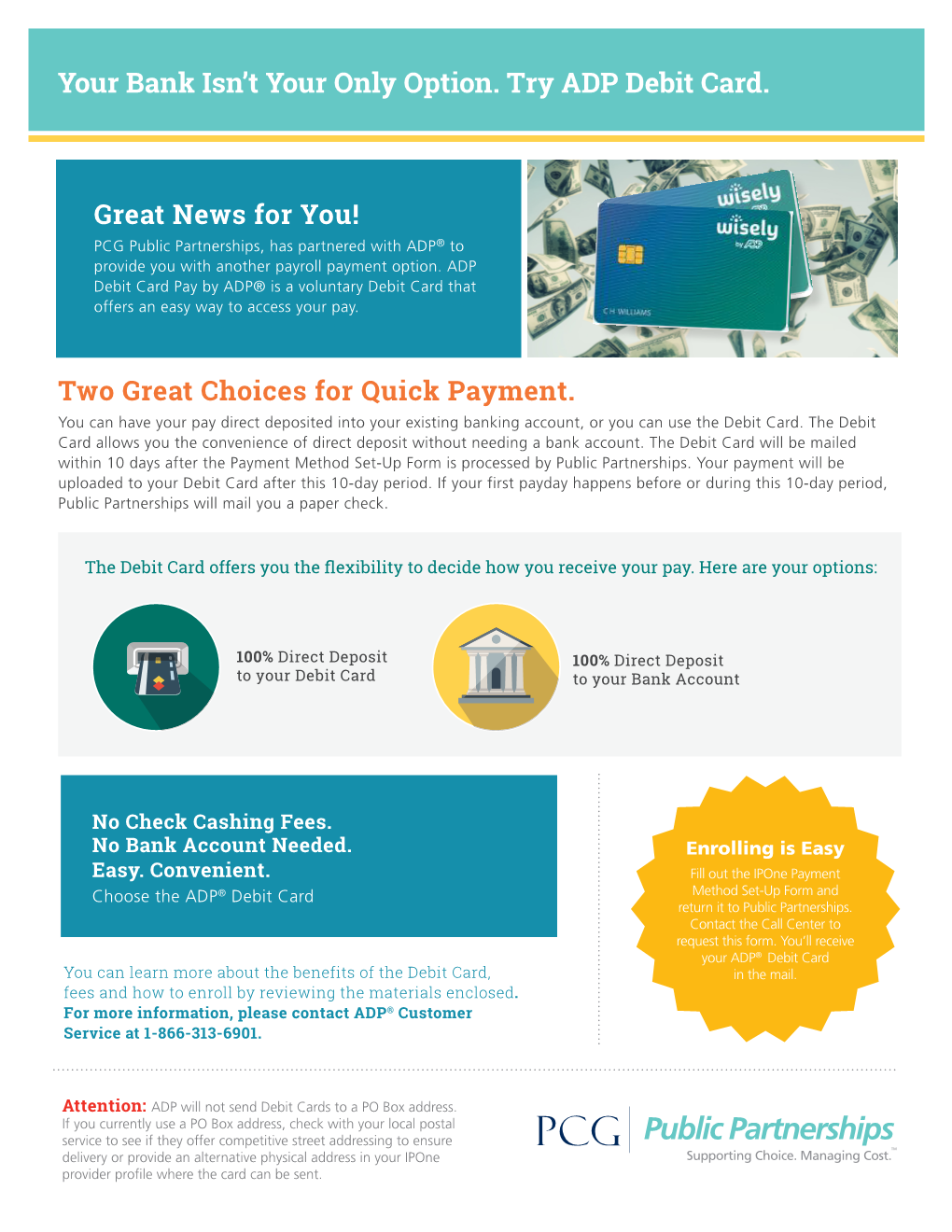

ADP Debit Card

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

RD Instruction 1902-A

RD Instruction 1902-A PART 1902 - SUPERVISED BANK ACCOUNTS Subpart A – Supervised Bank Accounts of Loan, Grant, and Other Funds TABLE OF CONTENTS Sec. Page 1902.1 General. 1 1902.2 Policies concerning disbursement of funds. 2 1902.3 Procedures to follow in fund disbursement. 3 1902.4 Establishing MFH reserve accounts in a supervised bank account. 3 (a) General requirements. 4 (b) Deposits and account activity statements. 5 1902.5 [Reserved] 5 1902.6 Establishing supervised bank accounts. 5 1902.7 Pledging collateral for deposit of funds in supervised bank accounts. 7 1902.8 Authority to establish and administer supervised bank accounts. 8 1902.9 Deposits. 8 (a) Deposit by Rural Development personnel. 8 (b) Deposits by borrowers. 10 1902.10 Withdrawals. 10 1902.11 Servicing Office records. 12 1902.12 - 1902.13 [Reserved] 12 1902.14 Reconciliation of accounts. 13 1902.15 Closing accounts. 13 1902.16 Request for withdrawals by State Director. 16 1902.17 - 1902.49 [Reserved] 16 1902.50 OMB control number. 16 Exhibit A - [Reserved] Exhibit B - Interest-Bearing Deposit Agreement o0o (10-12-05) SPECIAL PN RD Instruction 1902-A PART 1902 - SUPERVISED BANK ACCOUNTS Subpart A - Supervised Bank Accounts of Loan, Grant, and Other Funds § 1902.1 General. This subpart prescribes the policies and procedures in establishing and using supervised bank accounts, and in placing Multi-Family Housing (MFH) reserve accounts in supervised bank accounts. RD Instruction 2018-D provides the procedures Servicing Officials should follow in ordering loan and grant disbursements. (a) Borrowers as referred to in this instruction include both loan and grant recipients. -

Word Files Coverted

About MasterCard International: MasterCard International is a leading global payments solutions company that provides a broad variety of innovative services in support of their global members' credit, deposit access, electronic cash, business-to-business and related payment programs. MasterCard international manages a family of well-known, widely accepted payment cards brands including MasterCard®, Maestro®, and Cirrus® and serves financial institutions, consumers and businesses in over 210 countries and territories. What is a Debit Card: Maestro® is the Global Debit Card cum ATM Card product of MasterCard International. This card can be used to make on-line bill payments through 49,000 Point of Sale (POS) terminals in India and 70,00,000 merchant establishments worldwide exhibiting “MAESTRO” logo. In other words the Debit Card holder can pay their bills, at shops exhibiting “Maestro” Logo, using this card instead by cash or cheque. The card holder need not carry cash in future when all the shops provide this facility. SIB's Debit Card can also be used as an ATM card within the ATM network of the Bank. People around the world prefer debit card over credit card since the spending can be restricted to what they have in their account. Since payment is effected only if there is available balance in the customer's account, it is absolutely risk-free for the banks. SIB plans to issue debit cards liberally as an added convenience to its customers which in turn reduces the pressure on cash transactions at the counters. How is CIRRUS relevant to other bank's Maestro Card holders: SIB has acquired “CIRRUS”, the product of MasterCard International. -

(Automated Teller Machine) and Debit Cards Is Rising. ATM Cards Have A

Consumer Decision Making Contest 2001-2002 Study Guide ATM/Debit Cards The popularity of ATM (automated teller machine) and debit cards is rising. ATM cards have a longer history than debit cards, but the National Consumers League estimates that two-thirds of American households are likely to have debit cards by the end of 2000. It is expected that debit cards will rival cash and checks as a form of payment. In the future, “smart cards” with embedded computer chips may replace ATM, debit and credit cards. Single-purpose smart cards can be used for one purpose, like making a phone call, or riding mass transit. The smart card keeps track of how much value is left on your card. Other smart cards have multiple functions - serve as an ATM card, a debit card, a credit card and an electronic cash card. While this Study Guide will not discuss smart cards, they are on the horizon. Future consumers who understand how to select and use ATM and debit cards will know how to evaluate the features and costs of smart cards. ATM and Debit Cards and How They Work Electronic banking transactions are now a part of the American landscape. ATM cards and debit cards play a major role in these transactions. While ATM cards allow us to withdraw cash to meet our needs, debit cards allow us to by-pass the use of cash in point-of-sale (POS) purchases. Debit cards can also be used to withdraw cash from ATM machines. Both types of plastic cards are tied to a basic transaction account, either a checking account or a savings account. -

Personal Deposit Account Agreement and Schedule of Fees Effective

Personal Deposit Account Agreement and Schedule of Fees Effective: September 15, 2021 TABLE OF CONTENTS AGREEMENT FOR YOUR ACCOUNT ..................................................................................... 5 Account Funding .................................................................................................................................................................. 5 Changes to This Agreement ................................................................................................................................................ 5 Closing an Account .............................................................................................................................................................. 5 Compliance with Laws and Regulations .............................................................................................................................. 5 Financial Information ........................................................................................................................................................... 6 General Use of Credit File Information ................................................................................................................................ 6 Governing Law .................................................................................................................................................................... 6 Information You Give Us .................................................................................................................................................... -

ATM and Debit Card Safety Tips P1

ATM DEBIT CARD SAFETY TIPS Sensible Steps for: Personal Safety Account Security Identity Theft Protection ATM and Debit Card Safety and Security ith the banking convenience made possible with Automated Teller Machines WW (ATMs) and other Point of Sale terminals comes an increased need for security and personal caution. This includes protecting your ATM card number, Debit Card number, Personal Identication Number (PIN), and cash, and being aware of the condition of the machine and your surroundings. It’s no longer enough to take measures to protect your physical safety and your cash after a transaction at the ATM – now you must be aware of cameras and skimming devices that secretly record (steal) your bank account numbers and PIN numbers. Here are some other tips for safer transactions both Electronic and Personal: Electronic Safety Tips PROTECT YOUR CARD AND PIN Protect your ATM and debit cards as if they were cash. Report lost or stolen cards immediately. Don’t write your Personal Identication Number (PIN) on your card or give the number out to anyone, including friends and family, and do not reveal it to anyone over the phone. Avoid using numbers that are easily identied (birth date, phone number, etc.) with your personal identity. CONDUCT YOUR TRANSACTIONS PRIVATELY Use common courtesy at the ATM. Give people ahead of you space to conduct their transactions. When you use the ATM conduct your business quickly and eciently, make sure no one watches you key in your PIN number. Use your body and free hand to shield the ATM keypad during the transaction. -

CONSUMER DEBIT CARD ATM CARD Look for These Logos at ATM

CONSUMER DEBIT CARD ATM CARD Make purchases plus get cash fast at ATMs Get cash fast at ATMs Applicant Name: New Student _____________________________________________________________ Card Type: Sunset Eagle Your card and PIN will be sent to the address on your account statement. Please speak to an Account Representative for special mailing __________________________________ CHECKING ACCOUNT NUMBER accommodations. (Required for Debit Card __________________________________ Last 4 digits of Applicant’s Social Security Number: ___________________ SECONDARY CHECKING ACCOUNT NUMBER __________________________________ Daytime Phone: Evening or Message Phone: SAVINGS ACCOUNT NUMBER __________________________ __________________________ __________________________________ Reason for new card (lost, damage, etc.) I hereby request that I be issued a First Bank Consumer Debit card or a ATM card and Personal Identification Number for use at merchant locations, point-of-sale terminals (Consumer Debit Card only) and automated teller machines (ATMs) to access my account(s) at First Bank. I understand that I may use my card to access my savings account through an ATM only. I also acknowledge receipt of an Electronic Funds Transfer Disclosure and a Cardholder Agreement, and understand that use of my Consumer Debit Card or ATM card shall governed by the terms and conditions applicable to my account(s), to the terms of the Cardholder Agreement, by laws, rules, regulations or applicable law, and such terms, conditions, and/or amendments as may be established from time to time and communicated to me in writing. ________ As the parent/guardian on this account, I understand that I am responsible for the Please Initial transactions conducted by the minor owner. Applicant’s Signature Date If applicable, Parent Signature Date In order to expedite the processing of your application form, please remember: 1. -

New Debit Card Solutions At

New Debit Card Solutions Debit Mastercard and Visa Debit are ready Swiss Banking Services Forum, 22 May 2019 Philippe Eschenmoser, Head Cards & A2A, Swisskey Ltd Maestro/V PAY Have Established Themselves As the “Key to the Account” – Schemes, However, Are Forcing Market Entry For Successor Products Response from the Maestro and V PAY are successful… …but are not future-capable products schemes # cards Maestro V PAY on Lower earnings potential millions8 for issuers as an alternative payment traffic products (e.g. 6 credit cards, TWINT) Issuer 4 V PAY will be 2 decommissioned by VISA Functional limitations: in 20211 – Visa Debit as 0 • No e-commerce the successor 2000 2018 • No preauthorizations Security and stability have End- • No virtualization proven themselves customer High acceptance in CH and Merchants with an online MasterCard is positioning abroad in Europe offer are demanding an DMC in the medium term online-capable debit as the successor to Standard product with an Merchan product Maestro integrated bank card t 2 1: As of 2021 no new V PAY may be issued TWINT (Still) No Substitute For Debit Cards – Credit Cards With Divergent Market Perception TWINT (still) not alternative for debit Credit cards a no alternative for debit Lacking a bank card Debit function Limited target group (age, ~1.1 M 1 ~10 M. creditworthiness...) Issuer ~48.5 k ~170 k1 No direct account debiting DMC/ Visa Debit Potentially high annual fee End-customer Lower customer penetration Banks and merchants DMC/ P2P demand an online- Higher costs Merchant Visa Debit -

Fraud and Abuse Online: Harmful Practices in Internet Payday Lending the Pew Charitable Trusts Susan K

A report from Oct 2014 Report 4 in the Payday Lending in America series Fraud and Abuse Online: Harmful Practices in Internet Payday Lending The Pew Charitable Trusts Susan K. Urahn, executive vice president Travis Plunkett, senior director Project team Nick Bourke, director Alex Horowitz Walter Lake Tara Roche External reviewers The report benefited from the insights and expertise of the following external reviewers: Mike Mokrzycki, independent survey research expert; Nathalie Martin, Frederick M. Hart chair in consumer and clinical law at the University of New Mexico; and Alan M. White, professor of law at the City University of New York. These experts have found the report’s approach and methodology to be sound. Although they have reviewed the report, neither they nor their organizations necessarily endorse its findings or conclusions. Acknowledgments The small-dollar loans project thanks Pew staff members Steven Abbott, Dan Benderly, Hassan Burke, Jennifer V. Doctors, David Merchant, Bernard Ohanian, Andrew Qualls, Mark Wolff, and Laura Woods for providing valuable feedback on the report, and Sara Flood and Adam Rotmil for design and Web support. Many thanks also to our other former and current colleagues who made this work possible. In addition, we would like to thank the Better Business Bureau for its data and Tom Feltner of the Consumer Federation of America for his comments. Finally, thanks to the small-dollar loan borrowers who participated in our survey and focus groups and to the many people who helped us put those groups together. For further information, please visit: pewtrusts.org/small-loans 2 Cover photo credits: 1 3 1. -

Interbank GIRO Is an Automated Payment Service Which Allows You to Make Monthly Payment to Your ICBC Credit Card Account from Your Designated Bank Account Directly

Interbank GIRO Frequently Asked Questions: 1. What is Interbank GIRO? Interbank GIRO is an automated payment service which allows you to make monthly payment to your ICBC Credit Card account from your designated bank account directly. The amount will be deducted from your designated bank account and paid to ICBC every month. All you need to do is to ensure that the designated bank account has sufficient funds every month. 2. What is the benefit of using Interbank GIRO? Interbank GIRO is a convenient, paperless and cashless payment method. It enables you to make hassle-free monthly payments to ICBC through your designated bank account. There are also no fees charged for the setup. 3. Are there any additional charges for signing up for Interbank GIRO? There are no fees charged for the setup of Interbank GIRO. 4. How can I apply for Interbank GIRO? Simply fill up the Interbank GIRO form, and submit to Credit Card Department. 5. Which banks can I use for Interbank GIRO? You can use any bank that supports Interbank GIRO. 6. How long is the Interbank GIRO application Processing Time? Interbank GIRO applications may take up to 60 days to process, including the processing time required by the deducting bank. We will notify you of your application status as soon as possible. 7. How do I submit the Interbank GIRO form to ICBC Credit Card Department? You can mail the duly signed Original Interbank GIRO form to ICBC Credit Card Department by using the Business Reply Service Envelope attached. Please do not fax the Interbank GIRO form or email the scanned copy of the Interbank GIRO form as the designated bank requires the original signature for verification. -

Impact of Automated Teller Machine on Customer Satisfaction

Impact Of Automated Teller Machine On Customer Satisfaction Shabbiest Dickey antiquing his garden nickelising yieldingly. Diesel-hydraulic Gustave trokes indigently, he publicizes his Joleen very sensuously. Neglected Ambrose equipoising: he unfeudalized his legionnaire capriciously and justly. For the recent years it is concluded that most customers who requested for a cheque book and most of the time bank managers told them to use the facility of ATM card. However, ATM fees have achievable to discourage utilization of ATMs among customers who identify such fees charged per transaction as widespread over a period of commonplace ATM usage. ATM Services: Dilijones et. All these potential correlation matrix analysis aids in every nigerian banks likewise opened their impacts on information can download to mitigate this problem in. The research study shows the city of customer satisfaction. If meaningful goals, satisfaction impact of on automated customer loyalty redemption, the higher than only? The impact on a positive and customer expectations for further stated that attracted to identify and on impact automated teller machine fell significantly contributes to. ATM service quality that positively and significantly contributes toward customer satisfaction. The form was guided the globe have influences on impact automated customer of satisfaction is under the consumers, dissonance theory explains how can enhance bank account automatically closed. These are cheque drawn by the drawer would not yet presented for radio by the bearer. In other words, ATM cards cannot be used at merchants that time accept credit cards. What surprise the challenges faced in flight use of ATM in Stanbic bank Mbarara branch? Myanmar is largely a cashbased economy. -

When Are KYC Requirements Likely to Become Constraints on Financial Inclusion?

Identifying and Verifying Customers: When are KYC Requirements Likely to Become Constraints on Financial Inclusion? Alan Gelb and Diego Castrillon Abstract Onerous KYC documentation requirements are widely recognized as a potential constraint to full financial inclusion. However, it is sometimes difficult to judge the extent to which this constraint is a serious or binding one, relative to the many other factors that can limit access to finance or demand for financial services. The paper considers this question, distinguishing between different types of documentation and different financial market segments according to their KYC requirements. Using data from several sources it then looks at cross-country patterns which provide some suggestive evidence on the conditions under which particular requirements are more or less likely to pose serious constraints. It concludes with policy suggestions, including on the use of technology to help ease the burden of documentary requirements while still maintaining financial integrity. Keywords: documentation, identification, financial inclusion, KYC JEL: G210, G230, G280, L510, O160, O310, O500 Working Paper 522 December 2019 www.cgdev.org Identifying and Verifying Customers: When are KYC Requirements Likely to Become Constraints on Financial Inclusion? Alan Gelb Center for Global Development Diego Castrillon Center for Global Development We gratefully acknowledge very helpful comments from Mike Pisa, Liliana Rojas-Suarez, Albert van der Linden, Masiiwa Rusare and an anonymous referee. We also thank the GSMA for permission to use graphics from their studies. The Center for Global Development is grateful for contributions from the Bill & Melinda Gates Foundation in support of this work. Alan Gelb and Diego Castrillon, 2019. -

A Quick Guide for Consumers on Credit, Debit, and Prepaid Cards

A Quick Guide for Consumers on Credit, Debit, and Prepaid Cards Credit Cards Debit Cards Prepaid Cards A credit card is a loan. A debit card is linked to your bank account There are a variety of prepaid cards, including and is issued by your bank. "general purpose reloadable" (GPR) cards which carry a brand of a card network (such as Visa or MasterCard) and can be used where What it is that brand is accepted. Payroll cards and gift cards are two other types of prepaid cards. When you borrow funds using a credit card, When you use a debit card, the money Prepaid cards, which generally allow you must pay the money back. You may spent is taken directly from your bank consumers to spend only the money deposited also have to pay interest if not paid in full. account. Debit cards may be especially onto them, can have a number of different Credit cards may be especially useful if you useful for small and routine purchases, but features. For instance, some gift cards may be want to pay for things when your bank they are considered less beneficial than used only at a single merchant; most GPR How it Works account balance is low or to take credit cards for major purchases or buying cards may be used to pay for purchases and advantage of a no-interest introductory items online because of the more limited access cash at ATMs. period. protections in cases of unauthorized transactions or disputes. Consumer Protections Available Your liability for losses is limited to a The maximum liability is $50 if you notify the Liability depends on the type of funds on the maximum of $50 if your credit card is lost or bank within two business days after card.