The Knowledge Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Handbook for International Students

Handbook For Internatonal Students Natonal Insttute of Development Administraton (NIDA) Welcome Letter. Dear Internatonal Students and Scholars, Welcome to Natonal Insttute of Development Administraton (NIDA). You are about to begin a journey into your future. At NIDA we understand there are many unknowns ahead. Therefore, we are here to guide, assist and help you discover your path together with our warm support throughout your journey. NIDA ofers a quality and intellectually rigorous educatonal experience. I am more than certain that the experience you will receive from NIDA will exceed your expectaton. NIDA provides many programs and actvites (academic and non- academic) that help you grow as a true leader and gain crucial skills for today’s job market. We help prepare you for greatness. More importantly, we are aware that many students concern and worry about being on their own in this country, that is why we (both faculty members and staf) care about each one of you and will show our support and assist you in any ways that we can to make you feel like “Home” “We are part of you and you are a big part of us”, that is why the Ofce of Internatonal Afairs (OIA) at NIDA stands ready to be your second home with a warm hospitality and help you throughout out your new journey. Our goal is to see you successfully achieve your academic and personal goals. This handbook was designed and created with a lot of atenton and care. We hope that it can be your guide to the life in campus and surrounding areas. -

Shopping in Thailand

Siam International Legal Group | Thailand´s Largest Legal Network Service Shopping in Thailand Thailand, particularly Bangkok, is definitely a paradise for all shopaholics.The massive, modern, multi-storey shopping malls provide a myriad of choices for every budget and need. The only problem you must face is deciding where to go first because of the infinite shopping possibilities! But with a map and a dose of style-savvy, you are good to go! Thailand is renowned all over the world for its beautiful silk, jewelry and original exquisite handicrafts. It is also known for producing first-class fake goods. From the most luxurious to the cheapest—clothing, shoes, bags, apparels, jewelry, to branded luxury goods and even electronic devices such as mobile phones and laptop computers, you can find almost anything of your fancy here. In Bangkok, you can choose among a wide variety of Shopping malls and open-air markets. Like other big cities, shopping malls & department stores are places where you can but high quality products. Though there are also some shops and stalls in shopping centers where you can haggle for the discounted price, bargain hunters will be enjoying shopping in Thai markets for the most affordable goods. Shopping malls like Gaysorn, Siam Paragon, & Emporium are popular for tourists looking for international brands and world’s top quality designer wear. They are mostly open from 10am-10pm daily. These shopping centers are very accessible via (BTS), the city’s most efficient modern sky train. GAYSORN Business Hours: 10:00 - 20:00 Location: Ratchaprasong Junction BTS: Chitlom SIAM PARAGON Business Hours: 10:00 - 22:00 Location: Next to Siam Centre, Pathumwan BTS: Siam Tip: Tourist can apply for a ‘Tourist Discount Card’ on the information desk for a 5% discount on most purchases. -

TOD Factors Influencing Urban Railway Ridership in Bangkok

TOD Factors Influencing Urban Railway Ridership in Bangkok Varameth Vichiensan Nattapon Suk-kaew Masanobu Kii Department of Civil Engineering Mass Rapid Transit Authority Faculty of Engineering and Design Kasetsart University of Thailand Kagawa University Bangkok, Thailand Bangkok, Thailand Takamatsu, Japan [email protected] [email protected] [email protected] Yoshitsugu Hayashi Center for Sustainable Development and Global Smart City Chubu University, Aichi, Japan [email protected] Abstract— Currently, three urban railway system are A. Urban Development running in Bangkok Metropolitan Region - Bangkok Transit The city of Bangkok was established on the right bank of System (BTS) Bangkok Mass Rapid Transit (MRT) and Airport the Chao Phraya River in 1782 with a territory of 3.5 km2 and Rail Link (ARL). However, the development pattern in the area population of about 50,000. The city has built canals for around train stations are different. This paper presents a cluster analysis of urban railway stations in Bangkok that has influence communication and security functions. Since then people have railway ridership. The cluster analysis shows that transit station been attracted to reside along the waterway network. classification can be classified into three clusters – high-density Population has been continuously increasing with migrants commercial areas, high-density residential areas (most are in from countryside and foreign countries. The city has dense residential areas and close to economic areas) and continuously expanded to the west side of Chao Phraya river, medium-density commercial and residential areas (most are in so-called Thonburi side. The city has expanded to the north, moderate and low residential areas). -

A Guide to Health & Wellness Holidays in Thailand

HEALING HARMONY A Guide to Health & W ellness Holidays in T hailand HEALING HARMONY A Guide to Health & Wellness Holidays in Thailand Chiva-Som International Health Resort CREDITS Published by born Distinction Co., Ltd. 2044/20 New Petchburi Road, Bangkapi, Huay Kwang, Bangkok 10310 Thailand www.borndistinction.com Working Team for This Book Editor in Chief: Nuengnimmarn Na Nakorn Project Director: Jidapa Julakasilp Project Manager: Wanida Tirapas Advisor: Dr. Prapa Wongphaet, Dr. Anthony Perillo, Todd A. Nagle Content Editor: Jeff Petry, Todd A. Nagle, Jeremy Kempler-Johanson Proofreader: James Haft, Bonita Rose-Aimee Kennedy, Susanne Robinson Designer: Chira CH., J. Janjaturonrasamee, Asana Yuman Illustrations Assistant: Sasithorn Namamaka Editorial Assistant: Manatsawee Ketudat, Nipattra Weerathong, Santi Ngamlert, Kanyapak Chaipun, Sawarin Siriyong, Researcher: Sansanee Khurana, Panhathai Khaosawee Copyright © 2011 born Distinction Co., Ltd. All rights reserved. Reproduction in whole or in part by any means without prior written permission by the publisher is strictly prohibited. Printed in Bangkok, Thailand Healing Harmony: A Guide to Health and Wellness Holidays in Thailand ISBN: 978-616-90997-1-0 Chiva-Som International Health Resort MESSAGE FROM PUBLISHER It’s proven that smiling relieves stress, eases anxiety, boosts the immune system and lowers blood pressure, as well as releasing natural biological chemicals within our bodies that help reduce pain while boosting our mood and increasing happiness. The stress- free environment of our ‘Land of Smiles’ is the perfect place to not only recuperate from procedures, but also achieve better results through faster healing processes. Not only can you find a multitude of medical/wellness solutions in major cities such as Bangkok, Phuket and Pattaya, but also throughout the country with therapies available in smaller cities like Chiang Rai, or island paradises like Koh Chang. -

VIE Hotel Bangkok, Mgallery by Sof Itel

VIE Hotel Bangkok, MGallery by Sof itel is a modern and elegant 5-star luxury designed hotel, conveniently located in the heart of the city, only a few steps from the BTS Skytrain Ratchathewi station and easy travel throughout the city. A five minutes’ walk brings you to the city’s most famous shopping centres, such as Siam Discovery, MBK, Siam Center and Siam Paragon. VIE LITE MEETING PACKAGE: THB 4,999++ per room per night Book by 31st August for a meeting scheduled from now until 31st October 2019 Promo Code: VIELITE Package Inclusions: • Full-day meeting package (free flow coffee and/or tea, two coffee breaks and one lunch) • 1-night stay in a Deluxe Room with breakfast and high-speed Wi-Fi internet throughout the property *THB 300++ for an extra person/THB 1,200++ for extra bed with breakfast *THB 1,300++ for full-day meeting package for non-residential guests **THB 3,800++ for extended night stay (with breakfast for one) VIE Super Meeting Package: THB 5,999++ per room per night Book by 31st August for a meeting scheduled from now until 31st October 2019 Promo Code: VIESUPER Package Inclusions: • Full-day meeting package (free flow coffee and/or tea, two coffee breaks and one lunch) • 1-night stay in a Deluxe Suite with breakfast and high-speed Wi-Fi internet throughout the property • Reception cocktail dinner with free flow soft drinks at the Piano Bar *THB 300++ for an extra person/THB 1,200++ for extra bed with breakfast *THB 1,300++ for full-day meeting package for non-residential guests **THB 4,800++ for extended night stay (Breakfast for one) Terms and conditions: • Book by 31st August for a meeting scheduled from now until 31st October 2019 • Rates are subject to of 10% service charge and 7% government tax. -

Thailand – Bangkok 泰國– 曼谷

Thailand – Bangkok 泰國 – 曼谷 Days Nights OMR- 1801095-V4 3 日 2 晚 from up HK$2,230 Valid For Departure On 06Arp-31Oct18 於 5 月 31 日前訂購 4 月 23 日至 7 月 8 日出 發之套票,每位可享 1 張 Rabbit Card (價值 THB120)。 數量有限,先到先得 Adult Extension / room / night Hotel Room Type B’fast Stay Period 成人 (HK$) 延長續住每房每晚 (HK$) 酒店 房間類型 早餐 住宿日期 Half Twin Single Extra Bed Single / Twin Extra Bed 佔半房 單人房 加床 單人房 / 雙人房 加床 (5) Aetas Bangkok Superior 2,500 3,240 815 06Apr-31Oct18 2,370 320 Valid for Asian market, except Thailand Deluxe 2,700 3,650 1,015 BTS - Phloen Chit station Child Policy: Max.1 child under 12 years old sharing room using existing bed akyra Studio (king) 2,780 3,800 - 1,095 - 06Apr-31Oct18 (5) Akyra Thonglor Bangkok akyra Suite (king) 3,040 4,320 2,540 1,345 400 BTS - Thong Lo station Child Policy: Max.1 child under 12 years old sharing room using existing bed stay free, optional breakfast charge at $105; free breakfast for child 5 years old or below 1 Bedroom Superior 3,010 4,270 1,320 Suite (5) Anantara Baan Rajprasong 06Apr-31Oct18 2,440 345 1 Bedroom Deluxe Serviced Suites 3,090 4,420 1,400 Suite BTS - Ratchadamri station All room type : Stay on Fri-Sat, surcharge of HKD90/ room/ night Child Policy: Max.1 child under 12 years old sharing room using existing bed, compulsory breakfast charge at $90 (5) Anantara Bangkok Sathorn Premier 2,460 3,170 - 790 - 06Apr-31Oct18 BTS - Chong Nonsi station 1 Bedroom Suite 2,620 3,480 2,700 940 475 Deluxe 3,740 5,730 2,025 06Apr-31Oct18 2,800 525 Deluxe View 3,900 6,050 2,185 (5) Anantara Siam Bangkok Hotel Child Policy: Max.1 child under 12 years old sharing room using existing bed, compulsory breakfast charge at $145 30 days early bird promotion BTS - Ratchadamri station Deluxe 3,550 5,330 1,835 06Apr-31Oct18 2,800 525 Deluxe View 3,690 5,620 1,975 Premier Room 06Apr-31Oct18 2,360 2,960 2,280 685 270 Long Stay Benefit for min.4 nights: 1. -

Street Food in Bangkok Serving Food, As One Can Find Culinary Treasures on the Street at No Matter What Time It Is

17.6 cm 17.8 cm 17.8 cm 17.6 cm The delicious culinary adventures in Bangkok Street food is a part of Thai way of life for decades, for not only it is convenient, but it is also inexpensive and most certainly, Amazing Tastes of Thailand delicious. There is no shortage of street food vendors in Bangkok, where the mouthwatering-smelling option is endless, ranging from grilled pork skewers to fresh seafood cooked on the spot. Bangkok is a city that never sleeps, especially when it comes to Street Food in Bangkok serving food, as one can find culinary treasures on the street at no matter what time it is. Take an edible tour through Bangkok’s most vibrant roadside food scenes and discover for yourself why Bangkok is one of the best places in the world for street food! inch 10 Mango sticky rice Printed in Thailand by Promotional Material Production Division, Marketing Services Department, Tourism Authority of Thailand for free distribution. www.tourismthailand.org E/JAN 2020 The contents of this publication are subject to change without notice. 63-01-049 Leaflet_StreetFood new22-01_Q_coateduv2019.indd 1 63-01-049 Leaflet A_StreetFood new22-01_Q_coateduv2019 22/1/2563 BE 11:59 17.6 cm 17.8 cm 17.8 cm 17.6 cm The delicious culinary adventures in Bangkok Street food is a part of Thai way of life for decades, for not only it is convenient, but it is also inexpensive and most certainly, Amazing Tastes of Thailand delicious. There is no shortage of street food vendors in Bangkok, where the mouthwatering-smelling option is endless, ranging from grilled pork skewers to fresh seafood cooked on the spot. -

AW Leaflet CP Pratunam

CENTRE POINT HOTEL PRATUNAM GATEWAY OF A COLORFUL LIFE EXPERIENCE THE QUINTESSENTIALLY BANGKOK MODERN LIVING AND WARM HOSPITALITY THAT WILL FULFILL YOU COLORFUL JOURNEY WITH A GOOD TIME, EVERY DAY AND NIGHT COLORFUL & DELIGHTFUL HOTEL Exceptionally spacious, and fully equipped with in-room facilities and amenities • Balcony with City Views • Kitchen Utensils* • Cable TV • Living Area • DVD Player * • Magnetic Key Card • Electric Kettle • Microwave* • Free WiFi • Pantry and Dining Area • Fully Furnished Rooms • Refrigerator • Healthy Pillow* • Toaster* *Upon request FINEST FACILITIES Offer a comprehensive list of first class facilities at your disposal, providing optimum convenience for your business and leisure needs • Business Center* • Resident Lounge* • Children’s Indoor Playroom • Restaurant* • Complimentary Coffee Tea • Salt Water Swimming Pool and Herb Drink • Self – Service Laundry Room* • Conference Room* • Shower Room • Fitness Room • Shutter Corner • Jacuzzi and Sauna • Vending Machine* *Additional charge ATTRACTIONS Bangkok’s leading department stores, fashion boutiques and outlets, and IT mall: all within the vicinity • Bamrungrad Hospital • Phaya Thai Hospital • Central World • Pratunam Market • Erawan Shrine • Siam Discovery Center (Four-Faced Buddha) • Siam Paragon • ISETAN Department Store • Siam Square • MBK Shopping Mall • The Market • Pantip Plaza • The Platinum Fashion Mall TRANSPORTATION Close proximity to Bangkok’s fast and convenient modes of transport to get you around Bangkok in a matter of minutes • Airport Rail Link Express Train Phaya Thai Station • BTS Skytrain Ratchathewi Station For reservation, please contact Sales and Reservations Office Tel: +66 2 251 8083 Fax: +66 2 251 8900 [email protected] www.centrepoint.com CENTRE POINT HOTEL PRATUNAM 6 Soi Petchburi 15, Petchburi Road, Phaya Thai, Rajtaevee, Bangkok 10400 Thailand Tel: +66 2 653 6690 Fax: +66 2 255 3845 [email protected]. -

Essential Information for Exchange Students Faculty of Pharmacy Mahidol University

Essential Information For Exchange Students Faculty of Pharmacy Mahidol University International Relations Unit Faculty of Pharmacy, Mahidol University 2019 1 Content Overview 2 Visa 4 Embassies 6 Emergency Numbers 7 Travel Guide from the Suvarnabhumi Airport to Inner City Area 8 Getting Around In Bangkok 10 How to get to Faculty of Pharmacy, Mahidol University 11 How to purchase a Thailand SIM card 12 Shopping Centers & Malls 14 Thai Culture 16 2 Overview Faculty of Pharmacy, Mahidol University The Faculty of Pharmacy, Mahidol University at present time At present time, the Faculty offers pharmacy education at every level ranging from undergraduate to graduate (both Master and Doctoral levels) degrees in almost every aspects of pharmacy profession. For undergraduate study, a 6-year curriculum is currently offered. For graduate study, we offer a wide range of Master and Doctoral degrees encompassing almost every stages of the entire drug development process. For more information, please visit http://www.pharmacy.mahidol.ac.th/eng/ Facilities The current facility of the faculty consists of 2 buildings. Thepparat Building (construction completed in February 1991) and Ratcharat Building (construction completed in June 2000) are the two main buildings of the faculty. In 1991, Princess Sirindhorn presided in a ceremony to officially open Thepparat building for use. The building was also named after the Princess’s name. Thepparat Building, a 7th floor building, houses a 300-seat auditorium (3rd floor), two 150-seat lecture rooms (2nd floor), small lecture rooms (2nd floor), 7 large laboratories, the Faculty Drug Store (1st floor), Muslim prayer room (4th floor), part of central research laboratory, Office of the Dean, and other supporting units such as documentation office, finance and procurement officer, undergraduate student office, graduate student office, students affair office, and international affair office. -

Black Carbon in Pm2.5 at Roadside Site in Bangkok, Thailand

International Journal of GEOMATE, Aug., 2020, Vol.19, Issue 72, pp. 81 - 87 ISSN: 2186-2982 (P), 2186-2990 (O), Japan, DOI: https://doi.org/10.21660/2020.72.9245 Special Issue on Science, Engineering and Environment BLACK CARBON IN PM2.5 AT ROADSIDE SITE IN BANGKOK, THAILAND Pornsuda Phanukarn1, Hathairattana Garivait2 and Sopa Chinwetkitvanich3,* 1,3 Department of Sanitary Engineering, Faculty of Public Health, Mahidol University, Thailand; 2Department of Environmental Quality Promotion, Ministry of Natural Resources and Environment, Thailand *Corresponding Author, Received: 16 Aug. 2019, Revised: 30 Nov. 2019, Accepted: 24 Feb. 2020 ABSTRACT: Traffic is typically a major source of air pollution in urban areas of developing countries. The exhaust emissions include gaseous substances and particulate matter, which PM2.5 (particulate matter less than 2.5 micrometers in aerodynamic diameter) is the majority. In urban areas, the composition of PM2.5 at roadside site dominated by the carbonaceous combustion component, the major constituent wherein was represented as black carbon (BC). This study aimed to investigate the diurnal concentrations of BC related to PM2.5 by using a seven-wavelength aethalometer. Study site was located near one of congested roads in Bangkok, Thailand. The correlation between traffic volumes and BC concentrations at roadside were also discussed. Results showed that the 24-h average BC concentrations of this site were in the range of 1.5 – 15 µg/m3. The diurnal pattern of BC levels exhibited two peaks of BC concentrations occurring during 0500 to 0700 LST and 2100 to 2300 LST. The morning peak of BC evidently governed by traffic condition while the evening peak resulted from traffic associated with meteorological effect. -

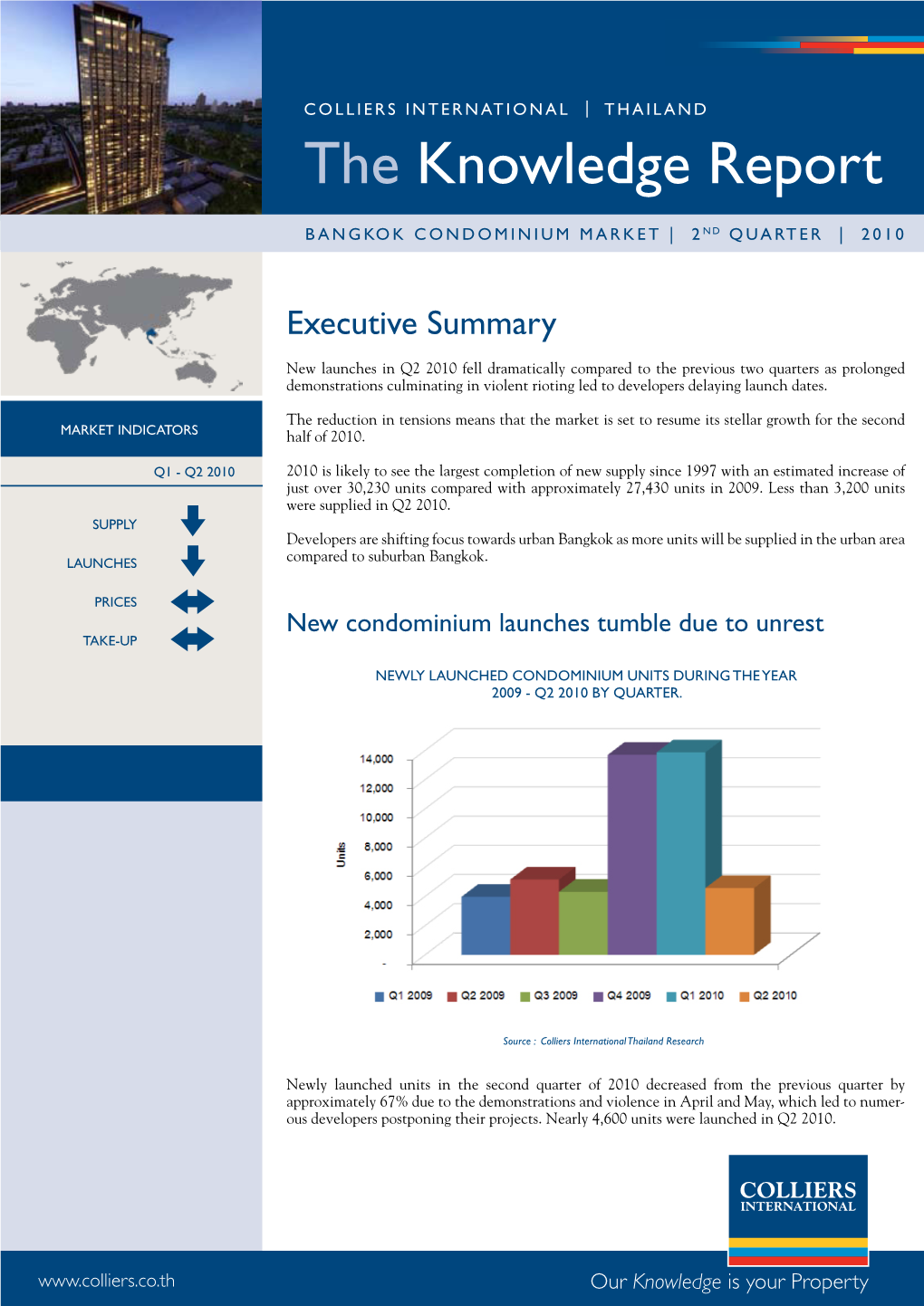

Bangkok Condominium Market REPORT

YEAR END 2010 | CONDOMINIUM THAILAND BANGKOK CONDOMINIUM MARKET REPORT Bangkok Condominium Market EXecUTIVE SUMMARY New launches in Q4 2010 continued to surge on the back of continued confidence in the residential market and affordable units being offered by developers. Overall 2010 represented a landmark year for the condominium market with over 60,000 units being launched in total. 2011 is set for another strong year for condominium launches but is then expected to moderate and a supply bubble is likely to be avoided as developers and authorities pay close attention to the market and its constraints. This year will represent a move from boom to consolidation. Market INDicatOrs Developers are dividing their attention to both urban and suburban Bangkok, with a similar number 2009 - 2010 being launched in both areas. Suburban Bangkok still remains firmly on the radar with listed developers targeting the low to mid end segment of the market, however non-listed developers are SUPPLY fighting back in Q4 2010 with many players launching smaller scale projects thus providing healthy LAUNCHES competition in the market. PRICES Issues regarding transport access to mass transit stations mean that the positive effects of these lines is not being fully realized and could be a problem for future new lines. TAKE-UP www.colliers.co.th BANGKOK CONDOMINIUM MARKET REPORT | Q4 2010 NEWLY LAUNCHED CONDOMINIUM Units DURING THE YEAR 2009 – Q4 2010 bY QUarter Source : Colliers International Thailand Research Newly launched units in the fourth quarter of 2010 slightly decreased but were resumed in Q3 and then continued forwards for Q4 2010. -

VIE Hotel Bangkok, Mgallery by Sof Itel

VIE Hotel Bangkok, MGallery by Sof itel VIE Hotel Bangkok, MGallery by Sofitel Dining options are superb with acclaimed La VIE is a modern and elegant 5-star luxury designed – Creative French Cuisine as well as YTSB – hotel and creation of renowned French architect Yellow Tail Sushi Bar, which is touted as the best J + H Boiffils, with a spellbinding atmosphere sushi in town. The hotel also features VIE Spa, and complete with works of art, exotic furniture, fitness with WE Signature Club and our soft shades and audacious colors. Conveniently outstanding rooftop VIE Pool as well as meeting located in the heart of the city, it is just steps and wedding venues. away from the BTS Skytrain Ratchathewi station Recognitions and awards and within walking distance of the city’s most • World Luxury Hotel Awards 2016 – 2018 famous shopping malls such as Siam Paragon, • World Luxury Spa Awards 2018 Siam Center, Siam Discovery Center, Central World, • TripAdvisor’s Excellence of the year 2016 – 2018 Central Embassy, The EmQuartier, Platinum Mall • Now Travel Awards 2012 – 2018” and MBK Center. • Thailand Tatler’s Best Restaurants 2010 – 2018 • Bangkok’s Best Restaurants Awards 2014 – 2018 Accommodation consists of 154 modern and • Wongnai User’s Choice 2014 – 2018 elegant duplexes, spacious rooms and suites. • A “Michelin Plate” by Michelin Guide Bangkok 2018 Meeting & Banqueting - VIE function rooms are dedicated and private with elegant modern designs and welcoming natural light. Event facilities, measuring 258 square meters, include banquet facilities which can cater for up to 200 people. The Ballroom boasts high ceilings with city views, while the adjoining foyer provides the ideal pre-function area.