other business as may properly come before the Meeting or any adjournment or postponement thereof. Particulars of the foregoing matters are set forth in the accompanying management proxy circular (“Proxy Circular”) of the Corporation dated March 19, 2021. The financial statements for the year ended December 31, 2020 and the independent report of the auditors' of the Corporation thereon are available on SEDAR at www.sedar.com. It is important that your shares be represented at the Meeting. Please note that the Meeting will be held in a virtual, audio only, online format conducted by live webcast at https://web.lumiagm.com/274057799.