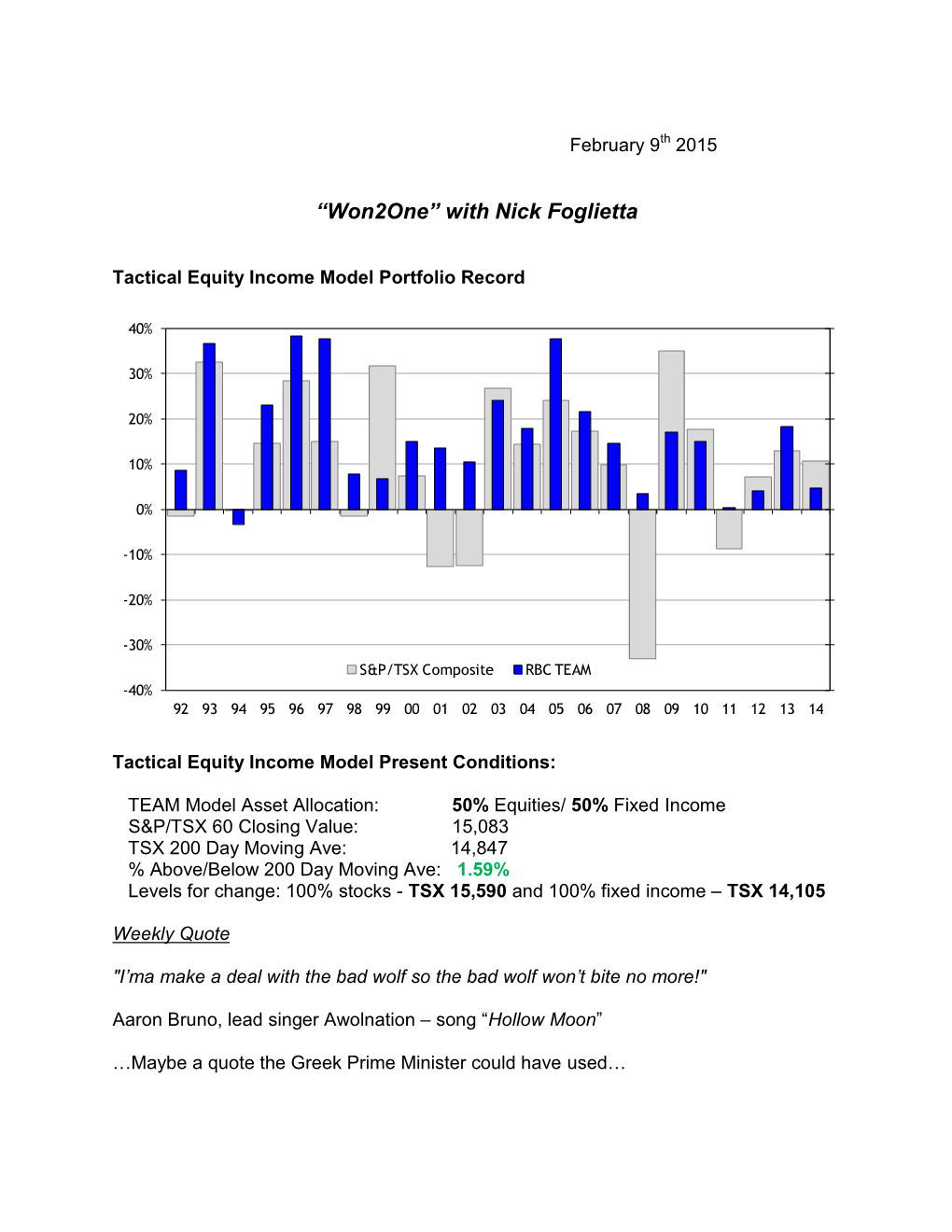

With Nick Foglietta

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Saladdays 23 Press Web.Pdf

23 THE TRASE THE ORIGINAL. SINCE NOW. DC_15S1.TRASE.GREEN.240X225+5.indd 1 17/02/15 17:57 One mag two Covers WHAT’S HOT Awolnation - Ramona Rosales Pushing - Federico Tognoli Editor In Chief/Founder - Andrea Rigano Art Director - Antonello Mantarro [email protected] Advertising - Silvia Rapisarda [email protected] Traduzioni - Fabrizio De Guidi Photographers Luca Benedet, Arianna Carotta, Alessio Fanciulli Oxilia, Alex Luise, Gaetano Massa, Fabio Montagner, Luca Pagetti, Enrico Rizzato, Federico Romanello, Ramona Rosales, Kari Rowe, Alberto Scattolin, Federico Tognoli Artwork Thunderbeard thunder-beard.blogspot.com Contributors Francesco Banci, Milo Bandini, Luca Basilico, Stefano Campagnolo, Marco Capelli, Matteo Cavanna, Cristiano Crepaldi, Young D, Fabrizio De Guidi, Flavio Ignelzi, Max Mameli, Marco Mantegazza, Simone Meneguzzo, Turi Messineo, Max Mbassadò, Angelo Mora(donas), Noodles, Eros Pasi, Marco Pasini, Davide Perletti, Salmo, SECSE, Alexandra Romano, Alessandro Scontrino, Marco ‘X-Man’ Xodo Stampa We Are Renegades / Rigablood Tipografia Nuova Jolly - Viale Industria 28 35030 Rubano (PD) Salad Days Magazine è una rivista registrata presso il 08 Black Hole 54 Cancer Bats Tribunale di Vicenza, N. 1221 del 04/03/2010. 12 Boost 58 Norm Will Rise 20 Awolnation 64 Family Album Get in touch 24 Justin “Figgy” Figueroa 72 Close Up - I Lottatori Del Rap www.saladdaysmag.com [email protected] 30 Don’t Sweat The Technique 76 Necro facebook.com/saladdaysmag 34 Lo Skateboard Alla Stretta Olimpica 81 Diane Arbus E Il Bambino Nel Parco twitter.com/SaladDays_it 37 Young Blood 84 Rebellion Fest Instagram - @saladdaysmagazine 40 Danny Trejo 87 Pseudo Slang L’editore è a disposizione di tutti gli interessati nel 44 Adolescents vs Svetlanas 92 Highlights collaborarecon testi immagini. -

8123 Songs, 21 Days, 63.83 GB

Page 1 of 247 Music 8123 songs, 21 days, 63.83 GB Name Artist The A Team Ed Sheeran A-List (Radio Edit) XMIXR Sisqo feat. Waka Flocka Flame A.D.I.D.A.S. (Clean Edit) Killer Mike ft Big Boi Aaroma (Bonus Version) Pru About A Girl The Academy Is... About The Money (Radio Edit) XMIXR T.I. feat. Young Thug About The Money (Remix) (Radio Edit) XMIXR T.I. feat. Young Thug, Lil Wayne & Jeezy About Us [Pop Edit] Brooke Hogan ft. Paul Wall Absolute Zero (Radio Edit) XMIXR Stone Sour Absolutely (Story Of A Girl) Ninedays Absolution Calling (Radio Edit) XMIXR Incubus Acapella Karmin Acapella Kelis Acapella (Radio Edit) XMIXR Karmin Accidentally in Love Counting Crows According To You (Top 40 Edit) Orianthi Act Right (Promo Only Clean Edit) Yo Gotti Feat. Young Jeezy & YG Act Right (Radio Edit) XMIXR Yo Gotti ft Jeezy & YG Actin Crazy (Radio Edit) XMIXR Action Bronson Actin' Up (Clean) Wale & Meek Mill f./French Montana Actin' Up (Radio Edit) XMIXR Wale & Meek Mill ft French Montana Action Man Hafdís Huld Addicted Ace Young Addicted Enrique Iglsias Addicted Saving abel Addicted Simple Plan Addicted To Bass Puretone Addicted To Pain (Radio Edit) XMIXR Alter Bridge Addicted To You (Radio Edit) XMIXR Avicii Addiction Ryan Leslie Feat. Cassie & Fabolous Music Page 2 of 247 Name Artist Addresses (Radio Edit) XMIXR T.I. Adore You (Radio Edit) XMIXR Miley Cyrus Adorn Miguel Adorn Miguel Adorn (Radio Edit) XMIXR Miguel Adorn (Remix) Miguel f./Wiz Khalifa Adorn (Remix) (Radio Edit) XMIXR Miguel ft Wiz Khalifa Adrenaline (Radio Edit) XMIXR Shinedown Adrienne Calling, The Adult Swim (Radio Edit) XMIXR DJ Spinking feat. -

Oaklandpostonline.Com February 14, 2018 // Volume 43

Oakland University’s THE Independent Student OAKLAND POST Newspaper Feb. 14, 2018 NO MERCY FOR DETROIT The Grizz Gang makes lots of noise as Men’s Basketball defeats Detroit Mercy in intense rivalry game PAGE 10 LETTER GRADES HIGH ROPES EXPANSION PROGRESS Grading system to change this fall Trustees introduce plan and funding Christopher Reed talks safety and to letter grade scale for recreation expansion schedule concerns of the OC PAGE 4 PAGE 5 PAGE 8 Photo by Elyse Gregory / The Oakland Post ontheweb Tune in online to listen to Samana Sheikh’s interview with Muslim fashion icon Ruma Begum about life and issues. thisweek www.oaklandpostonline.com February 14, 2018 // Volume 43. Issue 20 POLL OF THE WEEK What do you wish was a Winter Olympics award? A “Biggest snowboarding faceplant” B “Most vigorous curling sweeper” C “Best hockey boxing match” D “Most stylish team uniforms” Vote at www.oaklandpostonline.com LAST WEEK’S POLL What did you think of the Super Bowl? A) Fly Eagles, fly! 17 votes | 49% B) It’s impossible for me to care less PHOTO OF THE WEEK 7 votes | 20% C) The kid who took a selfie with JT tho PREGAME PARTY // Before the fan-favorite rivalry game against the University of Detroit 7 votes | 20% Mercy, alumni gathered in the Oakland Center to relive younger days and hang out with everyone’s favorite mascot: The Grizz. D) The Tom Brady era is over Photo // Brendan Triola 4 votes | 11% Submit a photo to [email protected] to be featured. View all submissions at oaklandpostonline.com THIS WEEK IN HISTORY February 16, 1962 Michigan State University - Oakland held its first dramatic play with “Alice in Wonderland.” February 14, 1963 MSU - Oakland officially became Oak- land University, totally independent of 9 15 19 Michgan State University. -

Alternative 2020

Mediabase Charts Alternative 2020 Published (U.S.) -- Currents & Recurrents January 2020 through December, 2020 Rank Artist Title 1 TWENTY ONE PILOTS Level Of Concern 2 BILLIE EILISH everything i wanted 3 AJR Bang! 4 TAME IMPALA Lost In Yesterday 5 MATT MAESON Hallucinogenics 6 ALL TIME LOW Monsters f/blackbear 7 ABSOFACTO Dissolve 8 POWFU Coffee For Your Head 9 SHAED Trampoline 10 UNLIKELY CANDIDATES Novocaine 11 CAGE THE ELEPHANT Black Madonna 12 MACHINE GUN KELLY Bloody Valentine 13 STROKES Bad Decisions 14 MEG MYERS Running Up That Hill 15 HEAD AND THE HEART Honeybee 16 PANIC! AT THE DISCO High Hopes 17 KILLERS Caution 18 WEEZER Hero 19 TWENTY ONE PILOTS The Hype 20 WALLOWS Are You Bored Yet? 21 LOVELYTHEBAND Broken 22 DAYGLOW Can I Call You Tonight? 23 GROUPLOVE Deleter 24 SUB URBAN Cradles 25 NEON TREES Used To Like 26 CAGE THE ELEPHANT Social Cues 27 WHITE REAPER Might Be Right 28 BLACK KEYS Shine A Little Light 29 LUMINEERS Life In The City 30 LANA DEL REY Doin' Time 31 GREEN DAY Oh Yeah! 32 MARSHMELLO Happier f/Bastille 33 AWOLNATION The Best 34 LOVELYTHEBAND Loneliness For Love 35 KENNYHOOPLA How Will I Rest In Peace If... 36 BAKAR Hell N Back 37 BLUE OCTOBER Oh My My 38 KILLERS My Own Soul's Warning 39 GLASS ANIMALS Your Love (Deja Vu) 40 BILLIE EILISH bad guy 41 MATT MAESON Cringe 42 MAJOR LAZER F/MARCUS Lay Your Head On Me 43 PEACH TREE RASCALS Mariposa 44 IMAGINE DRAGONS Natural 45 ASHE Moral Of The Story f/Niall 46 DOMINIC FIKE 3 Nights 47 I DONT KNOW HOW BUT THEY.. -

Sampling, Engagement, and Network Effects

Measuring Collective Attention in Online Content: Sampling, Engagement, and Network Effects Siqi Wu A thesis submitted for the degree of Doctor of Philosophy at The Australian National University March 2021 c 2021 by Siqi Wu All Rights Reserved Except where otherwise indicated, this thesis is my own original work. Siqi Wu 9 March 2021 Acknowledgments I would like to express my sincere gratitude to the people who have supported me in this Ph.D grind: • Prof. Lexing Xie. I am extremely honored to have Lexing to be my advisor. Her extensive knowledge in various fields and strong dedication to research motivate me to become a good researcher. • Dr. Marian-Andrei Rizoiu. Andrei is one of the smartest people that I know. He provided many insightful ideas when I was stuck. His research also sparked my interests in modeling online popularity. • Dr. Cheng Soon Ong. Cheng is my “think tank”. He never turned me down when I felt discouraged or desperately looked for advices, both in research and in life. • Members of the ANU Computational Media Lab – Swapnil Mishra, Quyu Kong, Alexander Mathews, Dawei Chen, Minjeong Shin, Dongwoo Kim, Jooyoung Lee, Rui Zhang, Alasdair Tran, Umanga Bista, Yuli Liu, Qiongkai Xu, and many others. I am grateful that I can work with a group of supportive talents. Much of my work is benefited from the discussions with them. • External collaborators – Yu-Ru Lin, Ali Mert Ertugrul, and Xian Teng from Univer- sity of Pittsburgh, Paul Resnick and James Park from Univeristy of Michigan, and Lu Cheng from Arizona State University. It has been a great pleasure to work with them. -

Chart-Topping Artists Headline Outdoor Music Festival in Redding, Calif

CHART-TOPPING ARTISTS HEADLINE OUTDOOR MUSIC FESTIVAL IN REDDING, CALIF. REDDING, Calif. (June 29, 2018) – Following a record year in 2017, the Redding Civic Auditorium recently wrapped up a successful spring that included several sold-out shows, plus the highest volume of events the venue has ever seen in a three-to fourth-month period. The Civic is following it up with its largest event yet – The Redd Sun Festival. The two-day outdoor music festival on Sept. 29-30 brings a day of rock ‘n’ roll plus back-to- back country music acts to the Redding Civic Auditorium’s huge lawn. The first day of the festival features rock headliner Awolnation, currently receiving major airplay on rock radio and having sat on the Billboard Hot 100 chart with its hit, “Handyman.” Awolnation’s previous Billboard hits include “Sail,” “I Am,” and “Hollow Moon.” They will take the festival’s big outdoor stage at 9 p.m.Saturday, following sets by fellow rock bands Candlebox, Lit, and Floater. Candlebox is best known for its hit, “Far Behind,” and Lit’s top charting hit was “My Own Worst Enemy.” Floater is based out of Portland, Ore., and has a significant Northern California following. Sunday’s lineup features county music headliner Eli Young Band, which has had five hits on the Billboard Hot 100 chart including “Even If It Breaks Your Heart,” “Crazy Girl,” and “Drunk Last Night.” Eli Young Band sold out Redding Civic Auditorium in 2014, and will kick off its 2018 set at 9 p.m., following a set by Frankie Ballard, whose Billboard hits include “Sunshine & Whiskey,” “Helluva Life,” and “Young & Crazy.” Carly Pearce, known for her hit song, “Every Little Thing,” will also play, with opener David Luning, a rising country star from the Bay Area. -

"A" - You're Adorable (The Alphabet Song) 1948 Buddy Kaye Fred Wise Sidney Lippman 1 Piano Solo | Twelfth 12Th Street Rag 1914 Euday L

Box Title Year Lyricist if known Composer if known Creator3 Notes # "A" - You're Adorable (The Alphabet Song) 1948 Buddy Kaye Fred Wise Sidney Lippman 1 piano solo | Twelfth 12th Street Rag 1914 Euday L. Bowman Street Rag 1 3rd Man Theme, The (The Harry Lime piano solo | The Theme) 1949 Anton Karas Third Man 1 A, E, I, O, U: The Dance Step Language Song 1937 Louis Vecchio 1 Aba Daba Honeymoon, The 1914 Arthur Fields Walter Donovan 1 Abide With Me 1901 John Wiegand 1 Abilene 1963 John D. Loudermilk Lester Brown 1 About a Quarter to Nine 1935 Al Dubin Harry Warren 1 About Face 1948 Sam Lerner Gerald Marks 1 Abraham 1931 Bob MacGimsey 1 Abraham 1942 Irving Berlin 1 Abraham, Martin and John 1968 Dick Holler 1 Absence Makes the Heart Grow Fonder (For Somebody Else) 1929 Lewis Harry Warren Young 1 Absent 1927 John W. Metcalf 1 Acabaste! (Bolero-Son) 1944 Al Stewart Anselmo Sacasas Castro Valencia Jose Pafumy 1 Ac-cent-tchu-ate the Positive 1944 Johnny Mercer Harold Arlen 1 Ac-cent-tchu-ate the Positive 1944 Johnny Mercer Harold Arlen 1 Accidents Will Happen 1950 Johnny Burke James Van Huesen 1 According to the Moonlight 1935 Jack Yellen Joseph Meyer Herb Magidson 1 Ace In the Hole, The 1909 James Dempsey George Mitchell 1 Acquaint Now Thyself With Him 1960 Michael Head 1 Acres of Diamonds 1959 Arthur Smith 1 Across the Alley From the Alamo 1947 Joe Greene 1 Across the Blue Aegean Sea 1935 Anna Moody Gena Branscombe 1 Across the Bridge of Dreams 1927 Gus Kahn Joe Burke 1 Across the Wide Missouri (A-Roll A-Roll A-Ree) 1951 Ervin Drake Jimmy Shirl 1 Adele 1913 Paul Herve Jean Briquet Edward Paulton Adolph Philipp 1 Adeste Fideles (Portuguese Hymn) 1901 Jas. -

Issue 161.Pmd

email: [email protected] website: nightshift.oxfordmusic.net Free every month. NIGHTSHIFT Issue 161 December Oxford’s Music Magazine 2008 Flying Fish! Little Fish on their crazy year inside NIGHTSHIFT: PO Box 312, Kidlington, OX5 1ZU. Phone: 01865 372255 NEWNEWSS Nightshift: PO Box 312, Kidlington, OX5 1ZU Phone: 01865 372255 email: [email protected] Online: nightshift.oxfordmusic.net THE ACADEMY will be renamed pub is currently owned by Greene the O2 Academy from 1st January King and they are searching for a 2009 after a partnership deal was new manager but as of yet struck between the mobile network everything is up in the air and the company and Live Nation, the current area manager is said not to majority shareholder company in be keen on live music. the Academy Music Group. The deal Allison Young, who has promoted follows on from Carling’s gigs at the Port, on St Clement’s, YOUNG KNIVES’ HENRY DARTNALL has been talking to Nightshift sponsorship of the venue expiring. for the last three and a half years about the band’s special ‘Homecoming’ gig at the Academy on Sunday A press release documenting the told Nightshift, “Our last night at 21st December, and his pride in the band’s acclaimed ‘Suprerabundance’ new partnership declared that “O2 the Port Mahon is on the 2nd album, released earlier this year. The Oxford show is part of a series of customers will gain priority access December. We are aware that there Academy Homecoming gigs at cities around the UK and will see Young to tickets to all gigs at the venues, is someone interested in the place; Knives taking over the entire venue and picking some of their favourite as well as other Live Nation events they, however, want to change it bands as support. -

To Search This List, Hit CTRL+F to "Find" Any Song Or Artist Song Artist

To Search this list, hit CTRL+F to "Find" any song or artist Song Artist Length Peaches & Cream 112 3:13 U Already Know 112 3:18 All Mixed Up 311 3:00 Amber 311 3:27 Come Original 311 3:43 Love Song 311 3:29 Work 1,2,3 3:39 Dinosaurs 16bit 5:00 No Lie Featuring Drake 2 Chainz 3:58 2 Live Blues 2 Live Crew 5:15 Bad A.. B...h 2 Live Crew 4:04 Break It on Down 2 Live Crew 4:00 C'mon Babe 2 Live Crew 4:44 Coolin' 2 Live Crew 5:03 D.K. Almighty 2 Live Crew 4:53 Dirty Nursery Rhymes 2 Live Crew 3:08 Fraternity Record 2 Live Crew 4:47 Get Loose Now 2 Live Crew 4:36 Hoochie Mama 2 Live Crew 3:01 If You Believe in Having Sex 2 Live Crew 3:52 Me So Horny 2 Live Crew 4:36 Mega Mixx III 2 Live Crew 5:45 My Seven Bizzos 2 Live Crew 4:19 Put Her in the Buck 2 Live Crew 3:57 Reggae Joint 2 Live Crew 4:14 The F--k Shop 2 Live Crew 3:25 Tootsie Roll 2 Live Crew 4:16 Get Ready For This 2 Unlimited 3:43 Smooth Criminal 2CELLOS (Sulic & Hauser) 4:06 Baby Don't Cry 2Pac 4:22 California Love 2Pac 4:01 Changes 2Pac 4:29 Dear Mama 2Pac 4:40 I Ain't Mad At Cha 2Pac 4:54 Life Goes On 2Pac 5:03 Thug Passion 2Pac 5:08 Troublesome '96 2Pac 4:37 Until The End Of Time 2Pac 4:27 To Search this list, hit CTRL+F to "Find" any song or artist Ghetto Gospel 2Pac Feat. -

Café Shapiro 2017 Anthology.Indd

20th Annual Café Shapiro Anthology 2017 February 6, 2017 February 7, 2017 February 9, 2017 February 13, 2017 February 15, 2017 Selected Poems & Short Stories Café Shapiro 2017 Anthology ©2017 The authors retain all copyright interests in their respective works. Reprinted by permission. All rights reserved. No part of this book may be reproduced without permission of the authors. Please contact [email protected] for permission information. Original Artwork provided by: Karen Duan University of Michigan Senior, Major: Architecture; Minor: Creative Writing Image is titled Eusapia - a graphite on bristol drawing, and a 2D translation of Italo Calvino’s fantastical narrative Invisible Cities. Introduction Introduction Welcome to the 20th Annual Café Shapiro! I am excited to introduce the 20th Annual Cafe Shapiro anthology and invite you to read the following inspiring and thoughtful University of Michigan stu- dent authored poems and short stories. These works will draw you into the creative process, welcome you to think and rethink your assumptions, and connect you with the students through their individual expression. You will find a unique window into the Michigan learning experience. When Cafe Shapiro first launched twenty years ago, it was a bold experiment, a student coffee break designed as part of the University’s Year of the Hu- manities and Arts (YoHA). As the University celebrates its bicentennial, Cafe Shapiro is an example of how past innovations become a part of current cam- pus traditions. YoHA set out to explore the role of the arts and humanities in civic and community life through a variety of programs. Twenty years later, Cafe Shapiro continues its tradition of featuring undergraduate student writers nominated by their Professors to perform their works and through during so continues to demonstrate the value of the arts and humanities. -

Billboard Magazine

THE HOT 100 ODD COUPLE Wiz Khalifa and Charlie Puth on their No. 1 hit PITCH PERFECT 2’S 91 STEALTH SOUNDTRACK No tracklist, no ‘Cups’ -.1 ...no worries? the BILLBOARD MUSIC2015 AWARDS STARRING Hosts Ludacris and Chrissy Teigen: ‘We’re turning the BBMAs into a party!’ May 16, 2015 | billboard.com Performer portfolio: Hozier, Pete Wentz, Nick Jonas and Meghan Trainor Stars reveal awards show horror stories: ‘...then the monkey bit Shakira’ Baller’s guide to Vegas: Pet a tiger, shop with Nas UK £5.50 WAKE UP ON THE RIGHT SIDE OF THE PLANE. Catch some Z’s when catching your next flight. Arriving ready is just one of the perks of flat-bed seats, Westin Heavenly® In-Flight Bedding, and everything else available on all our nonstops from LAX to JFK. KEEP CLIMBING AD E LTA Delta One available on long-haul international flights, and on transcontinental flights between JFK and LAX, and JFK and SFO. Get the details at delta.com/deltaone billboard (c SELIM LC and Nielsen Music, Inc.LC All rights reserved. “I’ve really been working to get here,” says T-Wayne of his chart leap. I. -- . "nil om/biz for complete rules and explanations. © 2015, Prometheus Global Media, L © 2015, Prometheus om/biz for complete rules and explanations. Title CERTIFICATION Artist 2 Weeks Ago Last Week This Week PRODUCER (SONGWRITER) IMPRINT/PROMOTION LABEL Peak Position Weeks On Chart #1 AG 18 4 WK S See You Again Wiz Khalifa Feat. Charlie Puth T-Wayne Whips Up A 0 DJ FRANK E,C.PUTH,A.CEDAR (J.FRANKS,A.CEDAR,C.J.THOMAZ,C.PUTH) UNIVERSAL STUDIOS/ATLANTIC/RRP sic, sales data as compiled by Nielsen Music and streaming activity data by online music sources tracked by Nielsen Music. -

CALL # AUTHOR TITLE ATOS Book Level: AR Points: Easy Reader E HAL Hall, Kirsten. a Bad, Bad Day 0.3 0.5 Easy Reader E MEI Meis

ATOS Book CALL # AUTHOR TITLE Level: AR Points: Easy Reader E HAL Hall, Kirsten. A bad, bad day 0.3 0.5 Easy Reader E MEI Meisel, Paul. See me run 0.3 0.5 Easy Reader E REM Remkiewicz, Frank. Gus gets scared 0.3 0.5 Easy Reader E Sul Sullivan, Paula. Todd's box 0.3 0.5 Easy Reader E Bal Ballard, Peg. Gifts for Gus : the sound of G 0.4 0.5 Easy Reader E COX Coxe, Molly. Big egg 0.4 0.5 Easy Reader E Mac McPhail, David, Big brown bear 0.4 0.5 Easy Reader E Mac McPhail, David, Big brown bear 0.4 0.5 Easy Reader E Mac McPhail, David, Rick is sick 0.4 0.5 Easy Reader E WIL Wilhelm, Hans, No kisses, please! 0.4 0.5 Easy Reader E WIL Wilhelm, Hans, Ouch! : it hurts! 0.4 0.5 Easy Reader E BON Bonsall, Crosby, Mine's the best 0.5 0.5 Easy Reader E Buc Buck, Nola. Sid and Sam 0.5 0.5 Easy Reader E Hol Holub, Joan. Scat cats! 0.5 0.5 Easy Reader E Las Lascaro, Rita. Down on the farm 0.5 0.5 Easy Reader E Mor Moran, Alex. Popcorn 0.5 0.5 Easy Reader E Tri Trimble, Patti. What day is it? 0.5 0.5 Easy Reader E Wei Weiss, Ellen, Twins in the park 0.5 0.5 Easy Reader E Kli Amoroso, Cynthia. What do I bring? : the sound of br 0.6 0.5 Easy Reader E Bal Ballard, Peg.