Downtown at a Glance (June 2019)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Espersonespersonesperson 808 Travis Street & 815 Walker Avenue • Houston, Texas

THETHETHE ESPERSONESPERSONESPERSON 808 TRAVIS STREET & 815 WALKER AVENUE • HOUSTON, TEXAS EXECUTIVE SUMMARY THETHETHE ESPERSONESPERSONESPERSON 808 TRAVIS STREET & 815 WALKER AVENUE • HOUSTON, TEXAS HFF, as the exclusive representative of the owner, is pleased to offer for sale a 100% fee simple interest in Esperson (the “Property”), a 19 and 27-story, 599,107 square foot office building located in Houston’s central business district. Constructed in 1927 and 1941 respectively, Esperson is the only iconic structure of Italian Renaissance in Houston’s most densified employment center. The property is currently 62% leased with 4 years remaining average lease term and is situated on 1.447 acres, a full city block. Located at the intersection of Rusk and Walker Street, Esperson has direct access to Houston’s METRO Rail and 7.5 mile underground tunnel system. Over the last 36 months, ownership invested nearly $9 million in non-leasing capital, positioning the asset at the top of its competitive set. Today, considerable value creation is achievable through rolling current in-place rents to market and through the lease up of the remaining 226,561 square feet of vacant space. Redeveloping and expanding Houston’s CBD infrastructure – realized through rebuilt streets – highways, new mass transit and enhanced public utilities coupled with new office, multi-family, and retail projects have transformed Houston’s core into a vibrant, modern 24/7 environment for people to live, work and play. Esperson offers investors prestige, history, quality, abundant amenities, and a prime location in Houston’s largest employment center. INVESTMENT SALES H. DAN MILLER, CCIM, SIOR Senior Managing Director Tel: (713) 852-3576 [email protected] MARTIN T. -

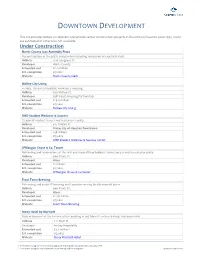

Downtown Development Project List

DOWNTOWN DEVELOPMENT This list provides details on all public and private sector construction projects in Downtown Houston since 1995. Costs are estimated or otherwise not available. Under Construction Harris County Jury Assembly Plaza Reconstruction of the plaza and pavilion including relocation of electrical vault. Address 1210 Congress St. Developer Harris County Estimated cost $11.3 million Est. completion 3Q 2021 Website Harris County Clerk McKee City Living 4‐story, 120‐unit affordable‐workforce housing. Address 626 McKee St. Developer Gulf Coast Housing Partnership Estimated cost $29.9 million Est. completion 4Q 2021 Website McKee City Living UHD Student Wellness & Success 72,000 SF student fitness and recreation facility. Address 315 N Main St. Developer University of Houston Downtown Estimated cost $38 million Est. completion 2Q 2022 Website UHD Student Wellness & Success Center JPMorgan Chase & Co. Tower Reframing and renovations of the first and second floor lobbies, tunnel access and the exterior plaza. Address 600 Travis St. Developer Hines Estimated cost $2 million Est. completion 3Q 2021 Website JPMorgan Chase & Co Tower Frost Town Brewing Reframing and 9,100 SF brewing and taproom serving locally inspired beers Address 600 Travis St. Developer Hines Estimated cost $2.58 million Est. completion 3Q 2021 Website Frost Town Brewing Moxy Hotel by Marriott Redevelopment of the historic office building at 412 Main St. into a 13‐story, 119‐room hotel. Address 412 Main St. Developer InnJoy Hospitality Estimated cost $4.4 million P Est. completion 2Q 2022 Website Moxy Marriott Hotel V = Estimated using the Harris County Appriasal Distict public valuation data, January 2019 P = Estimated using the City of Houston's permitting and licensing data Updated 07/01/2021 Harris County Criminal Justice Center Improvement and flood damage mitigation of the basement and first floor. -

6.20 Program.Pdf

LouCity Program Ad 2020 b.pdf 1 8/24/20 12:04 PM WE NEED TO BENOWNOW MOREMORE THANTHAN EVEREVER C M Y Just as LouCity players work together on the field, CM MY we work together in innovative ways with businesses, CY individuals, nonprofits and government orgs to CMY empower individuals and families in our community K to achieve their fullest potential. We mean it when we say that with your help, we will create a better – more equitable future for all – right here at home! Go LouCity! 502.426.8820 www.blairwood.com metrounitedway.org/2020 IN THIS ISSUE GAME PREVIEW 04 Match preview: what to watch for with Racing Lou FC and Houston Dash TEAM ROSTERS 05 A look at team rosters for Racing Louisville FC and Houston Dash LYNN FAMILY STADIUM 07 Key details about Racing Lou's home MAP OF LYNN FAMILY STADIUM 08 Map including sections, vendors, and more RACING STAFF 10 Racing Louisville's Coaches, Technical Staff, & Support Staff MEET THE TEAM 12-19 Player profiles for every athlete 2021 SEASON SCHEDULE 18 Racing Louisville's 2021 NWSL schedule COMMUNITY PARTNERS 19 A listing of Racing Louisville's business partners 03 match preview: what to watch for with racing lou fc vs houston dash By Jonathan Lintner After the NWSL’s international break, a revitalized HOME FIELD ADVANTAGE: Racing has found much Racing Louisville FC returns to action Sunday when more success in front of its supporters. Dating back hosting the Houston Dash at 3 p.m. inside Lynn Family to the preseason Challenge Cup tournament, the new Stadium. -

Franchise Disclosure Document

FRANCHISE DISCLOSURE DOCUMENT HILTON FRANCHISE HOLDING LLC A Delaware Limited Liability Company 7930 Jones Branch Drive, Suite 1100 McLean, Virginia 22102 703-883-1000 www.hiltonworldwide.com You will operate a Curio® hotel under a Franchise Agreement with us. The total investment necessary to begin operation of a typical 250-room Curio® hotel, excluding real property, is $3,599,405 to $112,461,595, including up to $463,675 that must be paid to us or our affiliates. This disclosure document summarizes certain provisions of your franchise agreement and other information in plain English. Read this disclosure document and all accompanying agreements carefully. You must receive this disclosure document at least 14 calendar days before you sign a binding agreement with, or make any payment to, the franchisor or an affiliate in connection with the proposed franchise sale. Note, however, that no government agency has verified the information contained in this document. The terms of your contract will govern your franchise relationship. Don’t rely on the disclosure document alone to understand your contract. Read all of your contract carefully. Show your contract and this disclosure document to an advisor, like a lawyer or accountant. Buying a franchise is a complex investment. The information in this disclosure document can help you make up your mind. More information on franchising, such as “A Consumer’s Guide to Buying a Franchise,” which can help you understand how to use this disclosure document, is available from the Federal Trade Commission. You can contact the FTC at 1-877-FTC-HELP or by writing to the FTC at 600 Pennsylvania Avenue, NW, Washington, DC 20580. -

Downtown Houston Residences

DOWNTOWN HOUSTON RESIDENCES CURRENT RESIDENCES OPEN DATE TYPE UNITS Beaconsfield Condos 1908 Condo 18 Plaza & Peacock Apartments 1927 Rental 32 Houston House Apartments 1968 Rental 394 Four Seasons Condominium 1980 Condo / Rental 104 Dakota Lofts 1994 Rental 53 Foley Building 1995 Single Family 1 White Oak Lofts 1997 Rental 12 Hermann Lofts 1998 Condo 33 The Rice 1998 Rental 312 New Hope Housing - 1414 Congress 1998 Affordable 57 St. Germain Lofts & Condos 1999 Condo 109 Bayou Lofts 2000 Condo 108 De George at Union Station (Veteran Housing) 2000 Affordable 99 Keystone Lofts 2000 Condo 31 Capitol Lofts 2001 Condo 37 Sabine Street Lofts (Marquis Lofts on Sabine) 2001 Rental 198 San Jacinto Lofts 2001 Condo 16 110 Milam 2001 Single Family 1 Commerce Towers 2002 Condo 132 Franklin Lofts 2003 Condo 62 Byrd's Lofts 2005 Condo 5 Eller Wagon Works 2005 Rental 32 Kirby Lofts on Main 2005 Condo 65 One Park Place 2009 Rental 346 Tennison Lofts 2009 Rental 39 CityView Lofts 2011 Rental 57 National Cash Register Building 2011 Single Family 1 SkyHouse Houston 2014 Rental 336 500 Crawford 2015 Rental 400 Block 334 2016 Rental 207 SkyHouse Main 2016 Rental 336 The Hamilton 2016 Rental 149 Market Square Tower 2016 Rental 463 The Star (1111 Rusk) 2017 Rental 286 1414 Texas Downtown 2017 Rental 285 Eighteen25 2017 Rental 242 ARIS Market Square 2017 Rental 274 Catalyst 2017 Rental 361 1711 Caroline 2018 Rental 220 Marlowe 2018 Condo 100 Camden Downtown 2020 Rental 271 Total Residential Properties: 41 Total Residential Units in Operation: 6,278 Updated: September 2020 RESIDENCES UNDER CONSTRUCTION OPEN DATE TYPE UNITS Sovereign at the Ballpark 2021 Rental 229 The Preston 2022 Rental 373 1810 Main - Fairfield Residential 2022 Rental 286 Trammell Crow Co. -

HOUSTON MAP DISTRIBUTION 200,000 Copies Twice Annually | Fall / Winter & Spring / Summer Hotel Locations

HOUSTON MAP DISTRIBUTION 200,000 Copies Twice Annually | Fall / Winter & Spring / Summer Hotel Locations Holiday Inn Express - Hobby/45-S Royal Sonesta - Galleria Holiday Inn Express - Pearland/Main St. Sheraton Suites - Galleria LaQuinta Inn & Suites - Hobby/Airport Blvd. St. Regis Hotel www.MAPAmerica.com LaQuinta Inn & Suites - Pearland Sonesta Suites - Galleria Marriott Hotel Houston - Hobby Westin Galleria/Westin Oaks Hotels Downtown/East Houston SpringHill Suites - Hobby (15 hotels) SpringHill Suites - Pearland Medical Center/Museum District/Reliant Best Western - Downtown (21 hotels) Club Quarters - Fannin St. Uptown/Galleria/Greenway Plaza Area Best Western - Medical Center Courtyard - Dallas St. (38 hotels) Candlewood Suites - Medical Center S. Main Crowne Plaza - Smith Aloft Hotel Galleria Comfort Suites - Medical Center/S. Main DoubleTree - Allen Center Best Western - Galleria/Fountainview Courtyard Marriott - Medical Center/S. Main Embassy Suites - Downtown Candlewood Suites - Galleria 610/Loop Central Crowne Plaza - Reliant Four Seasons - Lamar Comfort Inn - Westheimer/Wilcrest Econo Lodge - Medical Center Hilton Americas Houston - Downtown Comfort Suites - Galleria/Richmond Ave. Hampton Inn & Suites - Medical Center Holiday Inn Express - Downtown Courtyard by Marriott - Galleria/Sage Hilton - Plaza Medical Center Holiday Inn Express - Main Street Courtyard by Marriott - West University Holiday Inn - Astrodome Hotel ICON Crowne Plaza - River Oaks/SW Freeway Holiday Inn Express Medical Center Hyatt Regency - Downtown Crowne -

DOWNTOWN HOUSTON, TEXAS LOCATION Situated on the Edge of the Skyline and Shopping Districts Downtown, 1111 Travis Is the Perfect Downtown Retail Location

DOWNTOWN HOUSTON, TEXAS LOCATION Situated on the edge of the Skyline and Shopping districts Downtown, 1111 Travis is the perfect downtown retail location. In addition to ground level access. The lower level is open to the Downtown tunnels. THE WOODLANDS DRIVE TIMES KINGWOOD MINUTES TO: Houston Heights: 10 minutes River Oaks: 11 minutes West University: 14 minutes Memorial: 16 minutes 290 249 Galleria: 16 minutes IAH 45 Tanglewood: 14 minutes CYPRESS Med Center:12 minutes Katy: 31 minutes 59 Cypress: 29 minutes 6 8 Hobby Airport: 18 minutes 290 90 George Bush Airport: 22 minutes Sugar Land: 25 minutes 610 Port of Houston: 32 minutes HOUSTON 10 HEIGHTS 10 Space Center Houston: 24 minutes MEMORIAL KATY 10 330 99 TANGLEWOOD PORT OF Woodlands: 31 minutes HOUSTON 8 DOWNTOWN THE GALLERIA RIVER OAKS HOUSTON Kingwood: 33 minutes WEST U 225 TEXAS MEDICAL 610 CENTER 99 90 HOBBY 146 35 90 3 59 SPACE CENTER 45 HOUSTON SUGARLAND 6 288 BAYBROOK THE BUILDING OFFICE SPACE: 457,900 SQ FT RETAIL: 17,700 SQ FT TOTAL: 838,800 SQ FT TRAVIS SITE MAP GROUND LEVEL DALLAS LAMAR BIKE PATH RETAIL SPACE RETAIL SPACE METRO RAIL MAIN STREET SQUARE STOP SITE MAP LOWER LEVEL LOWER LEVEL RETAIL SPACE LOWER LEVEL PARKING TUNNEL ACCESS LOWER LEVEL PARKING RETAIL SPACE GROUND LEVEL Main Street Frontage 3,037 SQ FT 7,771 SQ FT RETAIL SPACE GROUND LEVEL Main Street frontage Metro stop outside door Exposure to the Metro line RETAIL SPACE GROUND LEVEL Houston’s Metro Rail, Main Street Square stop is located directly outside the ground level retail space. -

712 & 708 Main Street, Houston

712 & 708 MAIN STREET, HOUSTON 712 & 708 MAIN STREET, HOUSTON KEEP UP WITH THE JONES Introducing The Jones on Main, a storied Houston workspace that marries classic glamour with state-of-the-art style. This dapper icon sets the bar high, with historic character – like classic frescoes and intricate masonry – elevated by contemporary co-working space, hospitality-inspired lounges and a restaurant-lined lobby. Highly accessible and high-energy, The Jones on Main is a stylishly appointed go-getter with charisma that always shines through. This is the place in Houston to meet, mingle, and make modern history – everyone wants to keep up with The Jones. Opposite Image : The Jones on Main, Evening View 3 A Historically Hip Houston Landmark A MODERN MASTERPIECE THE JONES circa 1945 WITH A TIMELESS PERSPECTIVE The Jones on Main’s origins date back to 1927, when 712 Main Street was commissioned by legendary Jesse H. Jones – Houston’s business and philanthropic icon – as the Gulf Oil headquarters. The 37-story masterpiece is widely acclaimed, a City of Houston Landmark recognized on the National Register of Historic Places. Together with 708 Main Street – acquired by Jones in 1908 – the property comprises an entire city block in Downtown Houston. Distinct and vibrant, The Jones touts a rich history, Art Deco architecture, and famous frescoes – soon to be complemented by a suite of one-of-a-kind, hospitality- inspired amenity spaces. Designed for collaboration and social interaction, these historically hip spaces connect to a range of curated first floor retail offerings, replete with brand new storefronts and activated streetscapes. -

DOWNTOWN the OAKS Hobby Airport 24 M I N

THE WOODLANDS KINGWOOD TOMBALL SPRING ATSCOCITA 290 HUMBLE LOCATION WILLOWBROOK 59 CYPRESS 90 6 The Heights 15 min. IAH 99 River Oaks 17 min. 45 West University Place 14 min. Memorial 23 min. 290 59 90 The Galleria 16 min. THE Tanglewood 17 min. HEIGHTS 10 KATY MEMORIAL 10 The Medical Center 19 min. 610 TANGLEWOOD RIVER DOWNTOWN THE OAKS Hobby Airport 24 m i n . GALLERIA WEST George Bush Intercontinental UNIVERSITY 27 m i n. THE Airport (IAH) PLACE MEDICAL PORT OF CENTER HOUSTON 610 Sugar Land 27 m i n. 59 Port of Houston 40 min. Trinity Bay 99 Baybrook 32 min. HOBBY AIRPORT 90 Katy 37 min. 45 Cypress 35 min. Galveston Bay 288 SUGAR LAND BAYBROOK The Woodlands 36 min. 59 6 PEARLAND Kingwood 38 min. 65,720 150,000 22 residents currently live employees work Hotels downtown downtown (2 mile radius) 11 2,936 220,000 million people attend downtown Houston new residential units people visit downtown culture and entertainment planned or under on a daily basis attractions annually construction 1.2 million 7, 300 1,500 43.7 million 1.5 million people stay in downtown hotel rooms new hotel rooms SF of existing SF of office under Houston hotels annually under construction office space construction MAJOR EMPLOYERS Franklin Franklin Lofts? Old Cotton Islamic Hermann The Corinthian Harris Exchange Dawah Center Harris Lofts County County Family Law Harris Garage Center County Foley Sally’s Hotel Icon Congress Plaza Civil Courthouse George Bush Building (Jury Assembly) House Monument Congress Market Market 1414 Square Congress Garage Square Houston Hamilton Street Sesquicentennial Harris County Ballet Park Residences Majestic 1910 Courthouse Harris County Park Metro Harris County Juvenile Justice Admin. -

Harris County , Texas

H ARRIS C OUNTY, TEXAS BUDGET MANAGEMENT DEPARTMENT ECONOMIC DEVELOPMENT Harris County Economic Highlights, 2017 December 6, 2017 NOTE – most data pertains to Harris County only and not to the greater Houston Metropolitan Statistical Area Administration Building // 1001 Preston, Suite 500, Houston, TX 77002 // Tel: (713) 274-1400 prepared 12/06/17 Harris County Budget Management Department, Economic Development Harris County Economic Highlights, 2017 Table of Contents Topic Page Number 1. Harris County At a Glance …………………………………..…………………………… 3 2. Fortune 500 Headquarters …………………………………………………... 4 3. Top 100 Employers …………................................................................ 5 4.Harris County Rankings ……………………………………………………………………. 6 5.Harris County Business Climate …………………………...… .......................... 7 5 . 1 Cost of Living …………………………………………………………………………. 8 5 . 2 Cost of Doing Business and Tax Climate ………………………………………. 16 5 . 3 One Stop Shop – Business Resources……………………………………………. 17 6. Harris County’s Top Industries ………… ………………………………………………. 21 7. Harris County’s Strategic Advantages …………………………………………………. 24 7 . 1 Population Highlights …………………………………………………………. …… 25 7 . 2 Diversity ……………………………………………………………………………..… . 30 7 . 3 Education and Workforce ……………………………………………………………. 31 7 . 4 Transportation System ……………………………………………………………….. 36 7 . 5 Medical System ………………………………………………………………………… 41 8. Quality of Life …………………………………………………………………………...... 42 prepared 12/06/17 Page 2 of 43 Harris County Budget Management Department, Economic Development Table of Contents Harris County Economic Highlights, 2017 1. Harris County at a Glance Harris County is the best place to invest, open and operate your business. It has 34 cities within its boundaries including the City of Houston, its county seat. World Class Transportation System $68.2 billion (or 81%) of 4.59 million $0 18 2 1 1 3 4 Interstate highways All Exported Goods Residents State and Major Airports Spaceport Major Sea Major Rail 4 State highways from the Houston Metro Fortune 500 (U.S. -

HOUSTON METHODIST CONCUSSION CENTER Know the Signs and Symptoms

HOUSTON METHODIST CONCUSSION CENTER Know the Signs and Symptoms What is a concussion? A concussion is a mild brain injury. Concussions are caused by a bump, blow or jolt to the head or body. Even a “ding,” “getting your bell rung,” or what seems to be a mild bump or blow to the head can lead to a concussion and should be considered serious. What are the signs and symptoms? You can’t see a concussion. Signs and symptoms of concussion can appear immediately after the injury or may evolve over time. If your athlete reports one or more symptoms listed below, or if you notice the signs and symptoms yourself, keep your athlete out of action and seek medical attention immediately. Observable signs Symptoms reported by athlete • Appears dazed or stunned • Headache or “pressure” in head • Confused about assignment or position • Nausea or vomiting • Forgets an instruction • Balance problems or dizziness • Unsure of game, score or opponent • Double or blurry vision • Moves clumsily • Sensitivity to light or noise • Answers questions slowly • Feeling sluggish, hazy, foggy or groggy • Loses consciousness (even briefly) • Concentration or memory problems • Shows mood, behavior and personality changes • Confusion • Can’t recall events prior to or after a hit or fall • Just not “feeling right” or is “feeling down” • Loses balance or is unsteady when walking Danger signs Be alert for symptoms that worsen over time. The student or athlete should be seen in the emergency department right away if he or she has: • One pupil is larger than the other • Difficulty -

Greater Houston Convention and Visitors Bureau

GREATER HOUSTON CONVENTION AND VISITORS BUREAU 2014 - 2015 ANNUAL REPORT MISSION STATEMENT 2 STRUCTURE & FUNDING 2 2014 KEY ACCOMPLISHMENTS 2 CITY OFFICIALS 3 COUNTY OFFICIALS 3 LETTER FROM THE PRESIDENT 4 LETTER FROM THE CHAIRMAN 5 2014 BOARD OF DIRECTORS 6 2015 BOARD OF DIRECTORS 8 DESTINATION SALES 12 TOURISM 14 DESTINATION SERVICES 16 MEMBERSHIP 18 PARTNERSHIPS & EVENT DEVELOPMENT 20 MARKETING 22 HOUSTON FILM COMMISSION 24 VISITOR INFORMATION SERVICES 26 FINANCE & ADMINISTRATION 28 MISSION STATEMENT The mission of the Greater Houston Convention and Visitors Bureau is to improve the economy of greater Houston by attracting national and international conventions, trade shows, tourists and film projects to the area through sales, marketing and public relations efforts. STRUCTURE & FUNDING The Greater Houston Convention and Visitors Bureau is a 501(c)6 nonprofit corporation. The GHCVB is a marketing and service organization with a budget presently comprised of certain reserved funds and private funds raised through a variety of sources including investments in events, membership dues, advertising and in-kind contributions. At the beginning of 2014, the GHCVB’s primary source of funding was from a contract with the City of Houston which was assigned to the Houston First Corporation, or HFC, in 2011 and expired June 30, 2014. This contract funded approximately 92% of the GHCVB’s budget from a tax on hotel/ motel occupancy within the incorporated boundaries of Houston, Texas. Upon expiration of the contract on June 30, 2014, the GHCVB and HFC boards approved a strategic realignment between the two organizations to create a more efficient approach to marketing and selling Houston to tourists and conventions.