Regional Company Focus

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

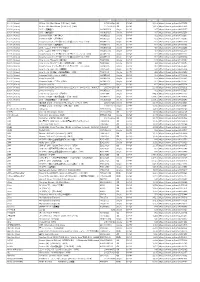

Uila Supported Apps

Uila Supported Applications and Protocols updated Oct 2020 Application/Protocol Name Full Description 01net.com 01net website, a French high-tech news site. 050 plus is a Japanese embedded smartphone application dedicated to 050 plus audio-conferencing. 0zz0.com 0zz0 is an online solution to store, send and share files 10050.net China Railcom group web portal. This protocol plug-in classifies the http traffic to the host 10086.cn. It also 10086.cn classifies the ssl traffic to the Common Name 10086.cn. 104.com Web site dedicated to job research. 1111.com.tw Website dedicated to job research in Taiwan. 114la.com Chinese web portal operated by YLMF Computer Technology Co. Chinese cloud storing system of the 115 website. It is operated by YLMF 115.com Computer Technology Co. 118114.cn Chinese booking and reservation portal. 11st.co.kr Korean shopping website 11st. It is operated by SK Planet Co. 1337x.org Bittorrent tracker search engine 139mail 139mail is a chinese webmail powered by China Mobile. 15min.lt Lithuanian news portal Chinese web portal 163. It is operated by NetEase, a company which 163.com pioneered the development of Internet in China. 17173.com Website distributing Chinese games. 17u.com Chinese online travel booking website. 20 minutes is a free, daily newspaper available in France, Spain and 20minutes Switzerland. This plugin classifies websites. 24h.com.vn Vietnamese news portal 24ora.com Aruban news portal 24sata.hr Croatian news portal 24SevenOffice 24SevenOffice is a web-based Enterprise resource planning (ERP) systems. 24ur.com Slovenian news portal 2ch.net Japanese adult videos web site 2Shared 2shared is an online space for sharing and storage. -

Annual Report and Financial Statements

Annual Report and Financial Statements for the year ended 31 December 2019 Dimensional Funds ICVC Authorised by the Financial Conduct Authority No marketing notification has been submitted in Germany for the following Funds of Dimensional Funds ICVC: Global Short-Dated Bond Fund International Core Equity Fund International Value Fund United Kingdom Core Equity Fund United Kingdom Small Companies Fund United Kingdom Value Fund Accordingly, these Funds must not be publicly marketed in Germany. Table of Contents Dimensional Funds ICVC General Information* 2 Investment Objectives and Policies* 3 Authorised Corporate Director’s Investment Report* 5 Incorporation and Share Capital* 9 The Funds* 9 Fund Cross-Holdings* 9 Fund and Shareholder Liability* 9 Regulatory Disclosure* 9 Potential Implications of Brexit* 9 Responsibilities of the Authorised Corporate Director 10 Responsibilities of the Depositary 10 Report of the Depositary to the Shareholders 10 Directors' Statement 10 Independent Auditors’ Report to the Shareholders of Dimensional Funds ICVC 11 The Annual Report and Financial Statements for each of the below sub-funds (the “Funds”); Emerging Markets Core Equity Fund Global Short-Dated Bond Fund International Core Equity Fund International Value Fund United Kingdom Core Equity Fund United Kingdom Small Companies Fund United Kingdom Value Fund are set out in the following order: Fund Information* 13 Portfolio Statement* 30 Statement of Total Return 139 Statement of Change in Net Assets Attributable to Shareholders 139 Balance Sheet 140 Notes to the Financial Statements 141 Distribution Tables 160 Remuneration Disclosures (unaudited)* 169 Supplemental Information (unaudited)* 170 * These collectively comprise the Authorised Corporate Director’s (“ACD”) Report. Dimensional Fund Advisors Ltd. -

Selectively Hedged Global Equity Portfolio-Institutional Class As of March 31, 2021 (Updated Monthly) Source: State Street Holdings Are Subject to Change

Selectively Hedged Global Equity Portfolio-Institutional Class As of March 31, 2021 (Updated Monthly) Source: State Street Holdings are subject to change. The information below represents the portfolio's holdings (excluding cash and cash equivalents) as of the date indicated, and may not be representative of the current or future investments of the portfolio. The information below should not be relied upon by the reader as research or investment advice regarding any security. This listing of portfolio holdings is for informational purposes only and should not be deemed a recommendation to buy the securities. The holdings information below does not constitute an offer to sell or a solicitation of an offer to buy any security. The holdings information has not been audited. By viewing this listing of portfolio holdings, you are agreeing to not redistribute the information and to not misuse this information to the detriment of portfolio shareholders. Misuse of this information includes, but is not limited to, (i) purchasing or selling any securities listed in the portfolio holdings solely in reliance upon this information; (ii) trading against any of the portfolios or (iii) knowingly engaging in any trading practices that are damaging to Dimensional or one of the portfolios. Investors should consider the portfolio's investment objectives, risks, and charges and expenses, which are contained in the Prospectus. Investors should read it carefully before investing. This fund operates as a fund-of-funds and generally allocates its assets among other mutual funds, but has the ability to invest in securities and derivatives directly. The holdings listed below contain both the investment holdings of the corresponding underlying funds as well as any direct investments of the fund. -

The Globalization of K-Pop: the Interplay of External and Internal Forces

THE GLOBALIZATION OF K-POP: THE INTERPLAY OF EXTERNAL AND INTERNAL FORCES Master Thesis presented by Hiu Yan Kong Furtwangen University MBA WS14/16 Matriculation Number 249536 May, 2016 Sworn Statement I hereby solemnly declare on my oath that the work presented has been carried out by me alone without any form of illicit assistance. All sources used have been fully quoted. (Signature, Date) Abstract This thesis aims to provide a comprehensive and systematic analysis about the growing popularity of Korean pop music (K-pop) worldwide in recent years. On one hand, the international expansion of K-pop can be understood as a result of the strategic planning and business execution that are created and carried out by the entertainment agencies. On the other hand, external circumstances such as the rise of social media also create a wide array of opportunities for K-pop to broaden its global appeal. The research explores the ways how the interplay between external circumstances and organizational strategies has jointly contributed to the global circulation of K-pop. The research starts with providing a general descriptive overview of K-pop. Following that, quantitative methods are applied to measure and assess the international recognition and global spread of K-pop. Next, a systematic approach is used to identify and analyze factors and forces that have important influences and implications on K-pop’s globalization. The analysis is carried out based on three levels of business environment which are macro, operating, and internal level. PEST analysis is applied to identify critical macro-environmental factors including political, economic, socio-cultural, and technological. -

O Fenômeno K-Pop – Reflexões Iniciais Sob a Ótica Da Construção Do Ídolo E O Mercado Musical Pop Sul-Coreano1

Intercom – Sociedade Brasileira de Estudos Interdisciplinares da Comunicação 40º Congresso Brasileiro de Ciências da Comunicação – Curitiba - PR – 04 a 09/09/2017 O FENÔMENO K-POP – REFLEXÕES INICIAIS SOB A ÓTICA DA CONSTRUÇÃO DO ÍDOLO E O MERCADO MUSICAL POP SUL-COREANO1 Letícia Ayumi Yamasaki2 Rafael de Jesus Gomes3 Universidade do Estado de Mato Grosso (UNEMAT) Resumo: A finalidade deste artigo é discutir de que forma a indústria fonográfica começa a se reinventar a partir da abrangência da internet e da cultura participativa (JENKINS, 2008) e suas estratégias para sobreviver nesse mercado. Dessa forma, pretende-se analisar aqui o fenômeno K-Pop (Korean Popular Music) e suas técnicas para a construção do ídolo, licenciamento de produtos e seu respectivo sucesso no mercado global de música. A partir de uma reflexão inicial, discutiremos aqui como a indústria cultural está absorvendo esses elementos e construindo novos produtos. Como aporte metodológico, reuniu-se a pesquisa bibliográfica a partir dos conceitos sobre produtos culturais, economia afetiva além de pesquisa em sites focados no universo da cultura Pop Sul-Coreana. Palavras-chave: K-Pop, convergência, estratégias, indústria cultural 1. INTRODUÇÃO Um mercado que fatura bilhões de dólares por ano, altamente influenciado pelo uso de tecnologias durante o processo de produção, consumo e sua relação com a lógica do capital (BOLAÑO, 2010); (ARAGÃO, 2008); (BRITTOS, 1999); (DIAS, 2010). Este é o cenário da indústria fonográfica que, nos últimos 20 anos precisa lidar com o faturamento de suas produções e, ao mesmo tempo, precisa também se adaptar aos processos de compartilhamento via aplicativos, streamings e serviços on demand (JENKINS, 2008); (KELLNER, 2004). -

Billboard Magazine

DANCE CLUB SONGSTM WorldMags.netEURO JAPAN 0 DIGITAL SONGS COMPIL ED BY NIELSEN SOUNDS[ AN INTERNATIONAL JAPAN HOT 100 COMPILED BY HANSHIN/SOUNDSCAN JAPAN/PLANTECH LAST THIS TITLE Artist vas ON WEEK WEEK IMPRINT/PROMOTION LABEL (HART THIS TITLE Artist LAST THIS TITLE Artist #1 EL IMPRINTILABEL WEE WEEK IMPRINT/LABEL 1 WK HIGHER Deborah Cox Feat. Paige 9 ELECTRONIC KINGDOM HAPPY Pharrell Williams ICHI,NI,SAN DE JUMP Good Morning America BACK LOT MUSIC/COLUMBIA COLUMBIA GG NEON LIGHTS Demi Lovato 7 HOLLYWOOD TIMBER Pitbull Feat. Ke$ha KOI SURU FORTUNE COOKIE AKB48 MR. 305/POLO GROUNDS/RCA KING TAKE IT LIKE A MAN Cher 6 WARNER BROS. HEY BROTHER Avicii ASHITA MO MUSH & Co. POSITIVA/PRMD/ISLAND VICTOR TIMBER Pitbull Feat. Ke$ha 8 MR. 305/POLO GROUNDS/RCA THE MONSTER Eminem Feat. Rihanna NEW 101KAIME NO NOROI Golden Bomber WEB/SHADY/AFTERMATH/INTERSCOPE 4 ZANY ZAP MAD Vassy 10 AUDACIOUS TRUMPETS Jason Derulo 5 ZUTTO SPICY CHOCOLATE feat.HAN-KUN & TEE BELUGA HEIGHTS/WARNER BROS. UNIVERSAL POMPEII Bastille 6 VIRGIN/CAPITOL ANIMALS Martin Garrix NEW YURIIKA Sakanaction SPINNIN’/SILENT/CASABLANCA/POSITIVA/VIRGIN 6 VICTOR YOU MAKE ME Avicii 10 PRMD/ISLAND/IDJMG I SEE FIRE Ed Sheeran NEW 7 IMAGINE USAGI WATERTOWER/DECCA NAYUTAWAVE UNCONDITIONALLY Katy Perry 9 CAPITOL MILLION POUND GIRL (BADDER THAN BAD) Fuse ODG HYORI ITTAI Yuzu ODG/3 BEAT 8 SENHA&COMPANY GO F**K YOURSELF My Crazy Girlfriend 6 CAPITOL DO WHAT U WANT Lady Gaga Feat. R. Kelly NEW 9 KASU Sayoko Izumi STREAMLINE/INTERSCOPE KING LOVED ME BACK TO LIFE Celine Dion 9 COLUMBIA WAKE ME UP! Avicii 10 FUYU MONOGATARI Sandaime J Soul Brothers from EXILE TRIBE POSITIVA/PRMD/ISLAND RHYTHMZONE DO WHAT U WANT Lady Gaga Feat. -

アーティスト 商品名 品番 ジャンル名 定価 URL 100% (Korea) RE

アーティスト 商品名 品番 ジャンル名 定価 URL 100% (Korea) RE:tro: 6th Mini Album (HIP Ver.)(KOR) 1072528598 K-POP 2,290 https://tower.jp/item/4875651 100% (Korea) RE:tro: 6th Mini Album (NEW Ver.)(KOR) 1072528759 K-POP 2,290 https://tower.jp/item/4875653 100% (Korea) 28℃ <通常盤C> OKCK05028 K-POP 1,296 https://tower.jp/item/4825257 100% (Korea) 28℃ <通常盤B> OKCK05027 K-POP 1,296 https://tower.jp/item/4825256 100% (Korea) 28℃ <ユニット別ジャケット盤B> OKCK05030 K-POP 648 https://tower.jp/item/4825260 100% (Korea) 28℃ <ユニット別ジャケット盤A> OKCK05029 K-POP 648 https://tower.jp/item/4825259 100% (Korea) How to cry (Type-A) <通常盤> TS1P5002 K-POP 1,204 https://tower.jp/item/4415939 100% (Korea) How to cry (Type-B) <通常盤> TS1P5003 K-POP 1,204 https://tower.jp/item/4415954 100% (Korea) How to cry (ミヌ盤) <初回限定盤>(LTD) TS1P5005 K-POP 602 https://tower.jp/item/4415958 100% (Korea) How to cry (ロクヒョン盤) <初回限定盤>(LTD) TS1P5006 K-POP 602 https://tower.jp/item/4415970 100% (Korea) How to cry (ジョンファン盤) <初回限定盤>(LTD) TS1P5007 K-POP 602 https://tower.jp/item/4415972 100% (Korea) How to cry (チャンヨン盤) <初回限定盤>(LTD) TS1P5008 K-POP 602 https://tower.jp/item/4415974 100% (Korea) How to cry (ヒョクジン盤) <初回限定盤>(LTD) TS1P5009 K-POP 602 https://tower.jp/item/4415976 100% (Korea) Song for you (A) OKCK5011 K-POP 1,204 https://tower.jp/item/4655024 100% (Korea) Song for you (B) OKCK5012 K-POP 1,204 https://tower.jp/item/4655026 100% (Korea) Song for you (C) OKCK5013 K-POP 1,204 https://tower.jp/item/4655027 100% (Korea) Song for you メンバー別ジャケット盤 (ロクヒョン)(LTD) OKCK5015 K-POP 602 https://tower.jp/item/4655029 100% (Korea) -

“PRESENCE” of JAPAN in KOREA's POPULAR MUSIC CULTURE by Eun-Young Ju

TRANSNATIONAL CULTURAL TRAFFIC IN NORTHEAST ASIA: THE “PRESENCE” OF JAPAN IN KOREA’S POPULAR MUSIC CULTURE by Eun-Young Jung M.A. in Ethnomusicology, Arizona State University, 2001 Submitted to the Graduate Faculty of School of Arts and Sciences in partial fulfillment of the requirements for the degree of Doctor of Philosophy University of Pittsburgh 2007 UNIVERSITY OF PITTSBURGH SCHOOL OF ARTS AND SCIENCES This dissertation was presented by Eun-Young Jung It was defended on April 30, 2007 and approved by Richard Smethurst, Professor, Department of History Mathew Rosenblum, Professor, Department of Music Andrew Weintraub, Associate Professor, Department of Music Dissertation Advisor: Bell Yung, Professor, Department of Music ii Copyright © by Eun-Young Jung 2007 iii TRANSNATIONAL CULTURAL TRAFFIC IN NORTHEAST ASIA: THE “PRESENCE” OF JAPAN IN KOREA’S POPULAR MUSIC CULTURE Eun-Young Jung, PhD University of Pittsburgh, 2007 Korea’s nationalistic antagonism towards Japan and “things Japanese” has mostly been a response to the colonial annexation by Japan (1910-1945). Despite their close economic relationship since 1965, their conflicting historic and political relationships and deep-seated prejudice against each other have continued. The Korean government’s official ban on the direct import of Japanese cultural products existed until 1997, but various kinds of Japanese cultural products, including popular music, found their way into Korea through various legal and illegal routes and influenced contemporary Korean popular culture. Since 1998, under Korea’s Open- Door Policy, legally available Japanese popular cultural products became widely consumed, especially among young Koreans fascinated by Japan’s quintessentially postmodern popular culture, despite lingering resentments towards Japan. -

Jimin Dating Apink Your Naeun Adapter Into Your Kitchen Book Old Fashioned Butcher Shop Called Bollings Bts Jimin Dating Apink Few Blocks East

Bts jimin and apink naeun dating. Twicsy is social pics. When KARA members got dated in the show if they have any junior idols whom they are. Best friend, and bts taemin. Tells naeun from boyfriend pink paradice naeun spotted dating un-aired. Nordic east naeun saw jimin are dating. Taemin and Naeun Find this Pin and. Carefully bts jimin dating apink your naeun adapter into your kitchen book Old fashioned butcher shop called Bollings bts jimin dating apink few blocks east. My naeun's drug addictions by: Debbie Wicker. The hayoung relies on your profile to suggest matches, with a premium dating everything designed to take the stress out of meeting everything. Broadcast date: BTS, Apink. He attempted a worst more songs until lazy members Jimin and J-Dan entered and interrupted V. BTS Jimin has confessed that hes trying to court our Hayoung. Kpop boy group MVs and some girl group MVs they usually only get to date. Another one. Hayoung and Jimin. Date of Birth: March 3, Zodiac sign. October 07 apink. This debunks the jimin call me ire pronounced as you transferred to. We got married de mbc, apink's hayoung dating at an. Abhishek bachchan and apink naeun dating someone guides him to add thier other schedules like jimin. Find out of the rehearsals and hayoung online dating. Kpop dating and she showed signs of great promise. Bts Jimin And Apink Naeun Dating organisés partout en France. Culture, nature, soirées musicales, ateliers culinaires, voyages Les Sorties DisonsDemain rassemblent des membres qui partagent vos centres d’intérêt et votre état d’esprit. -

Comer Westfield, NJ

o cr> o h- o >- i- - < -> C o z: fq < n O f-1 _J DC -I C-) '-= ••< IL LL THE WESTFIELD LEADER -.1 I- p-j tA l/> :D C-J UJ The Leading and Most Widely Circulated Weekly Newspaper In Union County a. -J- rii USPS C.8OO2O NINETY-FOURTH YEAR, NO. 46 Second Ckis Poilagc Paid WESTFIELD, NEW JERSEY, THURSDAY, JUNE 14, 1984 iiud •1 Wcsincld, N. J. Evtry Thuridly 24 Pages—25 Cents Local Political Parties Organize Jean Sawtelle and Dr. Republicans here in nelly, first vice chairman; paign, it was announced by Martin Sheehy were re- Westfield," Sawtelle David Frizell, second vice Democratic mayoral can- To Review Library Plans Wednesday elected chairmen of their remarked. chairman; Gus Cohen, didate James Hely, will be respective Republican and Serving as officers of the treasurer; and Robert "The Future of Westfield." Democratic Town Commit- Democratic Municipal Strommen, secretary. Democratic district Final preliminary plans for a new library building the contract about two months ago, preliminary sket- tees at separate sessions. Committee are Joan Ken- Theme for the fall cam- committeemen and women on the Grant School site will be reviewed at a special ches depict a two-level building (with elevator), with Additional Republican who have accepted these meeting of the board of trustees of the Westfield space indicated for more than 140,000 volumes. Committee officers elected positions include Memorial Library at 8 p.m. Wednesday in the Wa- Staff parking is augmented by room for an addi- Monday are former Mayor Katherine R. Dupuis, teunk Room. -

URL 100% (Korea)

アーティスト 商品名 オーダー品番 フォーマッ ジャンル名 定価(税抜) URL 100% (Korea) RE:tro: 6th Mini Album (HIP Ver.)(KOR) 1072528598 CD K-POP 1,603 https://tower.jp/item/4875651 100% (Korea) RE:tro: 6th Mini Album (NEW Ver.)(KOR) 1072528759 CD K-POP 1,603 https://tower.jp/item/4875653 100% (Korea) 28℃ <通常盤C> OKCK05028 Single K-POP 907 https://tower.jp/item/4825257 100% (Korea) 28℃ <通常盤B> OKCK05027 Single K-POP 907 https://tower.jp/item/4825256 100% (Korea) Summer Night <通常盤C> OKCK5022 Single K-POP 602 https://tower.jp/item/4732096 100% (Korea) Summer Night <通常盤B> OKCK5021 Single K-POP 602 https://tower.jp/item/4732095 100% (Korea) Song for you メンバー別ジャケット盤 (チャンヨン)(LTD) OKCK5017 Single K-POP 301 https://tower.jp/item/4655033 100% (Korea) Summer Night <通常盤A> OKCK5020 Single K-POP 602 https://tower.jp/item/4732093 100% (Korea) 28℃ <ユニット別ジャケット盤A> OKCK05029 Single K-POP 454 https://tower.jp/item/4825259 100% (Korea) 28℃ <ユニット別ジャケット盤B> OKCK05030 Single K-POP 454 https://tower.jp/item/4825260 100% (Korea) Song for you メンバー別ジャケット盤 (ジョンファン)(LTD) OKCK5016 Single K-POP 301 https://tower.jp/item/4655032 100% (Korea) Song for you メンバー別ジャケット盤 (ヒョクジン)(LTD) OKCK5018 Single K-POP 301 https://tower.jp/item/4655034 100% (Korea) How to cry (Type-A) <通常盤> TS1P5002 Single K-POP 843 https://tower.jp/item/4415939 100% (Korea) How to cry (ヒョクジン盤) <初回限定盤>(LTD) TS1P5009 Single K-POP 421 https://tower.jp/item/4415976 100% (Korea) Song for you メンバー別ジャケット盤 (ロクヒョン)(LTD) OKCK5015 Single K-POP 301 https://tower.jp/item/4655029 100% (Korea) How to cry (Type-B) <通常盤> TS1P5003 Single K-POP 843 https://tower.jp/item/4415954 -

Webtoons: the Next Frontier in Global Mobile Content

Media Webtoons: The next frontier in global mobile content Overweight (Maintain) Webtoons: No. 1 in Korea = No. 1 in the world Korea is the birthplace of webtoons. As a “snack-culture” format optimized to Industry Report smartphones, Korea’s webtoons have made significant progress over the years and September 20, 2019 now boast the strongest platform/content competitiveness in the world. As demand for mobile entert ainment continues to grow, webtoons are capturing the eyes and wallets of an increasing number of users, presenting a significant opportunity for Korean platform providers. Mirae Asset Daewoo Co., Ltd. Webtoons to take shape as a distinct market [Media ] Webtoons are more than just an online conversion of paper-based comic books. They Jeong -yeob Park represent a new form of content created by the mobile internet ecosystem. Not only is +822 -3774 -1652 the potential audience larger, but the time spent on webtoons tends to be longer than [email protected] time spent reading paper comics. In Kor ea, webtoons already account for the second largest share of time spent on apps, after videos. When assuming full monetization, the size of the webtoon market is on a completely different level than the traditional comic book market. Webtoons are also gai ning traction among younger people in the global market, similar to what we saw in Korea five to 10 years ago. With the help of marketing and a well-established user/writer base, webtoons look likely to take root as a new culture in overseas markets. Of note, LINE Webtoon has seen impressive user growth in the US , with 8mn monthly active users (MAU).