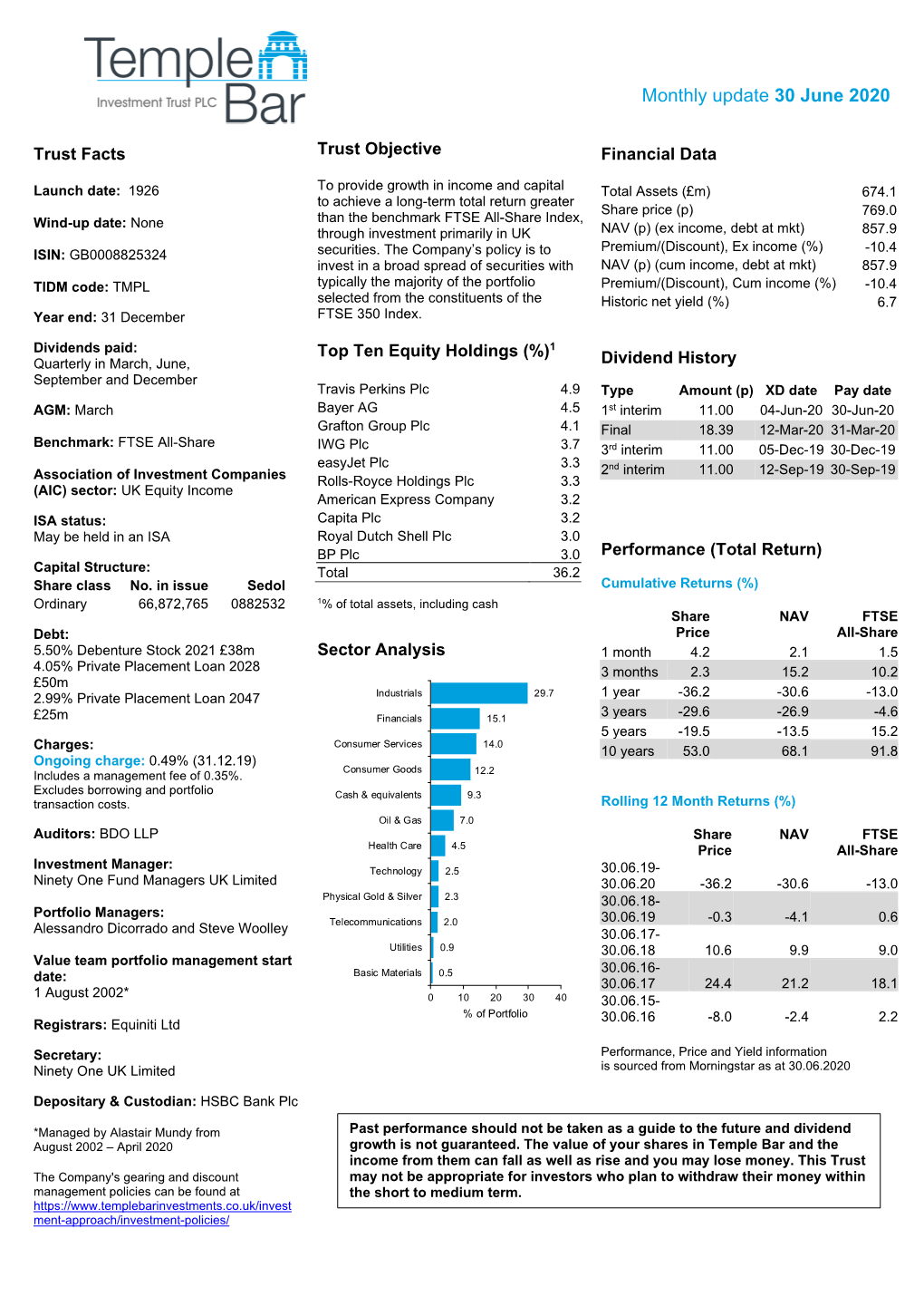

June 2020 Factsheet

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Proxy Vote Record

Company Name Ticker Country Meeting DateProposal Text Vote Instruction Abcam Plc ABC United Kingdom 04-Dec-20 Accept Financial Statements and Statutory Reports For Abcam Plc ABC United Kingdom 04-Dec-20 Approve Remuneration Report For Abcam Plc ABC United Kingdom 04-Dec-20 Reappoint PricewaterhouseCoopers LLP as Auditors For Abcam Plc ABC United Kingdom 04-Dec-20 Authorise the Audit and Risk Committee to Fix Remuneration of Auditors For Abcam Plc ABC United Kingdom 04-Dec-20 Re-elect Peter Allen as Director For Abcam Plc ABC United Kingdom 04-Dec-20 Re-elect Alan Hirzel as Director For Abcam Plc ABC United Kingdom 04-Dec-20 Elect Michael Baldock as Director For Abcam Plc ABC United Kingdom 04-Dec-20 Re-elect Louise Patten as Director For Abcam Plc ABC United Kingdom 04-Dec-20 Re-elect Mara Aspinall as Director For Abcam Plc ABC United Kingdom 04-Dec-20 Re-elect Giles Kerr as Director For Abcam Plc ABC United Kingdom 04-Dec-20 Authorise Issue of Equity For Abcam Plc ABC United Kingdom 04-Dec-20 Authorise Issue of Equity without Pre-emptive Rights For Abcam Plc ABC United Kingdom 04-Dec-20 Authorise Issue of Equity without Pre-emptive Rights in Connection with an Acquisition or Other Capital Investment For Abcam Plc ABC United Kingdom 04-Dec-20 Authorise Market Purchase of Ordinary Shares For Abcam Plc ABC United Kingdom 04-Dec-20 Accept Financial Statements and Statutory Reports For Abcam Plc ABC United Kingdom 04-Dec-20 Approve Remuneration Report For Abcam Plc ABC United Kingdom 04-Dec-20 Reappoint PricewaterhouseCoopers LLP as Auditors -

COVID-19 Proxy Governance Update

COVID-19 Proxy Governance Update 2020 AGM mid-season review FROM EQUINITI 01 Looking back and planning ahead It is incredible to note that it has been over 12 weeks since the official announcement on 23 March of the UK Government’s Stay at Home Measures, and nearly seven months since the severity of the pandemic became apparent in China. Over the said period, PLC boards, company secretaries and investor relations officers have kept their corporate calendars going thanks to rapid adoption of modified regulatory guidelines and inventive modes of engagement with investors. With annual general meetings being an obvious highlight in the corporate calendar, we take stock of the progress made so far over the 2020 AGM season, as well as using what we learned to plan ahead. Now that we are over the first ‘hump’ with the busy period of May AGMs out of the way, we are readying for the second ‘peak’ of June and July AGMs, and then an ‘easing’ until the second ‘mini’ season in the early autumn. As such, in this update, we look at: • 2020 AGM season statistics…so far • Proxy adviser engagement and ISS recommendations review • High-level assumptions for Q3 and Q4 • Relevant updates from the regulators, industry bodies and proxy advisers • Communications in the COVID-19 world – special commentary by leading financial PR firm,Camarco • How has COVID-19 impacted activism – special commentary by international law firm,White & Case 02 2020 AGM Season Statistics…so far Scope of data To assess progress and forecast what is to come, we look at the key statistics for the UK AGM season 2020 thus far. -

Parker Review

Ethnic Diversity Enriching Business Leadership An update report from The Parker Review Sir John Parker The Parker Review Committee 5 February 2020 Principal Sponsor Members of the Steering Committee Chair: Sir John Parker GBE, FREng Co-Chair: David Tyler Contents Members: Dr Doyin Atewologun Sanjay Bhandari Helen Mahy CBE Foreword by Sir John Parker 2 Sir Kenneth Olisa OBE Foreword by the Secretary of State 6 Trevor Phillips OBE Message from EY 8 Tom Shropshire Vision and Mission Statement 10 Yvonne Thompson CBE Professor Susan Vinnicombe CBE Current Profile of FTSE 350 Boards 14 Matthew Percival FRC/Cranfield Research on Ethnic Diversity Reporting 36 Arun Batra OBE Parker Review Recommendations 58 Bilal Raja Kirstie Wright Company Success Stories 62 Closing Word from Sir Jon Thompson 65 Observers Biographies 66 Sanu de Lima, Itiola Durojaiye, Katie Leinweber Appendix — The Directors’ Resource Toolkit 72 Department for Business, Energy & Industrial Strategy Thanks to our contributors during the year and to this report Oliver Cover Alex Diggins Neil Golborne Orla Pettigrew Sonam Patel Zaheer Ahmad MBE Rachel Sadka Simon Feeke Key advisors and contributors to this report: Simon Manterfield Dr Manjari Prashar Dr Fatima Tresh Latika Shah ® At the heart of our success lies the performance 2. Recognising the changes and growing talent of our many great companies, many of them listed pool of ethnically diverse candidates in our in the FTSE 100 and FTSE 250. There is no doubt home and overseas markets which will influence that one reason we have been able to punch recruitment patterns for years to come above our weight as a medium-sized country is the talent and inventiveness of our business leaders Whilst we have made great strides in bringing and our skilled people. -

Morningstar Report

Report as of 29 Sep 2021 Artemis Alpha Trust PLC , (GB0004355946) Morningstar Rating™ Peer Group Classification Last Close Last Actual NAV (27 Sep 2021) Discount Estimated Nav Not Rated Morningstar IT UK All 434.00 458.46 -5.34 458.46 Companies Investment Objective Performance To provide long-term capital and income growth by 232 investing predominantly in listed companies and to 199 achieve a NAV total return greater than the total 166 return of the FTSE All-Share Index. 133 100 67 2016 2017 2018 2019 2020 2021-08 1.68 24.30 -11.80 35.31 16.41 12.56 Fund Management Fee Summary A management fee is calculated by 0.75% p.a. of market capitalisation is less than or equal to GBP 250m; plus 0.70% p.a. that is more than GBP 250m but less than or equal to GBP 500m; plus 0.65% p.a. that is more than GBP 500m. No performance fee will be charged. Portfolio 30/04/2021 Asset Allocation % Long Short Net Equity Style Box™ Mkt Cap % Fund America Europe Asia Large Size Stocks 102.84 0.00 102.84 Giant 19.86 Bonds 0.00 0.00 0.00 Mid Large 25.53 Cash 2.88 13.24 -10.37 Medium 32.07 Other 7.53 0.00 7.53 Small Small 8.17 Value Blend Growth Micro 14.37 Style Average Mkt Fund Cap (Mil) Ave Mkt Cap GBP 6,753.1 <25 25-50 50-75 >75 2 Top Holdings Stock Sector Weightings % Fund World Regions % Fund Name Sector % hCyclical 64.09 Americas 1.27 Dignity PLC t 8.59 rBasic Materials - United States 1.27 easyJet PLC p 7.99 tConsumer Cyclical 48.98 Canada 0.00 Frasers Group PLC t 7.19 yFinancial Services 15.11 Latin America 0.00 Delivery Hero SE 6.56 Real Estate - t u Greater -

United Kingdom Small Company Portfolio-Institutional Class As of July 31, 2021 (Updated Monthly) Source: State Street Holdings Are Subject to Change

United Kingdom Small Company Portfolio-Institutional Class As of July 31, 2021 (Updated Monthly) Source: State Street Holdings are subject to change. The information below represents the portfolio's holdings (excluding cash and cash equivalents) as of the date indicated, and may not be representative of the current or future investments of the portfolio. The information below should not be relied upon by the reader as research or investment advice regarding any security. This listing of portfolio holdings is for informational purposes only and should not be deemed a recommendation to buy the securities. The holdings information below does not constitute an offer to sell or a solicitation of an offer to buy any security. The holdings information has not been audited. By viewing this listing of portfolio holdings, you are agreeing to not redistribute the information and to not misuse this information to the detriment of portfolio shareholders. Misuse of this information includes, but is not limited to, (i) purchasing or selling any securities listed in the portfolio holdings solely in reliance upon this information; (ii) trading against any of the portfolios or (iii) knowingly engaging in any trading practices that are damaging to Dimensional or one of the portfolios. Investors should consider the portfolio's investment objectives, risks, and charges and expenses, which are contained in the Prospectus. Investors should read it carefully before investing. This fund operates as a feeder fund in a master-feeder structure and the holdings listed below are the investment holdings of the corresponding master fund. Your use of this website signifies that you agree to follow and be bound by the terms and conditions of use in the Legal Notices. -

STOXX UK 180 Selection List

STOXX UK 180 Last Updated: 20210301 ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) Rank (FINAL)Rank (PREVIOUS) GB00B10RZP78 B10RZP7 ULVR.L 091321 UNILEVER PLC GB GBP Y 113 1 1 GB0009895292 0989529 AZN.L 098952 ASTRAZENECA GB GBP Y 105 2 2 GB0005405286 0540528 HSBA.L 040054 HSBC GB GBP Y 101.6 3 3 GB0007188757 0718875 RIO.L 071887 RIO TINTO GB GBP Y 76.5 4 7 GB0002374006 0237400 DGE.L 039600 DIAGEO GB GBP Y 75.8 5 4 GB00B03MLX29 B09CBL4 RDSa.AS B09CBL ROYAL DUTCH SHELL A GB EUR Y 69.3 6 8 GB0009252882 0925288 GSK.L 037178 GLAXOSMITHKLINE GB GBP Y 69 7 5 GB0007980591 0798059 BP.L 013849 BP GB GBP Y 68.3 8 9 GB0002875804 0287580 BATS.L 028758 BRITISH AMERICAN TOBACCO GB GBP Y 62 9 6 GB00BH0P3Z91 BH0P3Z9 BHPB.L 005666 BHP GROUP PLC. GB GBP Y 55.2 10 11 GB00B24CGK77 B24CGK7 RB.L 072769 RECKITT BENCKISER GRP GB GBP Y 50.9 11 10 GB0007099541 0709954 PRU.L 070995 PRUDENTIAL GB GBP Y 42.3 12 14 GB00B1XZS820 B1XZS82 AAL.L 490151 ANGLO AMERICAN GB GBP Y 40.5 13 15 GB00B2B0DG97 B2B0DG9 REL.L 073087 RELX PLC GB GBP Y 38.6 14 12 GB00BH4HKS39 BH4HKS3 VOD.L 071921 VODAFONE GRP GB GBP Y 37.7 15 13 JE00B4T3BW64 B4T3BW6 GLEN.L GB10B3 GLENCORE PLC GB GBP Y 36.5 16 18 GB00BDR05C01 BDR05C0 NG.L 024282 NATIONAL GRID GB GBP Y 32.7 17 16 GB0008706128 0870612 LLOY.L 087061 LLOYDS BANKING GRP GB GBP Y 31.8 18 22 GB0031348658 3134865 BARC.L 007820 BARCLAYS GB GBP Y 30 19 23 GB00BD6K4575 BD6K457 CPG.L 053315 COMPASS GRP GB GBP Y 29.9 20 21 GB00B0SWJX34 B0SWJX3 LSEG.L 095298 LONDON STOCK EXCHANGE GB GBP Y 25.2 21 17 GB00B19NLV48 B19NLV4 -

Premium Listed Companies Are Subject to the UK's Super-Equivalent Rules Which Are Higher Than the EU Minimum "Standard Listing" Requirements

List of Premium Equity Comercial Companies - 29th April 2020 Definition: Premium listed companies are subject to the UK's super-equivalent rules which are higher than the EU minimum "standard listing" requirements. Company Name Country of Inc. Description of Listed Security Listing Category Market Status Trading Venue Home Member State ISIN(S) 4IMPRINT GROUP PLC United Kingdom Ordinary Shares of 38 6/13p each; fully paid Premium Equity Commercial Companies RM LSE United Kingdom GB0006640972 888 Holdings Plc Gibraltar Ordinary Shares of 0.5p each; fully paid Premium Equity Commercial Companies RM LSE United Kingdom GI000A0F6407 AA plc United Kingdom Ordinary Shares of 0.1p each; fully paid Premium Equity Commercial Companies RM LSE United Kingdom GB00BMSKPJ95 Admiral Group PLC United Kingdom Ordinary Shares of 0.1p each; fully paid Premium Equity Commercial Companies RM LSE United Kingdom GB00B02J6398 AGGREKO PLC United Kingdom Ordinary Shares of 4 329/395p each; fully paid Premium Equity Commercial Companies RM LSE United Kingdom GB00BK1PTB77 AIB Group Plc Ireland Ordinary Shares of EUR0.625 each; fully paid Premium Equity Commercial Companies RM LSE Ireland IE00BF0L3536 Air Partner PLC United Kingdom Ordinary Shares of 1p each; fully paid Premium Equity Commercial Companies RM LSE United Kingdom GB00BD736828 Airtel Africa plc United Kingdom Ordinary Shares of USD0.50 each; fully paid Premium Equity Commercial Companies RM LSE United Kingdom GB00BKDRYJ47 AJ Bell plc United Kingdom Ordinary Shares of GBP0.000125 each; fully paid Premium -

FTSE 350 Companies Audited by KPMG

FTSE 350 companies audited by KPMG KPMG LLP1 expects to issue an audit report for 67 FTSE 350 companies within the next 12 months Data as at 30 June 2021 Company FTSE Index2 Industry classification (ICB Supersector)2 3i Group Plc FTSE 100 Financial services Aggreko Plc FTSE 250 Industrial goods and services AO World Plc FTSE 250 Retail Ascential Plc FTSE 250 Technology Ashmore Group Plc FTSE 250 Financial services Auto Trader Group Plc FTSE 100 Technology AVI Global Trust plc FTSE 250 Financial services Avon Rubber Plc FTSE 250 Industrial goods and services B&M European Value Retail SA FTSE 100 Retail Baillie Gifford Japan Trust Plc FTSE 250 Financial services Baillie Gifford Shin Nippon FTSE 250 Financial services Baillie Gifford US Growth Trust FTSE 250 Financial services Balfour Beatty Plc FTSE 250 Consumer products and services Barclays Plc FTSE 100 Banks Berkeley Group Holdings (The) Plc FTSE 100 Consumer products and services Big Yellow Group plc FTSE 250 Real estate British American Tobacco Plc FTSE 100 Food, beverage and tobacco BT Group Plc FTSE 100 Telecommunications Capita Plc FTSE 250 Industrial goods and services Chemring Group Plc FTSE 250 Industrial goods and services Compass Group Plc FTSE 100 Consumer products and services Computacenter Plc FTSE 250 Technology Croda International Plc FTSE 100 Basic resources Entain Plc FTSE 100 Travel and leisure Experian Plc FTSE 100 Industrial goods and services Grainger Plc FTSE 250 Real estate HICL Infrastructure Plc FTSE 250 Financial services International Consolidated Airlines Group -

Final Version Wework Article HBS Header 91Efe3b9-Fc0b-408B-B29e

Why WeWork Won’t Nori Gerardo Lietz Senior Lecturer of Business Administration, Harvard Business School Teaches Venture Capital/Private Equity and Real Estate Private Equity Sean Bracken, Research Associate, Harvard Business School Few startup companies, or corporate founders, have attracted as much attention as WeWork (“WeWork”1 or the Company). WeWork released its S-1 Registration Statement (the “Prospectus”) August 14th in anticipation of their IPO. The Prospectus pushes the boundaries of what are material nondisclosures permitted under the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). WeWork’s Prospectus clearly states that they are an “emerging company” under the JOBS Act which permits certain startup companies to apply different (lower) standards in terms of IPO disclosures. If the Prospectus complies with the JOBS Act, there is something seriously wrong with the JOBS Act. There has already been considerable commentary with complaints and hilarious comments about the byzantine corporate structure, the continuing projected losses, the plethora of conflicts, the complete absence of any substantive corporate governance, and the uncommon “New Age” parlance in the typical Prospectus. We stipulate to all of it but note there is a sense of “piling on” in terms of negative commentary. Remember many other high profile, recent IPO’d companies had plenty of conflicts, ridiculous corporate structures, pitiful corporate governance and flamboyant founders. The point of this piece isn’t to rehash what has already been written. Instead, we analyze the Company’s financials as presented in the Prospectus highlighting issues that haven’t been addressed. The Prospectus may present a less than complete picture of WeWork’s financial results. -

MITIE Group PLC (MTO:LN)

MITIE Group PLC (MTO:LN) Industrials/Professional Business Support Services Price: 69.00 GBX Report Date: September 29, 2021 Business Description and Key Statistics MITIE Group is a holding company. Through its subsidiaries, Co. is Current YTY % Chg engaged in the provision of strategic outsourcing services. Co.'s Technical Services division provides public and private sector Revenue LFY (M) 2,174 -2.1 customers with a range of project and maintenance services. The EPS Diluted LFY 0.24 187.1 division incorporates a range of primary engineering, maintenance, repair and project services, energy and carbon management Market Value (M) 253 services and water and real estate services. Co's Specialist Services incorporates several specialized services, including Shares Outstanding LFY (000) 365,956 Mitie's Care & Custody, Waste Management and Landscapes Book Value Per Share 0.22 businesses. Care & Custody provides critical public services in immigration, criminal justice and healthcare. EBITDA Margin % 5.10 Net Margin % 4.1 Website: www.mitie.com Long-Term Debt / Capital % 78.6 ICB Industry: Industrials Dividends and Yield TTM 0.00 - 0.00% ICB Subsector: Professional Business Support Services Payout Ratio TTM % 16.4 Address: The Shard;Leval 12;32 London Bridge Street London 60-Day Average Volume (000) 1,664 GBR 52-Week High & Low 77.30 - 27.25 Employees: 47,500 Price / 52-Week High & Low 0.89 - 2.53 Price, Moving Averages & Volume 85.5 85.5 MITIE Group PLC is currently trading at 69.00 which is 0.8% below its 50 day moving 77.9 77.9 average price of 69.53 and 13.3% above its 200 day 70.2 70.2 moving average price of 60.92. -

Avantis International Small Cap Value ETF As of July 2, 2021

Avantis International Small Cap Value ETF as of July 2, 2021 Issue Name Ticker CUSIP ISIN SEDOL Share Quantity Contract Count Market Value Weight Royal Mail PLC RMG 99080DFL5 GB00BDVZYZ77 BDVZYZ7 839,403 0 $6,735,765.34 0.70% AerCap Holdings NV AER N00985106 NL0000687663 B1HHKD3 124,273 0 $6,433,613.21 0.67% J Sainsbury PLC SBRY 999102EW2 GB00B019KW72 B019KW7 1,703,330 0 $6,411,095.50 0.67% St James's Place PLC STJ 999300288 GB0007669376 0766937 279,074 0 $5,844,713.50 0.61% M&G PLC MNG 99080TG21 GB00BKFB1C65 BKFB1C6 1,836,064 0 $5,798,902.22 0.60% Mitsui OSK Lines Ltd 9104 999102S98 JP3362700001 6597584 113,600 0 $5,308,163.47 0.55% Wm Morrison Supermarkets PLC MRW 9993015H3 GB0006043169 0604316 1,591,024 0 $5,280,515.16 0.55% Tate & Lyle PLC TATE 999102G00 GB0008754136 0875413 499,574 0 $5,254,832.10 0.55% Bellway PLC BWY 999301LN2 GB0000904986 0090498 111,848 0 $5,162,649.34 0.54% ASOS PLC ASC 990602XC3 GB0030927254 3092725 70,764 0 $5,096,509.43 0.53% Tourmaline Oil Corp TOU 89156V106 CA89156V1067 B3QJ0H8 169,402 0 $4,894,446.43 0.51% Marks & Spencer Group PLC MKS 999102CS3 GB0031274896 3127489 2,254,345 0 $4,772,251.66 0.50% Bekaert SA BEKB 999110XH7 BE0974258874 5827431 104,568 0 $4,724,213.48 0.49% Bure Equity AB BURE 999602MA0 SE0000195810 4152651 104,801 0 $4,722,878.38 0.49% Rheinmetall AG RHM 999110FZ7 DE0007030009 5334588 47,438 0 $4,694,016.19 0.49% ASR Nederland NV ASRNL 99080J7Q0 NL0011872643 BD9PNF2 119,362 0 $4,652,111.89 0.48% Singapore Press Holdings Ltd SPH 9993031L4 SG1P66918738 B012899 3,434,300 0 $4,413,882.62 0.46% -

United Kingdom Small Company Portfolio-Institutional Class As of March 31, 2021 (Updated Monthly) Source: State Street Holdings Are Subject to Change

United Kingdom Small Company Portfolio-Institutional Class As of March 31, 2021 (Updated Monthly) Source: State Street Holdings are subject to change. The information below represents the portfolio's holdings (excluding cash and cash equivalents) as of the date indicated, and may not be representative of the current or future investments of the portfolio. The information below should not be relied upon by the reader as research or investment advice regarding any security. This listing of portfolio holdings is for informational purposes only and should not be deemed a recommendation to buy the securities. The holdings information below does not constitute an offer to sell or a solicitation of an offer to buy any security. The holdings information has not been audited. By viewing this listing of portfolio holdings, you are agreeing to not redistribute the information and to not misuse this information to the detriment of portfolio shareholders. Misuse of this information includes, but is not limited to, (i) purchasing or selling any securities listed in the portfolio holdings solely in reliance upon this information; (ii) trading against any of the portfolios or (iii) knowingly engaging in any trading practices that are damaging to Dimensional or one of the portfolios. Investors should consider the portfolio's investment objectives, risks, and charges and expenses, which are contained in the Prospectus. Investors should read it carefully before investing. This fund operates as a feeder fund in a master-feeder structure and the holdings listed below are the investment holdings of the corresponding master fund. Your use of this website signifies that you agree to follow and be bound by the terms and conditions of use in the Legal Notices.