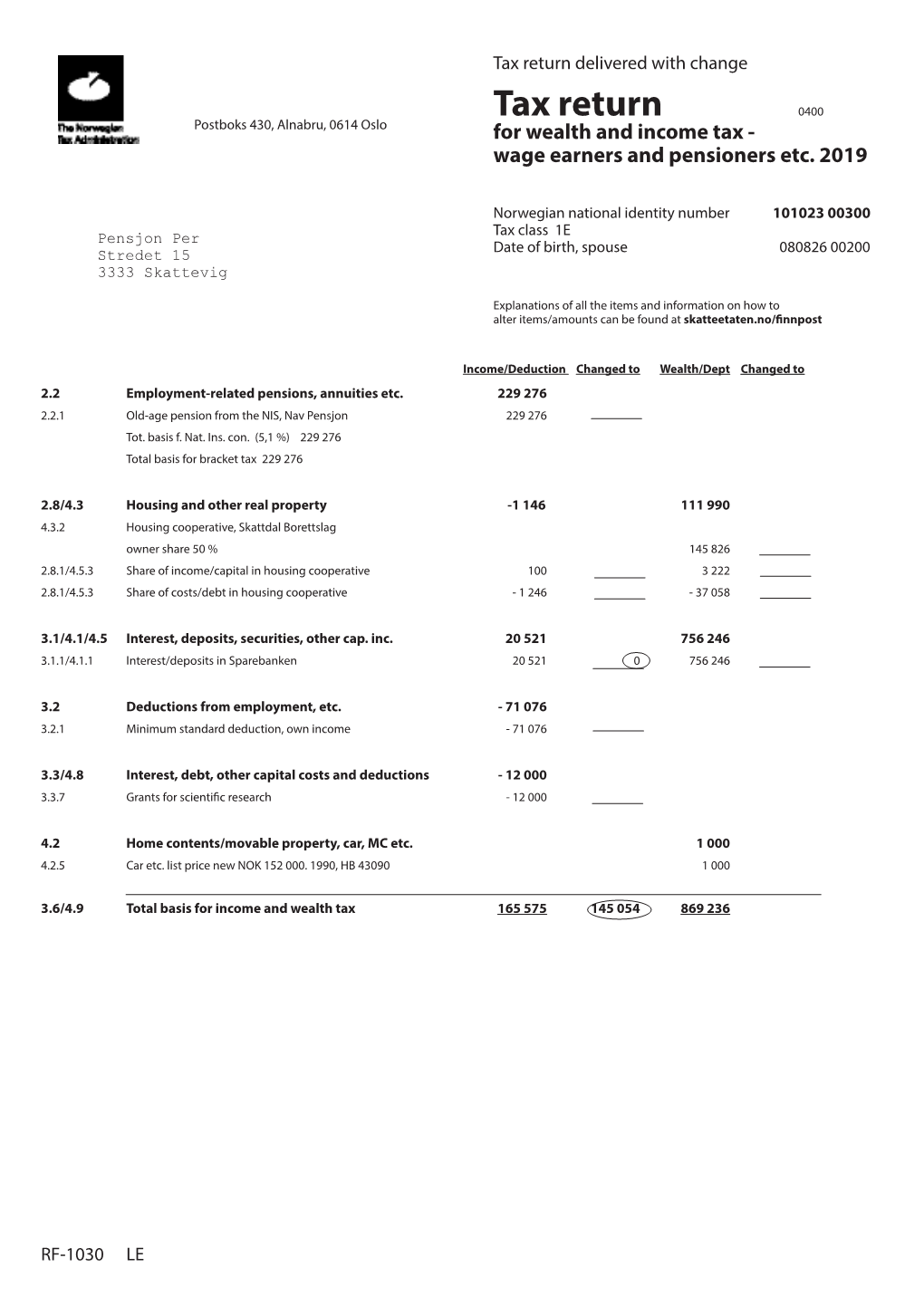

Tax Return Delivered with Change

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Taxation of Partnerships - Legal General Report for the Nordic Tax Research Council´S Annual Meeting on 22 May 2015 in Aarhus

Nordic Tax J. 2015 2:47–56 Report Open Access Liselotte Madsen Taxation of Partnerships - Legal general report for the Nordic Tax Research Council´s annual meeting on 22 May 2015 in Aarhus DOI 10.1515/ntaxj-2015-0005 though the similar Norwegian word is “utdeling”, and so Received Sep 08, 2015; accepted Sep 18, 2015 on. In English translation, the word “distribution” is used. I hope that it does not provide any linguistic challenges. The term partnership is used to the extent that it is not found necessary to indicate the national name, and ex- 1 Introduction and terminology presses only that it is a transparent business. First, a short review of the company law rules regard- This report has been written on the basis of a number of ing the establishment of partnerships will be carried out, Nordic national reports on the subject: Taxation of part- after which, the tax rules will be reviewed. nerships. The contributions from Denmark, Norway, Swe- den, and Iceland have been incorporated in the report to the best of my ability and by relevance. 2 Company law matters The term "partnership" is a general term for a num- ber of companies that have a common characteristic - First, it is relevant to relate to the company law rules ap- namely that they are not taxable entities, but rather trans- plicable to partnerships. A description of this has been parent for tax purposes. The company type, partnership, deemed important for the understanding of the civil law which is not a separate tax subject, can be found in all rules for partnerships, both in relation to the third parties the Nordic countries. -

Workshops No. 6/2005 165 the Future of the Corporate Taxation

√ Oesterreichische Nationalbank Stability and Security. Workshops Proceedings of OeNB Workshops Capital Taxation after EU Enlargement January 21, 2005 No. Eurosystem 6 The Future of the Corporate Income Taxation in the European Union Sijbren Cnossen University of Maastricht A. Introduction The future of capital income taxation in the European Union (EU) hinges importantly on the future of the corporation tax. No doubt, schedular capital (income) taxes on real estate and the earnings of small-businesses will be around for a long time to come, but the base of a comprehensive capital income tax requires the inclusion of corporate earnings, i.e. profits, interest and royalties. Capital income taxation, broadly defined, will wither if the body politic does not want to tax corporate earnings, either deliberately or by ignoring the policy and administrative issues that arise in a globalised capital market. Accordingly, this paper focuses mainly on corporation tax (CT) regimes. The future of the corporation tax starts now. Therefore, Part B surveys and evaluates the actual CT regimes in the EU to see whether they yield any clues about what the future may hold in store. The survey starts with an analysis of corporation-income tax relationships in the Member States centered on the treatment of distributed and retained profits. Subsequently, there is a comparison between nominal tax rates on various forms of capital income (retained profits, dividends, interest) and labor income. This is followed by a review of the most important tax base features, including the use of tax incentives. Finally, there is a discussion of a number of technical aspects that bear on the enforcement of the taxation of corporate earnings. -

The Double Taxation Relief NORWAY Order 1969

Supplement to the "Trinidad and Tobago Gazette" Vol. 8, No. 130 - 25th December, 1969 GOVERNMENT NOTICE NO. 175 TRINIDAD AND TOBAGO THE INCOME TAX ORDINANCE, CH. 33 No.1 ORDER MADE BY THE GOVERNOR-GENERAL UNDER SECTION 47(1) OF THE INCOME TAX ORDINANCE, AS ENACTED BY SECTION 32 OF THE FINANCE ACT, 1966 THE DOUBLE TAXATION RELIEF (NORWAY) ORDER, 1969 WHEREAS it is provided by subsection (1) of section 47 of the Income Tax Ordinance that if the Governor-General by Order published in the Gazette declares that arrangements specified in the Order have been made with the Government of any country with a view to affording relief from double taxation in relation to income tax and any tax of a similar character imposed by the laws of that country, and that it is expedient that those arrangements shall have effect: And whereas by a Convention dated the 20th day of June, 1969, made between the Government of Trinidad and Tobago and the Government of Norway, arrangements were made inter alia for the avoidance of double taxation: Now, therefore, the Governor-General in pursuance of the said subsection (1) of section 47 of the Income Tax Ordinance is please to order, and it is hereby ordered as follows:- 1. This Order may be cited as the Double Taxation Relief (Norway) Order, 1969. 2. It is hereby declared- 1 (a) that the arrangements specified in the Schedule have been made with the Government of Norway; (b) that it is expedient that those arrangements should have effect. SCHEDULE CONVENTION BETWEEN THE GOVERNMENT OF TRINIDAD AND TOBAGO AND THE GOVERNMENT -

Taxation and Investment in Norway 2016 Reach, Relevance and Reliability

Taxation and Investment in Norway 2016 Reach, relevance and reliability A publication of Deloitte Touche Tohmatsu Limited Contents 1.0 Investment climate 1.1 Business environment 1.2 Currency 1.3 Banking and financing 1.4 Foreign investment 1.5 Tax incentives 1.6 Exchange controls 1.7 Labor environment 2.0 Setting up a business 2.1 Principal forms of business entity 2.2 Regulation of business 2.3 Accounting, filing and auditing filing requirements 3.0 Business taxation 3.1 Overview 3.2 Residence 3.3 Taxable income and rates 3.4 Capital gains taxation 3.5 Double taxation relief 3.6 Anti-avoidance rules 3.7 Administration 3.8 Other taxes on business 4.0 Withholding taxes 4.1 Dividends 4.2 Interest 4.3 Royalties 4.4 Branch remittance tax 4.5 Wage tax/social security contributions 5.0 Indirect taxes 5.1 Value added tax 5.2 Capital tax 5.3 Real estate tax 5.4 Transfer tax 5.5 Stamp duty 5.6 Customs and excise duties 5.7 Environmental taxes 5.8 Other taxes 6.0 Taxes on individuals 6.1 Residence 6.2 Taxable income and rates 6.3 Inheritance and gift tax 6.4 Net wealth tax 6.5 Real property tax 6.6 Social security contributions 6.7 Other taxes 6.8 Compliance 7.0 Deloitte International Tax Source 8.0 Contact us Norway Taxation and Investment 2016 1.0 Investment climate 1.1 Business environment Norway is a constitutional monarchy, with a parliamentary democratic system of government. Powers are allocated among the executive, the legislature (Storting) and the court system. -

Statoil Asa Terms and Conditions of the Dividend Issue Under the Two Year

ISIN: NO 0010096985 Trading Symbol: STL 26 May 2017 STATOIL ASA TERMS AND CONDITIONS OF THE DIVIDEND ISSUE UNDER THE TWO YEAR SCRIP DIVIDEND PROGRAMME FOURTH QUARTER 2016 This document sets forth the terms and conditions (the "Terms and Conditions") relating to the subscription of new shares (the "Dividend Shares") of Statoil ASA ("Statoil" or the "Company"), each with a nominal value of NOK 2.50 (the "Dividend Issue") in connection with payment of the dividend of USD 0.2201 (NOK 1.8784) for the fourth quarter 2016 under the two year scrip dividend programme (the "Scrip Dividend Programme") approved by the general meeting of the Company on 11 May 2017. IMPORTANT INFORMATION Shareholders are urged to carefully read the information set forth under Section 15 "Selling and Transfer Restrictions". 1 THE DIVIDEND ISSUE On 11 May 2017, the general meeting of Statoil resolved to distribute a Dividend of USD 0.2201 (NOK 1.8784) per share for the fourth quarter 2016 (the “Dividend”) to the holders of the Company's shares (the "Shares") as of expiry of 10 May 2017 for holders of American Depositary Receipts (“ADRs”) on the New York Stock Exchange ("ADR Holders") and 11 May 2017 for shareholders on the Oslo Stock Exchange (together the "Existing Shareholders"), as registered with Deutsche Bank Trust Company Americas as the depositary for the ADRs and the Company’s shareholder register with the Norwegian Central Securities Depositary (Nw. Verdipapirsentralen) (the "VPS") as of expiry of 15 May 2017 (the "Record Date"), respectively. Existing Shareholders whose shares trade on the Oslo Stock Exchange will receive their Dividend in NOK. -

Economic Policy Caliph Umar Ibn Khattab

Munich Personal RePEc Archive Economic Policy caliph Umar ibn Khattab Kusnadi, Jamaludin Fakultas Syariah dan Ekonomi Islam IAIN Syekh Nurjati Cirebon 7 July 2018 Online at https://mpra.ub.uni-muenchen.de/87819/ MPRA Paper No. 87819, posted 11 Jul 2018 15:58 UTC ECONOMIC POLICY Caliph Umar Ibn Khattab Jamaludin Kusnadi EKOS 1 [email protected] Sejarah Pemikiran Ekonomi Islam Dr.H. Aan Jaelani, M.Ag Abstract Umar bin Khattab was a close friend of the Prophet Muhammad that did policies in Islamic economy, especially macroeconomy, and found wisdom way to manage property (country wealth) and made people benefit with three ways, first: take the right way, second: given in accordance with their rights, and third; avoid from bad. It showed that management of Umar bin Khattab was neat in the country took financial management policy, the country will not take people property in wrong way.1 Keywords ombudsmen, diwan, kharaj, public finance, Umar bin Khattab Jel A.11, .00, B11, B31 Background Umar bin Khattab, who earned his first commander of the faithful. At the time of Umar bin Khattab's Muslims are experiencing rapid success and ekomoninya already very advanced as booty or spoils of war is not a form of armor, but land is a vast country the Roman state. Dr.Abdul according to Ibrahim Al-Kaylan (2008)2 Omar bin Khattab confronts the problems of the State in the economy and make it a goal of an independent state. Dr.Mustofa Faydah explains in his book ta'sis Umar bin Khattab (1418H / 1997M)3 said that Zama Umar (13-23H / 634-644M) conquered most countries after the Prophet died. -

Publications 56 Economic Research Local Public Sector in Transition: a Nordic Perspective

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by National Library of Finland DSpace Services Government Institute for Publications 56 Economic Research Local public sector in transition: A Nordic perspective Antti Moisio (Ed.) Publications 56 October 2010 VATT PUBLICATIONS 56 Local public sector in transition: A Nordic perspective Antti Moisio (Ed.) Valtion taloudellinen tutkimuskeskus Government Institute for Economic Research Helsinki 2010 ISBN 978-951-561-937-2 (nid.) ISBN 978-951-561-938-9 (PDF) ISSN 0788-4990 (nid.) ISSN 1795-3332 (PDF) VATT Valtion taloudellinen tutkimuskeskus Government Institute for Economic Research Arkadiankatu 7, 00100 Helsinki, Finland Oy Nord Print Ab Helsinki, October 2010 Graphic design: Niilas Nordenswan Authors Jens Blom-Hansen Aarhus University Lars-Erik Borge Norwegian University of Science and Technology Claire Charbit OECD Matz Dahlberg Uppsala University Heikki A. Loikkanen University of Helsinki and VATT Antti Moisio Government Institute for Economic Research (VATT) Lasse Oulasvirta University of Tampere Anwar Shah World Bank Camila Vammalle OECD Preface and acknowledgement This book is intended to serve as a resource for those who want to understand the recent reforms of local government organisation, tasks and funding in Finland, Denmark, Norway and Sweden. A special focus of the book is on Finnish local government and how the present Finnish situation compares with developments in other countries. However, this book also offers a more general view of local government reforms and in the way that fiscal federalism has been affected by the global fiscal crisis. The articles in this book are written by researchers who are all acknowledged academic experts in local public finance and local governance. -

Islamic Radicalization in Norway: Preventative Actions

ISLAMIC RADICALIZATION IN NORWAY: PREVENTATIVE ACTIONS Tuva Julie Engebrethsen Smith (Research Assistant, ICT) Spring 2015 ABSTRACT The purpose of this paper is to analyse the process of radicalization of Muslims in Norway. The paper begins by outlining the Muslim population, demographics, mosques, organizations, as well as political participation. The paper further presents a theoretical approach to radicalization while looking at the issue of radicalization in Norway. After this section, follows some case studies of Norwegian foreign fighters in Syria and supporters of terrorist attacks in Africa. At last, the government´s response to radicalization in Norway is outlined, with a following conclusion that explains the increase of among Norway´s population. The views expressed in this publication are solely those of the author(s) and do not necessarily reflect the views of the International Institute for Counter-Terrorism (ICT) TABLE OF CONTENTS INTRODUCTION 3 PART 1: DEMOGRAPHY 5 Religion and Norway 5 Education 6 Socio-economic Conditions 7 Statistics Muslim Presence Norway 9 Muslim Community in Norway 11 Native Norwegians, Media, and Opposition to Muslims 11 Political Participation 15 Mosques and Islamic Centers 17 Central Jamaat Ahle Sunnat (CJAS) 17 Tawfiiq Islamic Center (TIC) 19 Islamic Cultural Centre (ICC) 20 Idara Minhaj ul-Quran (IMQ) 21 Organizations 22 The Prophet´s Ummah 22 Islam Net 25 PART 2: RADICALIZATION IN NORWAY 27 Theoretical Approach to Radicalization 27 Causes of Radicalization 28 Social Movement Theory 29 Radicalization -

Guide to the Norwegian Tax Administration Content Introduction

Guide to the Norwegian Tax Administration Content Introduction Introduction page 1 In this booklet you will find infor- The Norwegian tax Administration page 4 mation on how the Tax Population registration page 8 Administration is organized and Tax and assessment page 8 on its most important spheres of Appeal boards and right of appeal page 9 responsibility. VAT page 10 Inheritance tax page 11 Collectiom of Vat page 11 Glossary page 12 Important dates in the history of taxation page 14 Introduction page 1 2 3 Ministry of Finance Directorate of Taxes Directorate of Taxes Director General of taxation Stab: •Information Unit •Internal Audit Unit •Unit for Analysis of Developments in Law •Unit for Compliance and E conomic Cr ime Director of Division Office of the Director Assessment Collection Division Division Departmen t of Departmen t of Personal Taxation Departmen t of Departmen t Departmen t IT- Planning and and Popula tion Business Taxation of Collec tion of Organiza tional Departmen t Dev elopment Registration Services Cou nty tax Petroleum Cou nty tax assessment offic es Tax Office Col lection offices Central Tax Office for Large Enterprises Local tax assessment offic es Central Office for Local Tax For eign Tax Affairs collection offices Oslo Tax Assessment O ffice The Norwegian Tax Administration The overall goal of the Tax tax limitation, tax deductions, assessment appeal board. Administration is to ensure that rates for late delivery penalties, The local tax assessment office is taxes are correctly assessed and rates and basis for any additio- responsible for population regi- collected. At the same time, the nal tax, etc. -

Norwegian Taxation of Individuals and Goods Upon Cross Border Mobility A

Norwegian taxation of individuals and goods upon cross border mobility Attorney Ann Johnsen, Advokatfirmaet Hjort DA The main objective of the Norwegian taxation rules is to raise revenue to the Norwegian public sector. One of many underlying aims of the rules is to avoid double taxation and non-taxation in cross border situations. The relatively high tax level in Norway creates certain tax incentives, thus the legislation also has to secure the Norwegian tax base. This consideration may lead to double taxation, e.g. on imported motor vehicles, see item B.2.1.2.2. On the other hand, the legislation creates obvious situations of non-taxation, e.g. the opportunity to tax free import, see item B.2.1.2.1. In certain situations migrant workers may get advantages compared to sedentary workers, see item A.1.2.2. A TAXATION OF INDIVIDUALS A.1 Income taxes A.1.1 Tax liability A.1.1.1 Under which conditions are non-resident workers liable to tax? A.1.1.1.1 Domestic law According to the Tax Act1 Section 2-3 (1) (d) a person staying temporary in Norway working as an employee is liable to tax to Norway on remuneration which derives from sources here. In this context, there is a Norwegian source if the labour is performed for an employer who is liable to tax to Norway. Non-resident employees who are placed at the disposal of others to carry out work in Norway (hiring in of labour) are liable to tax on income from such work, cf. -

The Decisive Moment(S Or Periods) in the Application of Income Tax Rules and the Importance

http://www.diva-portal.org This is the published version of a paper published in Nordic Tax Journal. Citation for the original published paper (version of record): Kellgren, J., Furuseth, E., Kukkonen, M. (2019) The Decisive Moment(s or periods) in the Application of Income Tax Rules and the Importance of Events Thereafter: – a Swedish, Norwegian and Finnish Perspective and Comparison Nordic Tax Journal, (1): 41-55 https://doi.org/10.1515/ntaxj-2019-0003 Access to the published version may require subscription. N.B. When citing this work, cite the original published paper. Permanent link to this version: http://urn.kb.se/resolve?urn=urn:nbn:se:oru:diva-79301 Nordic Tax J. 2019; 1:41–55 Article Jan Kellgren*, Eivind Furuseth, and Matti Kukkonen The Decisive Moment(s or periods) in the Application of Income Tax Rules and the Importance of Events Thereafter – a Swedish, Norwegian and Finnish Perspective and Comparison https://doi.org/10.1515/ntaxj-2019-0003 These circumstances have a history and a future, Received Sep 10, 2018; accepted Oct 28, 2018 which may be of relevance for the assessment of the event or relationship to which the legal rules relate. However, it Abstract: For a correct application of tax laws, it is cen- is usually insignificant if, for example, an asset’s value was tral to know at what time or period the conditions of each higher or lower before this decisive point in time. The rules, case are to be tested against the respective tax rule. For as mentioned, aim at the conditions at a certain time or pe- example, in many questions, the conditions at the time of riod, hereinafter referred to as the decisive moment. -

Mandate and Summary

Official Norwegian Report (NOU) 2014:13 1 Capital Taxation in an International Economy Chapter 1 Chapter 1 Mandate and summary 1.1 Mandate On 15 March 2013, the Stoltenberg II Government appointed a commission to review corporate taxation in Norway in light of international developments. The Commission was given the following mandate: “Background Supporting the production capacity of the mainland economy is important. A broad range of meas- ures must be employed to improve competitiveness and ensure the efficient use of resources. Norway has found that tax reforms can have a positive effect on the economy. Tax-system design and robust- ness play an important role. The closer integration of markets as a result of globalisation has motivated various countries to amend their tax rules. Internationally, there is a trend towards combining lower corporate tax rates with measures to prevent undesirable cross-border tax planning. The purpose of this review is to ensure that Norway maintains a robust tax system that is better equipped to deal with the international mobility of tax bases. The tax system must also contribute to the future financing of the welfare system and make it attractive to invest and create jobs in Norway. The emphasis of the 1992 tax reform was on equal tax treatment, broad tax bases and low rates, with a particular focus on corporate and capital taxation. These guiding principles were also followed in the 2006 tax reform. The theoretical foundation and close integration of different parts of the tax system have produced a robust, stable tax system and reduced tax-adjustment incentives.