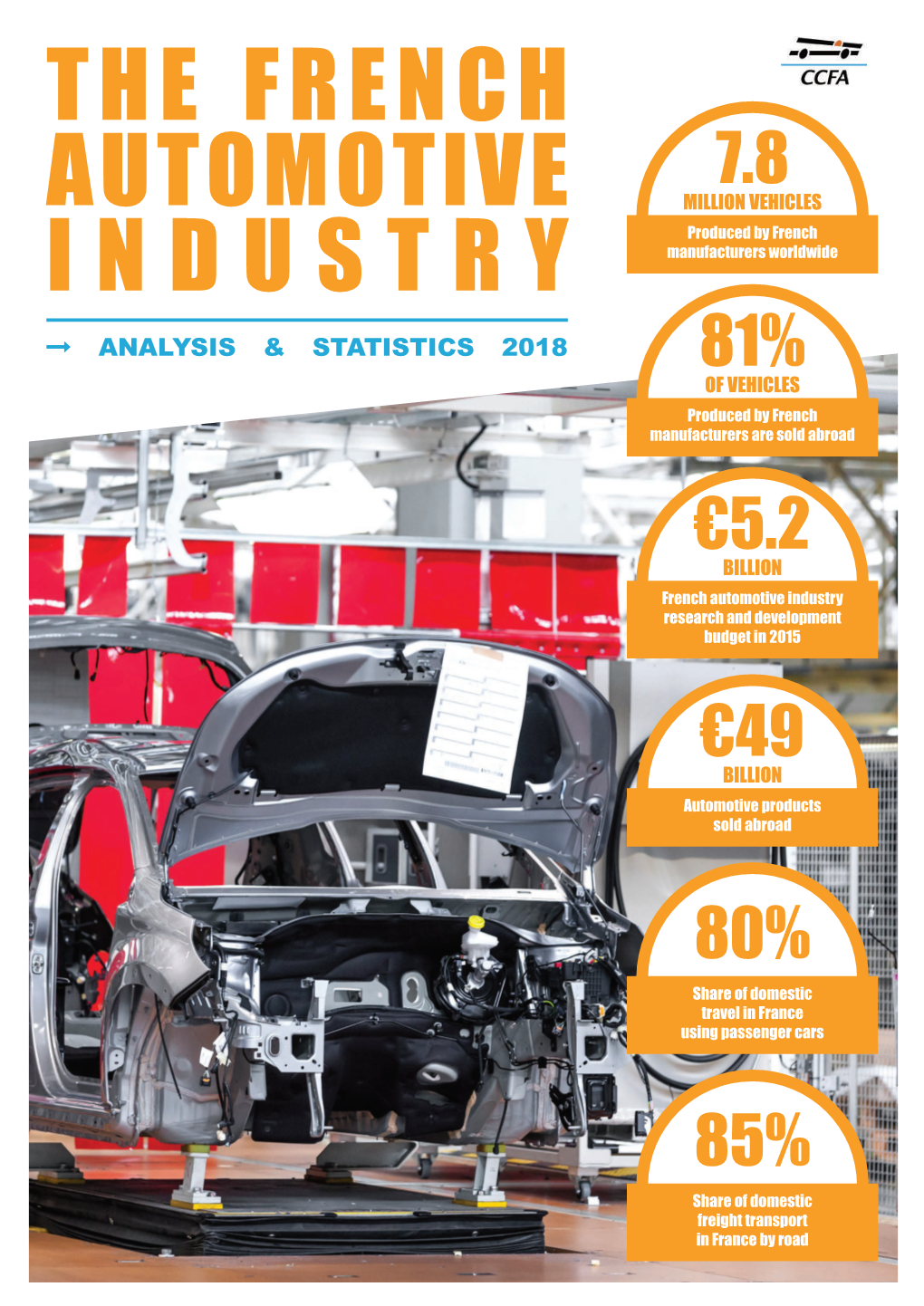

The French Automotive Industry

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Dacia, Still Dacia

PRESS RELEASE 01/14/2021 MORE DACIA, STILL DACIA • Building on a strong and efficient all-weather business model, the Dacia saga continues with a new chapter • The creation of the new Dacia-Lada business unit will boost Dacia’s competitiveness through leveraged engineering & manufacturing synergies with Lada • The New Dacia Bigster Concept embodies the Dacia brand evolution, breaking the C-segment glass-ceiling • Dacia stays Dacia, as affordable as ever, with a touch of coolness Boulogne-Billancourt – 14th January 2021. As part of Groupe Renault’s Renaulution strategy, Dacia unveiled its 5-year plan. With the creation of the Dacia-Lada business unit, Dacia will boost its efficiency and competitiveness, while going beyond its perimeter in terms of products. The presentation of the Bigster Concept paves the way for new horizons for Dacia in the C-Segment. “Dacia will stay Dacia, always offering a trustworthy, authentic, best value-for money proposition to smart buyers. With the creation of the Dacia-Lada business unit, we’ll leverage to the full the CMF-B modular platform, boost our efficiency and further increase our products competitiveness, quality and attractiveness. We’ll have everything we need to bring the brands to higher lands, with the Bigster Concept leading the way.” (Denis Le Vot, CEO Dacia and Lada brands, during the unveiling of Renaulution) An all-weather business model, as unique as it is efficient For the past 15 years, Dacia has consistently rolled out contemporary, simple, and appealing vehicles. Relying on an unrivalled know-how, Dacia leverages the best proven and amortized technical solutions from Groupe Renault and Renault Nissan Mitsubishi Alliance Thanks to a lean distribution model, Dacia has since carved out a name for itself in 44 countries, with 7 million vehicles sold so far and many best-sellers. -

Press Information (Revised November 20, 2013)(PDF: 28Pages 9.5MB)

Press Information For Immediate Release Mitsubishi Motors Lineup at 43rd Tokyo Motor Show 2013 TOKYO, November 20, 2013 - Mitsubishi Motors Corporation (MMC) will unveil three world premiere concept cars at the 43rd Tokyo Motor Show 2013*1 from November 20. Incorporating a new design that symbolizes the functionality and reassuring safety inherent to SUVs, the three concepts take as their theme MMC’s @earth TECHNOLOGY*2 and point to the direction MMC’s development and manufacturing will take in the near future. The MITSUBISHI Concept GC–PHEV*3 is a next-generation full-size SUV with full-time 4WD. It is based on a front engine, rear-wheel drive layout plug-in hybrid EV (PHEV) system comprising a 3.0-liter V6 supercharged MIVEC*4 engine mated to an eight-speed automatic transmission, with a high-output motor and a high-capacity battery to deliver all-terrain performance truly worthy of an all-round SUV. The MITSUBISHI Concept XR-PHEV*5 is a next-generation compact SUV developed to take driving pleasure to new levels. The MITSUBISHI Concept XR-PHEV uses a front engine, front-wheel drive layout PHEV system that is configured with a downsized 1.1-liter direct-injection turbocharged MIVEC engine, a lightweight, compact and high-efficiency motor with a high-capacity battery. These two concepts feature PHEV systems optimally tailored to different market and segment requirements. The MITSUBISHI Concept AR*6 is a next-generation compact MPV which combines SUV maneuverability with MPV roominess. It uses a lightweight mild hybrid system which comprises a downsized 1.1-liter direct-injection turbocharged MIVEC engine. -

Document Type Communiqué De Presse Groupe

PRESS RELEASE #RenaultResults REVENUES OF €11.3 BILLION IN THE THIRD QUARTER OF 2019 • Group revenues reached €11,296 million (-1.6%) in the quarter. At constant exchange rates and perimeter1, the decrease would have been -1.4%. • The Group sold 852,198 vehicles in the quarter, down -4.4% in a global market down -3.2%2. Excluding Iran, the decrease would have been -1.8% in a market down -2.3%. • The Group is pursuing its pricing policy in the third quarter. Boulogne-Billancourt, 10/25/2019 COMMERCIAL RESULTS: THIRD QUARTER HIGHLIGHTS In the third quarter, Groupe Renault sold 852,198 vehicles, down -4.4% in a market that fell by -3.2%. Excluding Iran, the decrease would have been -1.8% in a market down -2.3%. In Europe, the Group recorded a -3.4% decline in sales in a market up +2.4%. This decrease is partly due to a high comparison basis related to the introduction of the WLTP3 for passenger cars in September 2018 and the awaiting of the full availability of New Clio in Europe. In regions outside Europe, the Group over-performed the market. In a market down -6.2%, the Group recorded a -5.4% decrease in sales, mainly due to the decline in markets in Turkey (-21.7%), Argentina (-30.0%), and the end of sales in Iran since August 2018 (23,649 vehicles sold in the third quarter 2018). Excluding Iran, sales would have been down -0.3%. 1 In order to analyze the change in consolidated revenues at constant perimeter and exchange rates, Groupe Renault recalculates revenues for the current year by applying the average annual exchange rates of the previous year, and excluding significant changes in perimeter that occurred during the year. -

Note: This English Translation Is for Reference Purposes Only. in The

Note: This English translation is for reference purposes only. In the event of any discrepancy between the Japanese original and this English translation, the Japanese original shall prevail. We assume no responsibility for this translation or for direct, indirect or any other forms of damage arising from the translation. (Securities code: 7211) June 3, 2019 To our shareholders 3-1-21, Shibaura, Minato-ku, Tokyo MITSUBISHI MOTORS CORPORATION Chairman of the Board, CEO Osamu Masuko NOTICE OF THE 50TH ORDINARY GENERAL MEETING OF SHAREHOLDERS You are cordially invited to attend the 50th Ordinary General Meeting of Shareholders of Mitsubishi Motors Corporation (“MMC”) to be held as described as below. If you are unable to attend, as described in the “Notice on Exercising Voting Rights” (P. 3 and P. 4), you may exercise your voting right(s) in writing or via the Internet. To do so, please review the “Reference Materials” for the Ordinary General Meeting of Shareholders contained in this notice, and exercise your voting right(s) either by posting your voting form so that it arrives before 5:45 p.m. on Thursday, June 20, 2019 or inputting your vote on the website for exercising voting right(s) before the aforementioned date and time. 1. Date and time Friday, June 21, 2019 at 10:00 a.m. (Japan time) 2. Place 3-3-1 Shibakoen, Minato-ku, Tokyo Ho-O-No-Ma, 2F, Tokyo Prince Hotel (Please note that the place for this Ordinary General Meeting of Shareholders differs from the one for the previous meeting.) 3. Purposes Matters to report 1. -

Opel Grandland X 1.2 DI Turbo Start&Stop Dynamic

autotest Opel Grandland X 1.2 DI Turbo ADAC-Urteil Start&Stop Dynamic Fünftüriges SUV der unteren Mittelklasse (96 kW / 130 PS) AUTOTEST 2,6 er neue Grandland X soll den hierzulande wenig erfolgreichen Antara vergessen D machen. Wie beim Antara, der auf dem Chevrolet Captiva basierte, greift Opel AUTOKOSTEN 2,2 auch jetzt auf vorhandene Technik im Konzern zurück. Die technische Basis für den Grandland X liefert der Peugeot 3008. Zwar ist es den Rüsselsheimern gut gelungen, die Zielgruppencheck enge Verwandtschaft zu kaschieren, doch bei genauerem Hinsehen fallen dem kundi- gen Betrachter einige Gemeinsamkeiten auf. Unter der Haube werkelt beispielsweise Familie 2,5 der aus zahlreichen Peugeot- und Citroen-Modellen bekannte Dreizylinder-Benziner, Stadtverkehr 3,2 der 130 PS leistet und mit dem immerhin 1,4 Tonnen schweren Kompakt-SUV erstaun- lich wenig Mühe hat. Die Laufkultur geht ebenfalls in Ordnung, nur die Leistungsent- Senioren 2,4 fal-tung ist etwas unharmonisch. Im Innern bietet der Grandland X genügend Platz für vier Erwachsene samt Gepäck. Der Fahrer freut sich über einen aufgeräumten Arbeits- Langstrecke 2,8 platz und die weitgehend intuitive Bedienung. Auf den empfehlenswerten, vielfältig Transport 2,4 einstellbaren Ergonomiesitzen lassen sich selbst lange Strecken entspannt zurückle- gen, auch wenn das Fahrwerk etwas sensibler auf Unebenheiten ansprechen dürfte. Fahrspaß 3,2 Der nicht erhältliche Allradantrieb entlarvt den Grandland X als trendiges Lifestyle-Ge- fährt. Richtig zupacken kann der Opel weder im Gelände noch bei der Anhängelast. Für Preis/Leistung 2,4 knapp 30.000 Euro bekommt der Kunde ein gefälliges, gut ausgestattetes SUV. Beson- dere Stärken sucht man jedoch vergebens, große Schwächen allerdings auch. -

Catalogooilfilterskyfil.Pdf

oil filter SKO-2-2017 SKO-2-2018 OF. 9018 OF. 8806 CHEV. ASTRA 2.2 LTS. 4 LTS. 02/04 CHEV. ASTRA 1.8 LTS. 4 CIL. 00/01 MALIBU 2.2 LTS. 4 CIL. 04/08 CHEVROLET SKO-2-2020 SKO-2-2021 OF. 2518 OF. 10246 CHEV. SPARK 1.2 LTS. 4 CIL. 11/15 CHEV. ASTRA 1.8 LTS. 4 CIL. 07/08 CRUZE 1.8 LTS. 4 CIL. 11/15 SKA-L-2005 SKO-L-2006 OF. 3675 OF. 2933 CHEV. SIERRA V6 CHEV. ASTRA 2.4 LTS. 4 CIL. 04 SKO-L-2007 SKA-L-2008 OF. 3506 OF. 3387 CHEV. COLORADO 2.9 LTS. 4 CIL. 08/12 CHEV. CHEVY 1.6 LTS. 4 CIL. 01/12 CHEYENNE 5.3 LTS. 8V 03/07 CAVALIER 2.2 LTS. 4 CIL. 95/05 1 oil filter CHEVROLET SKO-L-2009 SKO-L-2010 OF. 05 CHEV. CAPTIVA SPORT 2.4 LTS. 4 CIL. 11/15 CHEV. SUBURBAN 7.4 LTS. 8V 92/95 ZAFIRA 2.2 LTS. 4 CIL. 02/07 SILVERADO 3500 HEAVY DUTY 5.7 LTS. 8V 03/05 CHRYSLER SKO-D-2033 SKO-D-2037 OF. 16 OF. 10060 CHRYS. GRAND VOYAGER 3.3 LTS. 6V 99/02 CHRYS. NITRO 4.0 LTS. 6V 09/11 RAM SRT-10 P-UP 8.3 LTS. 10V 04/06 JOURNEY 3.5 LTS. 6V 09/10 SKO-D-2038 SKO-D-2039 OF. 11665 OF. 3614 CHRYS. DURANGO 3.6 LTS. 6V 11/16 CHRYS. NEON 2.4 LTS. 4 CIL. 04/06 GRAND CARAVAN 3.6 LTS. -

Global Monthly Is Property of John Doe Total Toyota Brand

A publication from April 2012 Volume 01 | Issue 02 global europe.autonews.com/globalmonthly monthly Your source for everything automotive. China beckons an industry answers— How foreign brands are shifting strategies to cash in on the world’s biggest auto market © 2012 Crain Communications Inc. All rights reserved. March 2012 A publication from Defeatglobal spurs monthly dAtA Toyota’s global Volume 01 | Issue 01 design boss Will Zoe spark WESTERN EUROPE SALES BY MODEL, 9 MONTHSRenault-Nissan’sbrought to you courtesy of EV push? www.jato.com February 9 months 9 months Unit Percent 9 months 9 months Unit Percent 2011 2010 change change 2011 2010 change change European sales Scenic/Grand Scenic ......... 116,475 137,093 –20,618 –15% A1 ................................. 73,394 6,307 +67,087 – Espace/Grand Espace ...... 12,656 12,340 +316 3% A3/S3/RS3 ..................... 107,684 135,284 –27,600 –20% data from JATO Koleos ........................... 11,474 9,386 +2,088 22% A4/S4/RS4 ..................... 120,301 133,366 –13,065 –10% Kangoo ......................... 24,693 27,159 –2,466 –9% A6/S6/RS6/Allroad ......... 56,012 51,950 +4,062 8% Trafic ............................. 8,142 7,057 +1,085 15% A7 ................................. 14,475 220 +14,255 – Other ............................ 592 1,075 –483 –45% A8/S8 ............................ 6,985 5,549 +1,436 26% Total Renault brand ........ 747,129 832,216 –85,087 –10% TT .................................. 14,401 13,435 +966 7% RENAULT ........................ 898,644 994,894 –96,250 –10% A5/S5/RS5 ..................... 54,387 59,925 –5,538 –9% RENAULT-NISSAN ............ 1,239,749 1,288,257 –48,508 –4% R8 ................................ -

Aftersales Products and Services Free to Travel with Peace of Mind Your Business Never Stops

AFTERSALES PRODUCTS AND SERVICES FREE TO TRAVEL WITH PEACE OF MIND YOUR BUSINESS NEVER STOPS IVECO BUS COMMITMENT IS TO PROTECT THE VALUE, THE PERFORMANCE AND THE PRODUCTIVITY OF YOUR BUS OVER TIME. In choosing IVECO BUS you have made a quality choice. Nobody more than IVECO BUS can guarantee products, solutions and services tailored to your bus and your mission. With IVECO BUS you are sure that you can rely on the most proper maintenance, on high performance parts, on skilled experts, ready to help you always and wherever. And you can travel with peace of mind. 2 3 CERTIFIED RELIABILITY CONTROLLED PROCESSES IVECO BUS Genuine Parts are designed for your IVECO BUS guarantees that products bus and submitted to the most rigorous quality tests and suppliers comply with quality standards for conformity, robustness, safety and endurance. in terms of raw materials and production They last longer and perform better. Overtime. processes along the replacement parts supply chain. PRODU CTIVITY ADVANCED LOGISTIC QUALIFIED ASSISTANCE IVECO BUS guarantees the steady availability The IVECO BUS Authorised Service Network or the delivery within 24 hours of replacement parts guarantees excellent service performances thanks as well as the traceability from the warehouse to the long-lasting experience, the ongoing training, to the service centre destination. the continuous updating of diagnostics tools and highly specialized mechanics. In addition, IVECO BUS Assistance Non Stop is always ready to support you on the road 24 hours a day and 7 days a week. 4 5 GENUINE PARTS ACCESSORIES LINE YOUR BUS IS FAVOURITE SPARE PARTS % CUSTOMIZE THE BUS INCREASING ITS VALUE 10GENUINE 0 WHY TO CHOOSE IVECO BUS GENUINE PARTS? % IVECO BUS Accessories has developed a product line dedicated to all bus ranges in order to better respond to every needs. -

CNH Industrial, Following the Merger of Fiat Industrial and CNH Global N.V

Iveco Bus History The history of Iveco in bus manufacturing can be traced back to the early 20th century, when Renault and Fiat introduced their first bus designs in 1906 and 1907 respectively. Founded in 1899 in Turin, Italy, by a group of engineers and investors including Giovanni Agnelli, the first vehicle built by Fiat (Fabbrica Italiana di Automobili Torino) was a car. The firm soon branched out, though, into trucks and buses. In 1903, Fiat produced its first commercial vehicle, and in 1929 a specialist industrial vehicle division, Fiat Veicoli Industriali, was created. In 1933, Fiat acquired OM, a truck, car and farm machinery maker. The company continued developing its passenger and goods vehicle businesses, and in 1966 made a further purchase, that of UNIC, a French manufacturer of trucks. Three years later the automobile, truck, bus and defence vehicle maker Lancia was acquired by Fiat. In 1974, Fiat became the majority shareholder of Magirus Deutz, a German bus, truck and fire equipment manufacturer. The following year marked the birth of Iveco, when Fiat Veicoli Industriali brought together its own and acquired brands under a single entity, taking its name from the initials of the International Vehicles Corporation it created. A majority shareholding in the Czech bus manufacturer Karosa was acquired in 1996 by Renault VI, whose bus division would later be merged with that of Iveco. Renault expanded its bus interests further with the acquisition in 1998 of the French bus and coach manufacturer Heuliez Bus, which became a subsidiary of Renault VI. In 1999, Iveco and Renault merged their bus and coach interests into a single business, Irisbus, which was owned equally by the two partners. -

AVTOVAZ Call with Financial Analysts

AVTOVAZ Call with Financial Analysts Nicolas MAURE / Dr. Stefan MAUERER CEO / CFO 16.01.2017 Disclaimer Information contained within this document may contain forward looking statements. Although the Company considers that such information and statements are based on reasonable assumptions taken on the date of this report, due to their nature, they can be risky and uncertain and can lead to a difference between the exact figures and those given or deduced from said information and statements. PJSC AVTOVAZ does not undertake to provide updates or revisions, should any new statements and information be available, should any new specific events occur or for any other reason. PJSC AVTOVAZ makes no representation, declaration or warranty as regards the accuracy, sufficiency, adequacy, effectiveness and genuineness of any statements and information contained in this report. Further information on PJSC AVTOVAZ can be found on AVTOVAZ’s web sites (www.lada.ru/en and http://info.avtovaz.ru). AVTOVAZ Call with Financial Analysts 16.01.2017 2 AVTOVAZ Overview Moscow International Automobile Salon 2016 AVTOVAZ 50-years History 1966/1970 VAZ 2101 2016 LADA XRAY AVTOVAZ Call with Financial Analysts 16.01.2017 4 AVTOVAZ Group: Key information 408 467 Cars & KDs produced 20.1% MOSCOW AVTOVAZ 331 Representative office sales points 30 IZHEVSK LADA-Izhevsk countries TOGLIATTI plant AVTOVAZ Head-office & 2015: 176.5 B-Rub (2.6 B-Euro) Togliatti plants 2016: estimated T/O > 2015 51 527 p. AVTOVAZ Call with Financial Analysts 16.01.2017 5 LADA product portfolio -

BAB III PEMBAHASAN A. Gambaran Umum Perusahaan 1. Sejarah

BAB III PEMBAHASAN A. Gambaran Umum Perusahaan 1. Sejarah Perusahaan PT. Wahana Sun Solo merupakan salah satu cabang perusahaan yang bergerak di bidang retail otomotif di Indonesia, yaitu PT. Nissan Motor Indonesia yang berdiri sejak tahun 2001 pada saat Nissan Motor Ltd bergabung dengan Renault (perusahaan mobil ternama asal Prancis). Sebenarnya Nissan memperkenalkan diri di Indonesia sejak tahun 60-an ketika nama Nissan masih memakai Datsun. Krisis global pada tahun 1998, Nissan mengalami krisis di seluruh dunia termasuk Indonesia. Krisis menjadikan Nissan membangun aliansi dengan Reanult dan mengembangkan produksi mereka bersama untuk memperbaiki keadaan kedua perusahaan tersebut. Pada tahun 2000 Nissan-Renault mencanangkan program jangka panjang yang dilaksanakan oleh semua cabang Nissan-Reanult di seluruh dunia. PT NMI berdiri sejak masa aliansi Nissan-Renault. bergabung dengan grup Indomobil untuk memudahkan pengembangan produksi. Hingga sejak saat ini Indomobil- Nissan mempunyai lebih dari 60 dealer di seluruh Indonesia. 22 Nissan memiliki assembly plant di daerah perindustrian di kota Karawang, Jawa Barat. Di era 60-an Nissan pertama kali masuk secara resmi ke Indonesia pada tahun 1969 dengan nama Datsun melalui Agen Tunggal PT Indokaya yang didirikan oleh H. Abdul Wahab Affan bersama dengan saudara-saudaranya. Jenis kendaraan yang diproduksi pada tahun itu adalah pick up, multi purpose (jip) dan sedan dengan produksi rata-rata 750 unit/bln yang dipasarkan di kota-kota terbesar di Indonesia. Kemudian pada tahun 1974 PT Indokaya memproduksi Datsun Sena yang penggunaan kandungan lokalnya mencapai 75% guna memenuhi anjuran pemerintah untuk menjalankan program lokalisasi bagi kendaraan roda empat. Produksi yang dihasilkan rata-rata 250 unit per bulan. Pada tanggal 14 April 1981, keagenan tunggal Datsun dipegang oleh PT Wahana Wirawan. -

ATLAS-Anglais-MARS2013

COUV-ATLAS2011-ANG 19/02/13 10:19 Page 1 RENAULT ATLAS MARCH 2013 (www.renault.com) (www.media.renault.com) DRIVE THE CHANGE Cover concept: Angie - Design/Production: Scriptoria - VESTALIA RENAULT ATLAS MARCH 2013 01 CONTENTS Key figures (1) 02 Key facts and figures KEY FIGURES 04 The simplified structure of the Renault Group 05 The Renault Group, three brands THE RENAULT-NISSAN ALLIANCE € million 41,270 07 Structure 2012 revenues 08 A dedicated team to accelerate synergies 09 The Alliance in 2012 LE GROUPE RENAULT 12 Organization chart 14 Vehicle ranges 20 Engine and gearbox ranges 24 Motor racing RENAULT GROUP 2011 2012 28 Renault Tech 29 Parts and accessories Revenues 42,628 41,270 30 Financial information € million 31 RCI Banque Net income - Group share 2,139 1,735 32 Corporate social responsibility 33 Workforce € million Workforce 128,322 127,086 Number of vehicles sold(2) 2,722,883 2,550,286 DESIGN, PRODUCTION AND SALES 36 Research & development 40 Production sites 42 Worldwide production 48 Purchasing 49 Supply chain 50 Distribution network 51 Worldwide sales 54 Sales in Europe 60 Sales in Euromed-Africa (1) Published figures. 61 Sales in Eurasia (2) Renault Group including AVTOVAZ. 62 Sales in Asia-Pacific and China 63 Sales in Americas 64 114 years of history page This document is also published on the renault.com and declic@com websites. RENAULT ATLAS MARCH 2013 02 / 03 KEY FACTS AND FIGURES 2012 OCTOBER The Sandouville factory is transformed, ready to build the future Trafic. Renault enters into negotiations with JANUARY social partners, aimed at identifying and Renault further develops the entire developing the conditions and resources Mégane family, the brand's flagship required to guarantee a sound, sustai- for Quality, with the 2012 Collection.