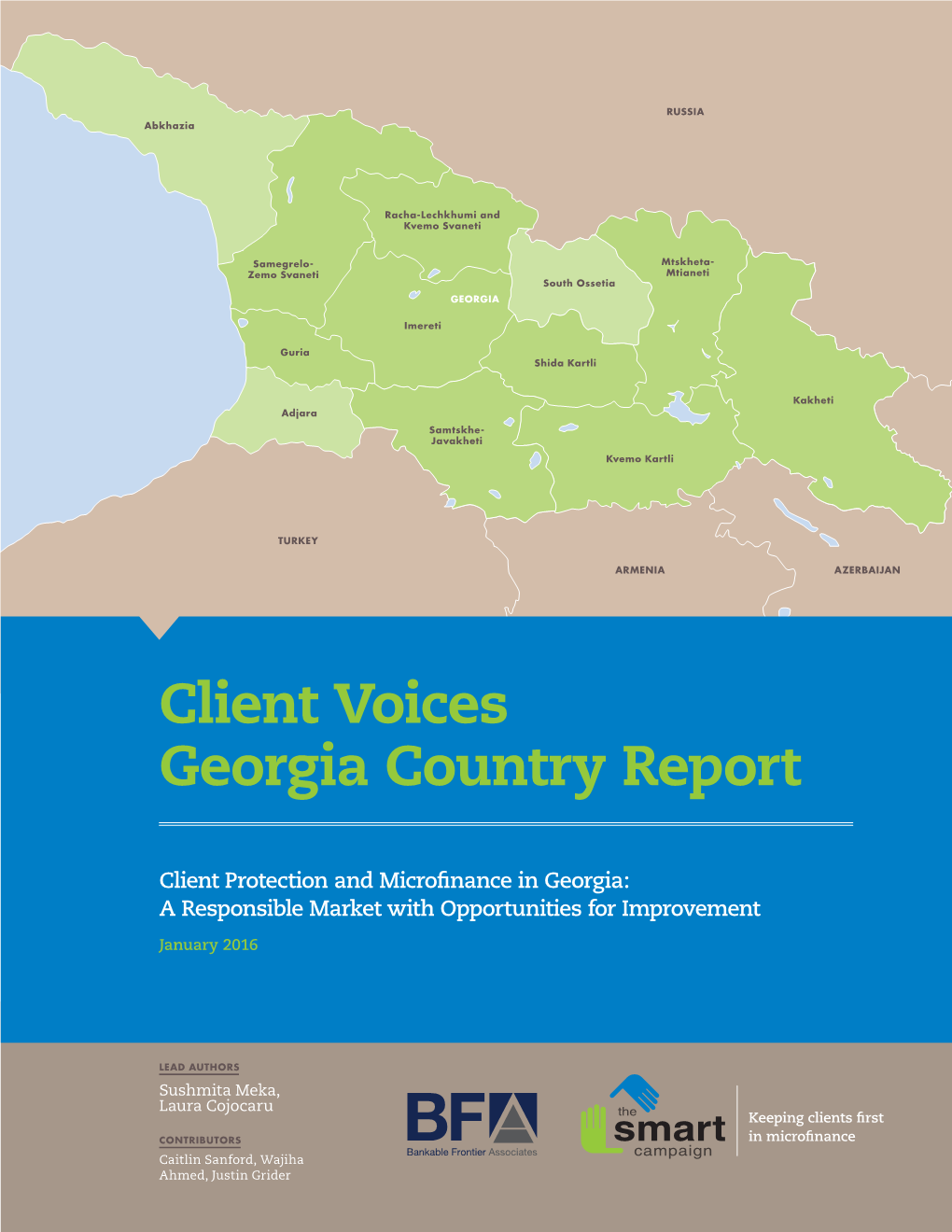

Client Voices Georgia Country Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Mineral Industry of Georgia in 2011

2011 Minerals Yearbook GEORGIA U.S. Department of the Interior September 2013 U.S. Geological Survey THE MINERAL INDUSTRY OF GEORGIA By Elena Safirova Prior to the proclamation of Georgian independence in in mining was $40.2 million, or 3.6% of the total FDI in the 1991, a range of mineral commodities were mined in Georgia, country (National Statistics Office of Georgia, 2012b). including arsenic, barite, bentonite, coal, copper, diatomite, lead, In 2011, Georgia ran a substantial trade deficit—the total manganese, zeolites, and zinc, among others. The country’s value of its exports ($2.19 billion) was greatly exceeded by metallurgical sector produced ferroalloys and steel. Since 1991, the total value of its imports ($7.06 billion). The country’s production of many of these mineral commodities had ceased or major export trade partners were, in order of value, Azerbaijan been significantly reduced. (which received 19.5% of Georgia’s exports), Turkey (10.4%), Following the Rose Revolution of 2003, the Government Armenia (10.2%), Kazakhstan (7.2%), the United States (6.6%), determined to revive the country’s industry. In 2007, Georgia Ukraine (6.5%), and Canada (5.2%). Its major import trade sold its three leading enterprises—Chiatura Manganese, partners were, in order of value, Turkey (which supplied 18.0% Vartzikhe Hydropower, and Zestafoni Ferroalloys to Stemcor of Georgia’s imports), Ukraine (10.0%), Azerbaijan (8.7%), Co. of the United Kingdom. Before the sale, the enterprises China (7.4%), Germany (6.8%), and Russia (5.5%). Mineral were in a difficult financial situation; for example, Zestafoni commodities, especially metals, played a significant role in Ferroalloys owed the Government $35 million in taxes. -

2018 Prospectus

Joint Stock Company Microfinance Organization Crystal (Identification Code: 212896570) Final Prospectus on the Emission of Bonds Inportant information for investors: Prospective investor must read the following disclaimer before continuing. The following disclaimer applies to the attached prospectus (the “Prospectus”) and prospective investor is therefore advised to read this carefully before reading, accessing or making any other use of the attached Prospectus. By accessing and using the Prospectus (including for investment purposes), prospective investor agrees to be bound by the following terms and conditions (modified from time to time). If the prospective investor receives the Prospectus via electronic means, he/she acknowledges that this electronic transmission (with attached Prospectus) is confidential and intended only for him/her. Therefore the investor agrees that he/she will not forward, reproduce or publish this electronic transmission or the attached Prospectus to any other person. The present Prospectus may be supplemented with additional information as stipulated by the law. Limitation of the Liability: Approval of the Prospectus by the National Bank applies to the Prospectus form only and may not be regarded as a conclusion on the accuracy of its content or the value of the investment described therein. Except for the cases stipulated by the applicable laws, no person other than the issuer, including the placement agent, the bondholders’ representative, the calculation and paying agent, the registrar, other advisers to the company nor any of their affiliates, Directors, Advisors or Agent shall bear responsibility for the content of the present Prospectus, the authenticity or completeness of the information presented therein, or any statement made by them or on behalf of them with regard to the company or issuance and offering of securities described in the present Prospectus. -

Who Owned Georgia Eng.Pdf

By Paul Rimple This book is about the businessmen and the companies who own significant shares in broadcasting, telecommunications, advertisement, oil import and distribution, pharmaceutical, privatisation and mining sectors. Furthermore, It describes the relationship and connections between the businessmen and companies with the government. Included is the information about the connections of these businessmen and companies with the government. The book encompases the time period between 2003-2012. At the time of the writing of the book significant changes have taken place with regards to property rights in Georgia. As a result of 2012 Parliamentary elections the ruling party has lost the majority resulting in significant changes in the business ownership structure in Georgia. Those changes are included in the last chapter of this book. The project has been initiated by Transparency International Georgia. The author of the book is journalist Paul Rimple. He has been assisted by analyst Giorgi Chanturia from Transparency International Georgia. Online version of this book is available on this address: http://www.transparency.ge/ Published with the financial support of Open Society Georgia Foundation The views expressed in the report to not necessarily coincide with those of the Open Society Georgia Foundation, therefore the organisation is not responsible for the report’s content. WHO OWNED GEORGIA 2003-2012 By Paul Rimple 1 Contents INTRODUCTION .........................................................................................................3 -

6. Imereti – Historical-Cultural Overview

SFG2110 SECOND REGIONAL DEVELOPMETN PROJECT IMERETI REGIONAL DEVELOPMENT PROGRAM IMERETI TOURISM DEVELOPMENT STRATEGY Public Disclosure Authorized STRATEGIC ENVIRONMENTAL, CULTURAL HERITAGE AND SOCIAL ASSESSMENT Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Tbilisi, December, 2014 ABBREVIATIONS GNTA Georgia National Tourism Administration EIA Environnemental Impact Assessment EMP Environmental Management Plan EMS Environmental Management System IFI International Financial Institution IRDS Imereti Regional Development Strategy ITDS Imereti Tourism Development Strategy MDF Municipal Development Fund of Georgia MoA Ministry of Agriculture MoENRP Ministry of Environment and Natural Resources Protection of Georgia MoIA Ministry of Internal Affairs MoCMP Ministry of Culture and Monument Protection MoJ Ministry of Justice MoESD Ministry of Economic and Sustaineble Developmnet NACHP National Agency for Cultural Heritage Protection PIU Project Implementation Unit PPE Personal protective equipment RDP Regional Development Project SECHSA Strategic Environmental, Cultural Heritage and Social Assessment WB World Bank Contents EXECUTIVE SUMMARY ........................................................................................................................................... 0 1. INTRODUCTION ........................................................................................................................................... 14 1.1 PROJECT CONTEXT ............................................................................................................................... -

146 Forty Seasons of Excavation: Nokalakevi

This article has been published by the Georgian National Museum in Iberia-Colchis, available online at http://dspace.nplg.gov.ge/bitstream/1234/242318/1/Iberia_Kolxeti_2017_N13.pdf. Copyright © 2017, Georgian National Museum. Paul Everill, Davit Lomitashvili, Nikoloz Murgulia, Ian Colvin, Besik Lortkipanidze FORTY SEASONS OF EXCAVATION: NOKALAKEVI-TSIKHEGOJI-ARCHAEOPOLIS Abstract. The ruins in the small village of Nokalakevi in Samegrelo, west Georgia, have attracted schol- arly interest since the first half of the 19th century. They were first excavated in 1930, confirming their identification as the remains of the fortress of Archaeopolis mentioned in early Byzantine historical sources, and known as Tsikhegoji or ‘the triple-walled fortress’ by the Georgian chroni- clers. The 40th season of excavation took place in 2015, part of an on-going collaboration be- tween the Anglo-Georgian Expedition to Nokalakevi, established in 2001, and the S. Janashia Museum expedition to Nokalakevi, which started work on the site in 1973. The fortifications en- close a naturally defensible area of approximately 20ha, with a steep limestone river gorge to the north, west and (to a lesser extent) the south, and a hilltop citadel standing more than 200m above the lower town. The site has seen human activity since at least the 8th century BC, with indications of a much earlier presence in the area. This paper seeks to outline the key results of the 40 seasons of excavation, against the backdrop of the shifting political landscape of Georgia. Introduction. In 2015 the multi-period site of Nokalakevi in western Georgia hosted its 40th season of exca- vation. -

Geopolitics of the Cancelled Anaklia Project

BLACK SEA STRATEGY PAPERS Geopolitics of the Cancelled Anaklia Project Maximilian Hess & Maia Otarashvili All rights reserved. Printed in the United States of America. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording, or any information storage and retrieval system, without permission in writing from the publisher. Authors: Maximilian Hess & Maia Otarashvili The views expressed in this report are those of the author alone and do not necessarily reflect the position of the Foreign Policy Research Institute, a non-partisan organization that seeks to publish well-argued, policy- oriented articles on American foreign policy and national security priorities. Eurasia Program Leadership Director: Chris Miller Deputy Director: Maia Otarashvili Editing: Thomas J. Shattuck Design: Natalia Kopytnik © 2020 by the Foreign Policy Research Institute October 2020 OUR MISSION The Foreign Policy Research Institute is dedicated to producing the highest quality scholarship and nonpartisan policy analysis focused on crucial foreign policy and national security challenges facing the United States. We educate those who make and influence policy, as well as the public at large, through the lens of history, geography, and culture. Offering Ideas In an increasingly polarized world, we pride ourselves on our tradition of nonpartisan scholarship. We count among our ranks over 100 affiliated scholars located throughout the nation and the world who appear regularly in national and international media, testify on Capitol Hill, and are consulted by U.S. government agencies. Educating the American Public FPRI was founded on the premise that an informed and educated citizenry is paramount for the U.S. -

Causes of War Prospects for Peace

Georgian Orthodox Church Konrad-Adenauer-Stiftung CAUSES OF WAR PROS P E C TS FOR PEA C E Tbilisi, 2009 1 On December 2-3, 2008 the Holy Synod of the Georgian Orthodox Church and the Konrad-Adenauer-Stiftung held a scientific conference on the theme: Causes of War - Prospects for Peace. The main purpose of the conference was to show the essence of the existing conflicts in Georgia and to prepare objective scientific and information basis. This book is a collection of conference reports and discussion materials that on the request of the editorial board has been presented in article format. Publishers: Metropolitan Ananya Japaridze Katia Christina Plate Bidzina Lebanidze Nato Asatiani Editorial board: Archimandrite Adam (Akhaladze), Tamaz Beradze, Rozeta Gujejiani, Roland Topchishvili, Mariam Lordkipanidze, Lela Margiani, Tariel Putkaradze, Bezhan Khorava Reviewers: Zurab Tvalchrelidze Revaz Sherozia Giorgi Cheishvili Otar Janelidze Editorial board wishes to acknowledge the assistance of Irina Bibileishvili, Merab Gvazava, Nia Gogokhia, Ekaterine Dadiani, Zviad Kvilitaia, Giorgi Cheishvili, Kakhaber Tsulaia. ISBN 2345632456 Printed by CGS ltd 2 Preface by His Holiness and Beatitude Catholicos-Patriarch of All Georgia ILIA II; Opening Words to the Conference 5 Preface by Katja Christina Plate, Head of the Regional Office for Political Dialogue in the South Caucasus of the Konrad-Adenauer-Stiftung; Opening Words to the Conference 8 Abkhazia: Historical-Political and Ethnic Processes Tamaz Beradze, Konstantine Topuria, Bezhan Khorava - A -

CAUCASIA and the FIRST BYZANTINE COMMONWEALTH: CHRISTIANIZATION in the CONTEXT of REGIONAL COHERENCE an NCEEER Working Paper by Stephen H

CAUCASIA AND THE FIRST BYZANTINE COMMONWEALTH: CHRISTIANIZATION IN THE CONTEXT OF REGIONAL COHERENCE An NCEEER Working Paper by Stephen H. Rapp, Jr. Independent Scholar National Council for Eurasian and East European Research University of Washington Box 353650 Seattle, WA 98195 [email protected] http://www.nceeer.org/ TITLE VIII PROGRAM Project Information* Principal Investigator: Stephen H. Rapp, Jr. NCEEER Contract Number: 826-5g Date: January 19, 2012 Copyright Information Individual researchers retain the copyright on their work products derived from research funded through a contract or grant from the National Council for Eurasian and East European Research (NCEEER). However, the NCEEER and the United States Government have the right to duplicate and disseminate, in written and electronic form, reports submitted to NCEEER to fulfill Contract or Grant Agreements either (a) for NCEEER’s own internal use, or (b) for use by the United States Government, and as follows: (1) for further dissemination to domestic, international, and foreign governments, entities and/or individuals to serve official United States Government purposes or (2) for dissemination in accordance with the Freedom of Information Act or other law or policy of the United States Government granting the public access to documents held by the United States Government. Neither NCEEER nor the United States Government nor any recipient of this Report may use it for commercial sale. * The work leading to this report was supported in part by contract or grant funds provided by the National Council for Eurasian and East European Research, funds which were made available by the U.S. Department of State under Title VIII (The Soviet-East European Research and Training Act of 1983, as amended). -

A Historical-Geographic Review of Modern Abkhazia

A Historical-Geographic Review of Modern Abkhazia by T. Beradze, K. Topuria, B Khorava Abkhazia (Abkhazeti) – the farthest North-Western part of Georgia is situated between the rivers Psou and Inguri on the coast of the Black Sea. The formation of Abkhazia within the borders is the consequence of complicated ethno-political processes. Humans first settled on the territory of modern Abkhazia during the Paleolithic Era. Abkhazia is the place where Neolithic, Bronze and Early Iron Eras are represented at their best. The first Georgian state – the Kingdom of Egrisi (Kolkheti), formed in 15. to 14. century BC, existed till the 2.century BC. It used to include the entire South-Eastern and Eastern parts of the Black Sea littoral for ages. The territory of modern Abkhazia was also a part of the Egrisi Kingdom. Old Greek historical sources inform us that before the new millennium, the territory between the rivers Psou and Inguri was only populated with tribes of Georgian origin: the Kolkhs, Kols, Svan-Kolkhs, Geniokhs. The Kingdom of Old Egrisi fell at the end of the 2.century BC and was never restored till 2.century AD. Old Greeks, Byzantines and Romans called this state - Lazika, the same Lazeti, which was associated with the name of the ruling dynasty. In 3. and 4. centuries AD, entire Western Georgia, including the territory of present Abkhazia, was part of this state. Based on the data of Byzantine authors, the South-East coastline part of the territory – between rivers Kodori and Inguri - belonged to the Odishi Duchy. The source of the Kodori River was occupied by the Georgian tribe of Misimians that was directly subordinated to the King of Egrisi (Lazeti). -

Regional Power Transmission Enhancement Project

1 Initial Environmental Examination April 2013 GEO: Regional Power Transmission Enhancement Project Prepared by Irakli Kaviladze for the Asian Development Bank. 2 CURRENCY EQUIVALENTS (As of 1 May 2013) Currency unit 1 GEL = 0.61 USD $ 1 USD $ = 1.65 GEL ABBREVIATIONS - ADB Asian Development Bank - APA Agency of Protected Areas - CEMP Construction Environmental Management Plan - CSC Construction Supervision Consultant - EA Executing agency - EIA Environmental Impact Assessment - EMP Environmental Management Plan - ESIA Environmental and Social Impact Assessment - GoG Government of Georgia - GRL Georgia Red List - GSE Georgia State Electrosystem - IEE Initial Environmental Examination - IEEE Institute of Electrical and Electronics Engineers - IMO Independent Monitoring Organization - KNP Kolkheti National Park - LARP Land acquisition and resettlement plan - NEA National Environmental Agency - NGO Non-governmental organization - PCB polychlorinated biphenyl - PIU Project Implementation Unit (within GSE) - SCADA Supervisory Control and Data Acquisition - SPS Safeguard Policy Statement (of ADB, June 2009) - TL Transmission line - UNFCCC United Nations Framework Convention on Climate Change 3 CONTENTS A Executive Summary 5 A.1 Policy, Legal, and Administrative Framework 6 A.2 Project Description 7 A.3 Description of the Environment (Baseline Data) 7 A.4 Anticipated Environmental Impacts and Mitigation Measures 10 A.5 Analysis of Alternatives 11 A.6 Information Disclosure, Consultation, and Participation 12 A.7 Grievance Redress Mechanism 12 -

Anaklia Deep Sea Port a New Strategic Pivot In

May 2019 Research Paper Beka Kiria Anaklia’s deep sea port – a new strategic pivot in Eurasia Photo: Anaklia port in Georgia. The design will bypass competing ports in the region with Superior connections to existing rail and road infrastructure, state-of-the-art equipment and communications infrastructure, berthing for 10,000 TEU vessels, flexibility for multiple cargo and vessel types, including dry bulk facility. Source: Anaklia Development Consortium Summary • The construction of Anaklia’s port will reshape not only the South Caucasus security environment but also diversify the landlocked Central Asian countries security landscape. • Through Anaklia, the US and the EU could easily reach landlocked Central Asian countries and allowing the EU to intensify the Central Asia strategy. • Anaklia could become instrumental in unfolding the U.S. Asia rebalancing strategy while China’s Belt and Road initiative is on the rise. • Georgia’s ports infrastructure development could support the process of re- establishment of the Greater Central Asian States Union under the EU’s flagship based on prospects of continental trade through Anaklia port and the development of common frameworks for economic policies and customs. • Through Anaklia bidding on Central Asian Union as a sub-strategy of the U.S. rebalancing strategy along the strong presence of Euro-Atlantic institutions in the region will undermine Russia’s sphere of influence. • Anaklia could shift the gravity of Russia's ‘sphere of influence’ strategy from South Caucasus to Central Asia. Potentially allowing Georgia and Ukraine to become NATO and EU members. GAGRA INSTITUTE – FIRST FULLY CLOUD OPERATED INDEPENDENT POLICY THINK-TANK 2 Introduction Anaklia is Europe’s easternmost seaport in Georgia and strategically the most important first deep-sea port on the eastern coast of the Black Sea. -

CONSTITUTION of GEORGIA We, the Citizens of Georgia, Whose Firm Will Is to Establish a Democratic Social Order, Economic Freedom

CONSTITUTION OF GEORGIA We, the citizens of Georgia, whose firm will is to establish a democratic social order, economic freedom, a rule-of-law and a social state, to secure universally recognized human rights and freedoms, to enhance state independence and peaceful relations with other peoples, drawing inspiration from centuries-old traditions of statehood of the Georgian nation and the historical-legal legacy of the Constitution of Georgia of 1921, proclaim the present Constitution before God and the nation. Constitutional Law of Georgia No 3710 of 15 October 2010 - LHG I, No 62, 5.11.2010, Art. 379 CHAPTER ONE General Provisions Article 1 1. Georgia shall be an independent, unified, and indivisible state, as confirmed by the Referendum of 31 March 1991, held throughout the territory of the country, including the Autonomous Soviet Socialist Republic of Abkhazia and the Former Autonomous Region of South Ossetia, and by the Act of Restoration of State Independence of Georgia of 9 April 1991. 2. The political structure of the State of Georgia shall be a democratic republic. 3. “Georgia” shall be the name of the State of Georgia. Article 2 1. The territory of the State of Georgia shall be determined as of 21 December 1991. The Constitution and legislation of Georgia shall acknowledge the territorial integrity of Georgia and the inviolability of state borders recognized by the world community of nations and international organizations. 2. Alienation/transfer of the territory of Georgia shall be prohibited. The state borders may be changed only by a bilateral agreement concluded with a neighboring state.