Understanding and Mitigating Synchronized Token Lifting and Spending in Mobile Payment

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Mobile Wallet Guide

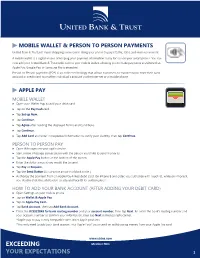

MOBILE WALLET & PERSON TO PERSON PAYMENTS United Bank & Trust just made shopping even easier! Using your phone to pay is faster, safer, and more convenient. A mobile wallet is a digital means of keeping your payment information ready for use on your smart-phone. You can now add your United Bank & Trust debit card to your mobile wallet, allowing you to make payments anywhere that Apple Pay, Google Pay, or Samsung Pay is accepted. Person-to-Person payments (P2P) is an online technology that allows customers to transfer funds from their bank account or credit card to another individual’s account via the Internet or a mobile phone. APPLE PAY MOBILE WALLET ▶ Open your Wallet App to add your debit card. ▶ Tap on the Pay Cash card. ▶ Tap Set up Now. ▶ Tap Continue. ▶ Tap Agree after reading the displayed Terms and Conditions. ▶ Tap Continue. ▶ Tap Add Card and enter in requested information to verify your identity, then tapContinue. PERSON TO PERSON PAY ▶ Open iMessages on your apple device. ▶ Start a new iMessage conversation with the person you’d like to send money to. ▶ Tap the Apple Pay button at the bottom of the screen. ▶ Enter the dollar amount you would like to send. ▶ Tap Pay or Request. ▶ Tap the Send Button (it is a white arrow in a black circle.) ▶ Authorize the payment from an Apple Pay-linked debit card. On iPhone 8 and older, you authorize with Touch ID, while on iPhone X, you double-click the side button to activate Face ID for authorization. HOW TO ADD YOUR BANK ACCOUNT (AFTER ADDING YOUR DEBIT CARD) ▶ Open Settings on your mobile phone. -

How Access Your Debit Card Using Apple, Google Or Samsung Pay

How Access your Debit Card using Apple, Google or Samsung Pay Apple Pay Open “Wallet” which is pre-installed on your phone. Tap the + button at the top-right of the screen to add one. If you don't have Touch ID setup yet, you'll be walked through registering your fingerprints. Next, use the camera viewfinder to scan in your card. Just center it in the frame and Apple Pay will grab all of the details, or you can enter them manually. Like with the other payment options, you'll need to verify your card using a text message or email code sent to you from your bank. Enter that and you're all set. To use Apple Pay while your phone is locked, just double tap the home button. It'll bring up your favorite debit or credit card, or you can select others at the bottom of the screen. Hold your finger to Touch ID as you tap the phone on an Apple Pay-approved reader. Google Pay Download Google Pay from the Google Play App Store. Open the app and tap "Add Credit or Debit card." You can choose cards already associated with your Google Account or add a new one. Agree to the terms and conditions that pop up. Then verify your card via email (you'll receive a number to enter into the app) That's it! Now, the next time you see a card reader with the Google Pay logo, just open the app, choose your card, and tap to pay. Samsung Pay Open up Samsung Pay, which should be pre-installed on your Samsung smartphone. -

Samsung Galaxy Note 5 N920R6 User Manual

SMART PHONE User Manual Please read this manual before operating your device and keep it for future reference. Legal Notices Warning: This product contains chemicals known to Disclaimer of Warranties; the State of California to cause cancer, birth defects, or other reproductive harm. For more information, Exclusion of Liability please call 1-800-SAMSUNG (726-7864). EXCEPT AS SET FORTH IN THE EXPRESS WARRANTY CONTAINED ON THE WARRANTY PAGE ENCLOSED WITH THE PRODUCT, THE Intellectual Property PURCHASER TAKES THE PRODUCT “AS IS”, AND All Intellectual Property, as defined below, owned SAMSUNG MAKES NO EXPRESS OR IMPLIED by or which is otherwise the property of Samsung WARRANTY OF ANY KIND WHATSOEVER WITH or its respective suppliers relating to the SAMSUNG RESPECT TO THE PRODUCT, INCLUDING BUT Phone, including but not limited to, accessories, NOT LIMITED TO THE MERCHANTABILITY OF THE parts, or software relating there to (the “Phone PRODUCT OR ITS FITNESS FOR ANY PARTICULAR System”), is proprietary to Samsung and protected PURPOSE OR USE; THE DESIGN, CONDITION OR under federal laws, state laws, and international QUALITY OF THE PRODUCT; THE PERFORMANCE treaty provisions. Intellectual Property includes, OF THE PRODUCT; THE WORKMANSHIP OF THE but is not limited to, inventions (patentable or PRODUCT OR THE COMPONENTS CONTAINED unpatentable), patents, trade secrets, copyrights, THEREIN; OR COMPLIANCE OF THE PRODUCT software, computer programs, and related WITH THE REQUIREMENTS OF ANY LAW, RULE, documentation and other works of authorship. You SPECIFICATION OR CONTRACT PERTAINING may not infringe or otherwise violate the rights THERETO. NOTHING CONTAINED IN THE secured by the Intellectual Property. Moreover, INSTRUCTION MANUAL SHALL BE CONSTRUED you agree that you will not (and will not attempt TO CREATE AN EXPRESS OR IMPLIED WARRANTY to) modify, prepare derivative works of, reverse OF ANY KIND WHATSOEVER WITH RESPECT TO engineer, decompile, disassemble, or otherwise THE PRODUCT. -

Mastercard with Samsung

MASTERCARD® WITH SAMSUNG PAY ISSUER FAQ 1. What has been announced? 6. How do consumers set up their MasterCard to make Samsung announced the official launch of its mobile payment payments with Samsung Pay? service, Samsung Pay, initially on the Samsung Galaxy S6 and Consumers will create a Samsung account and add a fi ngerprint and Samsung S6 edge, S6 edge+ and Galaxy Note5. Samsung Pay will backup PIN to the device Settings. They can use the phone’s camera broaden the reach for mobile payments at the POS and enable to scan the card information and then the account is secured with MasterCard® cardholders to use compatible Samsung devices for a fingerprint and backup PIN. Cardholders can load eligible Credit, everyday purchases, at both contactless (NFC) and magnetic stripe Debit, Prepaid, and Small Business cards that have been enabled on POS terminals in the U.S. MDES by participating Issuers for Samsung Pay. 2. When will Samsung Pay be available for consumers? 7. How does Samsung Pay address safety? The service is slated to be available in the U.S. on September 28, Safety features include tokenization and cryptogram validation via 2015, with a limited invitation-only Beta program prior. Samsung Pay MDES and cardholder validation via fingerprint authentication or is compatible with select cards and Samsung devices; see backup PIN. Samsung does not store or share any payment information www.samsung.com/pay for details. 8. Where can consumers use Samsung Pay? 3. What is MasterCard’s relationship with Samsung? Consumers can use Samsung Pay at merchants accepting contactless MasterCard is working with Samsung to deliver a seamless and payments as well as mag-stripe only terminals commonly deployed secure mobile payment experience at both contactless-enabled POS in-stores where a plastic card can be swiped. -

Samsung Galaxy GS9|GS9+ G960U|G965U User Manual

User manual Table of contents Features 1 Meet Bixby 1 Camera 1 Mobile continuity 1 Dark mode 1 Security 1 Expandable storage 1 Getting started 2 Galaxy S9 3 Galaxy S9+ 4 Assemble your device 5 Charge the battery 6 Start using your device 6 Use the Setup Wizard 6 Transfer data from an old device 7 Lock or unlock your device 8 Accounts 9 Set up voicemail 10 i UNL_G960U_G965U_EN_UM_TN_TA5_021820_FINAL Table of contents Navigation 11 Navigation bar 16 Customize your home screen 18 Bixby 26 Digital wellbeing and parental controls 27 Always On Display 28 Flexible security 29 Mobile continuity 33 Multi window 36 Edge screen 37 Enter text 44 Emergency mode 47 Apps 49 Using apps 50 Uninstall or disable apps 50 Search for apps 50 Sort apps 50 Create and use folders 51 Game Booster 51 ii Table of contents App settings 52 Samsung apps 54 Galaxy Essentials 54 Galaxy Store 54 Galaxy Wearable 54 Game Launcher 54 Samsung Health 55 Samsung Members 56 Samsung Notes 57 Samsung Pay 59 Smart Switch 60 SmartThings 61 Calculator 62 Calendar 63 Camera 65 Clock 71 Contacts 76 Email 81 Gallery 84 iii Table of contents Internet 90 Messages 93 My Files 95 Phone 97 Google apps 105 Chrome 105 Drive 105 Duo 105 Gmail 105 Google 105 Maps 106 Photos 106 Play Movies & TV 106 Play Music 106 Play Store 106 YouTube 106 Additional apps 107 Facebook 107 iv Table of contents Settings 108 Access Settings 109 Search for Settings 109 Connections 109 Wi-Fi 109 Bluetooth 111 Phone visibility 113 NFC and payment 113 Airplane mode 114 Data usage 114 Mobile hotspot 114 Tethering 116 -

What Is Samsung Pay?

Samsung Pay™ H A W A I I L A W Frequently Asked ENFORCEMENT FEDERAL CREDIT UNION Questions What is Samsung Pay? Samsung Pay is Samsung’s Mobile Wallet service that broadens the reach of mobile payments, by allowing HLEFCU MasterCard cardholders that enroll in the service to use compatible Samsung devices for everyday purchases at both contactless (NFC) and traditional magnetic stripe POS terminals. What devices are compatible with Samsung Pay? Samsung Pay is available to U.S. consumer on the Galaxy S6, Galaxy S6 edge, Galaxy S6 edge+, Galaxy S6 active, Galaxy Note5, and later devices. Galaxy S6, S6 edge, S6 edge+ and Note5 devices require the user to download an app to use Samsung Pay, while later devices will come preloaded with the required app. To download the app, visit the Google Play™ store. Is there a fee to use Samsung Pay? No, Samsung Pay is free; however, third party charges such as wireless carrier message and data rates may apply. Which HLEFCU cards will I be able to use with Samsung Pay? All HLEFCU Platinum MasterCard credit cards and MasterCard debit cards are available for use with Samsung Pay. How do I add my card to Samsung Pay? • Open the Samsung Pay app and, if you haven’t already done so, login to your Samsung account. • Touch Start to continue. • Then touch Use Fingerprint to assign your fingerprint as the verification method. If you do not already have your fingerprint on your device, you will be given a chance to add one at this time. • Create a Samsung Pay PIN and re-enter PIN to confirm. -

Payment Aspects of Financial Inclusion in the Fintech Era

Committee on Payments and Market Infrastructures World Bank Group Payment aspects of financial inclusion in the fintech era April 2020 This publication is available on the BIS website (www.bis.org). © Bank for International Settlements 2020. All rights reserved. Brief excerpts may be reproduced or translated provided the source is stated. ISBN 978-92-9259-345-2 (print) ISBN 978-92-9259-346-9 (online) Table of contents Foreword .................................................................................................................................................................... 1 Executive summary ................................................................................................................................................. 2 1. Introduction ....................................................................................................................................................... 4 2. Fintech developments of relevance to the payment aspects of financial inclusion ............. 6 2.1 New technologies ................................................................................................................................. 7 2.1.1 Application programming interfaces ......................................................................... 7 2.1.2 Big data analytics ............................................................................................................... 8 2.1.3 Biometric technologies ................................................................................................... -

Sustainable Development of a Mobile Payment Security Environment Using Fintech Solutions

sustainability Article Sustainable Development of a Mobile Payment Security Environment Using Fintech Solutions Yoonyoung Hwang 1, Sangwook Park 1,* and Nina Shin 2,* 1 School of Business, Seoul National University, Seoul 08826, Korea; [email protected] 2 School of Business, Sejong University, Seoul 05006, Korea * Correspondence: [email protected] (S.P.); [email protected] (N.S.) Abstract: Financial technology (fintech) services have come to differentiate themselves from tradi- tional financial services by offering unique, niche, and customized services. Mobile payment service (MPS) has emerged as the most crucial fintech service. While many studies have addressed the essential role of security when service providers and users choose to engage in financial transactions, the relationship between users distinct perceptions of security and MPS success determinants are yet to be examined. Thus, this study primarily aims to uncover the distinctive roles of platform and tech- nology security by investigating how users react differently to their varying understandings of the MPS usage environment. This study proposes a research model comprising two security dimensions (platform and technology) and three MPS success determinants (convenience, interoperability, and trust). We evaluated the proposed model empirically by using an online survey of 356 users. The survey accounts users experiences of the selected MPS. The results show that a security driven MPS can essentially enhance or deteriorate users positive perceptions of MPS success determinants while they use it for financial transactions. To further understand how this recent trend of user perception of security affects the overall MPS usage experience, this study provides theoretical insights into the roles of platform and technology securities. -

Alipay – the Main Silent Com- Petitor for Digital Payment Solutions

ALIPAY – THE MAIN SILENT COM- PETITOR FOR DIGITAL PAYMENT SOLUTIONS Fabian Meyer Artur Burgardt 23. Dezember 2016 COREtechmonitor | Blogpost Copyright © CORE GmbH http://www.coretechmonitor.com Key Facts AliPay, which currently has 450 million customers, processes 34% of the total billing volume of 860 billion Dollars outside China To respond effectively to Chinese tourists in Europe, a push has been made to increase the number of sales points in Europe that accept AliPay through partnerships with Wirecard (February 2016), Concardis (June 2016), Ingenico (August 2016) and SIX (De- cember 2016) AliPay has the potential to become a significant threat to the customer interface, cur- rently provided through banks and underlying earnings, without actively being noticed. Report middle class, and the ensuing exponential in- crease in this group’s readiness to travel, has Changing customer needs, the liberaliza- led to positive growth in payments outside tion of regulations, and the related digitali- the country to the tune of 292 billion Dollars. zation of the payment market are having an This means that ~34% of AliPay’s total trans- ever greater effect, as seen in the propor- action volume is already processed abroad, tional increase in the use of mobile pay- and this is acting as a catalyst for expansion ment methods. This being the case, it is ex- on the European market. pected that the global customer base will have increased by ~51%, and the volume The constantly growing number of sales of transactions by ~85% by the end of points that -

Analysys Mason Document

Apple and Samsung’s mobile payment success against Internet players in China depends on regulatory change April 2016 Enrique Velasco-Castillo Apple launched its Apple Pay mobile payment service in mainland China in February 2016, followed a few weeks later by the launch of Samsung Pay. This article explores Apple and Samsung’s potential for success, given the growing dominance of ChinaUnion Pay (CUP), and how changes in regulation may enable operators in the region to tackle changes in China’s mobile payments competitive landscape by adopting a broader array of digital services to increase growth in mobile commerce.1 Apple faces strong competition from entrenched local players like Alibaba and Tencent in China Mainland China is one of the few markets in the world where mobile payments replace, rather than complement, many traditional financial services, and for this reason the Chinese mobile payments market has reached critical mass in terms of user adoption and payments acceptance. The market is dominated by over-the-top (OTT) and e-commerce players, such as Alibaba (which operates Alipay through its subsidiary Ant Financial Services) and Tencent (WeChat Pay and QQ Wallet). WeChat’s success has been based on first driving user engagement using messaging, stickers and other social features and then increasing users’ adoption of payments and ecommerce facilities, such as person-to-person (P2P), bill or in- store payments. Alipay dominates because of Alibaba’s position as China’s largest ecommerce player, as well as its attractive features, such as interest-bearing deposits and free transfers to any bank account. For these companies, payments complement a wider range of value-added features that keep users highly engaged with their platforms. -

QR Code Merchant Payments

1 QR Code Merchant Payments A growth opportunity for mobile money providers In partnership with The GSMA represents the interests of Accourt is a specialist, IP-led global NTT DATA is a leading IT services mobile operators worldwide, uniting payments consultancy, providing strategic provider and global innovation partner AUTHORS more than 750 operators with nearly and operational payments consultancy headquartered in Tokyo, with business 400 companies in the broader mobile services worldwide. Its consultants are operations in over 50 countries. Our ecosystem, including handset and device experienced practitioners with front line emphasis is on long-term commitment, GSMA makers, software companies, equipment P&L experience, combining unrivalled combining global reach with local intimacy Anant Nautiyal, Senior Manager, providers and internet companies, as strategic expertise with operational to provide premier professional services Inclusive Tech Lab well as organisations in adjacent industry know-how. From defining and setting varying from consulting and systems Bart-Jan Pors, Director, sectors. The GSMA also produces the strategy, implementation, through to final development to outsourcing. Inclusive Fintech Mobile Money industry-leading MWC events held annually delivery, Accourt is dedicated to minimising Bruno Martins, Technology Lead, in Barcelona, Los Angeles and Shanghai, operational risk and ensuring a successful For more information, visit Inclusive Tech Lab as well as the Mobile 360 Series of regional outcome for its clients. -

Qr Code Payments Landscape

THE QR CODE PAYMENTS LANDSCAPE A LEVEL ONE PROJECT PERSPECTIVE OCTOBER 2019 THE LEVEL ONE PROJECT IS AN INITIATVE OF THE BILL AND MELINDA GATES FOUNDATION GLENBROOK PARTNERS This is A lAndscApe review of QR For this report we looked At the following CONTENTS PayMents Models Around the world, with MArket developments: an emphasis on developments in • SingApore SGQR emerging economies. • IndonesiA QRIS In this report, we describe the vArious • IndiA BhArAtQR and BHIM QR models, with pArticulAr Attention to how QR code iMpleMentAtions connect with • ThAilAnd StAndArdized QR Code the underlying pAyMents systeMs used • AlipAy w/ Europe WAllet Providers to process the pAyMents. • Mexico CoDi We Also Assess how the vArious Models • ChinA AlipAy are aligned with the Level One Project design principles and key concepts. • South AfricA SnApScAn • AsiA GrAbPAy This docuMent is A continuAtion of prior reseArch done for the Level One Project. The 2017 report “Research on QR Code-Based PayMents And its ApplicAtion in Emerging Markets”, which provides A detAiled history on how QR codes were introduced, cAn be downloaded from leveloneproject.org. 2 Glenbrook for Bill And MelindA Gates FoundAtion CONTENTS 5 INTRODUCTION 11 QR CODE MARKET MODELS 29 MARKET LANDSCAPE 48 FRAUD MANAGEMENT 57 FUTURE DIRECTIONS 62 LEVEL ONE ALIGNMENT 72 APPENDIX: QR CODE DATA FORMATS 3 Glenbrook for Bill And MelindA Gates FoundAtion Executive Summary QR Codes used for mercHAnt pAyments Are gAining rApid trAction worldwide. THese pAyments in generAl support Level One goals of growing the digitAl ecosystem: those tHAt work in conjunction with interoperAble payments systems are particularly well-aligned.