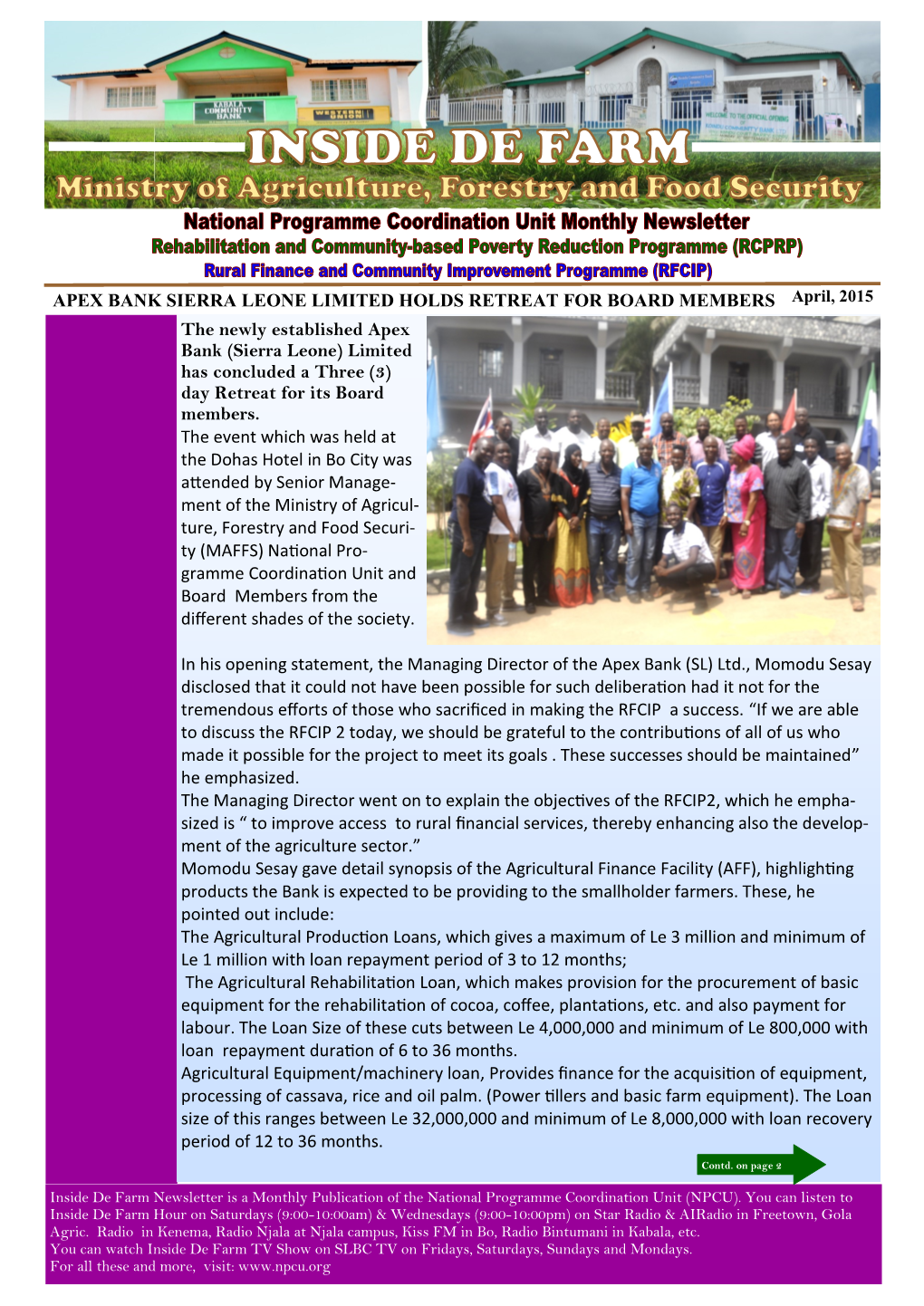

Apex Bank Sierra Leone Limited Holds

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

BTI 2020 Country Report — Sierra Leone

BTI 2020 Country Report Sierra Leone This report is part of the Bertelsmann Stiftung’s Transformation Index (BTI) 2020. It covers the period from February 1, 2017 to January 31, 2019. The BTI assesses the transformation toward democracy and a market economy as well as the quality of governance in 137 countries. More on the BTI at https://www.bti-project.org. Please cite as follows: Bertelsmann Stiftung, BTI 2020 Country Report — Sierra Leone. Gütersloh: Bertelsmann Stiftung, 2020. This work is licensed under a Creative Commons Attribution 4.0 International License. Contact Bertelsmann Stiftung Carl-Bertelsmann-Strasse 256 33111 Gütersloh Germany Sabine Donner Phone +49 5241 81 81501 [email protected] Hauke Hartmann Phone +49 5241 81 81389 [email protected] Robert Schwarz Phone +49 5241 81 81402 [email protected] Sabine Steinkamp Phone +49 5241 81 81507 [email protected] BTI 2020 | Sierra Leone 3 Key Indicators Population M 7.7 HDI 0.438 GDP p.c., PPP $ 1604 Pop. growth1 % p.a. 2.1 HDI rank of 189 181 Gini Index 34.0 Life expectancy years 53.9 UN Education Index 0.403 Poverty3 % 81.3 Urban population % 42.1 Gender inequality2 0.644 Aid per capita $ 71.8 Sources (as of December 2019): The World Bank, World Development Indicators 2019 | UNDP, Human Development Report 2019. Footnotes: (1) Average annual growth rate. (2) Gender Inequality Index (GII). (3) Percentage of population living on less than $3.20 a day at 2011 international prices. Executive Summary General elections were held in Sierra Leone in March 2018 to elect the president, parliament and local councils. -

The West Indian Mission to West Africa: the Rio Pongas Mission, 1850-1963

The West Indian Mission to West Africa: The Rio Pongas Mission, 1850-1963 by Bakary Gibba A thesis submitted in conformity with the requirements for the degree of Doctor of Philosophy Graduate Department of History University of Toronto © Copyright by Bakary Gibba (2011) The West Indian Mission to West Africa: The Rio Pongas Mission, 1850-1963 Doctor of Philosophy, 2011 Bakary Gibba Department of History, University of Toronto Abstract This thesis investigates the efforts of the West Indian Church to establish and run a fascinating Mission in an area of West Africa already influenced by Islam or traditional religion. It focuses mainly on the Pongas Mission’s efforts to spread the Gospel but also discusses its missionary hierarchy during the formative years in the Pongas Country between 1855 and 1863, and the period between 1863 and 1873, when efforts were made to consolidate the Mission under black control and supervision. Between 1873 and 1900 when additional Sierra Leonean assistants were hired, relations between them and African-descended West Indian missionaries, as well as between these missionaries and their Eurafrican host chiefs, deteriorated. More efforts were made to consolidate the Pongas Mission amidst greater financial difficulties and increased French influence and restrictive measures against it between 1860 and 1935. These followed an earlier prejudiced policy in the Mission that was strongly influenced by the hierarchical nature of nineteenth-century Barbadian society, which was abandoned only after successive deaths -

World Bank Document

ReportNo. 4457-SL SierraLeone i FinancialSector Study Public Disclosure Authorized February8, 1984 West Africa Region ProgramsI, Division B FOR OFFICIALUSE ONLY Public Disclosure Authorized Public Disclosure Authorized Documentof the WorldBank Public Disclosure Authorized This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosedwithout World Bank authorization. Currency equivalents Year US$ per Leone 1977 .95310 1978 .9531 1979 .9637 1980 .944:1 1981 .8516 1982 .8113 1983 (October) .3984 Fiscal year July 1 - June 30 FOR OFFICIALUSE ONLY Table of Contents Page No. SUMMARY AND RECOMMENDATIONS ...... .... ......... ........... .. i I. THE ECONOMY ...........................................................1 A. Aggregate savings and investment .............. .......... 2 B. Domestic and international value of the Leone .......... 2 C. Balance of payments .................................... 5 D. Government finances ........ oo..... ............... .... 8 E. Industry ................... ........... ... .. 9 F. Agricultural production problems .o ................. 9 II. MAJOR ISSUES OF THE FINANCIAL SYSTEM ..... o............... 12 A. The Government's demand for credit ..................... 13 B. Excess liquidity in the financial system ............. o 14 C. The foreign exchange pipeline .. o........................ 18 D Interest rate policy ......... .. o.. ......... .. 0 .... 20 III. THE RURAL FINANCIAL SYSTEM ................... -

Moving on After Trauma: How Women in Sierra Leone Rebuild Their Lives After Widowhood Through Ebola

Moving on after trauma: How women in Sierra Leone rebuild their lives after widowhood through Ebola. By: Desirée Hessels Cover Picture: A women in front of her house in Pettifu Brown, Sierra Leone (2016). All photographs presented in this thesis are from the author’s private collection and her own original work. 2 Wageningen University – Department of Social Sciences. MSc Thesis Sociology of Development and Change – Disaster Studies Chair Moving on after trauma: How women in Sierra Leone rebuild their lives after widowhood through Ebola June 2017 MSc International Development Studies. Specialisation: Desirée Hessels BSc (910717 – 331 – 030) Disaster Studies Supervisor: dr. Han van Dijk Thesis Code: SDC – 80736 3 Acknowledgements As a young girl, my attention was always drawn to the pictures of unfamiliar faces and stories from countries far away, to those that are tested by their environment in a way I would never have to experience. I wondered ‘how do they live their lives?’ This passion led me to study cultural anthropology and international development. During my studies, I read about women in post-conflict situations, and the inequality in human rights they experience. I was curious to discover these women’s personal stories and their experiences in that situation. This led me to Sierra Leone to conduct my Master thesis research. It was a year with many challenges, and high lights. I am thankful that I was provided this opportunity, it gave me more insight in the academic processes that research contains and it took me to places I would never imagine to see. The most challenging was the period before the field research, and being in the field was surprisingly enjoyable and educational on both academic and personal level. -

Organizational Strategies and Performance in the Banking Industry Focused on the Transnational Banks in Sierra Leone: an Ex Post Facto Study

Organizational Strategies and Performance in the Banking Industry Focused on the Transnational Banks in Sierra Leone: An Ex Post Facto Study Hassan Elsan Mansaray Department of Business Administration and Entrepreneurship Development, Institute of Public Administration and Management (IPAM) University of Sierra Leone, Freetown, Sierra Leone [email protected] Abstract Keywords To successfully examine the banking strategies used by organisational strategy; performance; banking industry; transnational banks transnational Banks in Sierra Leone to improve their performances, the researcher used a longitudinal research method to carry out the study. The method is used so as to achieve the research goals by focusing on the ensuing operating challenges to survive, grow and meets their set goals with the purpose of maintaining their core mandate as financial intermediaries as well as agents of economic growth in Sierra Leone and beyond. The study noted that the transnational Banks in Sierra Leone’s organizational strategies support every individual to comprehend where the banking business is moving and how the banks willpower can influence those strategies. Equally, the study further observed that their organizational strategies also explain their market positions and clarify how the transnational banks communicate with customers, competitors, and departmental changing structures to convey success. Based on the entire study, the transnational banks are on the advanced trajectory which can make them continuously achieve competitive advantage in the banking industry in Sierra Leone, since their strategies are positive towards meeting their goals. Although some improvements are needed on their marketing strategies, knowledge about bank products and services, innovation, strategy orientation, as well as wide improvement on employees’ satisfaction strategy to increase commitment and loyalty. -

Sierra Leone: a New Era of Reform?

SIERRA LEONE: A NEW ERA OF REFORM? Africa Report N°143 – 31 July 2008 TABLE OF CONTENTS EXECUTIVE SUMMARY AND RECOMMENDATIONS................................................. i I. INTRODUCTION ............................................................................................................. 1 II. THE 2007 ELECTIONS: NEW POLITICS ................................................................... 1 A. RESTORING LEGITIMACY TO ELECTIONS .....................................................................................1 B. RESURGENCE OF IDENTITY POLITICS...........................................................................................3 C. THE DECLINE OF PATRONAGE?...................................................................................................5 1. Cracks in the patronage system ............................................................................................6 2. The fear of the oligarchy ......................................................................................................7 III. THE NEW APC GOVERNMENT: REFORM AND REALPOLITIK......................... 9 A. EXECUTIVE POWER AND POPULISM.............................................................................................9 1. Identifying the problem ........................................................................................................9 2. Responding to the problem: running government “like a business concern”.....................10 3. Presidential appointments: southerners out, northerners in................................................11 -

Governance Transition Team (GTT) Report

Republic of Sierra Leone Office of the President Report of the Governance Transition Team 2018 Executive Summary This is the Report of the Governance Transition Team (GTT) as mandated by His Excellency President Julius Maada Bio when he announced its setting up in a State House Press Release on 6 April 2018, two days after being sworn into office. An astonishing level of fiscal indiscipline and rampant corruption by the former APC Government of President Ernest Koroma had led to the near-collapse of Sierra Leone’s economy by the time the Government of President Julius Maada Bio was sworn into office. The economy was left burdened with external debt amounting to US $1.6 billion, domestic debt amounting to Le 4.99 trillion or US$658 million, and an exploded payroll (salaries and other compensation for government employees) of Le.2 trillion (US $263 million) or 14.4% of the GDP. The national currency became moribund, trading at Le.7600 to a dollar. In addition, the Government owes vendors (for goods and services) an extremely large amount of US $1.4 billion. The State’s liabilities as at 30 March 2018 amounted to US $3.7 billion. Inflation as at March 2018 was 17.2. Overall, economic growth plummeted from 6% in 2016 to 3.7% in 2017. Consequent of the APC government’s inability to close the fiscal gap and adhere to agreed actions under the Extended Credit Facility, the IMF suspended disbursement of both budgetary and balance of payment support to Sierra Leone in 2017. Other budgetary support agencies including World Bank, EU, and African Development Bank withheld their budgetary support from the second half of 2017 to date. -

Leveraging Diaspora Remittances on Post Ebola Recovery in Sierra Leone

Baseline Assessment Report Leveraging Diaspora Remittances on Post Ebola Recovery in Sierra Leone 016/2015 1 The contents of this report are the sole responsibility of the author and cannot be taken to reflect the views of the ACP Secretariat and its Member States governments, the European Commission or the International Organization for Migration. Prepared by Awoleye J. Olatunji Date: 21st April, 2016 2 Contents List of acronyms................................................................................................................................... 3 Executive summary .............................................................................................................................. 5 Introduction and background ............................................................................................................... 7 Overview of The State Of Affairs: Background Information on Ebola Virus Disease Outbreak 2014: Trends, Magnitude and Dimensions .................................................................................................... 8 The Potential of Cash Transfer Programmes for Developing Countries ............................................. 9 Diaspora Remittances and Sierra Leone ............................................................................................ 10 Leveraging Diaspora Remittances: Some Guiding Issues for Developing Framework of Analysis and Baseline Assessment Tool .......................................................................................................... -

Bank Portfolio Allocation: Evidence from Sierra Leone

University of Ghana http://ugspace.ug.edu.gh BANK PORTFOLIO ALLOCATION: EVIDENCE FROM SIERRA LEONE BY BAIMBA AUGUSTINE BOCKARIE (10297268) THIS THESIS IS SUBMITTED TO THE UNIVERSITY OF GHANA, LEGON IN PARTIAL FULFILLMENT OF THE REQUIREMENT FOR THE AWARD OF MPHIL ECONOMICS DEGREE JUNE, 2012. University of Ghana http://ugspace.ug.edu.gh DECLARATION This is to certify that this thesis is the result of a research undertaken by Baimba Augustine Bockarie towards the award of a Master of Philosophy degree in the Department of Economics, University of Ghana. ----------------------------------------------------- BAIMBA AUGUSTINE BOCKARIE ------------------------------------------------- -------------------------------------------------- DR. S. K. K. AKOENA DR. E. OSEI-ASSIBEY (SUPERVISOR) (SUPERVISOR) i University of Ghana http://ugspace.ug.edu.gh ABSTRACT Bank portfolio allocation is an important determinant of the efficacy of monetary policy through the bank lending channel of monetary policy transmission mechanism. This study generally investigates the factors that influence banks‟ portfolio allocation in Sierra Leone. Specifically, the study looks into the effects of risk premium, leverage ratio, and credit risk on banks‟ earning asset portfolio allocation in Sierra Leone between 2002 and 2011. Using annual bank level data on an unbalanced panel of thirteen commercial banks for the study period, and employing time and bank specific fixed effects model for estimation, it is confirmed that risk premium, the share of non-performing loans in the banks‟ loan portfolio, tier 1 capital ratio (leverage ratio), and local currency deposit levels positively and significantly affect the share of loan supply to the private sector in banks‟ earning assets. On the other hand the loan-deposit ratios (or advance-deposit ratio) and bank size has significant negative effects on the share of loans in banks‟ earning assets. -

C4C Manifesto

Coalition For Change (C4C) - MANIFESTO For 2018 PREAMBLE Our nation is at a crossroad. Quality of life in Sierra Leone is at its lowest. Unemployment is peaking at an all-time high of 70 per cent while inflation is hovering at 18 per cent. Our national debt is hitting US$2 billion. The number of mothers dying during childbirth is on the increase. It is a pity that in today's 21st century, only 13 per cent of our population have access to electricity and drinking water running through our pipes is also a daily hassle for the greatest majority of our people. Ours is a country that deserves to have made a great deal more progress than she has achieved. In our recent history, our Nation has experienced much abuse of the Law of the Land, disease outbreaks, joblessness, hunger, crime, economic discrimination, environmental degradation and disasters, and unprecedented corruption. Collectively these experiences have resulted in a tragic loss of hope in our country's capacity to stand and take her right of place among the comity of progressive Nations. It would be recalled that when HE Sam-Sumana partnered Mr. Ernest Koroma and they the elections of 2007, the Sierra Leonean economy began to wake up from the doldrums. The duo inherited a GDP of 2,158 billion US Dollars and built the economy to achieve a GDP of 5.015 Billion USD by the middle of 2015. However, after the illegal dismissal of VP Sam-Sumana from office, the country's GDP came tumbling down from US$5 billion to US$3.7 billion. -

Sierra Leone 2017

SIERRA LEONE 2017 PERSPECTIVE FINANCE INFRASTRUCTURE AGRICULTURE TRADE & INDUSTRY MINING SOCIAL DEVELOPMENT TOURISM THE FUTURE OF FISHING Sierra Fishing Company is a vertically integrated seafood business that is already Sierra Leone’s largest supplier and exporter of fish. Now it is investing in an ambitious expansion of its fishing fleet, processing plants and storage Sierra Fishing Co. facilities in order to provide new Kissy Dockyard P.O. Box 1143 customers around the world with high- +232 (0)76 76 76 76 +232 (0)88 76 76 76 76 [email protected] quality sustainable seafood and value- www.sierrafishingcompany.com added products at a competitive price. CONTENTS 06 26 40 Ernest Bai Koroma, President of the Republic of FINANCE INFRASTRUCTURE Sierra Leone 28 A remarkable economic 42 Prioritising INTERVIEW recovery infrastructure to benefit the BRIEFING country and investors 30 Privatisation on the BRIEFING 10 horizon in the financial PUBLISHER: 45 The infrastructure SANTIAGO ORDIERES perspective sector opportunists IN-DEPTH IN-DEPTH ASSOCIATE PUBLISHER: 12 Forward-looking Sierra BARBARA CZARTORYSKA 32 Momodu L. Kargbo, 46 Mohamed Gento Leone bounces back with Minister of Finance and Kamara, CEO and Country ambitious plans HEAD OF INSTITUTIONAL Economic Development Director — Gento Group BRIEFING RELATIONS: INTERVIEW INTERVIEW SOPHIA SHEPODD 18 Victor Bockarie Foh, 35 Joseph S. Mans, Director 48 Leonard Balogun EDITOR: Vice-President of the General — National Social Koroma, Minister of SALLY CRAIL Republic of Sierra Leone Security -

Employment and Growth in Small-Scale Industry

EMPLOYMENT AND GROWTH IN SMALL-SCALE INDUSTRY Empirical Evidence and Policy Assessment from Sierra Leone Enyinna Chuta and Carl Liedholm St. Martin's Press New York @ International Labour Organisation 1985 To ourparents All rights ieserved. For information, write: St. Martin's Press, Inc., 175 Fifth Avenue, New York, NY 10010 Prin'ed in Hong Kong Published in the United Kingdom by The Macmillan Press First published Ltd. in the United States of America in 1985 ISBN 0-312-24458-4 Library of Congress Cataloging in Publication Data Chuta, Enyinna. Employmezt and growth in smal!-scale industry. Includes index. I. Small business--Sierra Leone. 2. Labor supply- Sierra Leone. I. Liedholm, Carl. II. Title. HD2346.S5C46 1985 338.6'42'09664 84-24771 ISBN G- 3 12-24458-4 Contents xi List of Tables xv List of Figures xv Foreword Preface 1 I INTRODUCTION Small-scale Industry PART I The Role of Rural and Urban in Employment Generation PROFILE OF SMALL-SCALE 2 DESCRIPTIVE 13 INDUSTRY IN SIERRA LEONE Sector 13 2.1 Overall Importance of the Small-scale Industry Relative Importance of Categories of Small-scale 2.2 17 Industry 22 2.3 Annual Output and Value-added 23 2.3.1 Seasonal Variations in Output 27 2.4 Material and Services Input and Stock Inputs 28 2.5 Capital Services 31 2.6 Initial Capital Stock Requirements 35 2.6.1 Sources of Initial Capital 37 2.6.2 Sources of Expansion Capital Excess Capacity 37 2.6.3 40 2.7 Labour Input 45 2.7.1 Characteristics of Apprentices 48 2.7.2 Characteristics of Proprietors 3 DETERMINANTS OF DEMAND FOR AND SUPPLY SMALL-SCALE