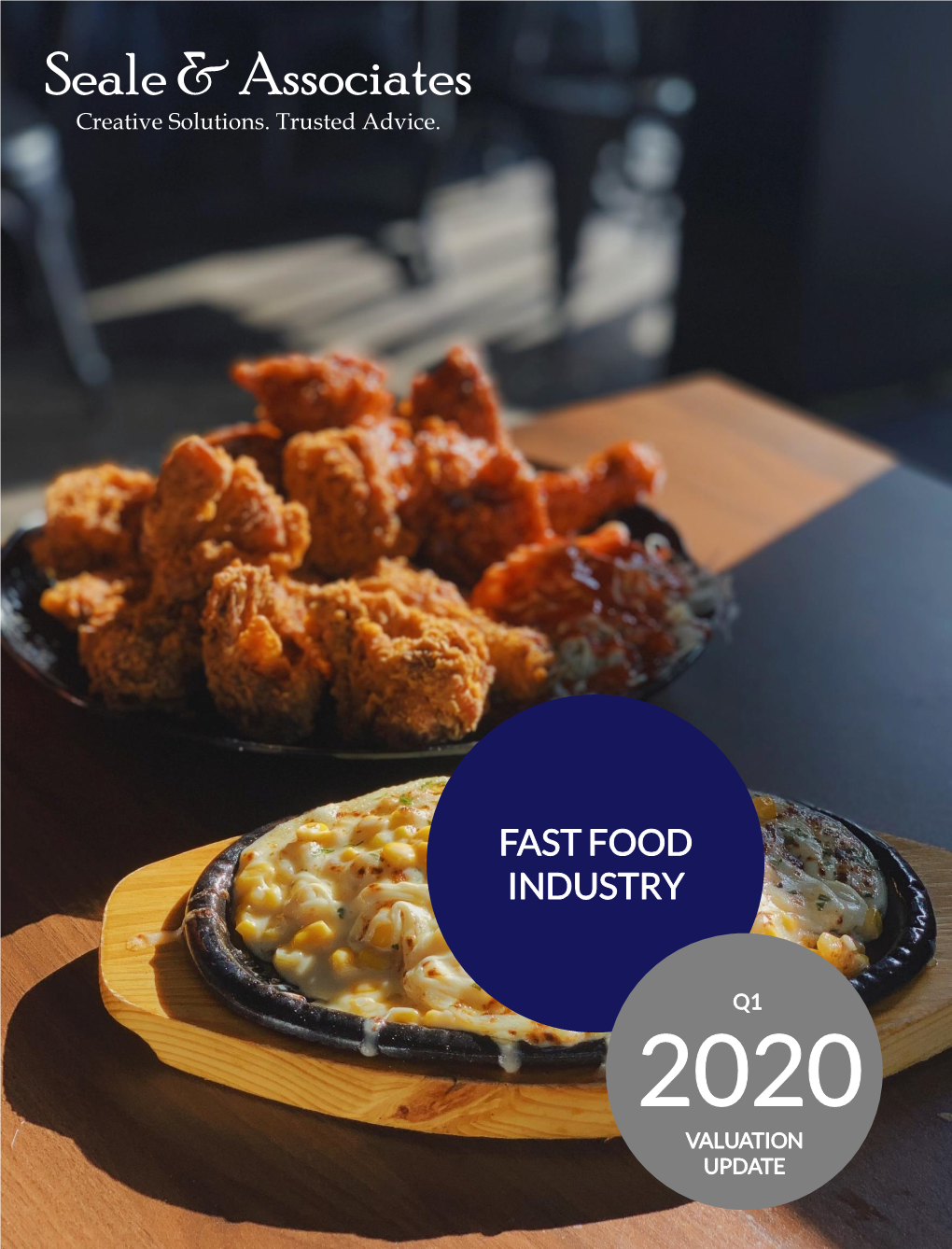

Valuation Update Q1 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Differences in Energy and Nutritional Content of Menu Items Served By

RESEARCH ARTICLE Differences in energy and nutritional content of menu items served by popular UK chain restaurants with versus without voluntary menu labelling: A cross-sectional study ☯ ☯ Dolly R. Z. TheisID *, Jean AdamsID Centre for Diet and Activity Research, MRC Epidemiology Unit, University of Cambridge, Cambridge, United a1111111111 Kingdom a1111111111 ☯ These authors contributed equally to this work. a1111111111 * [email protected] a1111111111 a1111111111 Abstract Background OPEN ACCESS Poor diet is a leading driver of obesity and morbidity. One possible contributor is increased Citation: Theis DRZ, Adams J (2019) Differences consumption of foods from out of home establishments, which tend to be high in energy den- in energy and nutritional content of menu items sity and portion size. A number of out of home establishments voluntarily provide consumers served by popular UK chain restaurants with with nutritional information through menu labelling. The aim of this study was to determine versus without voluntary menu labelling: A cross- whether there are differences in the energy and nutritional content of menu items served by sectional study. PLoS ONE 14(10): e0222773. https://doi.org/10.1371/journal.pone.0222773 popular UK restaurants with versus without voluntary menu labelling. Editor: Zhifeng Gao, University of Florida, UNITED STATES Methods and findings Received: February 8, 2019 We identified the 100 most popular UK restaurant chains by sales and searched their web- sites for energy and nutritional information on items served in March-April 2018. We estab- Accepted: September 6, 2019 lished whether or not restaurants provided voluntary menu labelling by telephoning head Published: October 16, 2019 offices, visiting outlets and sourcing up-to-date copies of menus. -

Market Insights Restaurants Dealreader

Restaurants DealReader 2H 2018 Market Insights 2018 was a busy year for M&A in the restaurant sector and appetite for investments remains robust headed into 2019. Despite recent macro variability and the sector facing a number of challenges, primarily related to traffic and minimum wage hikes, strategic acquirers, private equity groups and family offices continue to be active. Investors with multi-brand portfolios are typically seeking investments that can either provide incremental growth (particularly if their current portfolio has experienced flat-to-negative comps), expand their competencies (especially related to digital technology) or provide meaningful synergies from day one (although buyers are not as forthcoming in pricing in such synergies to the valuations). In regards to growth equity, we expect strong activity to continue in 2019, especially for differentiated fast casual concepts. Investors will continue to be interested in concepts that are on-trend (e.g., healthy, better-for- you menu), have demonstrated strong consumer engagement, have a model that is proven across multiple geographies (without any store closures) and that have a well-defined growth story in terms of scaling up. Selected Upcoming Industry Events Restaurant Leadership Conference (April 7-10, 2019 – Phoenix, AZ) UCLA Annual Restaurant Industry Conference (April 25, 2019 - Los Angeles, CA) National Restaurant Association Show (May 18-21, 2019 – Chicago, IL) Commentary Restaurant Industry Trends .The restaurant industry experienced a more Monthly Same-Store -

Interim Report for Q3 2020 Amrest Holdings SE Capital Group 10 NOVEMBER 2020

(all figures in EUR millions unless stated otherwise) Interim Report for Q3 2020 AmRest Holdings SE capital group 10 NOVEMBER 2020 AmRest Group Interim Report for 9 months ended 30 September 2020 1 (all figures in EUR millions unless stated otherwise) AmRest Group Interim Report for 9 months ended 30 September 2020 2 (all figures in EUR millions unless stated otherwise) Contents FINANCIAL HIGHLIGHTS (CONSOLIDATED DATA) ........................................................................................................... 5 PART A. DIRECTORS’ REPORT FOR Q3 2020 ..................................................................................................................... 7 PART B. CONDENSED CONSOLIDATED INTERIM REPORT FOR Q3 2020 ................................................................ 18 PART C. SEPARATE INTERIM REPORT FOR Q3 2020 ..................................................................................................... 44 AmRest Group Interim Report for 9 months ended 30 September 2020 3 (all figures in EUR millions unless stated otherwise) ighlights H AmRest Group Interim Report for 9 months ended 30 September 2020 4 (all figures in EUR millions unless stated otherwise) Financial highlights (consolidated data) 9 months ended 30 September 30 September 2019 2020 Revenue 1 125.4 1 432.5 EBITDA* 154.8 266.4 Profit/(loss) from operations (113.6) 73.0 Profit/(loss) before tax (160.4) 37.9 Net profit/(loss) (159.8) 28.3 Net profit/(loss) attributable to non-controlling interests (1.2) 1.1 Net profit/(loss) attributable -

The State of the Deal and Deloitte Queensland Index

The State of the Deal and Deloitte Queensland Index March 2021 – Queensland Index Exceeds $100 billion THE STATE OF THE DEAL | March 2021 – Queensland Index Exceeds $100 billion Contents Executive Summary 1 Then & Now – Investment Landscape 3 Then & Now – Deloitte Queensland Index 4 Queensland Economic Update 7 The Deloitte Queensland Index Q1 2021 8 Contacts 11 Sources 12 ii THE STATE OF THE DEAL | March 2021 – Queensland Index Exceeds $100 billion Executive Summary Following the significant rebound in the second half of 2020, companies in the Deloitte Queensland Index exceeded $100 billion at 31 March 2021, the highest month end market capitalisation on record for the State. Deloitte Queensland Index S&P/ASX All Ordinaries Companies in the Deloitte return in Q1 2021 return in Q1 2021 Queensland Index 3.5% 2.4% 169 at 31 March 2021 10.6% in Q4 2020 14.0% in Q4 2020 173 at 31 December 2020 90 companies increased Market capitalisation as at Mar-21 market capitalisation (53%) 66 companies decreased market $101.6b capitalisation (39%) 12 no movement (7%) $97.2b as at Dec-20 $18.5b as at Sep-02 5 delistings 1 listing (1%) Announced QLD M&A Disclosed value of announced transactions in Q1 2021 QLD M&A transactions in Q1 2021 64 $1.9b 92 in Q4 2020 $3.3b in Q4 2020 1 THE STATE OF THE DEAL | March 2021 – Queensland Index Exceeds $100 billion The Deloitte Queensland Index increased by 3.5% in Q1 2021 Queensland M&A more broadly remains strong with with total market capitalisation increasing to $101.6b at 64 transactions announced in Q1 2021 including: Mar-21, the highest month end value on record for the State. -

Fast Food and Takeaway Food Services in Australia April 2019 Bao Vuong

Freshen up: Consumer health consciousness Thisbrings report was healthier provided to ingredients to the table RMIT Library (2133773121) by IBISWorld on 19 August 2019 in accordance with their licence agreement with IBISWorld IBISWorld Industry Report H4512 Fast Food and Takeaway Food Services in Australia April 2019 Bao Vuong 2 About this Industry 15 Major Markets 27 Collins Foods Limited 2 Industry Definition 17 International Trade 28 Subway Systems Australia Pty Limited 2 Main Activities 18 Business Locations 2 Similar Industries 29 Operating Conditions 3 Additional Resources 20 Competitive Landscape 29 Capital Intensity 20 Market Share Concentration 30 Technology and Systems 4 Industry at a Glance 20 Key Success Factors 30 Revenue Volatility 20 Cost Structure Benchmarks 31 Regulation and Policy 5 Industry Performance 22 Basis of Competition 32 Industry Assistance 5 Executive Summary 23 Barriers to Entry 5 Key External Drivers 23 Industry Globalization 33 Key Statistics 6 Current Performance 33 Industry Data 8 Industry Outlook 24 Major Companies 33 Annual Change 11 Industry Life Cycle 24 McDonald’s Australia Holdings Pty 33 Key Ratios Limited 13 Products and Markets 25 Competitive Foods Australia Pty Ltd 34 Jargon & Glossary 26 Domino’s Pizza Enterprises Limited 13 Supply Chain 26 Yum! Restaurants Australia Pty Limited 13 Products and Services 27 Craveable Brands Pty Ltd 15 Demand Determinants www.ibisworld.com.au | (03) 9655 3881 | [email protected] WWW.IBISWORLD.COM.AU Fast Food and Takeaway Food Services in Australia April 2019 2 About this Industry Industry Definition Industry firms primarily provide fast usually provided in takeaway containers food, such as burgers, pizza, sandwiches or packaging, and is consumed on the and sushi, and takeaway for immediate premises, taken away or delivered. -

Amrest Acquires Starbucks Business in Germany

AmRest acquires Starbucks business in Germany Wroclaw, Poland, 20th April 2016, AmRest Holdings SE („AmRest”, “the Company”) (WSE: EAT), the largest publicly listed restaurant operator in Central Europe, announced today that on April 19th, 2016 the Company signed an agreement with Starbucks Coffee Company to acquire its equity stores in Germany. The transaction will come into effect as of May 23rd, 2016 and will result in AmRest having the license to operate and develop Starbucks brand in that country. Since entering Germany in 2002 with two stores in Berlin, Starbucks business has expanded to 158 stores across the country. The portfolio of 144 equity cafés together with 14 licensee stores makes Germany the largest market for Starbucks in the continental Europe. “We’ve built an impressive business in Germany over the past 14 years, employing nearly 2,000 partners across the market. But we know Germany could be a much bigger market for us and we have ambitious growth plans to be where our customers live, work and travel.” - said Kris Engskov, president of Starbucks, Europe, Middle East and Africa (EMEA). He continued: “We are proud to expand our partnership with AmRest, who are recognized across Europe as one of the most entrepreneurial, people-focused companies in food retail, and have been remarkably successful in bringing the Starbucks experience to these important markets.” AmRest has been a partner licensee for Starbucks since 2008, when it opened its first café in the Czech Republic. Since then, AmRest has developed Starbucks stores in Czech Republic, Poland, Hungary, Bulgaria, Romania and recently adding Slovakia, where the first Starbucks is planned to be opened by mid 2016. -

Socially Conscious Australian Equity Holdings

Socially Conscious Australian Equity Holdings As at 30 June 2021 Country of Company domicile Weight COMMONWEALTH BANK OF AUSTRALIA AUSTRALIA 10.56% CSL LTD AUSTRALIA 8.46% AUST AND NZ BANKING GROUP AUSTRALIA 5.68% NATIONAL AUSTRALIA BANK LTD AUSTRALIA 5.32% WESTPAC BANKING CORP AUSTRALIA 5.08% TELSTRA CORP LTD AUSTRALIA 3.31% WOOLWORTHS GROUP LTD AUSTRALIA 2.93% FORTESCUE METALS GROUP LTD AUSTRALIA 2.80% TRANSURBAN GROUP AUSTRALIA 2.55% GOODMAN GROUP AUSTRALIA 2.34% WESFARMERS LTD AUSTRALIA 2.29% BRAMBLES LTD AUSTRALIA 1.85% COLES GROUP LTD AUSTRALIA 1.80% SUNCORP GROUP LTD AUSTRALIA 1.62% MACQUARIE GROUP LTD AUSTRALIA 1.54% JAMES HARDIE INDUSTRIES IRELAND 1.51% NEWCREST MINING LTD AUSTRALIA 1.45% SONIC HEALTHCARE LTD AUSTRALIA 1.44% MIRVAC GROUP AUSTRALIA 1.43% MAGELLAN FINANCIAL GROUP LTD AUSTRALIA 1.13% STOCKLAND AUSTRALIA 1.11% DEXUS AUSTRALIA 1.11% COMPUTERSHARE LTD AUSTRALIA 1.09% AMCOR PLC AUSTRALIA 1.02% ILUKA RESOURCES LTD AUSTRALIA 1.01% XERO LTD NEW ZEALAND 0.97% WISETECH GLOBAL LTD AUSTRALIA 0.92% SEEK LTD AUSTRALIA 0.88% SYDNEY AIRPORT AUSTRALIA 0.83% NINE ENTERTAINMENT CO HOLDINGS LIMITED AUSTRALIA 0.82% EAGERS AUTOMOTIVE LTD AUSTRALIA 0.82% RELIANCE WORLDWIDE CORP LTD UNITED STATES 0.80% SANDFIRE RESOURCES LTD AUSTRALIA 0.79% AFTERPAY LTD AUSTRALIA 0.79% CHARTER HALL GROUP AUSTRALIA 0.79% SCENTRE GROUP AUSTRALIA 0.79% ORORA LTD AUSTRALIA 0.75% ANSELL LTD AUSTRALIA 0.75% OZ MINERALS LTD AUSTRALIA 0.74% IGO LTD AUSTRALIA 0.71% GPT GROUP AUSTRALIA 0.69% Issued by Aware Super Pty Ltd (ABN 11 118 202 672, AFSL 293340) the trustee of Aware Super (ABN 53 226 460 365). -

Asx Clear – Acceptable Collateral List 28

et6 ASX CLEAR – ACCEPTABLE COLLATERAL LIST Effective from 20 September 2021 APPROVED SECURITIES AND COVER Subject to approval and on such conditions as ASX Clear may determine from time to time, the following may be provided in respect of margin: Cover provided in Instrument Approved Cover Valuation Haircut respect of Initial Margin Cash Cover AUD Cash N/A Additional Initial Margin Specific Cover N/A Cash S&P/ASX 200 Securities Tiered Initial Margin Equities ETFs Tiered Notes to the table . All securities in the table are classified as Unrestricted (accepted as general Collateral and specific cover); . Specific cover only securities are not included in the table. Any securities is acceptable as specific cover, with the exception of ASX securities as well as Participant issued or Parent/associated entity issued securities lodged against a House Account; . Haircut refers to the percentage discount applied to the market value of securities during collateral valuation. ASX Code Security Name Haircut A2M The A2 Milk Company Limited 30% AAA Betashares Australian High Interest Cash ETF 15% ABC Adelaide Brighton Ltd 30% ABP Abacus Property Group 30% AGL AGL Energy Limited 20% AIA Auckland International Airport Limited 30% ALD Ampol Limited 30% ALL Aristocrat Leisure Ltd 30% ALQ ALS Limited 30% ALU Altium Limited 30% ALX Atlas Arteria Limited 30% AMC Amcor Ltd 15% AMP AMP Ltd 20% ANN Ansell Ltd 30% ANZ Australia & New Zealand Banking Group Ltd 20% © 2021 ASX Limited ABN 98 008 624 691 1/7 ASX Code Security Name Haircut APA APA Group 15% APE AP -

Past Gold & Silver Plate Winners

Past Gold & Silver Plate Winners For 66 years, the IFMA Gold & Silver Plate Awards have acknowledged the most outstanding operator talents in our $600 billion foodservice industry. Since its Silver Plates are awarded in the following inception, the Gold & Silver Plate program segments: has followed the tradition of “recognizing excellence to encourage excellence.” Business & Industry/Foodservice Management As the highest possible operator honor in Chain Fast Service the industry, the Gold & Silver Plate Awards Chain Full Service program has grown and evolved in response Colleges & Universities to the rigorous demands of an industry Elementary & Secondary Schools which itself has experienced continued Health Care growth and evolution. In this way, the Gold Hotels & Lodging & Silver Plate Awards program has reached Independent Restaurants and maintained its coveted position as the Specialty Foodservices most significant and widely-recognized operator tribute. Following is a listing of all past winners segmented by category and by year. One look shows that our winners comprise pioneers, leaders and legends of the foodservice industry. IFMA GOLD PLATE AWARD RECIPIENTS 1964 HENRY A. MONTAGUE* (Dec.) BY YEAR Greyhound Food Management, Inc. The following is a chronological listing of IFMA’s 1965 JUSTUS W. PUTSCH* (Dec.) Gold Plate Award recipients. The listing indicates Putsch’s Plaza Restaurants, Inc. each winner’s title and/or company affiliation at the time the award was given. NORMAN BESS** (Dec.) American Society of Association *= Gold Plate Award Winner Executives **= Honorary Gold Plate Winner 1966 JAMES F. HUTTON* (Dec.) 1955 FRED A. SIMONSON* (Dec.) Automatic Retailers of America, Inc. Greenfield-Mills Restaurant Company 1967 GERALD RAMSEY* (Dec.) 1956 WALTER F. -

Participant List

PARTICIPANT LIST Please find below a list of current participants in the Quarterly Salary Review. For a complete list by super sector, sector and segment refer to Mercer WIN®. 3M Australia API 7-Eleven Stores API Management A Menarini Australia APL Co. (Aus) - BR A.P.Moller-Maersk AS (AU) Apotex Abbott Australasia APT Management Services (APA Group) AbbVie Aquila Resources Actelion Pharmaceuticals Australia Arrium Mining & Materials Adama Australia Arrow Electronics Australia Adelaide Brighton Asahi Beverages Australia Adelaide Football Club Asaleo Care Australia adidas Australia Ascendas Hospitality Australia Fund Management Adventist Healthcare Aspen Australia AECOM Astrazeneca Afton Chemical Asia Pacific LLC AT & T Global Network Services Australia Aggreko Australia ATCO Australia AIA Australia Atlas Iron Aimia Proprietary Loyalty Australia Ausenco Air New Zealand – Australia AusGroup Akzo Nobel Australia Australia Post Alcatel-Lucent Australia Australian Catholic University Alcon (Novartis) Laboratories Australia Australian Computer Society Alexion Australasia Australian Fashion Labels Allergan Australian Red Cross Blood Service Alphapharm Avaloq Australia Alstom Transport Australia Aveo Group Amadeus IT Pacific Aviall Australia American Express Global Business Travel Australia AVJennings Holdings Amgen Australia Avon Products AMT Group BaptistCare NSW & ACT Amway of Australia Barminco Apex Tool Group BASF Australia © March 2017 Mercer Consulting (Australia) Pty Ltd Quarterly Salary Review 4.1 PARTICIPANT LIST Beam Global Australia -

AMREST an Effective Recipe for Robust Global License Management

AMREST An Effective Recipe for Robust Global License Management COMPANY BACKGROUND AmRest operates restaurants such as Burger King, Pizza Hut and Starbucks in Central Europe, Eastern Europe and as far afield as China. It uses numerous retail and business software applications – from point-of-sale to engineering and business software – to support more than 25,000 staff. CHALLENGE Without strong controls in place, license management was extremely painstaking. Obtaining the right information regarding licenses and entitlement involved analyzing a mass of data. With multiple audits from major vendors to manage, accurate discovery for an IT estate across a global operation was a prerequisite for ensuring the company was correctly licensed. SNOW’S CONTRIBUTION The Snow Platform, comprising Snow License Manager, Snow Inventory and Software Recognition Service, is installed on-premiseSnow enables the company to identify license risks and provides a platform for effective Software Asset Management. BUSINESS BENEFITS • Accurate inventory and discovery giving full visibility and insight into actual license usage • Identification of more than €150,000 of unlicensed and unauthorized software • Optimization of licenses and significant cost reduction • Introduction of business unit charge backs for license costs • Creation of a white list of approved applications SAM HERO Pawel Szczepaniak, Software License Manager at AmRest, explains the benefits of devoting resource to strong license management. “In less than 12 months thanks to Snow, I have been able to transform how the company views license management. As a result, the need for a new role was created to focus specifically manage and optimize licenses across AmRest’s global operations.” SNOWSOFTWARE.COM MANAGING EXPENSIVE SOFTWARE APPLICATIONS “Using Snow, we have identified AmRest is the largest independent restaurant operator in more than €100,000 of unlicensed Central and Eastern Europe. -

Wszystko Jest Możliwe!

(all figures in EUR millions unless stated otherwise) Wszystko jest możliwe! Interim Report for 9 months ConsolidatedConsolidated Directors’ Directors’Directors’ Report ReportReport endedforfor 6the months year 30 ended ended September 31 3300 December JuneJune 2012019 20189 2018 AmRest Holdings SE AmRestAmRest HoldingsHoldings SESE Madrid, 15 November 2018 2278 AFUGUSTEBRUARY 201 2019 9 AmRest Group 1 Consolidated Directors’ Report for 6 months ended 30 June 2019 (all figures in EUR millions unless stated otherwise) AmRest Group 2 Consolidated Directors’ Report for 6 months ended 30 June 2019 (all figures in EUR millions unless stated otherwise) CONTENTS FINANCIAL HIGHLIGHTS (CONSOLIDATED DATA) .........................................................................4 GROUP BUSINESS OVERVIEW ...................................................................................................5 FINANCIAL AND ASSET POSITION OF THE GROUP ........................................................................8 BRANDS OPERATED BY THE GROUP ....................................................................................... 14 KEY INVESTMENTS................................................................................................................ 18 PLANNED INVESTMENT ACTIVITIES ......................................................................................... 19 SIGNIFICANT EVENTS AND TRANSACTIONS IN 2018 ................................................................. 19 EXTERNAL DEBT .................................................................................................................